Are household goods the new hyperscalers?

Looking at forward stock valuations, the premium investors have been paying for the megacap stocks has disappeared.

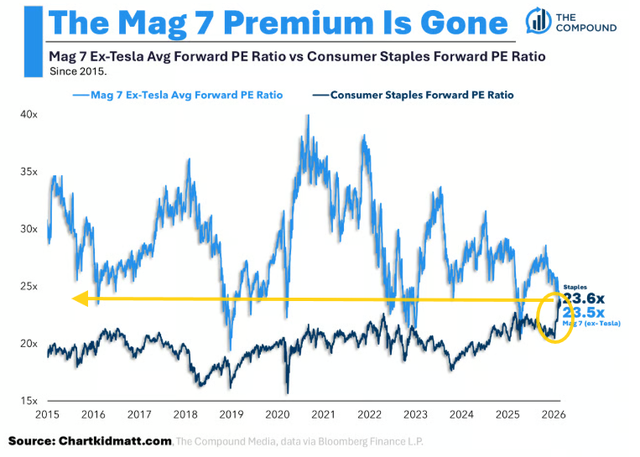

In a post, Neil Sethi of Sethi Advisors highlights a chart from Ritholtz Wealth Management’s Matt Cerminaro that says that as of Feb. 25, the average forward PE ratio of the Mag 7 (ex-Tesla) — Apple (AAPL), Amazon (AMZN), Alphabet (GOOG) (GOOGL), Meta (META), Microsoft (MSFT), Nvidia (NVDA) — is now below the Consumer Staples (XLP) sector.

“While Matt notes it has been slowly closing for a while, I can’t help but notice the sharp rise in the forward P/E for Staples to what is now the highest in at least a decade, while the top 6 have fallen to around the least in that time,” Sethi said.

Matt Cerminaro

“A lot of this is likely the Walmart (WMT) and Costco (COST) effect (they are 20% of XLP and trade at P/Es in the 40-50 range currently), but even there it seems things are quite stretched, and I have a hard time seeing most other Staples stocks suddenly becoming big earnings compounders.”

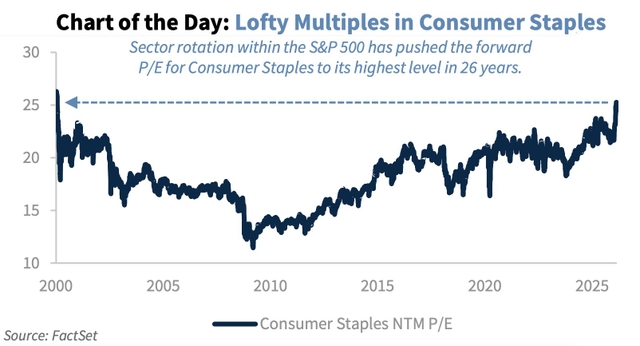

Raymond James CIO Larry Adams notes that Consumer Staples forward P/E has risen to 25x, which is “the highest level since 2000 and now the third-highest multiple among the S&P 500’s (SPY) (IVV) (VOO) 11 sectors.”

Raymond James