Summary:

- AT&T has halted excavation of their lead-sheathed cables around the Lake Tahoe Area.

- In 2021, AT&T agreed to remove a small network of lead-sheathed cables that may come into contact with the lake water to avoid future litigation risks.

- As a local to the Truckee Meadows/Tahoe area, I will add my two cents on the water system in the area as it relates to lead pollution.

- AT&T and Verizon remain two of the cheapest stocks in the market.

Aron Hughes/iStock via Getty Images

Another litigation scare

Similar to 3M (MMM), AT&T (NYSE:T) and Verizon (VZ) are now seeing their shares hacked down by the mighty sword of litigation threats. While no one can know the veracity of the claims that swirl around telecoms with lead-sheathed wires in the ground, I will do my best to add my two cents about the AT&T situation. AT&T has now halted excavating of their lead-sheathed cables around the Lake Tahoe area. As someone who is local and pays attention to the tap water that runs out of Lake Tahoe, I have never seen elevated lead reports associated with tap water that is derived from the lake.

This latest scare may be way overblown. AT&T, along with Verizon is one of the cheapest stocks in the market based on earnings yield and dividend. Let’s take a look at the Lake Tahoe case.

Where this all started

Back in 2021 to avoid any future litigation risks, AT&T agreed to remove a small network of lead-sheathed cables that may come into contact with the lake water. As a local to the area, we know how vitally important Lake Tahoe is.

Not only is it Northern Nevada’s best recreational hot spot, but it’s also the tap water that is consumed by all those that are served within the Truckee Meadows water system. This includes most of Washoe County. The lake is a vital part of the wildlife that lives in the marsh lands below the lake. This is one of the reasons Washoe County is one of the few counties in the United States to still not have fluoridated water. The local environmentalists care deeply about the wildlife connected to the watershed system.

The most direct recipients of any lead pollution in the watershed would be Incline Village and some of the areas of Reno and Carson City that are closest to Lake Tahoe. The Truckee Meadows Water Authority has a water quality map, updated frequently. From my knowledge, never has the tap water system in Incline Village, Truckee California, Carson City or Reno, Nevada been found to have had elevated lead levels.

