Summary:

- PayPal’s stock has fallen 16% year to date and 41% over the last twelve months.

- The departure of Elliott Management from PayPal may concern investors, but we take the exit with a grain of salt.

- PayPal’s current valuation in our view represents a mispricing of the stock.

chameleonseye

Fallen Angel?

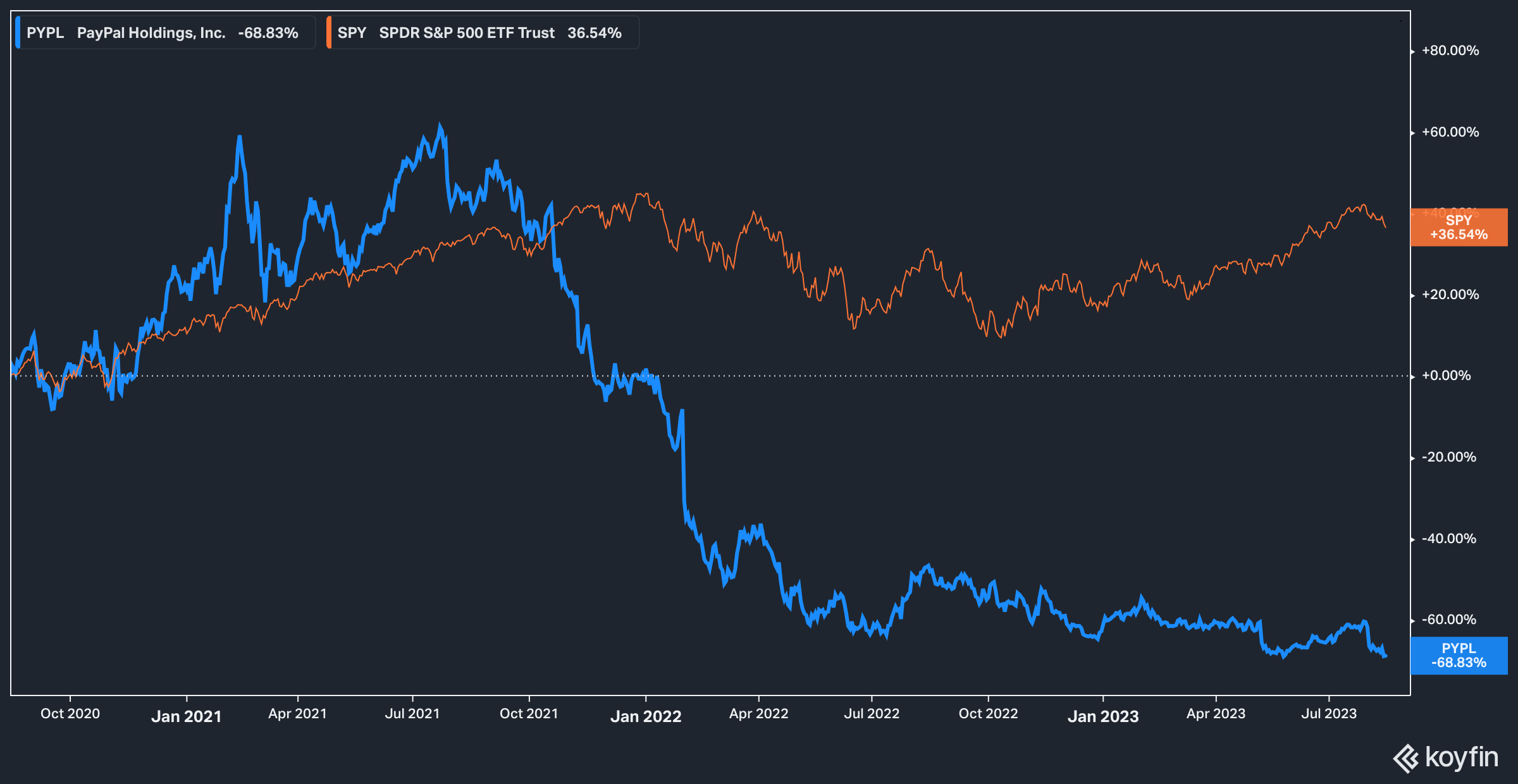

PayPal (NASDAQ:PYPL), the payments company founded by the ‘PayPal Mafia’ (a group of founders and early employees who went on to start their own high-profile companies such as LinkedIn, Tesla (TSLA), and others), has had a rough go of things in 2023, falling 16% year to date and 41% over the last twelve months.

