Despite a holiday-shortened week, earnings season rolls on with another eventful slate ahead, as a diverse mix of consumer, energy, technology, healthcare, financial, and materials companies step into the spotlight.

The lineup spans defensive bellwethers and cyclical plays alongside growth-oriented disruptors, offering a broad snapshot of demand trends, margins, and capital allocation across the economy.

Retail and consumer activity will be gauged through results from Walmart (WMT), Booking Holdings (BKNG), DoorDash (DASH), Etsy (ETSY), eBay (EBAY), Carvana (CVNA), Wayfair (W), and Opendoor Technologies (OPEN). Energy and materials updates from Occidental Petroleum (OXY), Energy Transfer (ET), Devon Energy (DVN), Transocean (RIG), Newmont (NEM), Pan American Silver (PAAS), Kinross Gold (KGC), and Nutrien (NTR) will shed light on commodity pricing, volumes, and capital discipline.

Technology and industrial signals will come from Palo Alto Networks (PANW), Analog Devices (ADI), SolarEdge Technologies (SEDG), Dropbox (DBX), Deere (DE), and Medtronic (MDT), while Southern Company (SO) and Expand Energy (EXE) add insight into utilities and infrastructure-linked demand.

Financial and insurance-focused names such as Blue Owl Capital (OWL) and Lemonade (LMND) round out the week.

Below is a rundown of major quarterly updates anticipated in the week of February 16 to February 20:

Monday, February 16

The U.S. stock market closed in observance of the President’s Day holiday.

Tuesday, February 17

Palo Alto Networks (PANW)

Palo Alto Networks (PANW) is scheduled to report FQ2 results after Tuesday’s close, with analysts forecasting ~14%–16% Y/Y growth in both revenue and earnings.

The cybersecurity major has been in focus following the completion of its $25B acquisition of CyberArk, under which CyberArk shareholders received $45 in cash plus 2.2005 PANW shares per CyberArk share. Palo Alto also announced plans to dual list on the Tel Aviv Stock Exchange, reinforcing its strategic ties to Israel’s cybersecurity ecosystem.

Wall Street maintains a Buy rating on the stock, while Seeking Alpha’s Quant Rating stands at Hold.

SA contributor Star Investments highlights PANW’s long-term transformation from a hardware-centric firewall vendor into a cloud-based, platform-driven security provider. However, recent acquisitions, including CyberArk and Chronosphere, introduce execution and integration risks, even as the long-term thesis remains intact for patient investors.

On the more cautious side, SA author Bay Area Ideas rates the stock a Sell, pointing to premium valuation and signs of slowing momentum. While Q1 FY26 delivered solid 16% Y/Y revenue growth and strong profitability, next-generation ARR growth decelerated to 29% from 32%. Management’s guidance for Q2 and FY26 implies further slowing across revenue, RPO, and next-gen ARR, raising concerns about near-term demand. Additional headwinds include DRAM pricing pressures and China-related restrictions, with U.S. government tailwinds viewed as more medium- to long-term.

- Consensus EPS Estimates: $0.94

- Consensus Revenue Estimates: $2.58B

- Earnings Insight: The company has beaten EPS and revenue expectations in 8 straight quarters.

Also reporting: Energy Transfer LP (ET), Medtronic (MDT), Devon Energy (DVN), Hecla Mining (HL), Genuine Parts (GPC), Sunoco (SUN), EQT (EQT), Caesars Entertainment (CZR), Cadence Design Systems (CDNS), FirstEnergy (FE), Kenvue (KVUE), Nano Nuclear Energy (NNE), Expand Energy (EXE), and more.

Wednesday, February 18

Occidental Petroleum (OXY)

Occidental Petroleum (OXY) is set to report Q4 results after Wednesday’s close, with analysts forecasting a sharp 72% Y/Y decline in earnings alongside an 18% drop in revenue, reflecting weaker oil prices and compressed margins.

Seeking Alpha’s Quant Rating holds the stock at Hold, broadly aligning with sell-side caution around near-term growth.

However, views diverge among SA contributors. Investing Group Leader Long Player, who rates the stock as a Strong Buy, sees OXY as a compelling contrarian opportunity, noting the stock now trades below Warren Buffett’s average purchase levels. The bull case rests on OXY’s investment-grade balance sheet, recent acquisitions that could drive profitability in the next commodity upcycle, and resilience during cyclical downturns, with greater upside expected when energy prices recover.

On the more cautious side, Investing Group Leader Stone Fox Capital maintains a Hold, arguing OXY trades at a sector premium despite falling toward $40, supported largely by the perceived “Buffett put.” Earnings remain under pressure, with the stock trading at ~30x 2026 EPS and free cash flow yields trailing peers such as Devon Energy. While the $9.7B OxyChem sale to Berkshire Hathaway strengthens liquidity and supports debt reduction, it does not fully offset lower forward earnings, leaving valuation and leverage as key overhangs.

- Consensus EPS Estimates: $0.22

- Consensus Revenue Estimates: $5.59B

- Earnings Insight: The company has beaten EPS expectations in 8 straight quarters and revenue in just 50% of those reports.

Also reporting: Nutrien (NTR), eBay (EBAY), Fiverr International (FVRR), Bausch Health Companies (BHC), Booking Holdings (BKNG), SolarEdge Technologies (SEDG), Macerich Company (MAC), Analog Devices (ADI), Kinross Gold (KGC), IAMGOLD (IAG) Pan American Silver (PAAS), Teck Resources Limited (TECK), DoorDash (DASH), and more.

