gk-6mt/iStock Editorial via Getty Images

Boeing (NYSE:BA) on Tuesday was downgraded to Underweight from a previous investment rating of Equal Weight by analysts at financial-services firm Wells Fargo. They said the aerospace and defense company faces longer-term pressure on its cash flow amid efforts to develop new aircraft.

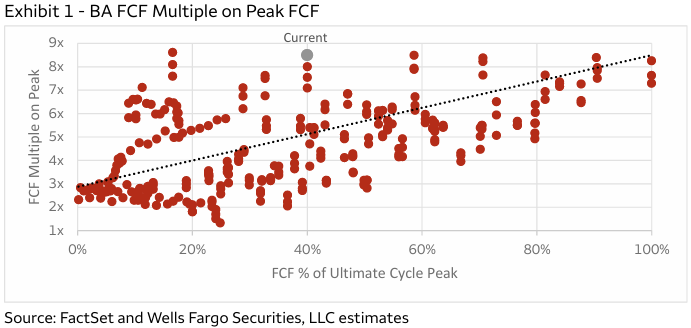

“Boeing (BA) had a generational free cash flow opportunity this decade, driven by ramping production on mature aircraft and low investment need,” Matthew Akers, analyst at Wells Fargo, said in a September 3 report. “But after extensive delays and added cost, we now see growing production cash flow running into a new aircraft investment cycle, capping FCF a few years out.”

The bank forecasts that Boeing’s (BA) free cash flow will peak in 2027 at less than the company’s prior target of $10 billion. Wells Fargo’s estimates for free cash flow are 15% to 20% below the average estimates among Wall Street analysts for 2026 to 2027.

“Boeing (BA) carries $45 billion net debt on its balance sheet, and we estimate paying this down would consume all of its cash through 2030,” according to Wells Fargo. “However, we doubt it can kick off a new aircraft program ($40 billion-plus investment) without first cleaning up its balance sheet.”

Wells Fargo forecasts that Boeing (BA) will need to issue more stock to raise $30 billion and improve its capital structure.

The bank cut its price target on Boeing (BA) to $119 a share from $185 a share previously, based on a multiple of 12 times peak cash, discounted to a year from today.

Boeing’s (BA) new chief executive, Kelly Ortberg, started on August 8. After a near-catastrophe on a Boeing (BA) 737 Max in January, the Federal Aviation Administration has capped output of the best-selling plane until the company shows improvements to safety and product quality.