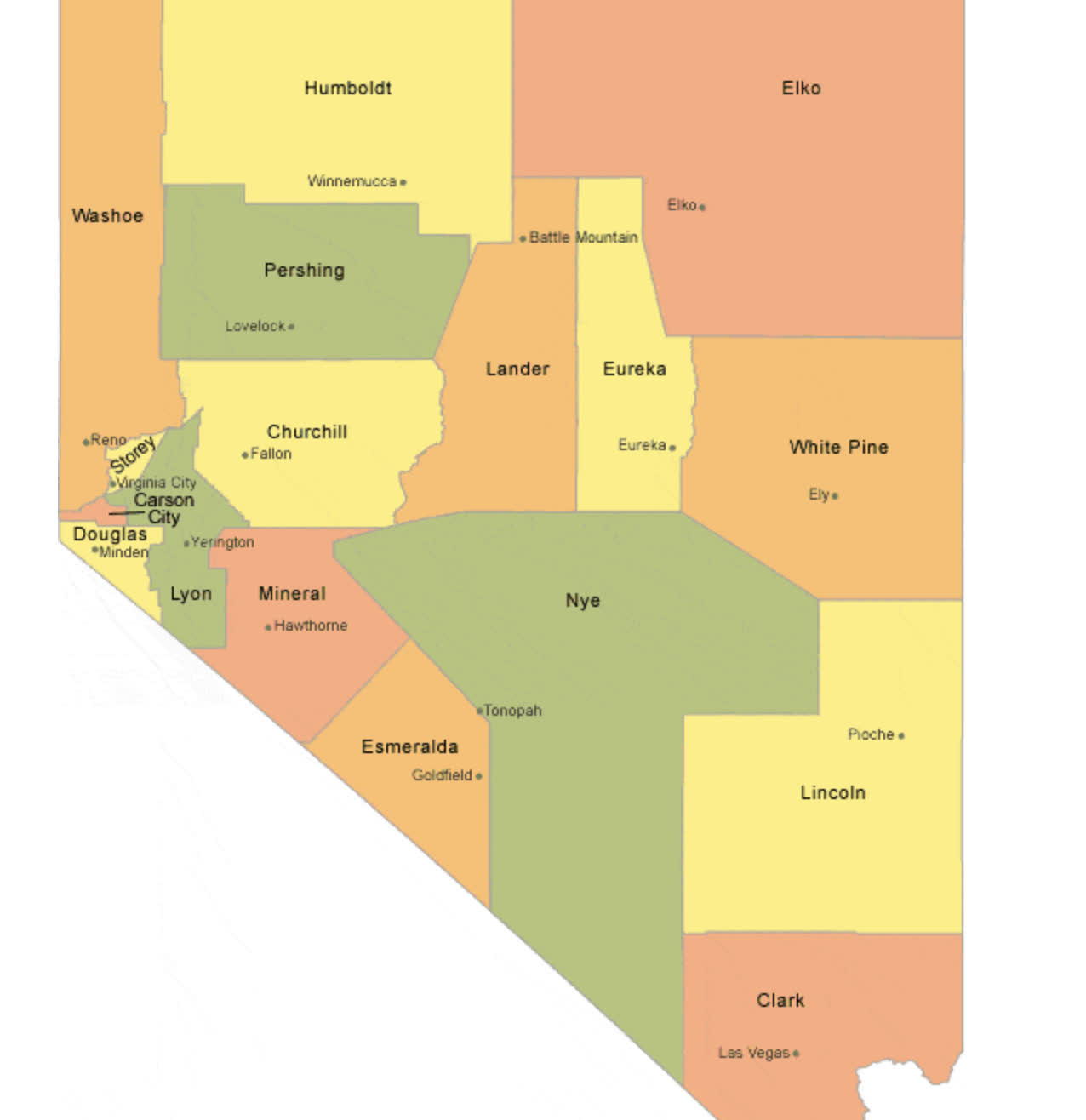

Areas where lead tested high in Nevada

The most recent analysis on lead in the greater Nevada water systems happened in 2016, here are the details from the local Reno Gazette:

A recent report in USA Today shows that 23 Nevada public water systems are not compliant with safety standards for contaminants. Public records from the Nevada Department of Environmental Protection show that three state public water systems exceed recommended safety levels for contaminants including lead, uranium, arsenic, and coliform bacteria.

The three state water systems posing the most harm exceed the EPA’s recommended safety level for lead, which is 15 parts per billion. All three water systems are under investigation for unsafe drinking water that is supplied to the public.

- Goodsprings School – Located in Clark County, the Goodsprings water system showed lead levels of 16 parts per billion.

- Fort Churchill Power Plant – Located in Lyon County, the Fort Churchill Power Plant water system showed lead levels of 16 parts per billion.

- Marigold Mine Potable Water System – Located in Humboldt County, the Marigold Mine Water System shows lead levels of 50 parts per billion, the highest lead levels in the entire state of Nevada.

geology.com

Washoe County is the most important of all these counties when looking to see if the lead-sheathed cables have an impact on groundwater. Whatever ends up in the Lake Tahoe Watershed normally ends up in the municipal tap water system of Washoe County. The study showed elevated lead levels in Clark County, far to the South incorporating Las Vegas. Lyon County, pretty far to the East of the lake in the furthest Eastern portion, also had high lead levels. The last was Humboldt County which borders Oregon.

Clark and Humboldt are not even served by the same water resource as Washoe County. Las Vegas is certainly served by Lake Mead and Humboldt is most likely a combination of Oregon and Nevada wells. The same goes for the closest area to Washoe with high lead levels, Lyon County which is mostly dependent on underground well water, not directly influenced by the Lake.

