Summary:

- Visa and Mastercard operate two of the best businesses in the world, as the duopoly responsible for processing most of the world’s transactions.

- Even after decades of market outperformance and high double-digit growth, the companies have plenty of room for growth, as their new services expand and cash usage continues to decline.

- Based on the companies’ P/E ratios, both trade below their historical valuations, and Mastercard trades at a 21% premium over Visa.

- While Mastercard outgrew Visa in terms of volumes and revenues, Visa increased the margin gap between the two and outgrew in terms of absolute dollars.

- I estimate both stocks will provide market-beating returns, and expect Visa to outperform due to its better margins, similar growth prospects, and more attractive valuation.

2Ban

Visa Inc. (NYSE:V) and Mastercard Incorporated (NYSE:MA) are international brands, trusted by billions of people to process their payments all over the world. Even after decades of outperformance and impressive high double-digit growth, I believe there’s still plenty of room for upside, as cash still takes a major portion of global transactions, and the companies are diversifying their offerings to new services.

As the companies trade below their historical multiples, I believe both will provide market-beating returns. However, I still find the underlying assumptions in Mastercard’s 21% premium over Visa wrong, and thus I estimate Visa is the better buy.

Background

At the beginning of April, I wrote articles covering both Mastercard and Visa. In both articles, I covered the companies’ businesses in-depth, described their complicated revenue streams, and provided comprehensive valuation models.

In the Mastercard article, I focused on detailing my investment thesis in payment networks and explained why I found Visa a superior investment, after comparing the companies’ margins, growth, and valuations.

In the Visa article, I focused on the companies’ immense growth prospects and addressed the main risks with their businesses. Specifically, I talked about competition from the likes of FedNow and the regulatory pressures the companies face occasionally.

I urge you to read both articles because this article will be dedicated to comparing the companies’ recent earnings results and providing updated valuation models.

Well, since my last article, Mastercard outperformed Visa, while both companies trailed the market. So far, we were wrong.

Now, let’s see how the companies performed in the second quarter of CY2023, which of them provided better results, and reassess our investment thesis accordingly.

Reaffirming The Investment Thesis

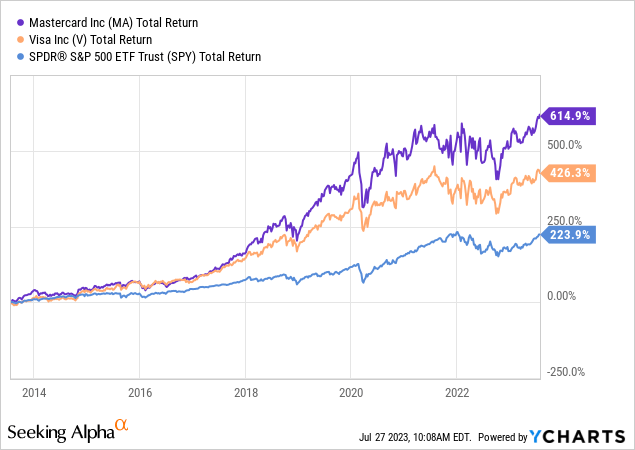

Both Visa and Mastercard have been the engine for the digitalization of payments worldwide for many decades now. Riding their self-created trend, the companies have provided investors with market-beating returns, through sequential double-digit growth in earnings.

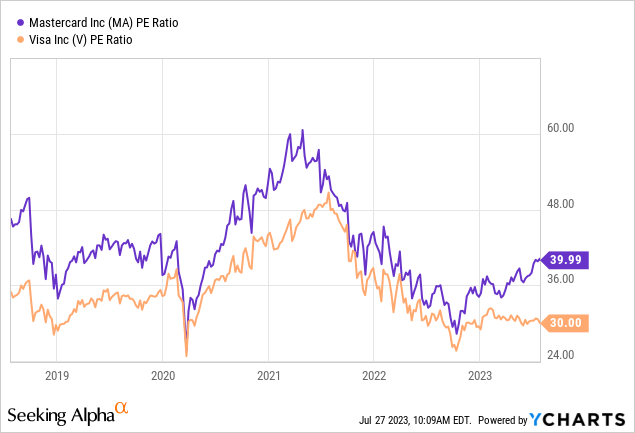

As penetration continues to increase at a fast pace and cash becomes less and less popular, investors worry the future isn’t as bright as the past. Accordingly, both stocks are trading below their 5-year average P/E ratios.