Koyfin

Those with a longer time horizon are likely to be even more distressed–as pictured above, the stock has shed 68% of its value over the last three years. While of course much of this movement can be blamed on a rising interest rate environment and the subsequent flight of investors from growth stocks, the stock has also not been helped by the recent news that Paul Singer’s Elliott Management had dumped its stake in PayPal, or the fact that active users on PayPal’s core offerings have been slightly down for the past two quarters.

And yet, PayPal’s current situation seems to us a bit overblown. The company, after all, is quite profitable and has a robust suite of payment and wallet services business lines. The company recently entered into an agreement with private equity giant KKR (KKR) for the purchase of 40 billion euro’s worth of PayPal’s buy-now-pay-later receivables, and on August 14th it was announced that PayPal had found a replacement for CEO Dan Schulman in Intuit (INTU) executive Alex Chriss.

Oh, and did we mention that the company expects to repurchase $1 billion of its common stock in the rest of 2023 and commit $4-5 billion to repurchase shares in 2024?

With all of this considered, is it reasonable to say that the stock has fallen too far at this point? Let’s dive in.

Anemic Growth, or Strategic Thinking?

The obvious answer to that question is the fact that investors are likely to be unhappy with PayPal (or any company) whose core business appears to be flat or declining overall. The fact that an astute player like Elliott would dump its stake is likely in the forefront of many investors’ minds.

However, we think that readers would do well to consider that Elliott’s departure from PayPal may not be due to the fact that it made a mistake and that PayPal thus presents a poor investment–if Elliott didn’t want it, the thinking goes, why would I? Well, it often happens in the world of hedge funds that new opportunities come along which simply appear better or more timely in the eyes of its portfolio managers, or for any other number of reasons. PMs may assess overexposure in a particular sector and thus trim or eliminate a stock from their holdings which otherwise would stay. Funds may decide that their limited partners are simply not patient enough to wait out a turnaround effort.

In other words, while it is certainly notable that Elliott dropped its position, it is also unclear without insight into the firm’s investment process that the selling of the position was done because PayPal was a “bad investment.”

Second, it has been no secret that CEO Dan Schulman is preparing to move on from the company, announcing in February 2023 his intention to retire. For any company this creates a bit of a conundrum–current initiatives continue to be executed, but CEOs on the way out (responsible ones, at least) are generally loathe to radically overhaul portions of the business ahead of handing the reigns to their successor.

To support this point, Schulman has spent 2023 expanding and refining PayPal’s existing and more nascent business lines (such as merchant services and one-click wallet payments), without launching any sort of product or growth initiative which might be viewed unfavorably by his successor and cause investors a bit of CEO-transition whiplash.

Given all of the above, it is not surprising to us that the company has prioritized cost rationalization and profit maximization over all-out growth. Doing so prepares the company to be a leaner organization in the hands of new leadership. And we also remind readers that PayPal has not exactly turned in a disappointing performance on the revenue front–the company has posted high single-digit revenue growth using year-over-year comps for the last four quarters.

Others, of course, do not see things this way. They simply see a company failing to aggressively grow its user base, and which should therefore be dropped. We think that, in the near to intermediate term, they are likely to be proven wrong.

A New Stable Business?

We are not, generally speaking, fans of cryptocurrency in general in its current form. The space is rife with regulatory problems. Despite that, however, it is unlikely to go away, and the financial technology which has grown from the space will almost certainly endure.

The general lack of transparency in the space, particularly around stablecoins, means that PayPal’s recently announced stablecoin (dubbed ‘PayPal stablecoin‘) could be something of a game changer in the space.

Given the fact that PayPal is a publicly audited company, investors will have a bridge between the TradFi and DeFi worlds in the PayPal stablecoin–something which PayPal stands to gain from handsomely. A high-functioning, dollar-back stablecoin ecosystem is vital to the smooth functioning of cryptocurrency markets, and the introduction of a reputable player like PayPal is likely to give the industry a boost in terms of trust and transparency.

Of course, there are challenges. The coin will be issued by Paxos Trust Company, and that company will publish a monthly reserve report starting in September 2023 which will detail the holdings that back the stablecoin. The only problem we can see is that–like other stablecoins–the reserve report will only receive an attestation from a third-party auditor, rather than a full audit (the two types of review are quite different in scope and rigor).

