On the back of a wild rally in 2023, Tesla’s stock is once again trading at a significant premium to its big tech peers.

While the near-term business outlook remains uncertain, Tesla’s long-term future looks brighter than ever.

In this note, we will review near-term and long-term risk-reward for TSLA to see if it is a buy, sell, or hold at current levels.

Justin Sullivan

Introduction

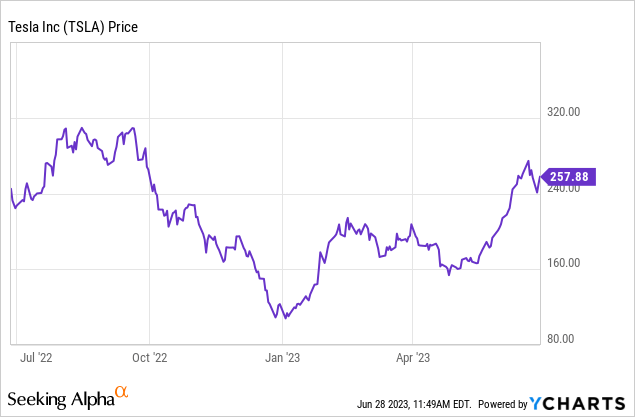

After hitting a capitulatory bottom in early 2023, Tesla, Inc. (NASDAQ:TSLA) stock has rocketed up by more than +150% despite repeated warnings from Elon Musk [Tesla’s CEO] on the state of the economy. While the near-term business outlook for Tesla remains uncertain due to the macroeconomic environment, investors have seemingly turned optimistic on the stock based on Musk’s bullish long-term outlook and hyperbolic statements on Tesla’s ambitious projects such as FSD [self-driving generalized AI], Cybertruck, Optimus Humanoid Bot, Dojo AI chips, and more:

In recent weeks, Tesla’s stock has been bid up higher like there’s no tomorrow, with a series of partnership announcements projecting Tesla’s NACS (North American Charging Standard) as the industry standard for EV charging in the US. Major automakers like Ford (F), General Motors (GM), and Volvo are adopting NACS, which will enable their customers to utilize Tesla’s supercharger network. While Tesla’s supercharger network is only a small piece of the EV giant’s business right now, NACS becoming the industry standard is a massive win for the company. According to Goldman Sachs (GS) estimates, Tesla could rake in more than $25B per year in revenue from its supercharger network business in the long run if it were to open up this asset to other EV makers.

Mr. Market is clearly getting enthusiastic about Tesla, and I am quite happy about Tesla emerging as the industry standard for EV charging. In late-2022/early-2023, I was incredibly bullish on Tesla in the mid to low $100s, at a time when the market was selling it off like a drunken sailor:

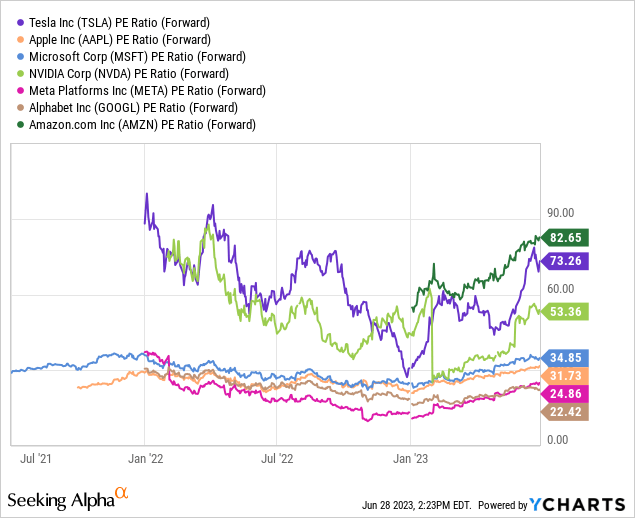

Tesla’s valuation has moderated significantly over the last twelve months, so much so that one could argue reasonably that Tesla is a value stock at this point. From a long-term standpoint, strong business fundamentals and reasonable valuation make Tesla a lucrative investment idea at current levels.

Despite near-term downside risk, Tesla is a high-quality business that I want to own for the long haul. And I will continue to accumulate more shares slowly in the upcoming weeks and months.

Key Takeaway: I rate Tesla a “Strong Buy” in the low $100s, with a strong preference for staggered accumulation over 6-12 months.

However, as you may know, I downgraded TSLA stock to a “Neutral/Hold” rating after the release of its Q1 earnings report in April. My altered stance was based on greater macroeconomic uncertainties, dangers of Tesla’s recession playbook [making it a binary bet on FSD], and ominous technical setup.