As I mentioned in my previous articles, cash still accounts for trillions of dollars in transactions worldwide. Both companies are still seeing volumes grow at a double-digit pace, despite the general perception of a slowing consumer economy.

Additionally, the non-consumer-payment businesses of both companies are growing rapidly and becoming a more important part of their respective enterprises. For Mastercard, value-added services revenues were $2.2B in the quarter, up 16.3% Y/Y. For Visa, total revenues amounted to $1.9B, up 19.0% Y/Y.

I estimate the non-consumer-payments categories will continue to grow sequentially at a high-teens pace, as both companies continue to add new services, expand services into new geographies, and penetration with existing clients deepens.

In short, I am still extremely bullish on Mastercard and Visa, and I believe both are still great investments, with a market-beating future ahead of them.

Who Won the Quarterly Earnings Battle?

Let’s not fool ourselves, Mastercard and Visa are essentially identical businesses. Yes, they have some different partners and some different solutions, but in essence, both companies are qualitatively the same.

Some investors decide to own both, but I see no reason to do so, as I aim for a concentrated market-beating portfolio. As we acknowledged that qualitatively they are almost identical, the only way to differentiate between Visa and Mastercard is by comparing their quantitative aspects.

At the time of writing this article, Mastercard is trading at a 21% premium compared to Visa, based on the companies’ expected 2024 P/E ratios. In my Mastercard article, I wrote the following regarding its premium:

In my view, the main reason the market values Mastercard at a premium compared to Visa is simply its size. Generally speaking, if all else is equal, a smaller company has a higher potential to outgrow a larger peer. Looking at 2022, Visa is 1.3X larger than Mastercard in terms of sales. Thus, it’s understandable the market assumes Mastercard will outgrow Visa, meaning that there isn’t a real gap if we’re going to base our multiple on future earnings.

Then, I showed the underlying assumption of the market isn’t supported by the companies’ results, as Visa and Mastercard grew revenues and volumes at a similar pace between 2016-2022. Based on the valuation gap and Visa’s much better margins, I came to the conclusion Visa is the better investment.

Let’s see how the companies fared in the three months that ended in June 2023, and find out if my conclusion is still valid. Just one important thing to note beforehand, Visa’s fiscal year is a quarter ahead of Mastercard’s, meaning Visa’s fiscal Q3-23 is comparable to Mastercard’s Q2-23. For convenience, I will refer to calendar periods from now on.

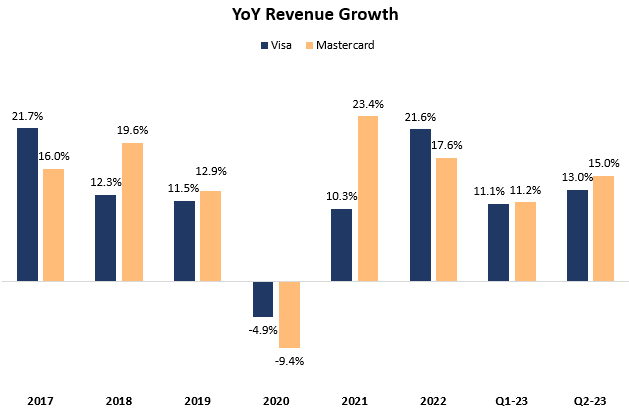

Revenue Growth – Mastercard Wins

Created and calculated by the author using data from the companies’ reports; Last quarter’s figures are on a constant currency basis.

In the second quarter of 2023, Mastercard grew revenues by 15%, whereas Visa grew by 13%. In absolute dollars, Visa outgrew Mastercard by $121M. However, it’s the second quarter in a row that Mastercard outgrew Visa, and this time it was by a wider margin. Thus, Mastercard wins the revenue growth battle.