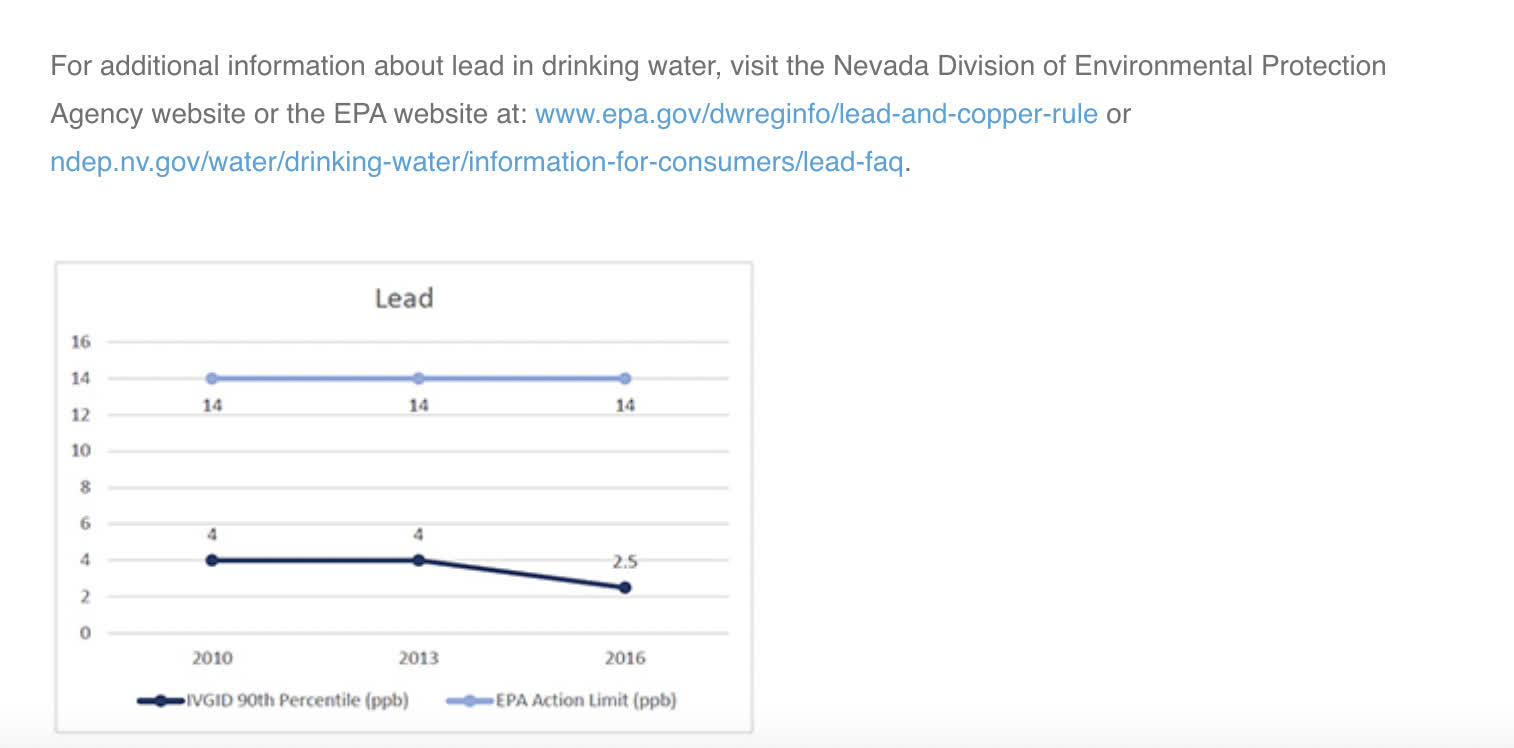

Incline Village

yourtahoeplace.com

The above is from the same 2016 study. This information is from the Water Quality website for the Incline Village Water system. The is one of the most affluent cities in all the United States, a playground of tech millionaires and billionaires. The environment is heavily monitored and the lead levels of the tap water for Incline Village were far below the EPA action limit at 2.5 ppb. The EPA action limit is 14 ppb. Incline Village would be ground zero to see if any lead was entering the tap water system since they are first on the watershed connect-a-dot.

Valuation

Throwing a dart at the AT&T or Verizon valuation grades could lead you to a value thesis on a variety of metrics. When something is trading under book value, that always leads me to a quick Graham Number valuation. This is based on the price to book times the price to earnings not exceeding the fair number of 22.5. The price target is set by taking the square root of the book value times EPS times 22.5. In this case, the forward EPS estimates look like the following:

Seeking Alpha

Using the forward estimate of $2.43/share for 2023 as our earnings input and TTM book value per share of $13.9 as our book value input we get the following:

SQRT: $2.43 X $13.9 X 22.5 = $27.56

With AT&T now trading at roughly half of the fair value, the margin of safety may now be wide enough for some skeptical investors. This is a major utility company that I don’t see going anywhere anytime soon.