Based on its forward P/E multiple, Tesla is still 15-20% under its valuation from January 2022 [the height of the liquidity bubble of 2020-21]. However, after having gotten to a valuation in-line with its big tech peers in early 2023, Tesla once again commands a hefty premium.

While Tesla bulls may argue that TSLA deserves a premium due to faster growth at the EV giant and potential FSD-driven margin expansion, bears would contend that Tesla is a CAPEX-intensive manufacturing business with far lower profit margins compared to other big tech companies. In my view, both bulls and bears have a defensible argument.

So, is Tesla a “Sell” at current levels, or is it still a good long-term investment?

To answer this question, we will be reviewing near-term and long-term risk-reward for TSLA. First, we shall look at analyst targets & estimates, business trends, technical charts, and quant factor grades to assess Tesla’s near-term risk-reward. And then, we will analyze TSLA’s absolute valuation to assess its long-term risk-reward. Without further ado, let’s dive right in!

What Is The Short-Term Prediction For TSLA?

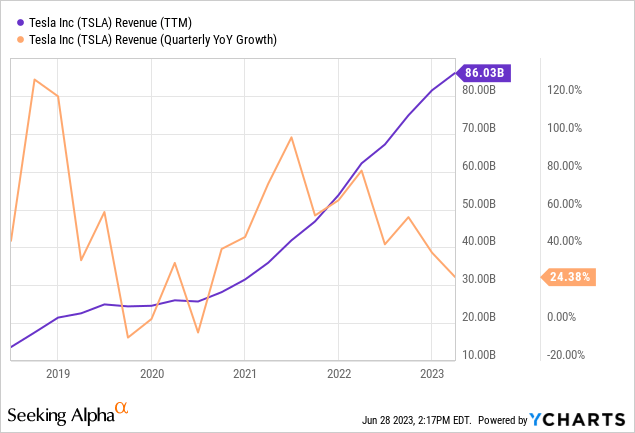

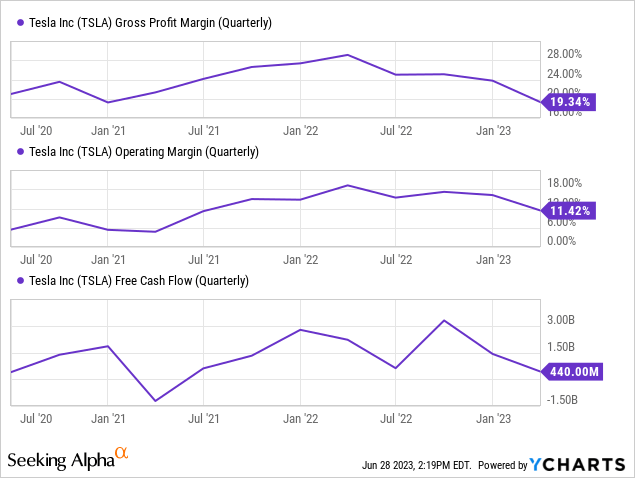

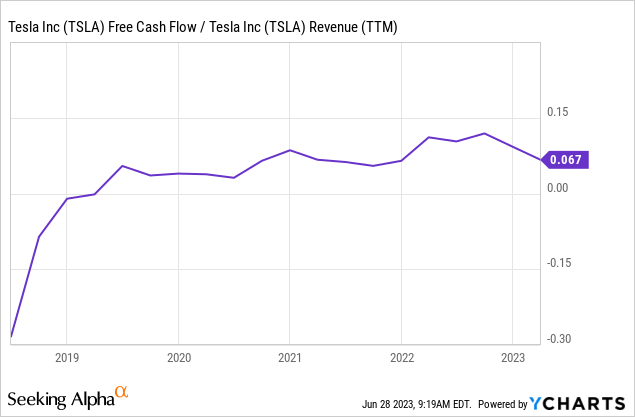

Tesla is accelerating the world’s transition to sustainable energy; however, this growth story is hitting a snag of sorts, with auto demand showing signs of cracking under the pressure of FED’s aggressive monetary policy. Over the last few quarters, Tesla’s revenue growth rates have been decelerating sharply, and management has responded to demand challenges with a flurry of price cuts to hit volume targets. The resultant effect of Tesla’s dangerous recessionary playbook is quite evident from its margin trends. In Q1 2023, Tesla’s operating margin fell to 11.4%, and free cash flows sunk to just $440M. While Tesla’s sales growth is looking fine, the cost of doing so is hurting profitability to a great extent.

Given Tesla’s balance sheet strength and the monetization potential of FSD, I think Musk & Co. would likely continue to sacrifice margins in order to maintain unit volumes. However, the longer this strategy is in place, the investment thesis’ reliance on FSD achieving full autonomy keeps climbing. And while Tesla may solve FSD, I do not like to invest in binary bets as a long-term-oriented investor.