Valuations and Cash Flows

It is our thesis that the wider market has now pushed down PayPal’s stock to a level beneath its intrinsic and historic value. We’ll start with valuations.

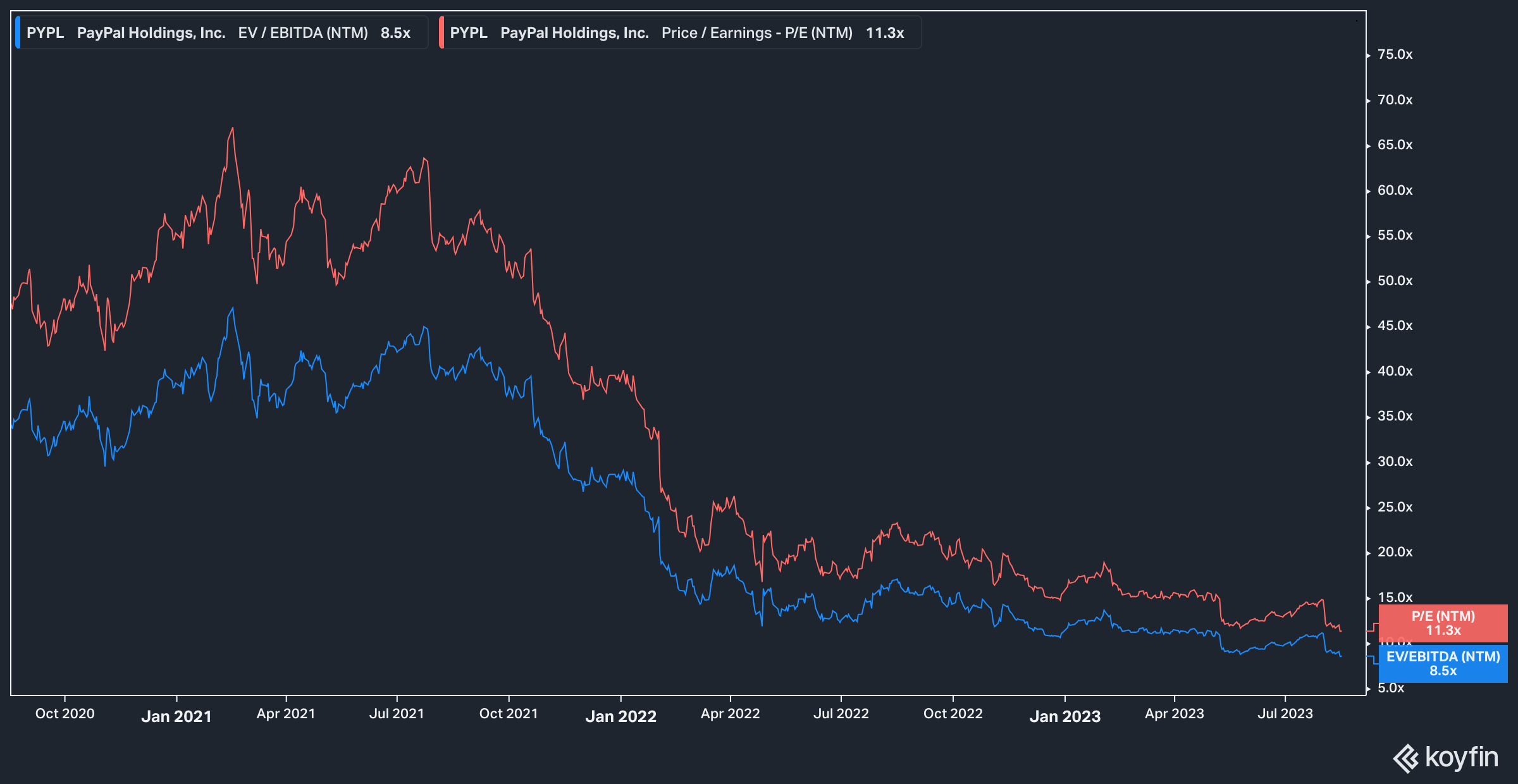

Koyfin

On a forward valuation basis, PayPal is plumbing new lows. From its wild valuation highs just over two years ago of more than 50x forward earnings, today the stock trades at just 11x forward earnings and 8.5x EV/EBITDA.