Risks

Who knows how far litigation fears can bring down the telecoms? We’ve seen what can happen to 3M and others like them. If you think this company will exist in 10 years, now would be a great entry point. If you don’t, I’m not going to blame you. If free cash flow cannot be brought up to the level that management is confident in generating to maintain the current dividend, a cut will send this down further. If it is sustained, let’s look at the potential of a static 8% dividend with the stock getting up to the fair value of $27 in the next decade.

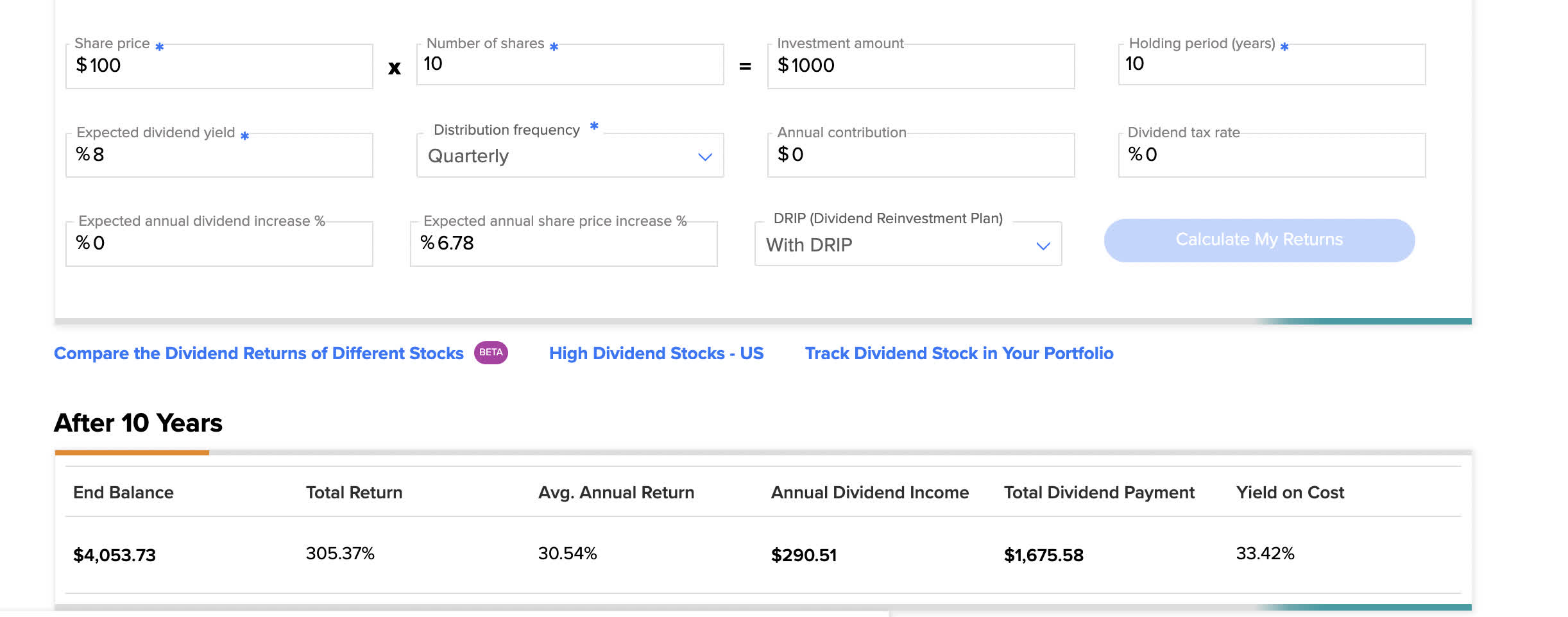

Dividend DRIP model

Assumptions:

- Stock rises from $14 to $27 in the forward 10 years, a CAGR of 6.78% per annum.

- Stock pays a static 8% dividend from this entry point.

- All dividends on DRIP.

Tipranks

The results are quite stunning at this entry point if you believe the company can make it to intrinsic value in the next 10 years and if you believe they can maintain this crazy high dividend.