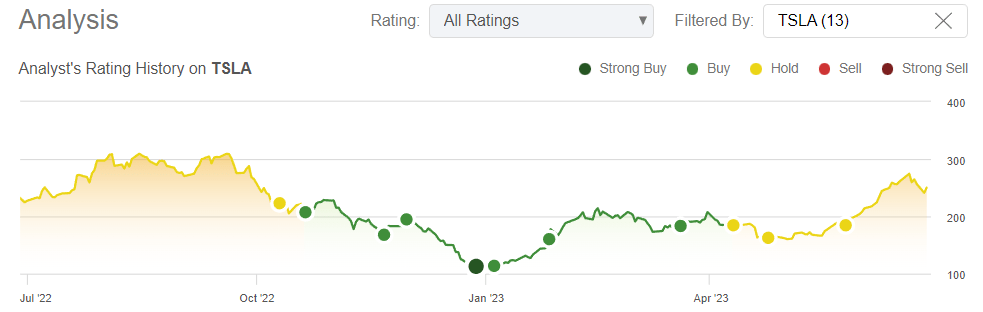

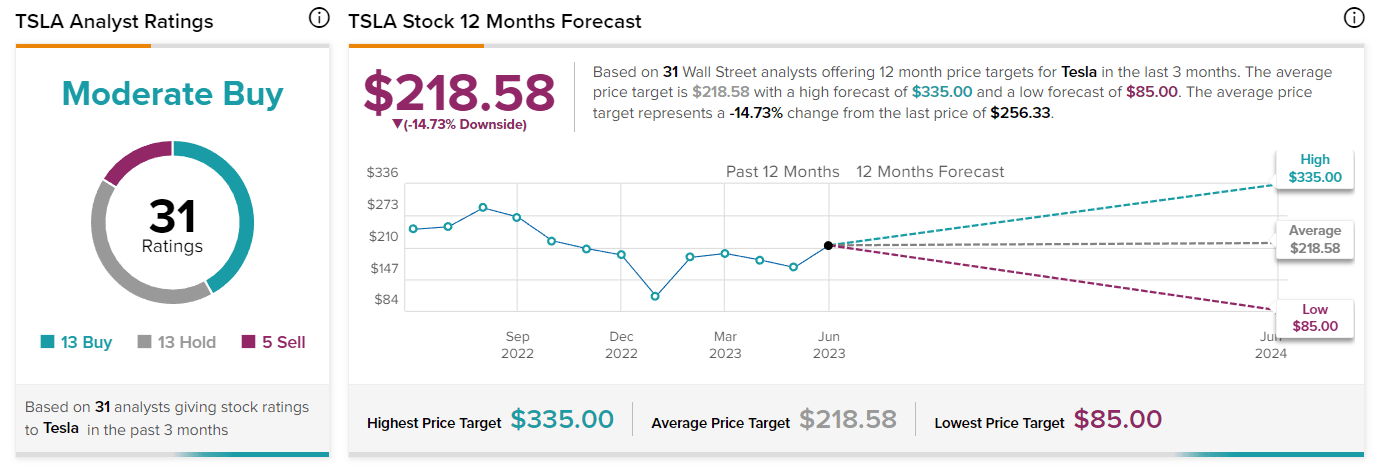

After rallying by +150% year-to-date in 2023, Tesla seems to have regained its darling status among retail and institutional investors. However, multiple Wall Street analysts have downgraded Tesla in recent weeks. And the overall analyst ratings for Tesla are quite mixed. Out of 31 analysts covering the stock, 13 analysts rate it a “Buy”, 13 analysts rate it a “Hold”, and 5 analysts rate it a “Sell”.

Tesla Analyst Forecast (TipRanks)

Despite having a wide forecasted range of $85-335, Tesla’s consensus 12-month price target sits at $218.58, which implies a downside of ~15% from current levels.

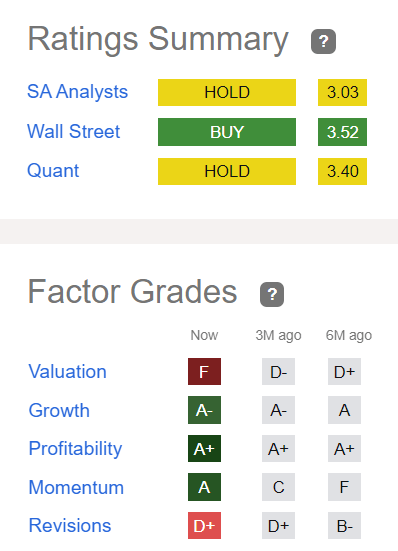

As of writing, Wall Street has a neutral stance on Tesla, and my fellow SA analysts share this view too. Furthermore, TSLA is rated a “HOLD” based on its SA Quant rating score of 3.40/5.

