Summary:

- Alphabet is a strong buy ahead of earnings due to its 97% Ultra SWAN quality, hyper-growth dividend potential, and 22% discount to historical fair value.

- Expected returns: One-year 30%, two-year 52% (21% CAGR), and five-year 142% (19% CAGR), significantly outperforming the S&P.

- Key risks: Regulatory challenges, technological disruption, and intense market competition, but Alphabet’s exceptional risk management (89th percentile) and AA+ credit rating mitigate long-term concerns.

- Despite volatility, Alphabet’s current fundamentals suggest a 90% chance of generating 13%-26% long-term returns, with an 87% likelihood of outperforming the S&P over 50 years.

- The company’s $710 billion in growth spending, more than $500 billion in coming buybacks, and $315 billion in net cash by 2029 all bode very well for future dividend growth from this tech utility.

tiero

Bottom Line Up Front: Google Earnings Are On Tuesday, Oct. 29, It’s a Strong Buy You Don’t Want To Miss

There are three reasons why Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) is a strong buy, and you might want to buy ahead of earnings.

- 97% Ultra SWAN (sleep well at night) quality that keeps getting better (94% dividend safety).

- Hyper-growth dividend growth potential, as far as the eye can see.

- A world-class company at a 22% discount to historical fair value (coiled spring ready to soar).

Consensus Total Return Potentials

- Not a forecast.

- Consensus return potential.

- These are the expected returns if and only if these companies grow as expected and return to historical fair value by the end of 2026.

- Fundamentals would justify that.

2-Year Consensus Return Potential: 52% potential (21% CAGR) vs S&P 17% (8%)

FAST Graphs, FactSet

5-Year Consensus Return Potential: 142% (19% CAGR) vs 76% (12% CAGR) S&P.

FAST Graphs, FactSet

Alphabet’s Incredible Fundamentals Summary

Dividend Kings Zen Research Terminal

Reason 1: World-Class Ultra SWAN Quality

Alphabet’s new dividend is getting steadily safer as its cash flows and payout ratios remain shallow risk.

| Rating | Dividend Kings Safety Score (Over 1,000 Metric Model) | Approximate Dividend Cut Risk (Average Recession) | Approximate Dividend Cut Risk In Pandemic Level Recession |

| 1 – unsafe | 0% to 20% | over 4% | 16+% |

| 2- below average | 21% to 40% | over 2% | 8% to 16% |

| 3 – average | 41% to 60% | 2% | 4% to 8% |

| 4 – safe | 61% to 80% | 1% | 2% to 4% |

| 5- very safe | 81% to 100% | 0.5% | 1% to 2% |

| Alphabet | 94% | 0.5% | 1.30% |

| S&P Risk Rating | 89% Risk Management Percentile, Very Good | AA+ stable outlook credit rating = 0.29% 30-year bankruptcy risk | 20% or Less Max Risk Cap (each) |

Based on the Dividend King’s safety and quality model, which is calibrated to the S&P’s historical risk of dividend cuts in recessions and severe recessions since World War II, I estimate a 1.3% risk of GOOGL cutting its dividend even in another Pandemic or Great Recession level shock.

GOOGL Consensus Dividend Profile

| Year | Dividend | EPS | FCF Per Share | EPS Payout Ratio | FCF Payout Ratio | Dividend Cost (Billions) | Retained Earnings |

Retained Free Cash Flow |

| 2024 | $0.39 | $7.65 | $6.10 | 5.1% | 6.4% | $4,805.58 | $89,457.72 | $70,358.62 |

| 2025 | $0.52 | $8.68 | $7.39 | 6.0% | 7.0% | $6,407.44 | $100,547.52 | $84,652.14 |

| 2026 | $0.62 | $9.91 | $9.24 | 6.3% | 6.7% | $7,639.64 | $114,471.38 | $106,215.64 |

| 2027 | $0.66 | $11.53 | NA | 5.7% | NA | $8,132.52 | $133,940.14 | NA |

| Total/Annualized (2024 to 2027) | 19.2% | 14.7% | 23.1% | 3.9% | 2.4% | $26,985.18 | $438,416.76 | $261,226.40 |

(Source: FactSet)

GOOGL’s payout ratio is 5% to 7%, depending on the year, but that’s well below the 60% rating agencies consider safe for most industries.