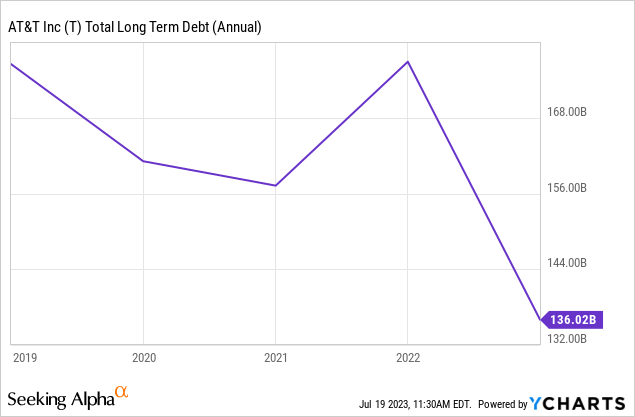

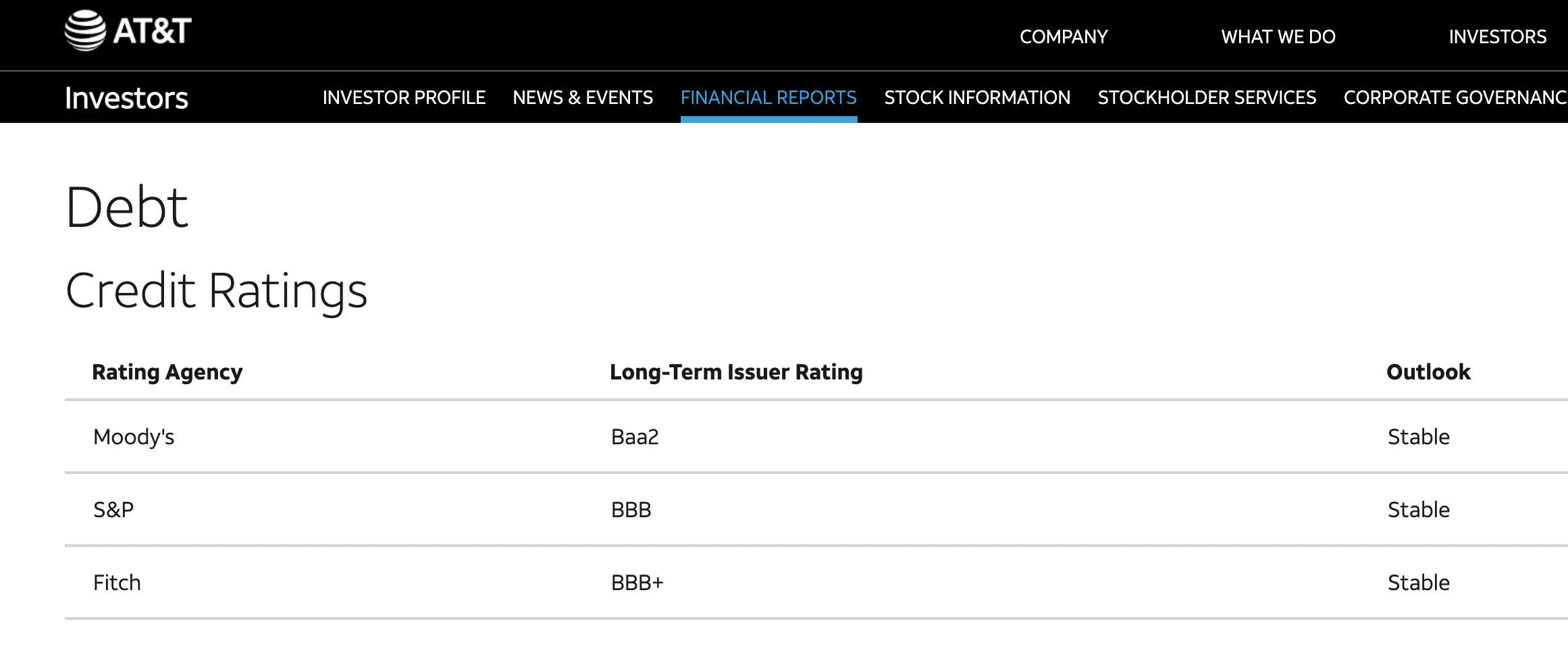

Debt

Debt has always been the number one concern with AT&T. A good portion was spun off in the Warner Bros. Discovery (WBD) deal and it continues to be paid down.