Tesla Quant Rating (SeekingAlpha)

While Tesla’s [technical] “Momentum (F to A)” grade has improved significantly over the last six months, its “Valuation (D+ to F)”, “Growth (A to A-)”, and “Revisions (B- to D+)” grades have deteriorated. And while Tesla’s “Profitability” grade has held up under this relative grading system, we know that Tesla’s profitability has degraded significantly in recent quarters. Hence, I believe Tesla’s quant factor grades are not ideal and will get weaker soon. Hence, from a quant factor grade perspective, Tesla is definitely not a buy.

In my previous note in May, I said the following about Tesla’s technical chart:

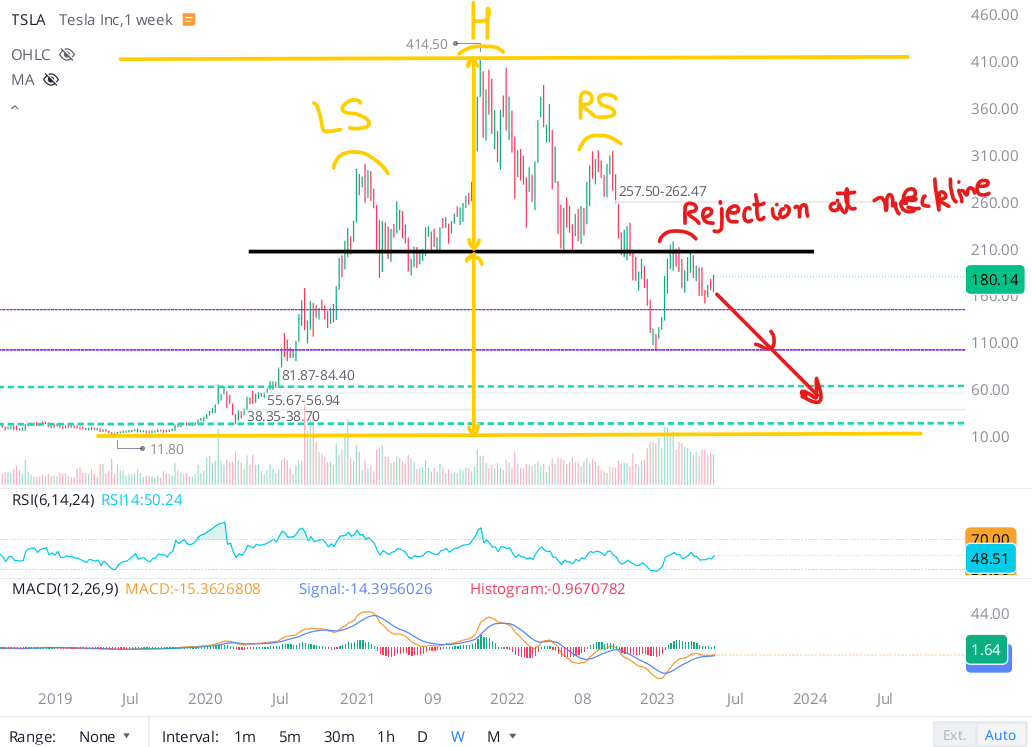

Despite Elon Musk’s dire warnings on the economy, investors have been piling into TSLA stock, which apparently looks set to re-test the neckline of its head and shoulders pattern. As you can observe in the chart below, Tesla’s stock has already been rejected twice at this key technical level.

If Tesla fails to break past this area of resistance, technically, the stock could be headed back down to the mid $100s [and even to the low $100s] in a continuation of the reverse gamma squeeze we saw in late-2022.

WeBull Desktop

In my view, another rejection from the neckline would be extremely bearish for the stock. From a technical perspective, a breakdown of an H&S formation could result in a downward move equivalent to the gap between the head and the neckline. In Tesla’s case, that level falls in the range of $40-60 (based on how you draw the neckline [horizontal or slanted]).

Now, I am not saying Tesla, Inc. stock is headed down to the mid-double digits; however, technicals suggest that this is a possible outcome. From a valuation perspective, Tesla can trade at such levels if it loses growth in a dire economy and the stock gets priced like a traditional automaker (~5-10x earnings). Hence, it is not unrealistic.

WeBull Desktop

While I don’t think Tesla should be valued like a traditional automaker, I wouldn’t rule it out, as Mr. Market can do crazy things. That said, I would view such a sharp selloff as a massive buying opportunity. Now, such a move is very unlikely to materialize until and unless we end up in a deep recession, which is certainly not my base case right now.