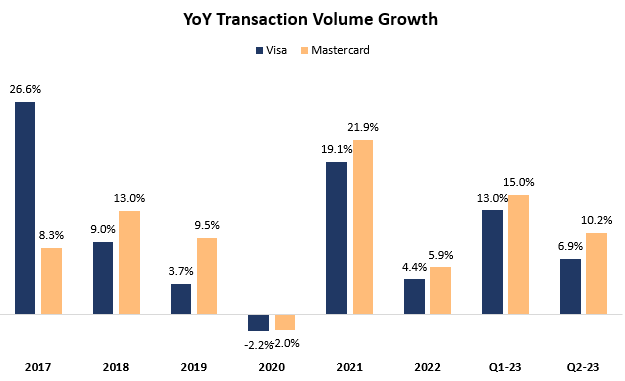

Volume Growth – Mastercard Wins

Created and calculated by the author using data from the companies’ reports.

Looking at transaction volume, in the second quarter of 2023, Mastercard outgrew Visa by 3.3 percentage points. In absolute dollars, Visa outgrew Mastercard by $37B. Visa still processes a much larger volume of transactions, almost 70% larger than Mastercard. In my view, Visa’s ability to maintain its share is impressive, and yet, Mastercard deserves the win here.

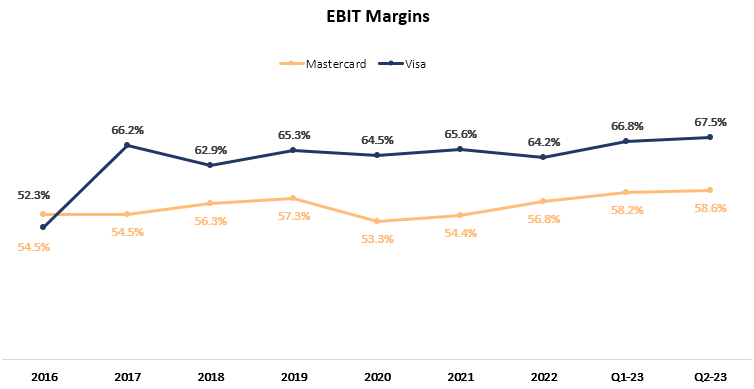

Margins – Visa Wins

Created and calculated by the author based on data from the companies’ reports; Margins are adjusted for litigation expenses.

As we can see, the margin gap between the companies has widened, increasing from 8.6 points in Q1-23 to 8.9 points in Q2. Visa, being more profitable than Mastercard, increases the importance of Mastercard’s relative growth. To put it simply, for each incremental dollar, Visa makes $0.68 in operating profit, whereas Mastercard makes $0.59. Thus, in order to grow absolute operating profit at the same pace as Visa, Mastercard needs to outgrow its revenues by 16%. In the last quarter, Mastercard managed to outgrow Visa by a mere 2.0%.

Mastercard Wins The Calendar Q2-23 Battle

By itself, the fact that Mastercard is starting at a lower baseline doesn’t automatically mean it will easily outgrow Visa. Despite Mastercard’s better quarterly results, I reaffirm my initial conclusion.

The premium Mastercard is getting has only increased since my previous article, as its stock outperformed Visa’s. Visa is still growing on par with Mastercard, despite being the larger company. Visa also continues to be more efficient and more profitable, whilst innovating at least at the same level as Mastercard, with the former growing its non-consumer-payment services by 16.3%, compared to the latter’s 19.0%.

Thus, I still find Visa more attractive.