For context PayPal’s closest competitor in many spaces, Block (SQ), currently trades at 28x forward earnings and 20x EV/EBITDA. PayPal’s valuation today, in fact, trades more in line with Global Payments (GPN), a stock with half the market capitalization and a third of PayPal’s annual sales. Today, GPN trades at 11x forward earnings and 11x EV/EBITDA–a multiple higher than industry leader PayPal’s.

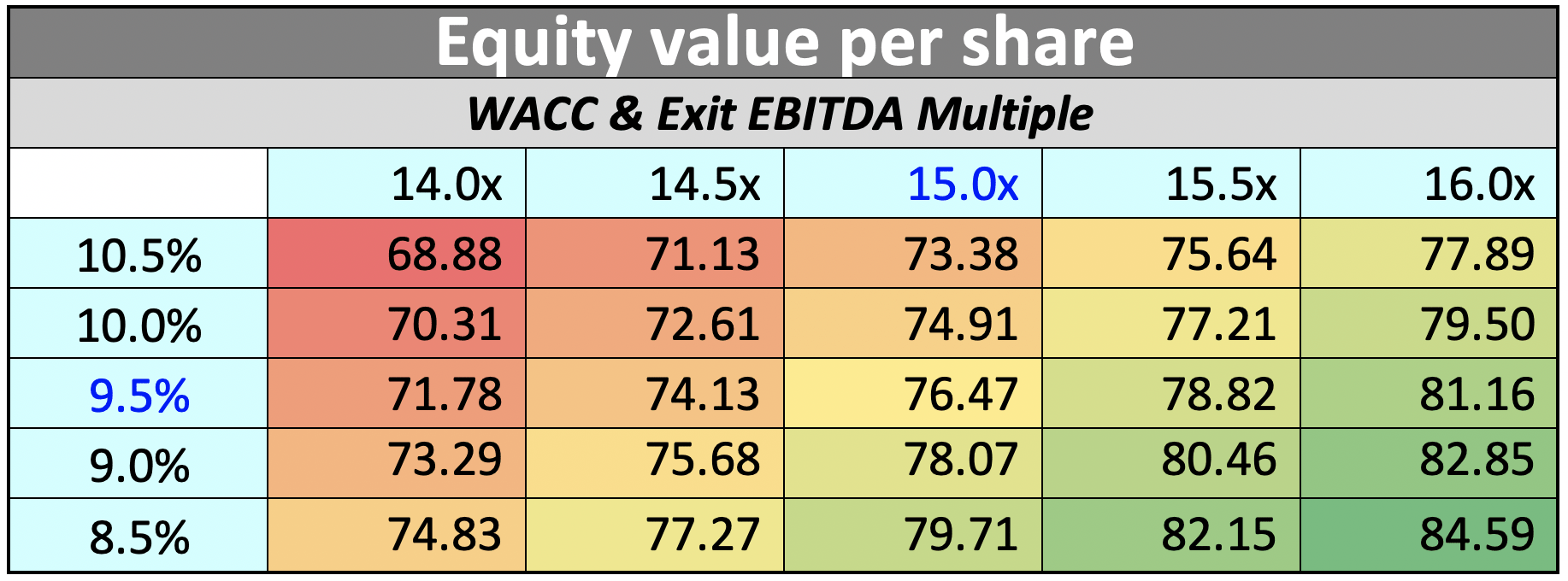

The stock also appears to be undervalued on an intrinsic basis as well. We modeled a discounted cash flow on the company which accounted for multiple factors, including the dilutive potential of outstanding stock awards and a 4% annual growth rate.

Author Calculations, Company Filings

Utilizing a 9.5% weighted average cost of capital [WACC] as our median assessment, and a target 15x EBITDA multiple, we estimate a fair value based on future cash flows for PayPal at roughly $76. We also note that our WACC assumption is on the more aggressive side, as the company issued 40-year bonds in May 2022 with a 5.32% effective rate.

Analysts on the street would also be likely to call our estimate conservative.

