Summary:

- LCID has missed its own production/ delivery estimates again, based on the FQ1’23 annualized numbers.

- Depending on the volatile macroeconomic environment and auto loan default rates, we may see the stock further retest its support levels ahead.

- Combined with the potential recession by H2’23 and recovery only by 2025, we reckon LCID’s execution may remain challenged, worsening its cash burn.

Feverpitched

The Recession May Impact LCID’s Execution

With the Fed already predicting a mild recession in H2’23 and recovery only by 2025, Lucid’s (NASDAQ:LCID) intermediate-term prospects were made even more uncertain due to the intensifying EV price war.

All Tesla’s (NASDAQ:TSLA) models were further discounted as an effort to boost sales at a time of expanding manufacturing capacity and tightening discretionary spending, nearing -11% YTD for Model 3 and -20% for Model Y. Notably, the automaker also slashed prices for the Model S and Model X by over -$3K, potentially triggering further headwinds for LCID.

With LCID’s entry model offerings priced from $87K onwards, way above the average EV prices of $61.48K in 2022, and the market leader, TSLA’s Model 3 at $41.99K, it was unsurprising that some consumers had considered canceling their backorders, one which had been made relatively difficult since late 2022.

One key difference between LCID and TSLA was that the latter could naturally afford the price cuts, due to its highly profitable EBIT margins of 11.4% in FQ1’23 (-4.6 points QoQ and -7.8 YoY). This feat was admirable even by ICE standards, such as Ford Blue’s (NYSE:F) EBIT margin of 7.2% (+3.1 points YoY) and General Motors’ (NYSE:GM) overall EBIT margins of 9.2% (-2.1 points YoY) in FY2022.