Seeking alpha

Interest expense has been on the decline for the past 5 years, here we can do a back of the napkin of the WACC of debt for AT&T assuming a TTM interest expense of $6.19 Billion and :

- $123.44 Billion Long Term Debt

- $4.0 Billion Short Term Debt

- $2.137 other current liabilities

- Total interest bearing liabilities of $129.577 Billion

- 6.19 Billion/$129.577= 4.7% cost of debt capital.

Maturities

With $13.75 Billion in debt maturing within one year, that’s about 10% of AT&T’s total debt load that either needs to be paid off or refinanced in the next year.

investors.att

Currently comping out BBB-rated corporate debt on my brokerage shows consistent coupons in the 4.8-5.5% range. Even issuing new debt at the high end would only raise the cost of debt by about one tenth of one percent if we assume they are refinancing 10% of the debt at shorter durations than 10 years and do not pay any portion of that down.

Ebit to net interest coverage

- TTM EBIT of $25.88 Billion

- Net interest expense of $6.19 Billion

- Coverage of 4.18 X

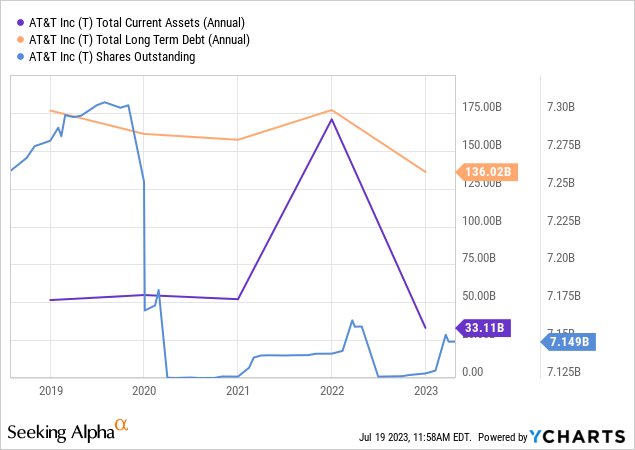

Balance sheet

Long-term debt and current assets have both dipped post spin-off. Shares outstanding are pretty flat and uneventful. Paying down debt, and maintaining a safe level of EBIT to net interest coverage while generating sufficient free cash flow to cover the dividend is the best we can hope for.

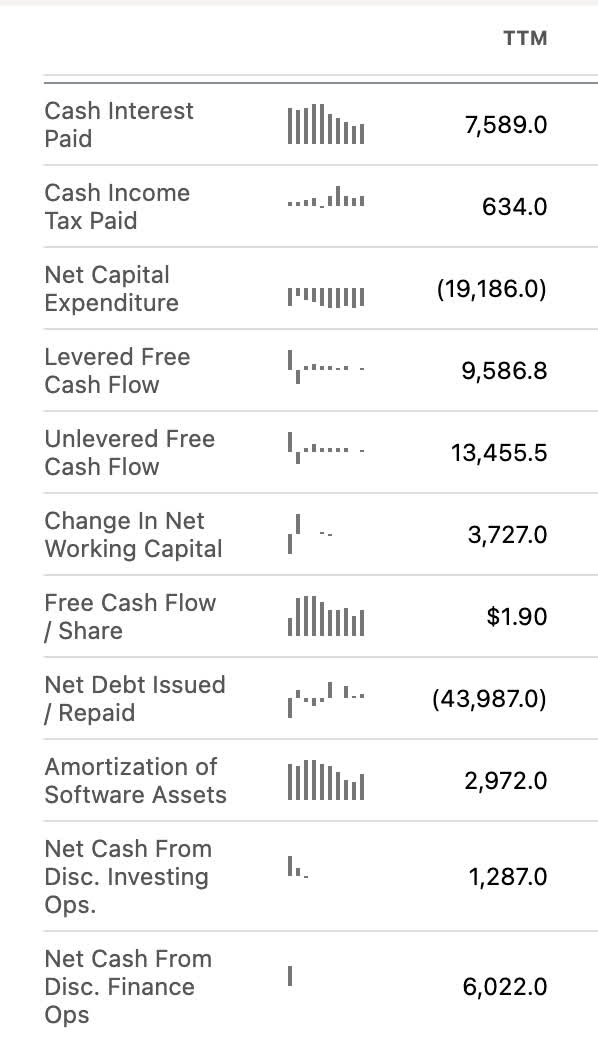

Free cash flow and the dividend

seeking alpha

With the forward dividend at $1.11 and free cash flow/share TTM at $1.9, the current payout is slated at 58%. Management indicates this will improve. Looks good right here unless you believe litigation reserves will start to pop up if lead cable liability materializes into a reality.