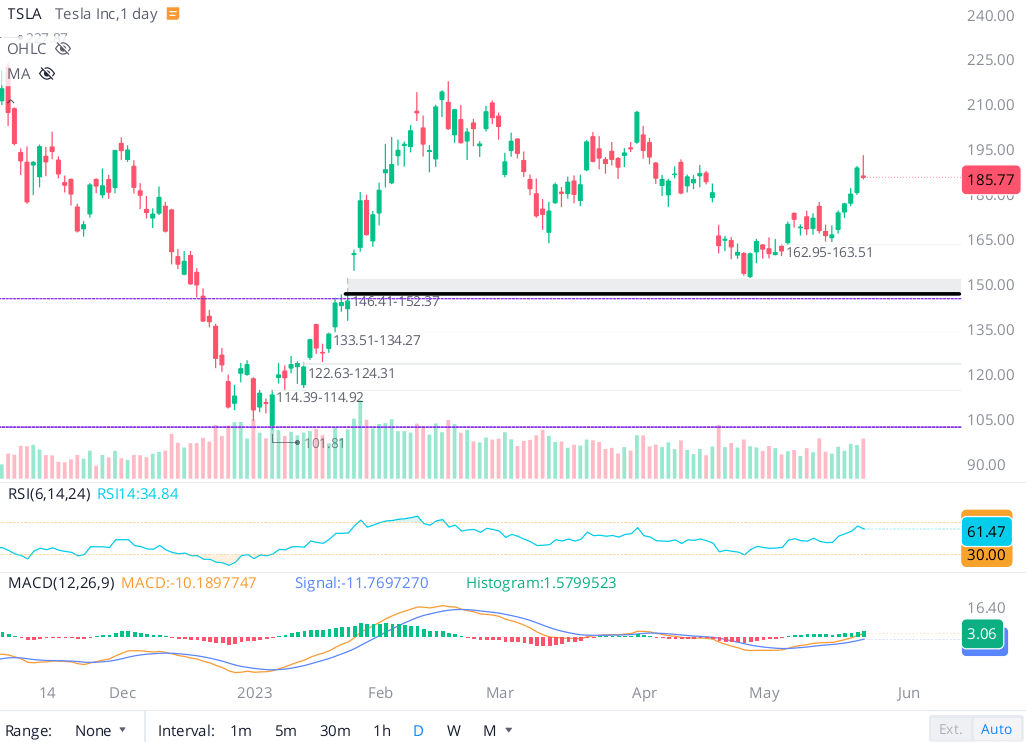

In the short term, I think a move down to $145 is very much on the table, given we still haven’t filled the gap there. And if Tesla fails to hold that level, I can even see a re-test of recent lows, i.e., the low $100s.

WeBull Desktop

In a nutshell, Tesla’s technical chart is looking ominous. A breakout of the neckline at $215 would make me change my view here. However, for the time being, I think investors can afford to remain patient with Tesla, Inc. stock and wait for a better entry point. If Tesla gets down to the mid-$100s, I will resume accumulation via a DCA plan.