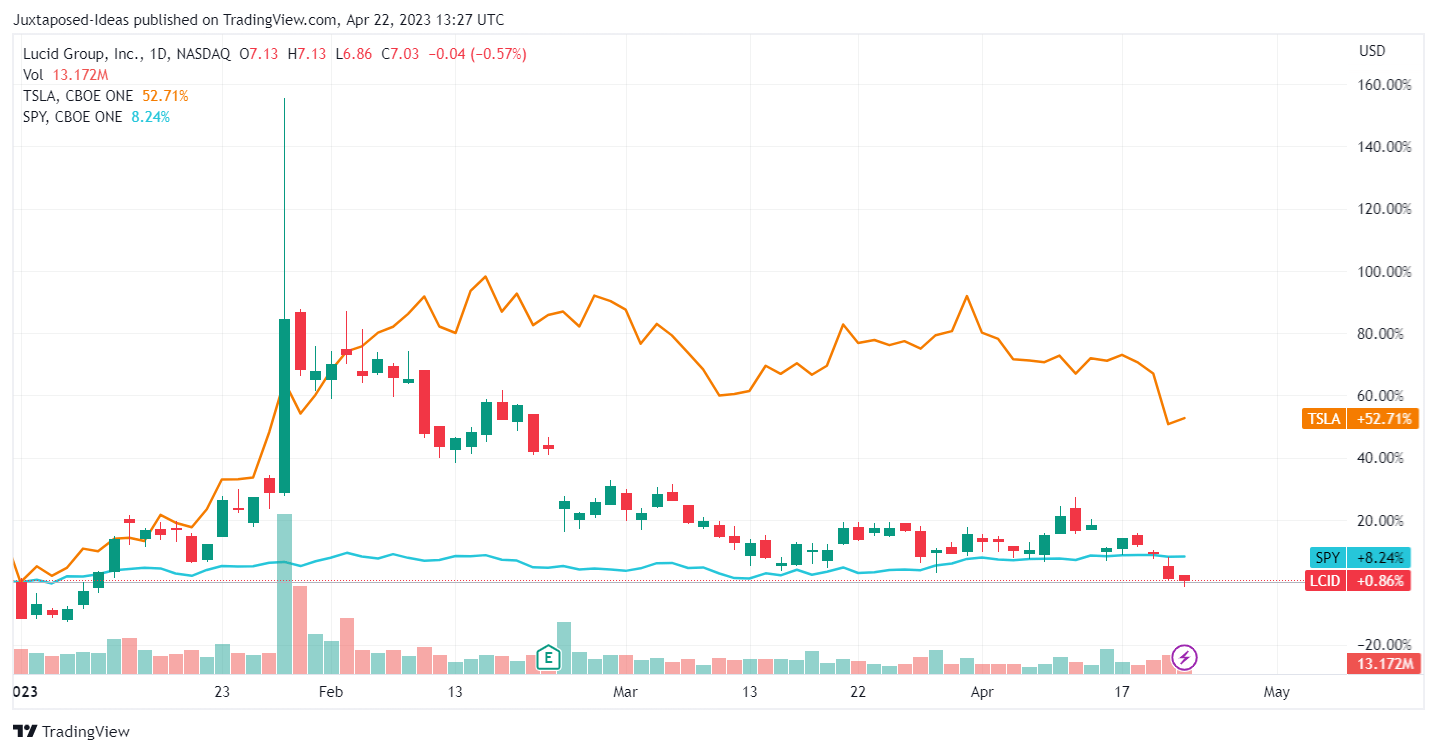

LCID & TSLA YTD Stock Price

Trading View

With LCID still losing money on every vehicle it delivered, at gross margins of -138.8% and EBIT margins of -290.9% by the latest quarter, it was no wonder that the stock had underperformed at +0.86% YTD against the market leader at +52.71% and SPY at +8.24%.

The automaker had further shot itself in the foot, by failing to ramp up its production output as per previous guidance of up to 14K vehicles in 2023 (+94.9% YoY). Based on its guidance, investors were possibly projecting a quarterly output of 3.5K vehicles (in line QoQ).

However, those hopes had been dashed, with LCID reporting Q1’23 production of 2.31K vehicles (-33.8% QoQ) and delivery of 1.4K (-27.4% QoQ). Based on those numbers, we were looking at an annualized production output of only 9.24K vehicles, missing even the lowest range estimate of 10K in 2023.

In addition, if we were to look closer at the automaker’s FY2022 and FQ1’23 numbers, one might guess a rising number of vehicles sitting around undelivered. For example, it produced 7.18K of vehicles while only 4.36K were delivered, suggesting a 2.82K excess in FY2022. The same was observed for its FQ1’23 numbers, with an 0.91K excess.

Therefore, we reckon that LCID’s upcoming earnings call may bring about a growing inventory value, expanding beyond FQ4’22 numbers of $834.4M (+21.7% QoQ and +555.7% YoY).

Then again, we must also highlight that the management had guided that FQ1’23 deliveries might underperform, due to the “strategic decision to moderate some production as they transition to buildable configuration.” Therefore, we may see its delivery numbers improve over time, culminating in the peak volume by FQ4’22, attributed to the activation of Phase 2 production ramp-up from FQ3’22 onwards.

Furthermore, in response to the uncertain macroeconomic outlook and potential deceleration in demand, LCID had already delayed part of its capital expenditures through 2024. For 2023, it had guided a capex of between $1.5B and $1.75B, compared to FY2022 levels of $1.1B and previous 2023 guidance of $2B.

This was on top of the headcount reduction by 1.29K or 18%, which market analysts expected to save up to $100M in annualized expenses, compared to the $1.55B (+10.7% YoY) of operating expenses reported in FY2022.

Nonetheless, even with an annualized cash burn of $1.45B, LCID may need to raise more cash by 2024, due to the dwindling cash/ equivalents of $3.91B by the latest quarter (-37.5% YoY). Unfortunately, we reckon a capital raise may be challenging at the moment, attributed to the recent banking crisis that stemmed from the SVB collapse.

The peak recessionary fears and the Fed’s continuous hikes had partly contributed to the pessimistic market sentiments, drying up venture capitalist funding to $65.9B in FQ4’22 (-64% YoY), returning to pre-pandemic levels. As similarly witnessed with LCID, many unprofitable startups had rapidly drawn down their deposits with SVB, triggering cash flow issues for the bank.

As a result of the funding tightness, we reckon LCID may rely on Saudi Arabia’s Public Investment Fund again, with the latter expanding its stake beyond 60.61% as of December 22, 2022. However, while the PIF may have immense funds, it is uncertain how long this lifeline may last with the potential demand destruction, especially given TSLA’s and legacy automakers’ aggressive price cuts thus far.

The auto loan market appeared tight as well, with the number of outstanding auto loans and delinquency rates (past 90+ days) for the age 30 to 49 group drastically rising to 52% and 4.9% by December 2022, nearing LCID’s audience demographics of between 25 to 44 years old.

This might be attributed to the tremendous increase in the average auto loan value to $24K by December 2022, expanding by +41% from 2019 levels of $17K. Given the rising inflationary pressures and elevated interest rate environment, we might see more defaults ahead, triggering further headwinds to the automaker’s premium strategy.

Combined with the fact that LCID opted not to compete in the mid-priced mass market segment, we remain uncertain about its prospects through 2024, if not 2023. Due to its hefty price tag, we will not be surprised if more order cancellations occur moving forward, triggering further headwinds to its delivery cadence as more consumers are lured away by discounted options.

