Summary:

- AT&T’s share price continues to decline, but I believe the market is incorrect and that the stock has bottomed.

- Bridgewater Associates, led by Ray Dalio, started a new position in AT&T, adding 1.98 million shares.

- AT&T has the ability to generate significant free cash flow and has a manageable debt profile, which supports my bullish stance.

PM Images

It’s 13F season, and I am looking at which positions the largest institutions, and hedge funds are moving in and out of. Just because an institution, hedge fund, CNBC commentator, or Seeking Alpha contributor is bullish or bearish on a company doesn’t mean they are correct. I have been incorrect on AT&T (NYSE:T) for years as its share price continues to erode. The market hasn’t responded well to anything AT&T has done, and the spinoff of Warner Media hasn’t unlocked value for shareholders the way management envisioned. Shares of AT&T have declined by -22.81% over the past year, and since April 19th, shares have fallen -27.97% crashing through the $15 level. AT&T briefly traded under $14 and is flirting with that level again. I continue to believe the market is incorrect as AT&T’s valuation is inexpensive, and the amount of FCF generated is more than enough to service its debt while paying the current dividend. While many institutions and hedge funds added and reduced their shares of AT&T in Q2, Ray Dalio’s Bridgewater Associates started a new position in AT&T, adding 1.98 million shares. While Bridgewater has over $196 billion in assets under management (AUM), $30 million is still $30 million, and Bridgewater probably isn’t throwing a dart at the board to make their investment decisions. It can always get worse, but in AT&T’s case, I think it’s bottomed, and I’ll follow Ray Dalio and dollar cost average down on AT&T while the yield is 7.78%.

Seeking Alpha

This 13F season has been interesting for AT&T

For those who are unfamiliar with Form 13F, the SEC requires all institutional investment managers with at least $100 million in AUM to disclose their equity holding through a quarterly filing. The Form 13F lists all positions a hedge fund or financial institution engages in throughout the quarter and is typically filed 45 days after the last day of the calendar quarter. Some refer to this as following smart money as it discloses what professionals do with their AUM.

