Summary:

- Exxon is set to acquire Denbury in an all-stock transaction that values Denbury at a slight premium.

- The move is entirely motivated by Denbury’s carbon capture assets; for a large player like Exxon, it makes sense to expand in this space and benefit from the government subsidies.

- Exxon’s move may also increase the interest in other smaller companies that own carbon capture assets.

pcess609

Exxon Mobil Corporation (NYSE:XOM) announced that it had entered into a definitive agreement to acquire Denbury Inc. (DEN). The deal is an all-stock transaction and Denbury’s shareholders with will get 0.84 Exxon shares for each Denbury share. This values Denbury’s stock at $89.45, a tiny premium above yesterday’s close of $86.74.

Who is Denbury?

Denbury is a small onshore producer with ambitions in the carbon capture area. As I wrote in my recent DEN article, perhaps these ambitions were indeed too big for Denbury’s size:

One important way in which Denbury differs from its peer group is the emphasis on its carbon capture, utilization and storage (or CCUS) business. While “CCUS” or “carbon capture”, just like “hydrogen”, has quickly become one of the energy transition’s buzzwords, the reality is that it is usually larger companies seeking to develop these projects; not many small oil players are active in this space.

To be fair, Denbury’s involvement in CCUS is probably due to rather unique circumstances. DEN’s oil production had been relying on “enhanced oil recovery” (or EOR) through the injection of CO2 into its reservoirs since the 1990s:

EOR using CO2 is one of the most efficient tertiary recovery mechanisms for producing crude oil. When injected under pressure into underground, oil-bearing rock formations, CO2 acts somewhat like a solvent as it travels through the reservoir rock, mixing with and modifying the characteristics of the oil so it can be produced and sold.

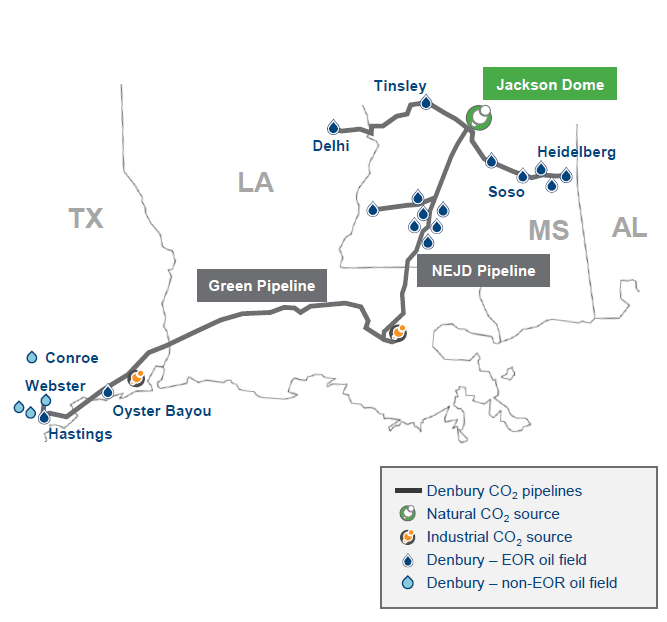

Historically, Denbury has used CO2 from naturally occurring reserves like its Jackson Dome asset in Mississippi and has developed a pipeline network to transport the CO2 to its oil producing fields:

Denbury Investor Presentation

When the ESG trend accelerated and the U.S. and other governments became focused on carbon, Denbury likely quickly connected the dots and figured they could position their pipeline infrastructure to source industrial CO2 instead and in this way capture (no pun intended) the generous Section 45Q tax credits.

Why is Exxon acquiring Denbury?

There’s little doubt that the CCUS business is the only driver behind the acquisition. Exxon pretty much said the same:

Acquiring Denbury reflects our determination to profitably grow our Low Carbon Solutions business by serving a range of hard-to-decarbonize industries with a comprehensive carbon capture and sequestration offering. The breadth of Denbury’s network, when added to ExxonMobil’s decades of experience and capabilities in CCS, gives us the opportunity to play an even greater role in a thoughtful energy transition, as we continue to deliver on our commitment to provide the world with the vital energy and products it needs.

As I wrote before, as an oil producer Denbury isn’t particularly impressive and its stock was a bit overpriced. The acquisition price is actually below where DEN traded in back in May.

Is the acquisition a good deal for the Denbury and Exxon shareholders?