Updated Mastercard Model

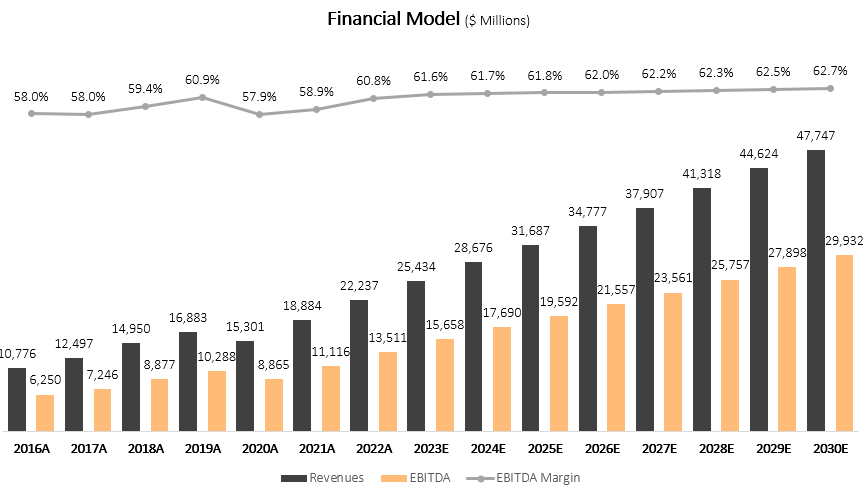

I used a discounted cash flow methodology to evaluate Mastercard’s fair value. I assume the company will grow revenues at a CAGR of 10.0% between 2023-2030, which is according to the company’s long-term growth targets. I believe revenues will grow at that pace due to sequential declines in cash usage, which will result in high GDV growth. Additionally, I expect the continued introduction of new value-added services and the growth of existing ones. I find this growth rate to be reasonable, as there’s still a huge untapped market, which amounts to $7.6T worth of volumes.

I project Mastercard’s EBITDA margins will increase incrementally up to 62.7%, which is 2 points higher over 2022. This projection results in EBITDA growth slightly above revenue growth, which is based on my assumption Mastercard will continue to benefit from operational leverage.

Created and calculated by the author based on Mastercard’s financial reports and the author’s projections

Taking a WACC of 7.5%, I estimate Mastercard’s fair value at $419.8B or $443 per share, reflecting 9.4% upside over its market value at the time of writing.

Updated Visa Model

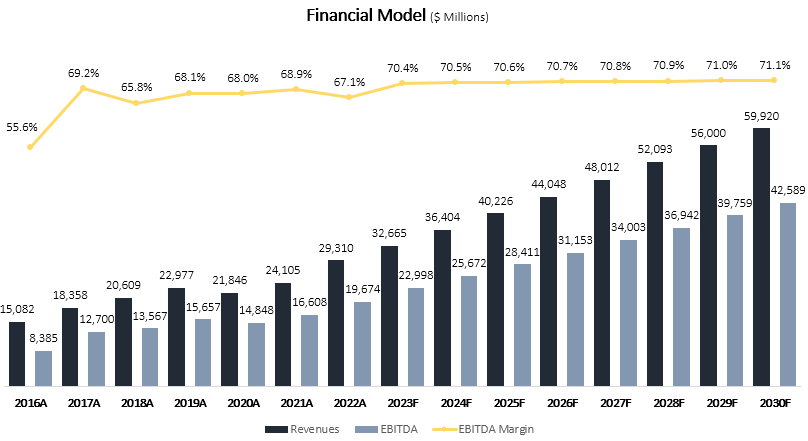

I used the same methodology to evaluate Visa’s fair value. I assume the company will grow revenues at a CAGR of 9.4% between 2023-2030, which is according to the company’s long-term growth targets, and slightly below my projection for Mastercard. I believe Visa shares the same growth prospects as Mastercard, but it starts at a higher baseline.

I project Visa’s EBITDA margins will increase incrementally up to 71.1%, which is slightly above the company’s margins for the first nine months of its fiscal 2023. This projection results in EBITDA growth slightly above revenue growth, meaning I forecast Visa will continue to benefit from operational leverage as well, but to a lesser extent.

Created and calculated by the author based on Visa’s financial reports and the author’s projections

Taking a WACC of 7.5%, I estimate Visa’s fair value at $580.5B or $285 per share, reflecting 19.9% upside over its market value at the time of writing.

Conclusion

Mastercard and Visa operate two of the best businesses in the world as an essential duopoly. The companies show no sign of slowing down, with a whole lot of cash transactions still occurring, as well as the introduction and expansion of new services outside of consumer payments.

As both companies are currently trading around 10% below their past 5-year average P/E ratios, I estimate both will provide market-beating returns well into the future. However, the 21% premium Mastercard is getting over Visa is unjustified in my view, reflecting Visa is more attractive at current prices.

Looking at my fair value estimates, I place Visa at a 29x P/E multiple based on consensus estimates for 2024, and I value Mastercard at a 31x multiple, reflecting my estimate for the fair premium at 5.7%.

Thus, I reiterate Visa as a Strong Buy and Mastercard as a Buy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of V either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.