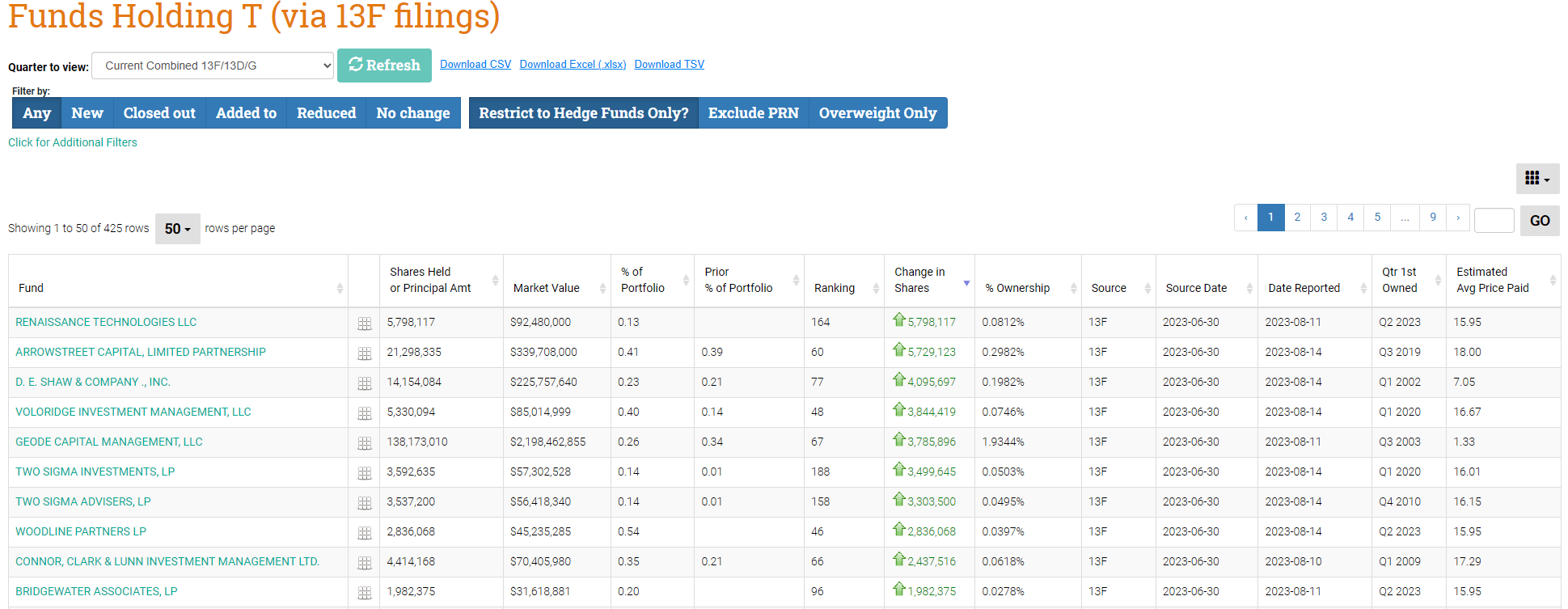

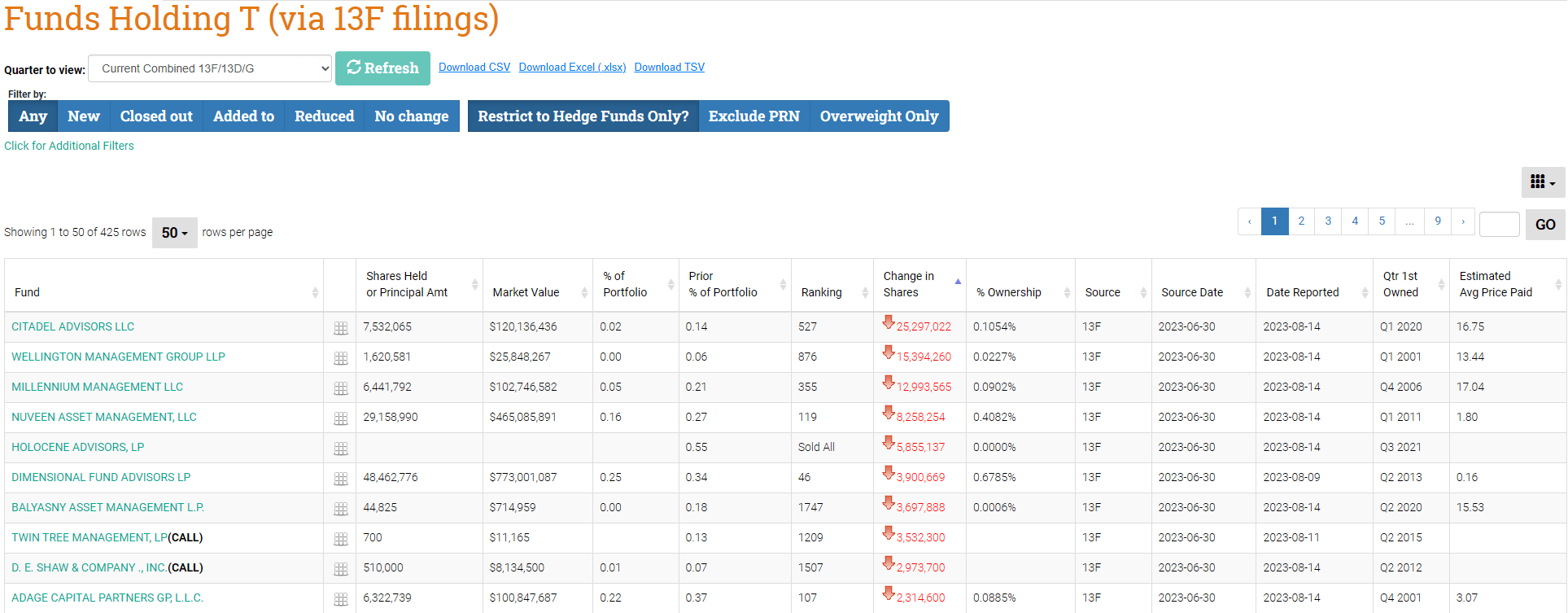

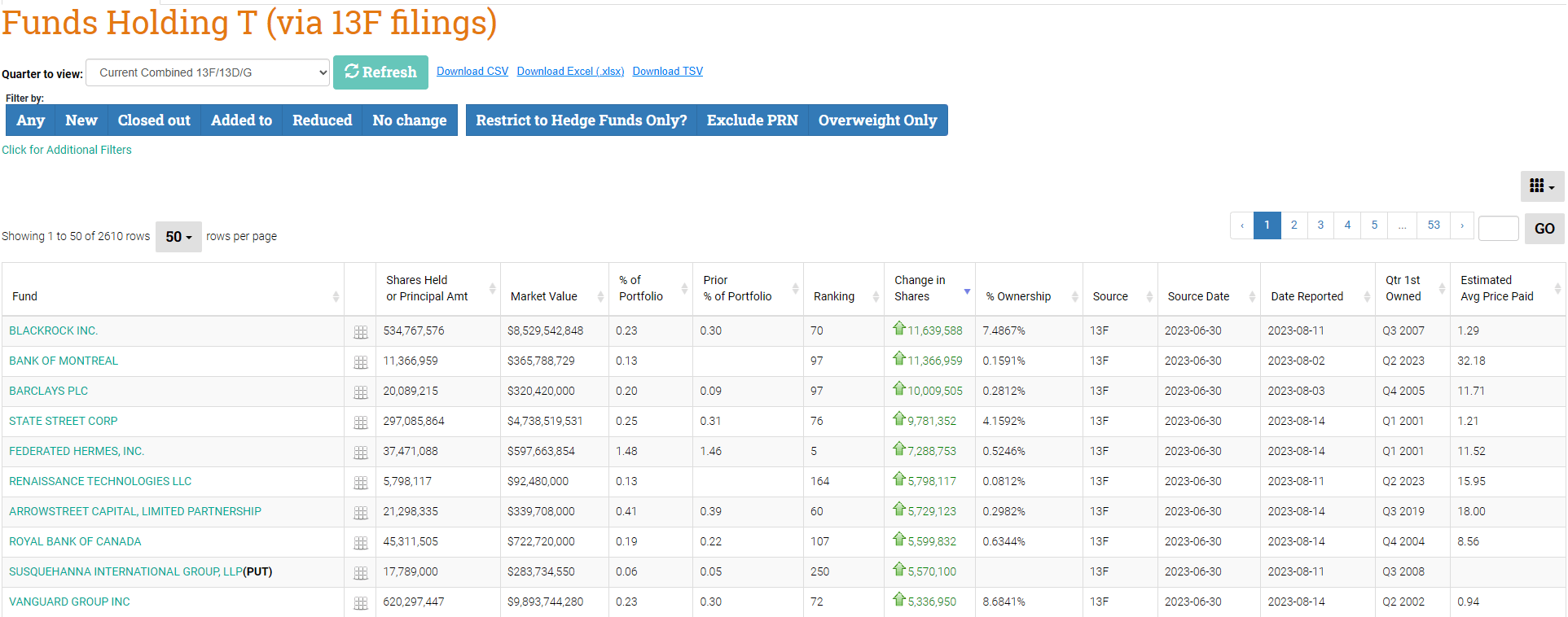

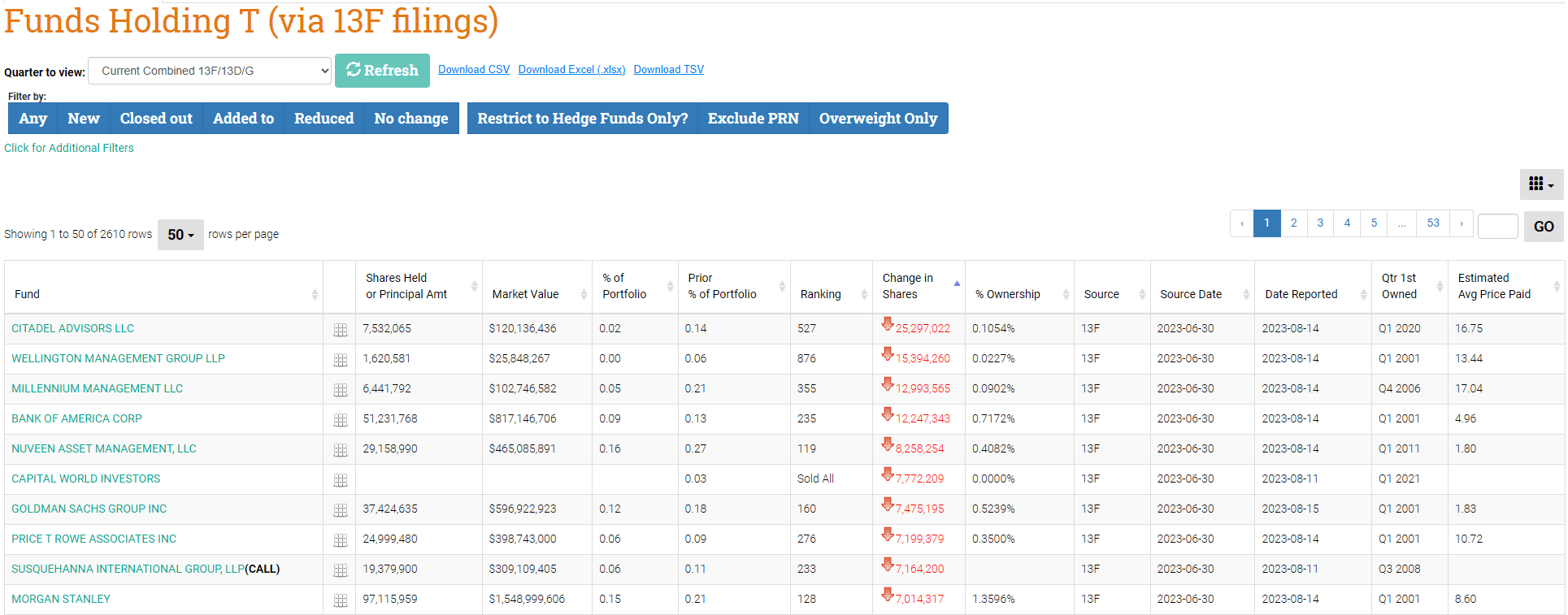

I utilize Whale Wisdom to see what professional institutions do with their AUM. Below is a snapshot of the 10 largest additions and reductions from hedge funds and financial institutions.

Top ten hedge funds adding shares of AT&T

Whale Wisdom

Top ten hedge funds reducing shares of AT&T

Whale Wisdom

Top 10 Financial institutions adding shares of AT&T

Whale Wisdom

Top 10 Financial institutions reducing shares of AT&T

Whale Wisdom

As I indicated earlier, just because a financial institution allocates its capital in a specific way doesn’t mean they are correct. I track what professional money managers are doing to see who is bullish or bearish on a position and to look at the inflows and outflows from institutional players. In Q2, AT&T saw