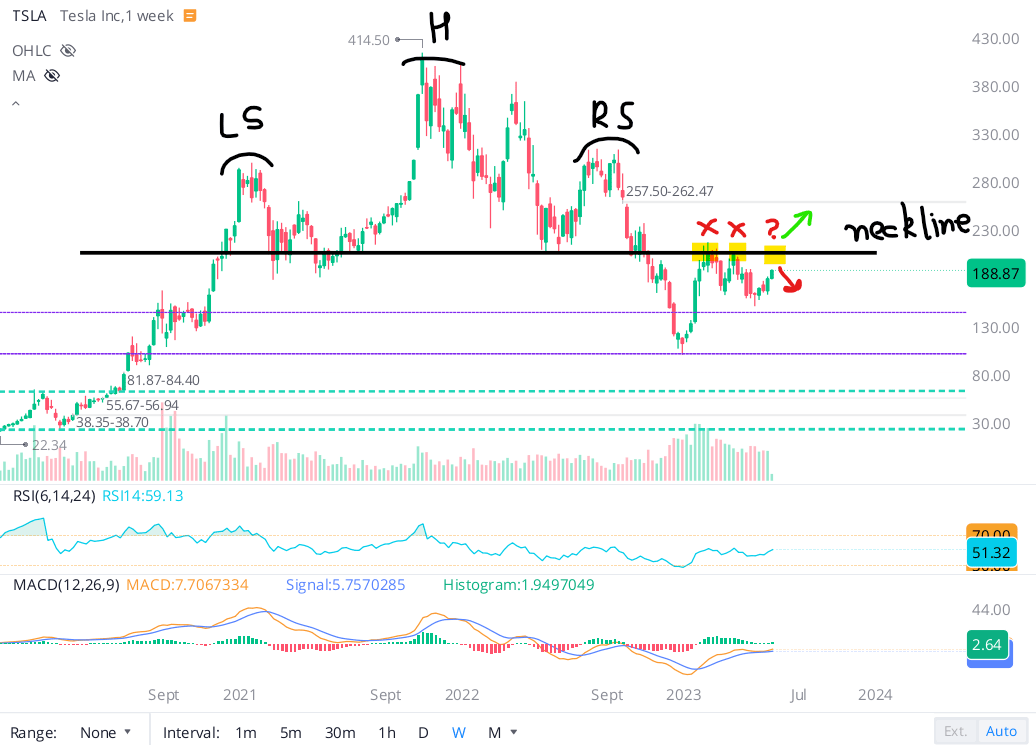

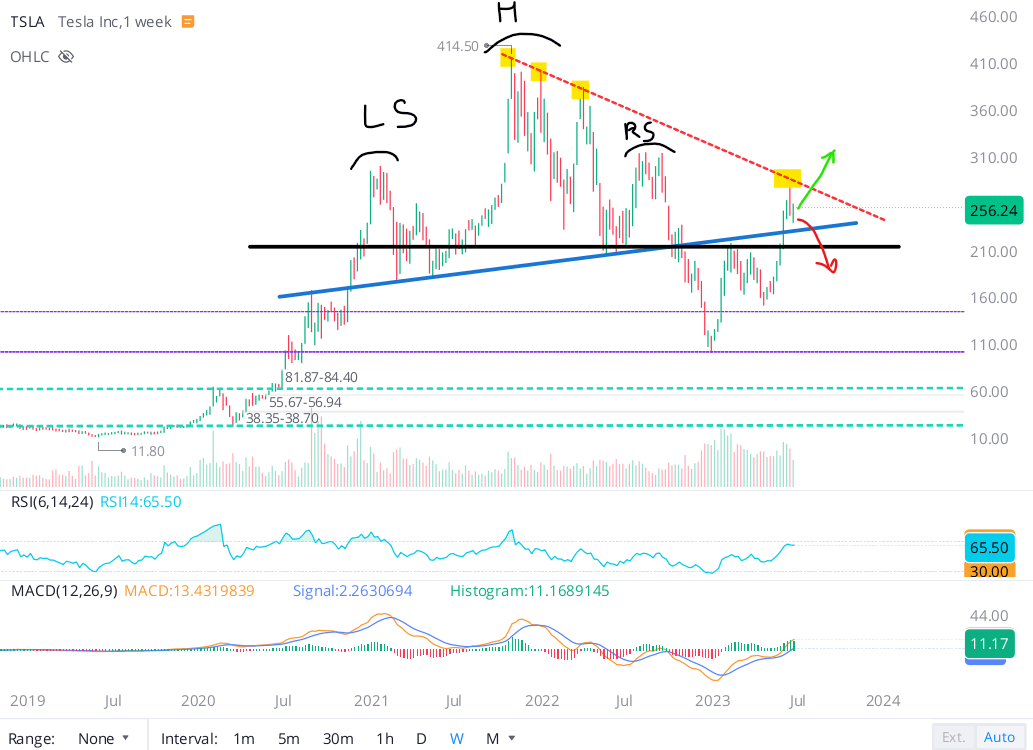

Since then, Tesla broke out to the upside above that key head-and-shoulders neckline level of $215 and rallied up to ~$280 before pulling back down to the $250s where it sits right now.

WeBull Desktop

While it is getting close, Tesla’s stock is not quite in overbought territory, with an RSI of 65. As long as TSLA trades above the straight [black] and slanted [blue] necklines of the H&S pattern, I hold a constructive [bullish] view on Tesla’s technical chart. For a continuation of the rally, I would like to see a bullish breakout above recent highs at ~$280, which is also the bearish trendline [red dotted line] that connects previous local tops.

At this moment in time, I am not sure if Tesla’s breakout is real or if it is a bull trap. And until Tesla breaks above $280 or below $215, I am going to hold the fort [keep my existing long position in place]. From a technical perspective, Tesla is currently in a no-trade zone [$215 to $280].

Where Will Tesla Stock Be In 2025?