GOOG is expected to grow the dividend at 19% annually through 2027 while retaining $261 billion in free cash flow after dividends and funding all operations and future growth.

Alphabet Balance Sheet Consensus Forecast

| Year | Total Debt (Millions) | Cash | Net Debt (Millions) | Interest Cost (Millions) | EBITDA (Millions) | Operating Cash Flow (Millions) |

| 2023 | $13,253 | $24,048 | -$97,663 | $308 | $120,517 | $84,293 |

| 2024 | $13,130 | $48,378 | -$101,786 | $1,780 | $147,474 | $108,438 |

| 2025 | $12,679 | $95,141 | -$117,199 | $2,842 | $168,202 | $122,916 |

| 2026 | $12,722 | $149,158 | -$147,432 | $3,598 | $190,690 | $138,293 |

| 2027 | $11,127 | $327,520 | -$285,043 | $268 | $214,272 | $156,187 |

| 2028 | $10,627 | $471,248 | -$345,067 | NA | $250,612 | $184,051 |

| 2029 | $10,127 | $641,556 | -$314,667 | NA | $291,745 | $213,716 |

| Annualized Growth (2023-2027) | -4.4% | 72.9% | 21.5% | -3.4% | 15.9% | 16.8% |

(Source: FactSet)

GOOG is expected to grow the most prominent net cash pile today into a $315 billion mountain of net cash by 2029.

GOOGL Buyback Consensus Forecast

| Year | Consensus Buybacks ($ Millions) | % Of Shares (At Current Valuations) | Market Cap |

| 2023 | $61,504 | 3.1% | $2,016,284 |

| 2024 | $60,234 | 3.0% | $2,016,284 |

| 2025 | $60,153 | 3.0% | $2,016,284 |

| 2026 | $61,443 | 3.0% | $2,016,284 |

| 2027 | $97,136 | 4.8% | $2,016,284 |

| 2028 | $116,027 | 5.8% | $2,016,284 |

| 2029 | $137,017 | 6.8% | $2,016,284 |

| Total 2024 through 2029 | $532,010 | 26.4% | $2,016,284 |

| Annualized Rate | 4.90% | Average Annual Buybacks | $88,668 |

(Source: FactSet)

GOOGL is expected to back $532 billion worth of stock through 2029, making the $315 billion net cash pile forecast by 2029 even more impressive.

- It bodes well for the rate of dividend growth.

| Year | Debt/EBITDA | Net Debt/EBITDA (3 Or Less Safe According To Credit Rating Agencies) |

Interest Coverage (8+ Safe) |

| 2023 | 0.11 | -0.81 | 273.68 |

| 2024 | 0.09 | -0.69 | 60.92 |

| 2025 | 0.08 | -0.70 | 43.25 |

| 2026 | 0.07 | -0.77 | 38.44 |

| 2027 | 0.05 | -1.33 | 582.79 |

| 2028 | 0.04 | -1.38 | NA |

| 2029 | 0.03 | -1.08 | NA |

| Annualized Change | -17.5% | 4.9% | 20.8% |

(Source: FactSet)

GOOGL’s balance sheet is a fortress that’s expected to strengthen over time.

| Rating Agency | Credit Rating | 30-Year Default/Bankruptcy Risk | Chance of Losing 100% Of Your Investment 1 In |

| S&P | AA+ Stable Outlook | 0.29% | 344.8 |

| Moody’s | Aa2 (A.A. equivalent) Stable Outlook | 0.51% | 196.1 |

| Consensus | AA+ Stable Outlook | 0.40% | 250.0 |

(Source: S&P, Moody’s)

The risk of buying GOOGL today, in terms of the risk of your investment going to zero in the next three decades, is estimated by rating agencies at 1 in 250.

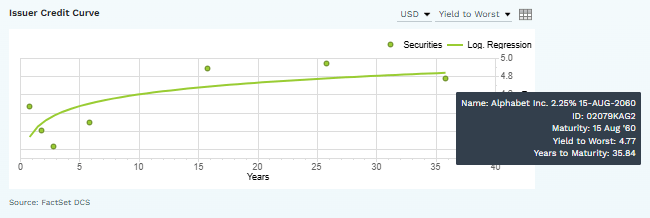

(Source: FactSet)

Google sold 40-year bonds in 2020 at a 2.25% yield.