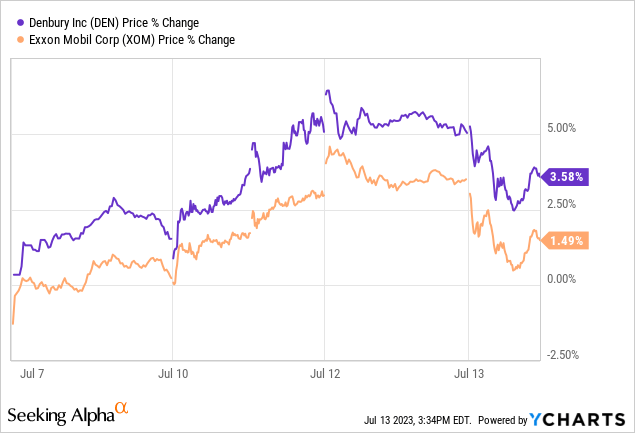

Today both XOM and DEN are down so the market probably wasn’t too happy about the announcement as with a number of recent acquisitions:

Denbury was overpriced in my view, so from that perspective its management may have done well to cash out on the CCUS franchise value instead of pouring a lot of capex to really make it work.

For Exxon, some investors may be perhaps disappointed with what on the surface appears like a Shell (SHEL) or BP (BP) type of move into a non-core ESG area. However, the reality is that Joe Biden is paying $85 per ton of CO2 (you could of course argue it’s you and I who are ultimately paying it). There’s no reason for Exxon not to claim some of that money given they have the engineering expertise and scale to do it.

What does the acquisition mean for other carbon capture plays?

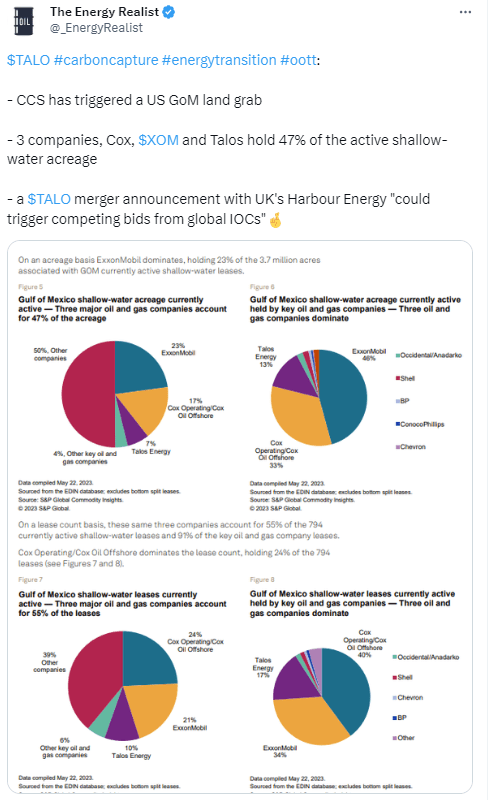

Exxon is a leader in the energy industry, so when Exxon does something, others may follow. I recently took note of an interesting and highly speculative analysis from IHS that talked about the high ownership concentration of potential carbon storage sites in the US Gulf of Mexico (one of the areas where a lot of industrial CO2 is generated):

Twitter

The thesis was that Cox, a private company, Exxon and Talos Energy (TALO) together hold almost 50% of the suitable acreage. The speculation was that if the UK’s Harbour Energy announced it would acquire Talos, which was rumored but hasn’t happened yet, that may open up a bidding war among the bigger fish (meaning mostly the majors). So it wouldn’t be surprising if someone else, perhaps Chevron (CVX), follows suit and also tries to make a deal, but for now it is just speculation.

The bottom line

We can debate whether CCUS will contribute to any climate goals and whether as societal cost-benefit the whole exercise makes sense in the first place, but the money paid for it is real. Given the CCUS enterprise requires a larger scale, it makes sense for the big players like Exxon to be in this space. For the smaller fish and early movers like Denbury and Talos, the opportunity may be simply to sell to the highest bidder and cash out.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of XOM; TALO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

My articles, blog posts, and comments on this platform do not constitute investment recommendations, but rather express my personal opinions and are for informational purposes only. I am not a registered investment advisor and none of my writings should be considered as investment advice. While I do my best to ensure I present correct factual information, I cannot guarantee that my articles or posts are error-free. You should perform your own due diligence before acting upon any information contained therein.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.