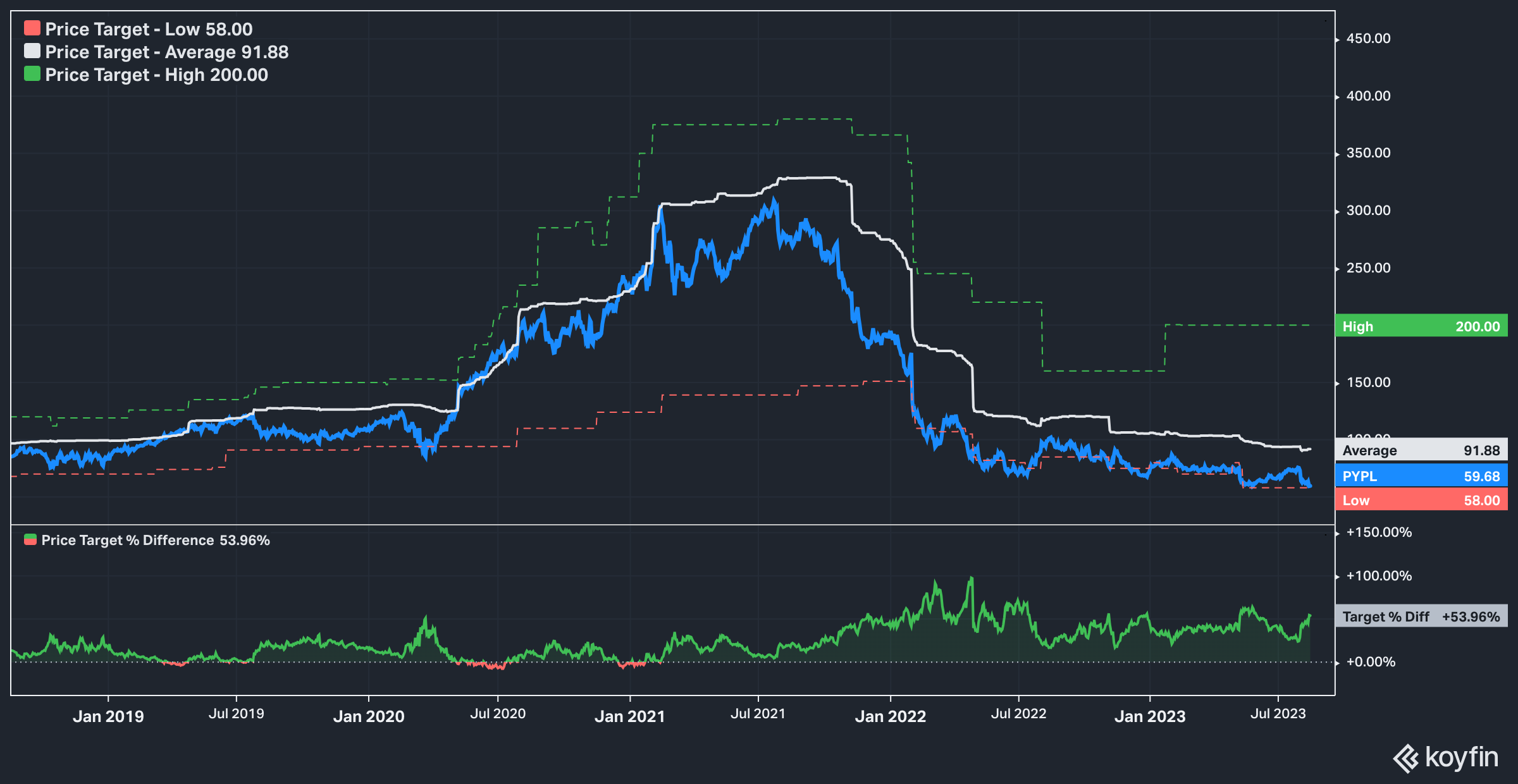

Koyfin

As of today the average analyst price target for PayPal sits at $91, 53% above current levels. For context with our model in the snapshot above, this target price correlates with a roughly 18x EBITDA multiple target.

The Bottom Line

PayPal is no longer a scrappy start-up, but rather a solid member of the payments world firmament–a fact that we believe the market seems to have forgotten. As such, we believe that its shares are currently undervalued, and that investors with the right time horizon and degree of investing patience have a high potential for reward. A primary risk to our thesis is a botched CEO transition, or a failure by the incoming leadership team to clearly articulate their value proposition to users and investors. Despite this, we believe that PayPal has robust offerings that are set to grow in the future, and that the market will eventually realize that the stock is fundamentally mispriced.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: The information contained herein is opinion and for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Factual errors may exist, and while they will be corrected if identified the author is under no obligation to do so. Author is also under no obligation to update changes of view. The opinion of the author may change at any time and the author is under no obligation to disclose said change. Nothing in this article should be construed as personalized or tailored investment advice. Before buying or selling any stock, you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal, and readers should not utilize anything in our research as a sole decision point for transacting in any security for any reason.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.