more outflows than inflows from the 50 most active financial institutions on both sides of the AT&T trade. The 50 firms that added the most shares accounted for 176.06 million shares of AT&T added, while the 50 firms most actively reducing their position sold 218.26 million shares. The most notable hedge funds selling were Citadel Advisors run by Ken Griffin, and Millennium Management run by Israel Englander, while Bridgewater Associates, led by Ray Dalio, started a position in AT&T. On the institution side, Bank of America (BAC), Goldman Sachs (GS), and Morgan Stanley (MS) we’re all in the top ten firms reducing their exposure to AT&T, while BlackRock (BLK), Bank of Montreal (BMO), Barclays, State Street (STT), and Vanguard were on the other side adding shares.

AT&T has been a troubled stock for more than a decade, and no matter what side of the trade professionals are on, the market is the ultimate decision-maker. While respectable fund managers are reducing their positions, it is interesting to see Bridgewater start a position in AT&T. I feel that Ray Dalio is one of the best minds in the business, and while I am not making decisions based on what others do, it’s reassuring that others may see the same things I do that makes me believe that the market continues to be incorrect on AT&T’s valuation.

Why I am still bullish after the negative returns AT&T has delivered for me

Shares of AT&T have fallen -45.32% over the past decade, and I am still not ready to throw in the towel. Looking at AT&T’s chart is painful as it’s been caught in a perpetual downward trend since the pandemic. AT&T has continued to make lower lows over the past decade, and I don’t blame anyone for exiting their positions. Today AT&T is trading at a $101.95 billion market cap, and I still feel it’s low despite market sentiment or its debt profile.