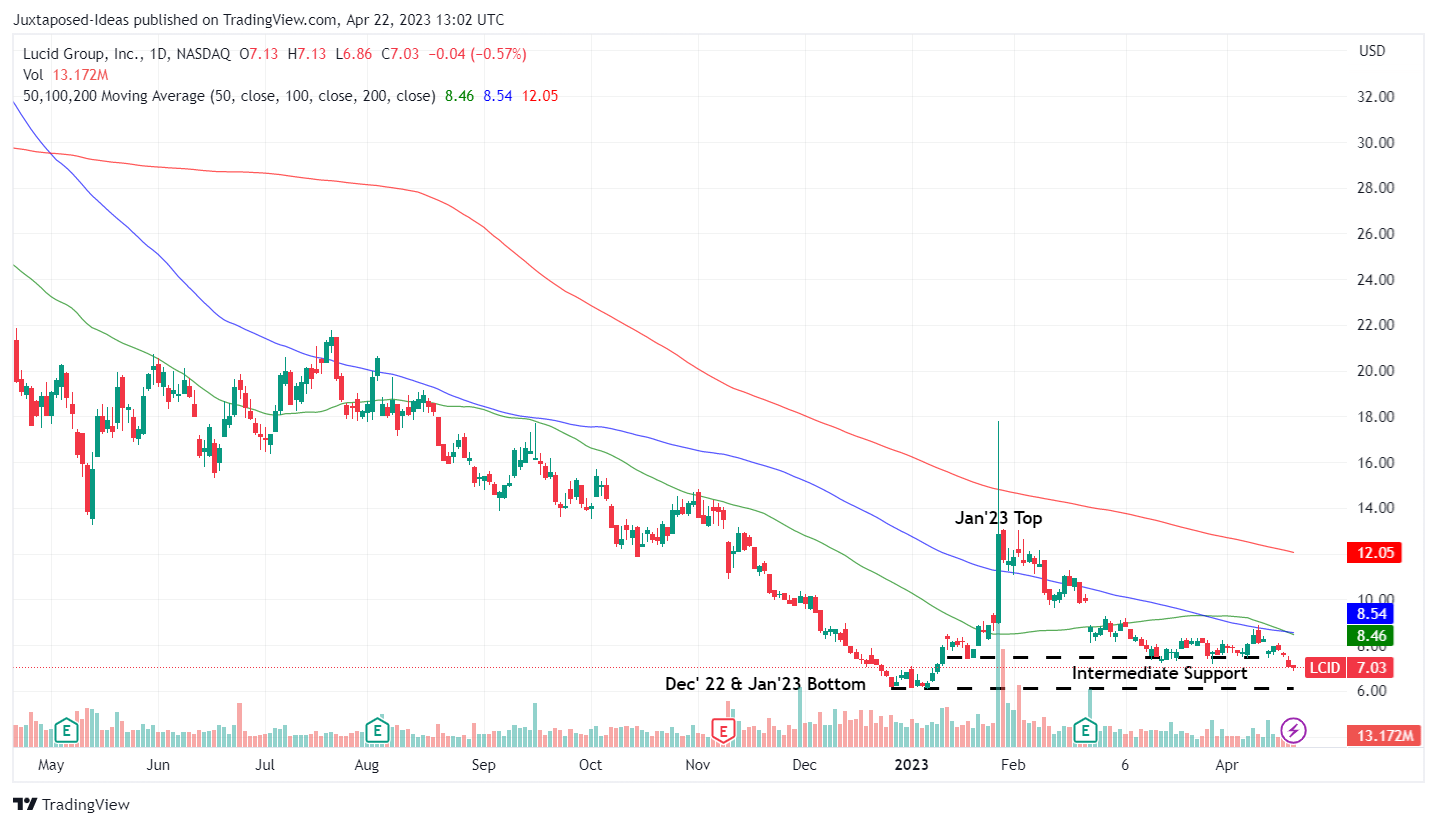

LCID 1Y Stock

Trading View

With the LCID stock already breaching through its intermediate support of $7.50s, we reckon the stock may potentially retest its previous January 2023 bottom of $6.20 in the near term, further worsened by the elevated short interest of 22.63% at the time of writing.

Furthermore, assuming that the tightened discretionary spending continues over the next few quarters, the automaker may potentially miss delivery estimates, affecting its financial performance while accelerating its cash burn ahead. These events may trigger further downward pressure on the stock, potentially charting new lows ahead.

As a result, we do not recommend anyone to add the LCID stock here, due to the potential volatility.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.