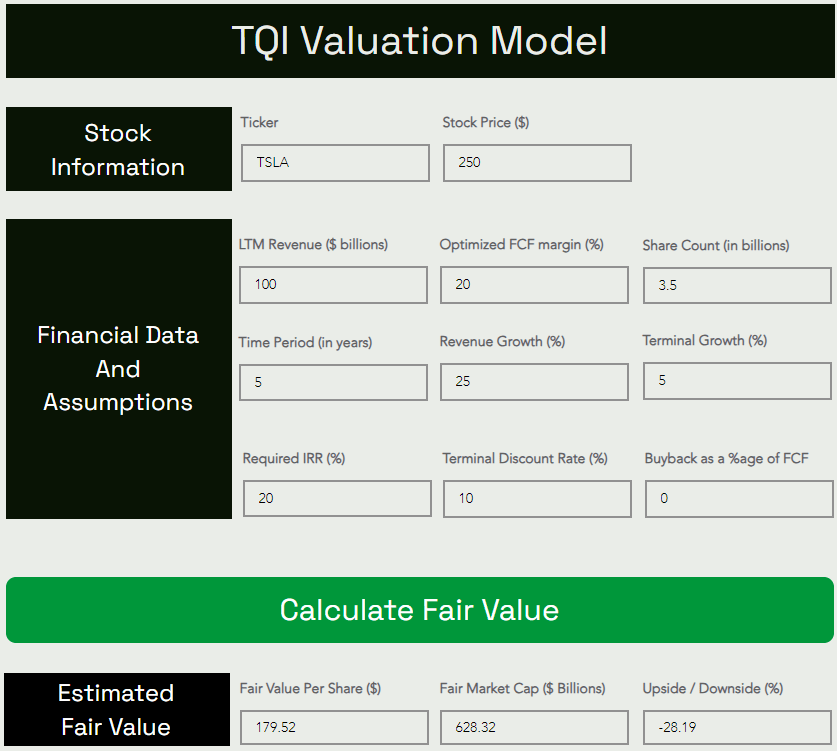

To answer this question, we will utilize TQI Valuation Model with the following assumptions:

Revenue base: $100B [2023 estimate]

Modeling period: 5 years

Modeling period revenue growth: 25% CAGR [As of today, consensus analyst estimates peg Tesla’s CAGR revenue growth at ~20.58% per year for the next five years. However, I think Tesla could do a lot better in terms of growth (especially if its ambitious generalized-AI projects like FSD and Optimus Humanoid bot succeed), and so, I am ascribing a 25% CAGR revenue growth rate for the modeling period.]

SeekingAlpha

Optimized FCF margin: 20% [While Tesla’s TTM FCF margin is only ~6.7%, the EV giant could end up boasting software-like FCF margins (30-40%) over the long run if FSD achieves level-5 autonomy. Now, even without FSD, I can see Tesla’s FCF margins heading up to ~10-15% on efficiencies of scale. While this assumption is somewhat tricky, I am going with an optimized (steady-state) FCF margin of 20% for Tesla.]

All other assumptions are relatively straightforward, but if you have any questions, please feel free to share them in the comments section.

Here’s my latest valuation for Tesla:

TQI Valuation Model (TQIG.org)

Using a 5-yr modeling period and somewhat aggressive assumptions, we deduced a ~$180 fair value estimate for Tesla. At its current price of $250, Tesla has a downside of ~28% to its fair value.

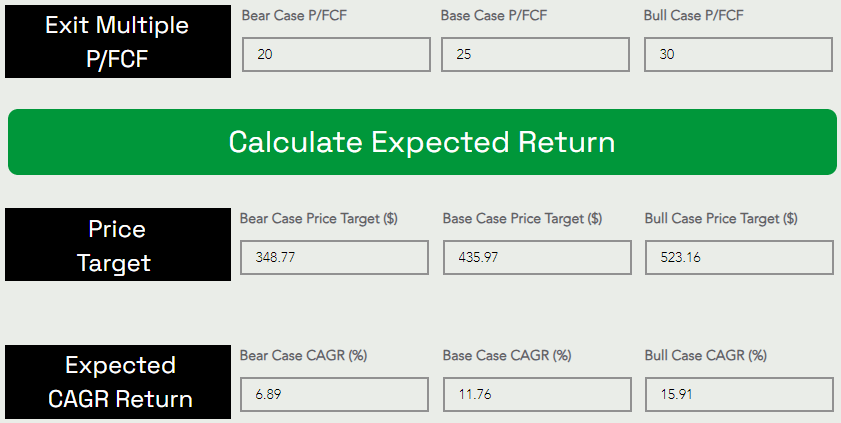

Assuming a base case exit multiple of ~25x P/FCF, TSLA could be trading at ~$436 per share five years from now.

TQI Valuation Model (TQIG.org)

At this estimated future price, Tesla would generate a 5-yr CAGR return of ~12%, which is lower than my investment hurdle rate of 15%. Hence, I think TSLA’s long-term risk/reward is still unfavorable for bulls, with the stock having gotten too far, too fast, above its fair value.