Seeking Alpha

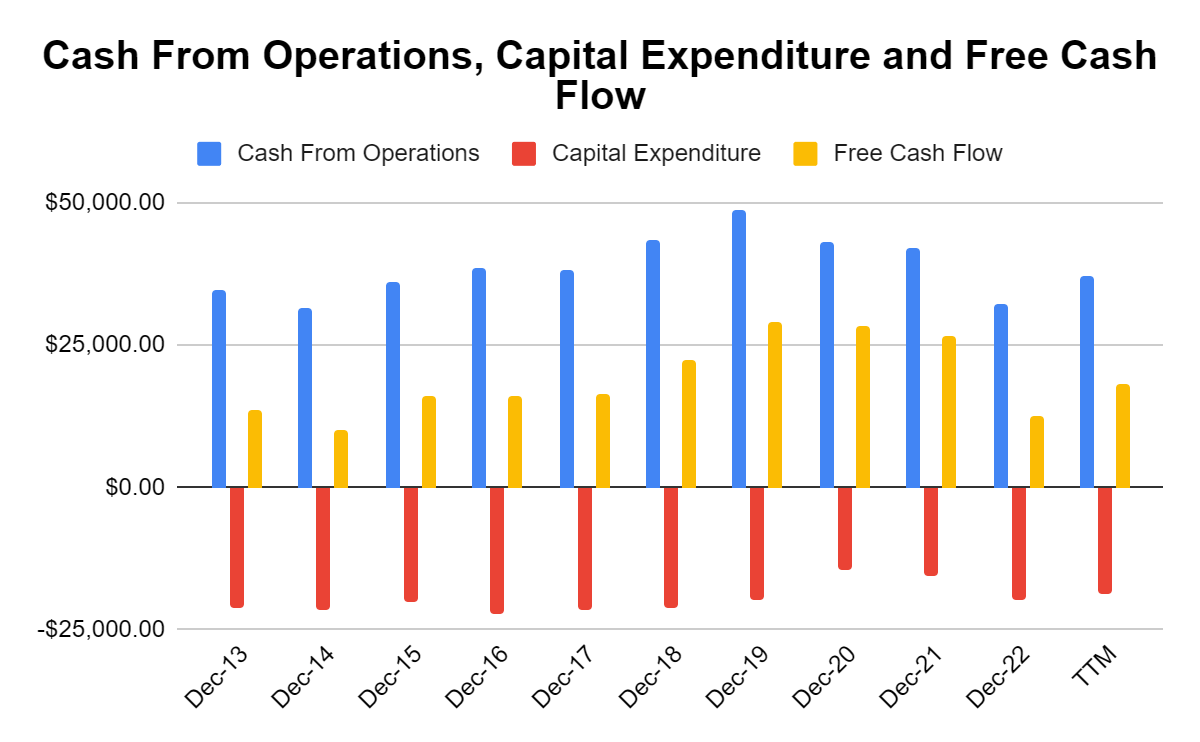

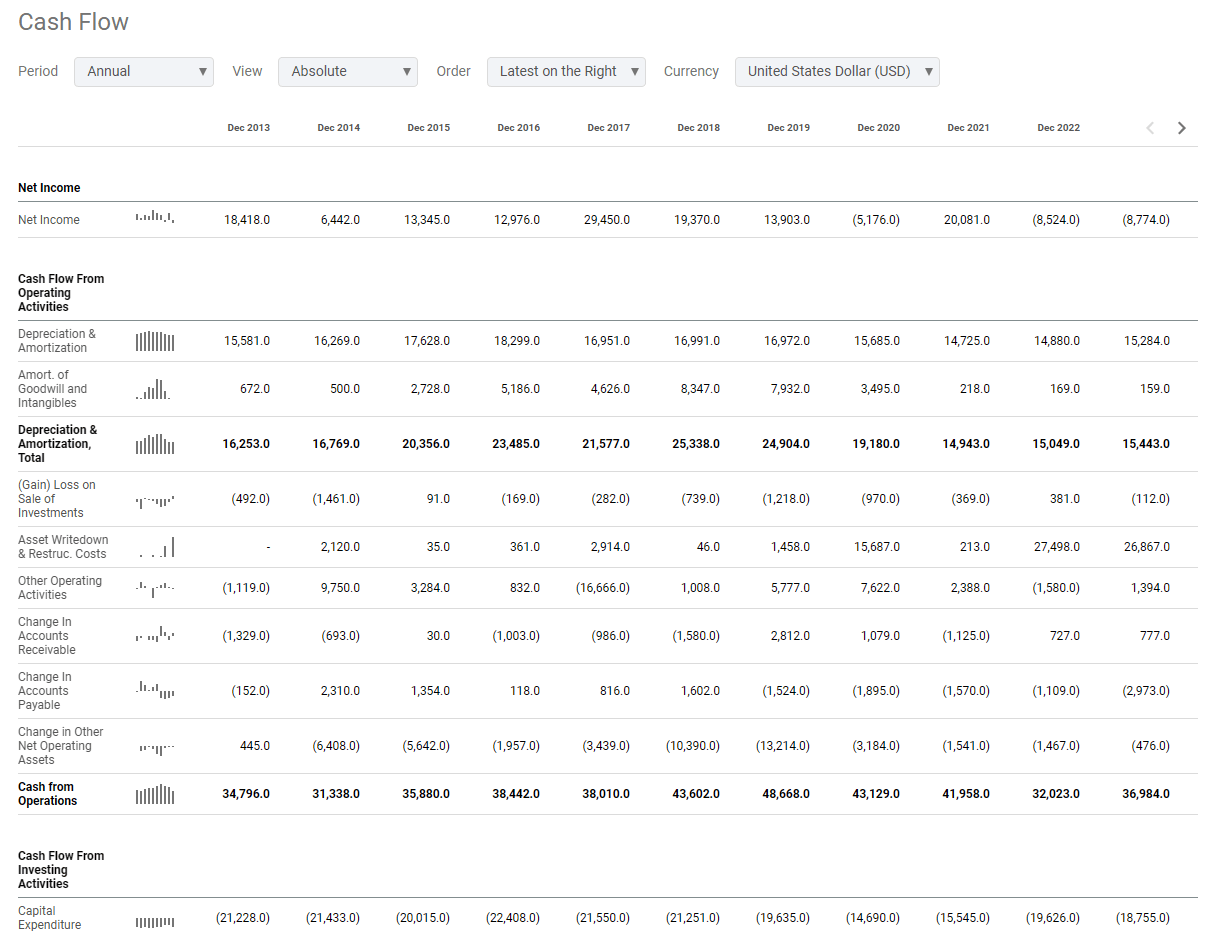

I put feelings aside and look at the numbers, and while market sentiment is an essential aspect of investing, sometimes it can overtake fundamentals. Despite AT&T being an unpopular company, nobody can dispute their ability to produce billions in free cash flow (FCF). Over the past decade (2014 – TTM), AT&T has generated $195.13 billion in FCF. Q1 2023 wasn’t optimal for AT&T as they generated $1 billion in FCF, significantly lower than the analyst estimates of $2.6 billion. Some questioned if AT&T could achieve its projections post Warner Media as their guidance called for $16 billion in FCF for the 2023 fiscal year. AT&T has divested assets and reduced its exposure outside of wireless, and that came at a financial cost. The $29.03 billion in FCF generated in 2019 and $28.44 billion generated in 2020 will be difficult to replicate, but AT&T doesn’t have to. AT&T is a smaller, more focused company today, as its sights are set on its core business of communications. In Q2 of 2023, AT&T generated $4.1 billion in FCF and indicated they would be generating roughly $11 billion in the 2nd half of 2023.

AT&T doesn’t have a problem generating FCF, and I focus on FCF because this is the pool of capital that is utilized to pay dividends, buy back shares, reduce debt, and make acquisitions. In the back half of 2023, AT&T plans to pay roughly $5 billion in dividends, allocate $2 billion toward spectrum clearing costs, and reduce its net debt by roughly $4 billion from the remaining FCF. So far, AT&T has generated $5.1 billion in throughout the first half of 2023, and with $11 billion in FCF expected in the back half of 2023, AT&T will deliver on its annualized FCF projections. AT&T also has the ability to drive future FCF by taking market share from its competitors. AT&T has added 2 million postpaid phone subscribers in the past year and grew its average revenue per user (ARPU) by $0.82. The mobility unit generated an additional $700 million of revenue in Q2 YoY while its EBITDA increased by $600 million to $8.7 billion. If AT&T can continue replicating its top-line growth, it should be able to see incremental YoY growth in its FCF, which will provide value for AT&T And its shareholders.