Thursday, February 19

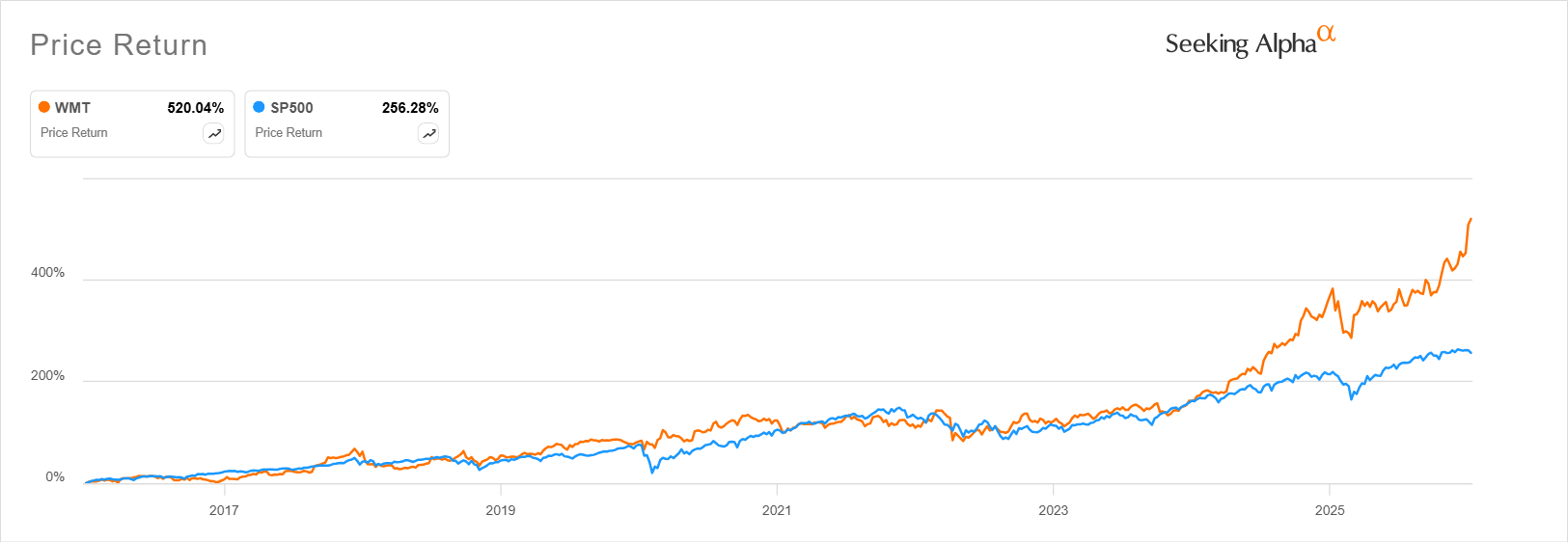

Walmart (WMT)

Walmart (WMT) is set to report Q4 earnings before Thursday’s open in one of the most closely watched releases of the week. Analysts are forecasting 10%+ Y/Y growth in earnings on ~5% revenue growth, underscoring continued margin resilience despite a moderating consumer backdrop.

The stock has climbed ~20% YTD and nearly 30% over the past year, pushing Walmart into the $1T+ market cap club.

Sell-side analysts maintain a Strong Buy consensus, pointing to Walmart’s unmatched scale, pricing power, market share gains, and steady progress in omnichannel and e-commerce.

That optimism contrasts with Seeking Alpha’s Quant Rating of Hold, reflecting valuation concerns.

Several SA contributors are more cautious. Stuart Allsopp rates the stock a Strong Sell, arguing the rally, fueled by the Google Gemini partnership and Nasdaq 100 inclusion, has pushed valuation to extremes, with WMT now trading near 46x earnings and 60x+ free cash flow, despite limited real sales growth over the past five years. He also flags execution risks tied to higher costs, potential brand dilution, and pressure on retail media economics.

Similarly, Cash Flow Venue maintains a Strong Sell, noting Walmart’s exceptional long-term performance (~520% total return over the past decade, far outpacing the S&P 500), but argues fundamentals no longer justify the premium. While recent results showed solid execution, including ~6% revenue growth, 27% e-commerce growth, and margin improvement, WMT now trades at valuation multiples exceeding peers such as Amazon, Alphabet, Meta, and even Nvidia, raising the risk of multiple compression if growth remains in the mid-single digits.

- Consensus EPS Estimates: $0.72

- Consensus Revenue Estimates: $188.46B

- Earnings Insight: Walmart has exceeded EPS in 7 of the past 8 quarters and revenue expectations in 6 of those reports.

Also reporting: Newmont Mining (NEM), Etsy (ETSY), Southern Company (SO), Deere & Company (DE), Transocean (RIG), Lemonade (LMND), Dropbox (DBX), Consolidated Edison (ED), First Majestic Silver (AG), Opendoor Technologies (OPEN), Appian (APPN), Wayfair (W), Universal Display (OLED), Akamai Technologies (AKAM), and more.

Friday, February 20

The week wraps up on a lighter note, with only a handful of earnings scheduled for Friday’s pre-market session. Notable names include PPL Corporation (PPL), AdvanSix (ASIX), AngloGold Ashanti (AU), Western Union (WU), HudBay Minerals (HBM), Lamar Advertising (LAMR), Cogent Communications (CCOI), and Portland General Electric (POR).