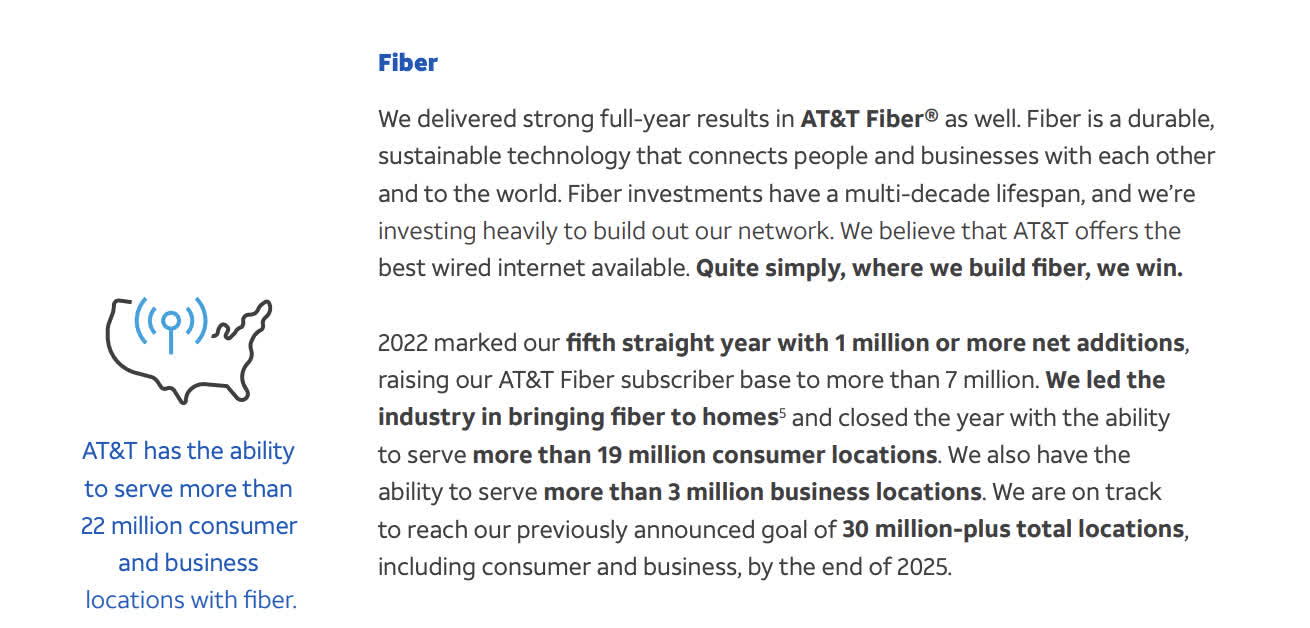

Catalysts and trajectory

- Fiber installation

investors.att

- 5G and wireless

investors.att investors.att

Rolling into 2023, AT&T is solely focused on its core business of expanding its cellular and internet network/customers. This is the business I like, utility-like without a ton of quirks. The company became more attractive to me post spin-off of Warner Brothers Discovery, regardless of the dividend cut. Regulated businesses pursuing unregulated businesses for growth opportunities is nothing new. It also fails quite a lot.

I don’t need huge growth in this investment, just cover the dividend and give me a slow increase in revenue that tracks inflation. At this price for the stock, that’s all I expect, and need to make a great return in the next decade for the entry point.

Summary

AT&T and Verizon are incredibly cheap and an amazing buy if you believe they can make it to a fair, Graham Number intrinsic value in the next decade while maintaining the dividend. The management of both does not seem nervous about covering the dividends, but management is not always honest either. Being local to the area where some of these first lead-sheathed cable issues are emanating from, I’m not seeing evidence of any lead pollution in the local news regarding tap water.

The Lake Tahoe/Truckee Meadows water shed is an excellent case study on whether or not the cables pose a threat to water systems. For now, it seems Mark Zuckerberg’s jet ski probably poses a bigger threat to the lake than the AT&T cables. Buy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MMM, T, VZ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.