Steven Fiorillo, Seeking Alpha Seeking Alpha

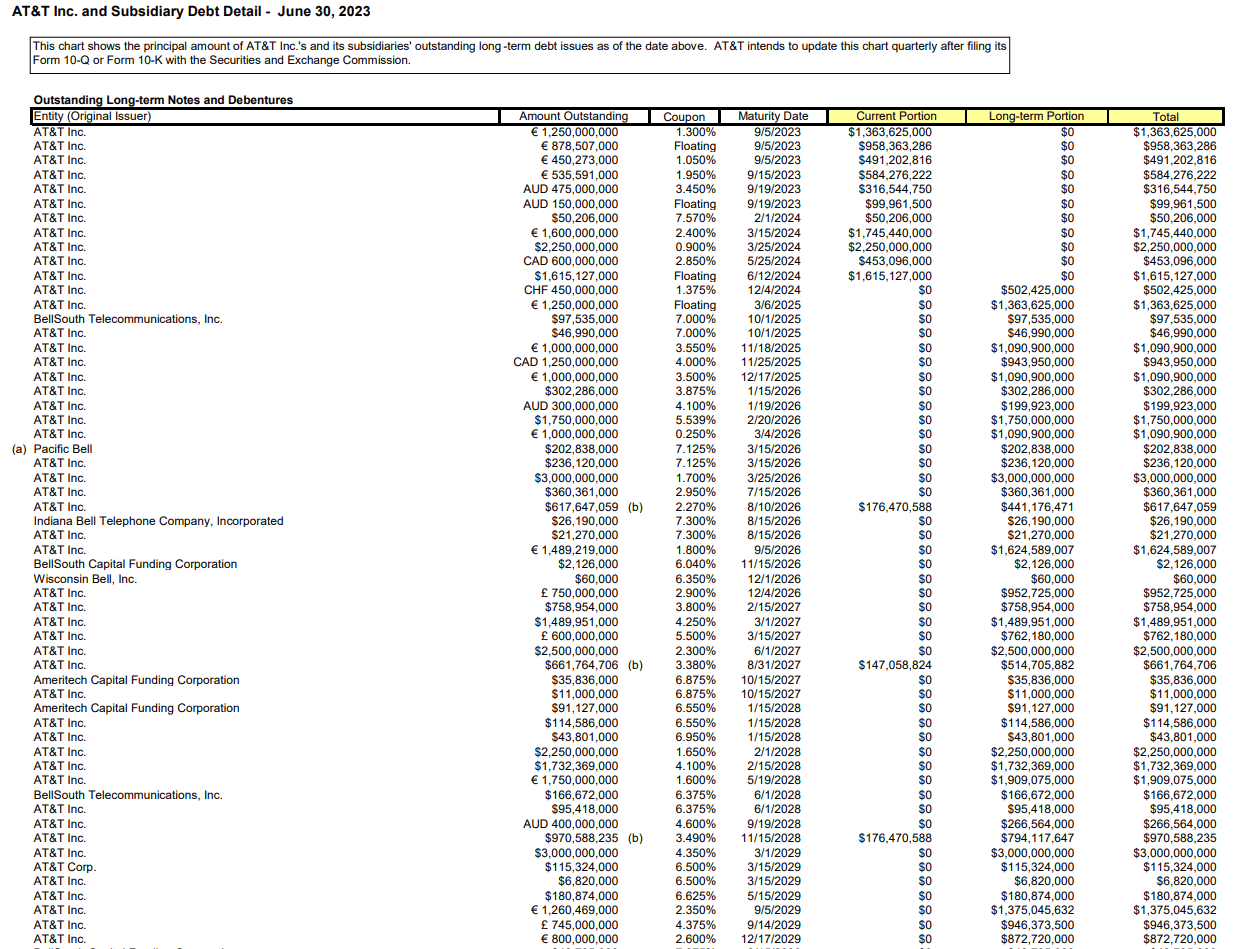

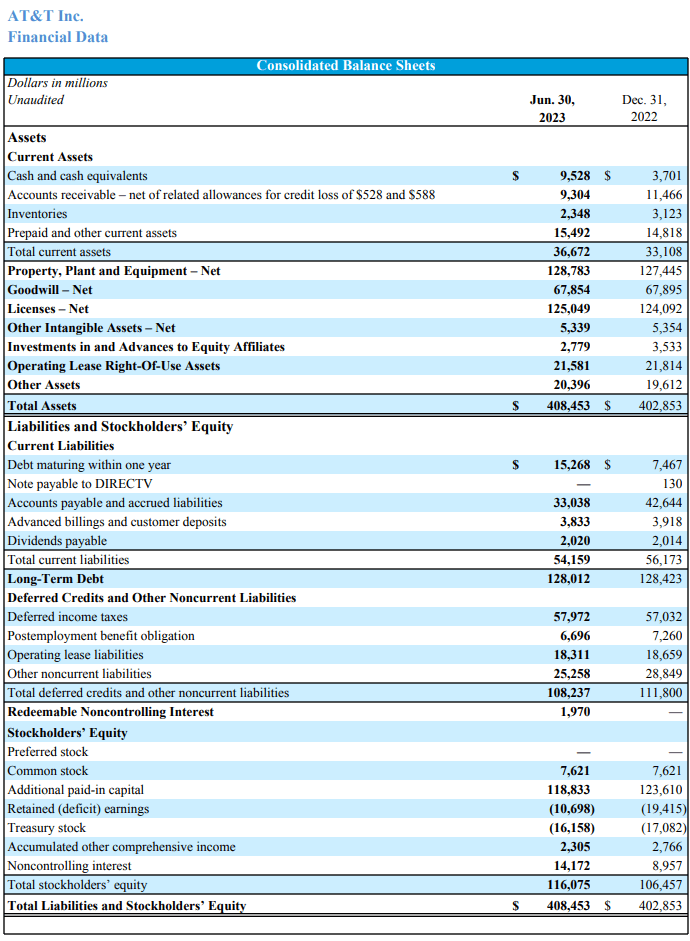

Going into 2023, AT&T had $147.67 billion in long-term debt obligations. Despite AT&T’s profitability and putting perception aside, debt has been a focal point of the bear case. Very few companies have a clean balance sheet without debt obligations, and even the most profitable company in the market, Apple (AAPL), has $98.07 billion of long-term debt on its balance sheet. At the close of Q2, AT&T had $146.65 billion in long-term debt, of which $10.43 billion is due over the next year. I have no idea what AT&T plans on doing, but with rates over 5%, I don’t believe it’s worth issuing new bonds or refinancing. The majority of their current debt has been issued at favorable rates, especially with $2.25 billion due on 3/25/24 with a 0.9% coupon.

Many people don’t look into the details. They see $147.67 billion on the balance sheet and never ask what is AT&T’s ability to service the debt. AT&T currently has $9.53 billion in cash on its balance sheet, with another $2.78 billion in investments. There is $10.43 billion of debt maturing over the next year and an additional $502.43 million maturing in December of 2024. There is $4 billion earmarked for debt reduction in the back half of 2023 from the $11 billion of FCF expected to be generated. According to AT&T’s debt maturity schedule, it looks like $3.81 billion will come due in the back half of 2023, leaving them with roughly $200 million of FCF left over. AT&T can repay its debt obligations in 2023 from its FCF without touching its cash on hand.

If this is what AT&T chooses to do, then they could possibly start out 2024 with a similar cash position as they have now. On an annualized basis, AT&T is paying roughly $8.2 billion in dividends which is 51.25% of its FCF. If AT&T were to generate $16 billion of FCF in 2024 and generate it evenly, AT&T would have roughly $1.95 billion retained FCF each quarter after dividends are paid. AT&T has at least $6.62 billion of debt maturing in the first half of 2024, with another $500 million coming due later in the year. If the retained $1.95 billion in quarterly FCF was allocated to the maturing debt, then AT&T would only utilize $2.26 billion of its cash on hand to repay the remaining maturing debt, leaving then with $6.95 billion in cash on hand and another $3.95 billion of FCF after dividends being generated in the 2nd half of the year. AT&T’s debt situation isn’t as grim as some believe, and they have the ability to service and repay their debt obligations with ease.