If we were to extrapolate prices based on Tesla’s projected 5-yr CAGR return, I see TSLA’s share price reaching ~$224.22 per share (or ~$800B in market cap) by the end of 2025.

End of Year

Tesla Share Price Target

2023

$179.52

2024

$200.63

2025

$224.22

Given Tesla’s current stock price of $250 per share, TSLA looks like dead money for the next couple of years. While we may never see TSLA plunging back down into the $100s (if an economic recession can be avoided), the stock is likely to consolidate its stellar year-to-date rally for quite some time, and the digestion period could be as long as a couple of years.

Concluding Thoughts: Is TSLA Stock A Sell Or A Good Long-Term Investment?

According to my analysis, Tesla’s stock has a ~30% downside to its fair value. And the risk/reward is looking unattractive, with TSLA stock offering ~12% CAGR return for the next five years. While these sorts of returns may be acceptable for many individuals, I see far better plays in what I believe is a stock pickers’ market. From a quant factor grade perspective, Tesla is not a buy. And technically, Tesla is in a no-trade zone despite strong momentum.

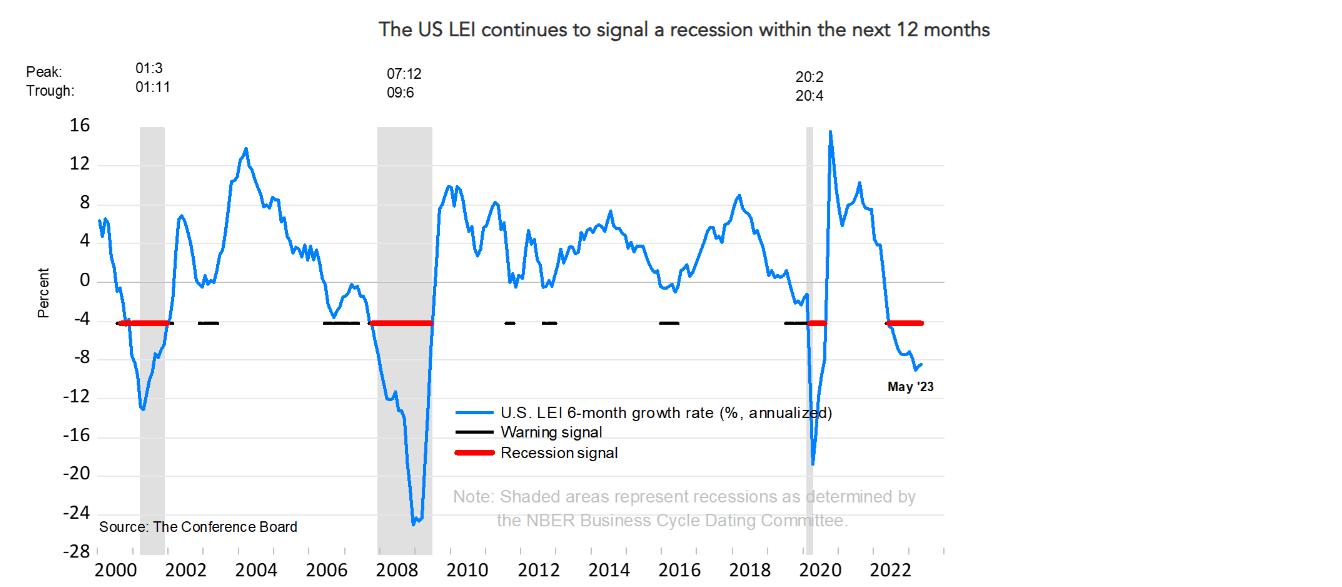

Leading Economic Indicators (Conference Board)

With a potential recession still ahead of us, Tesla’s near-term business outlook remains uncertain, and for those worried about near-term market gyrations, buying treasuries yielding ~5-5.5% while waiting for a better entry point (in the high-$100s) is a fine idea.

After weighing near-term and long-term risk-reward, I am keeping a neutral stance on TSLA at current levels. If Tesla slides back to ~$180 without significant deterioration in the business’s financial performance, I would re-start accumulation and add more TSLA to my long position. On the flip side, if Tesla’s valuation gets out of whack with reality in the next 6-12 months (downside risk rises from ~30% to, say, ~50-60% [TSLA gets to $360-400+]), I would happily take more gains here by gradually selling out of my long position in Tesla.

Key Takeaway: I rate Tesla “Neutral/Hold” in the $250s.

Thanks for reading, and happy investing! Please share your thoughts, questions, and/or concerns in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking to upgrade your investing operations?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our marketplace service – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.