AT&T AT&T

What I think the market needs to see before the perception of AT&T changes

No matter what occurs, the market hasn’t rewarded AT&T. While AT&T is an FCF machine, trading at roughly 6.32x its FCF and a forward 2023 P/E of 5.87, the market still perceives AT&T as a value trap, not a value play. For this to change, I think AT&T needs to do 3 things, get the debt under $100 billion, start annual dividend increases, and authorize a buyback program. Unfortunately, this is a multi-year approach, and shareholders will probably need to sit back, collect the dividend, and wait a few years. AT&T hasn’t seen its debt level under $100 billion since 2014, so getting out of the triple digits would be meaningful. I think AT&T needs to authorize a $2 billion buyback plan and repurchase $100 million worth of shares on a quarterly basis to show the street they believe in the long-term plan management has put forward. Once the debt is under $100 billion, I think they should start doing a small annual dividend increase. If these things come together, I feel it would get investors excited about AT&T again, and the bear case would evaporate because the street would have proof that AT&T has changed its ways and is serious about deleveraging the balance sheet. I am in this for the long haul and plan on collecting my dividends while I wait for AT&T to turn around.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of T, AAPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: I am not an investment advisor or professional. This article is my own personal opinion and is not meant to be a recommendation of the purchase or sale of stock. The investments and strategies discussed within this article are solely my personal opinions and commentary on the subject. This article has been written for research and educational purposes only. Anything written in this article does not take into account the reader’s particular investment objectives, financial situation, needs, or personal circumstances and is not intended to be specific to you. Investors should conduct their own research before investing to see if the companies discussed in this article fit into their portfolio parameters. Just because something may be an enticing investment for myself or someone else, it may not be the correct investment for you.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.