Today, those bonds yield 4.77% after the Fed hiked by over 5%.

The U.S. government is unlikely to obtain 4.77% yields on 36-year bonds if it sells long-duration maturities.

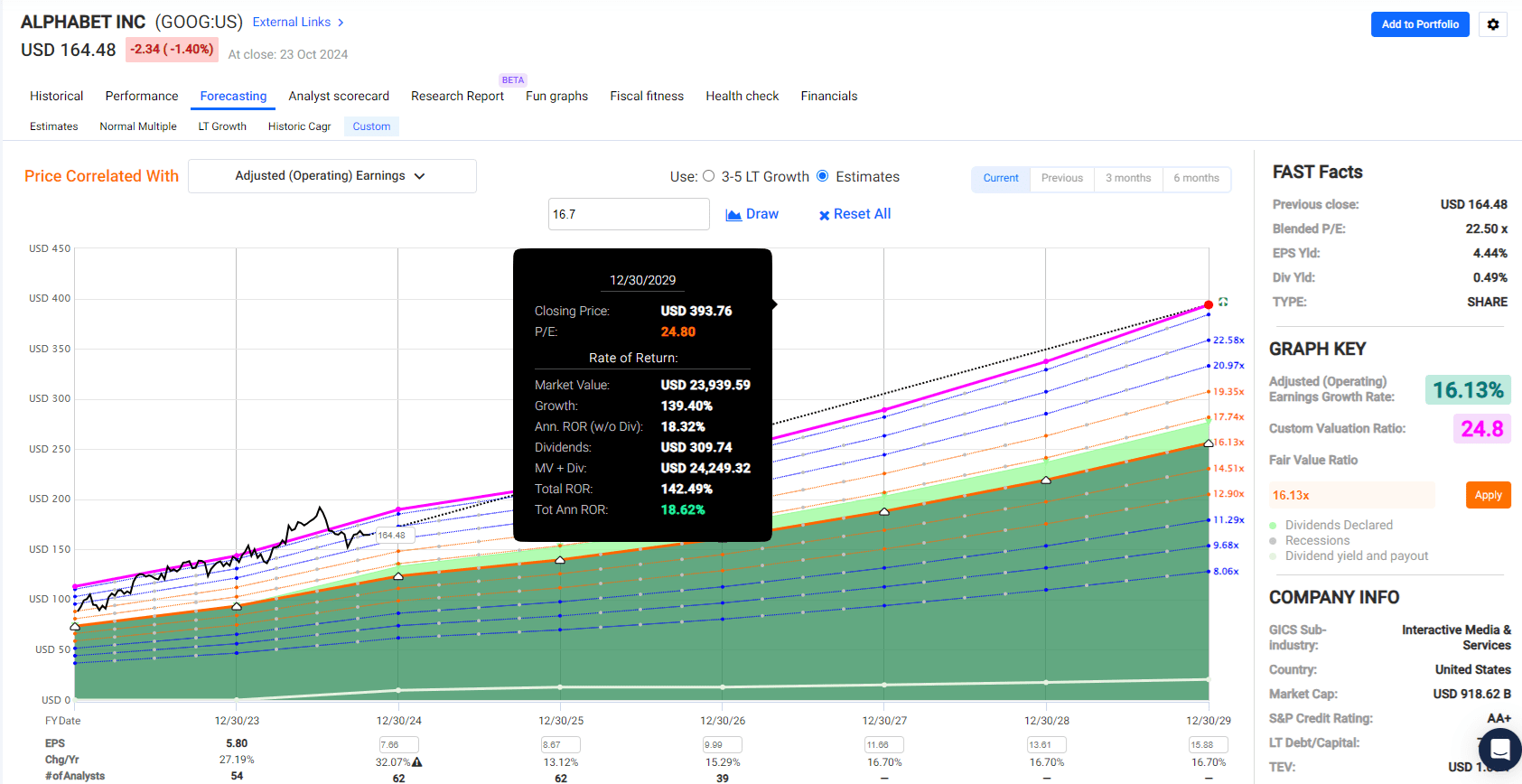

Reason 2: Incredible Dividend Growth Potential For Years To Come

GOOGL’s dividend could quickly grow faster than earnings for many years before the payout ratio reached levels that would impact dividend safety.

FactSet

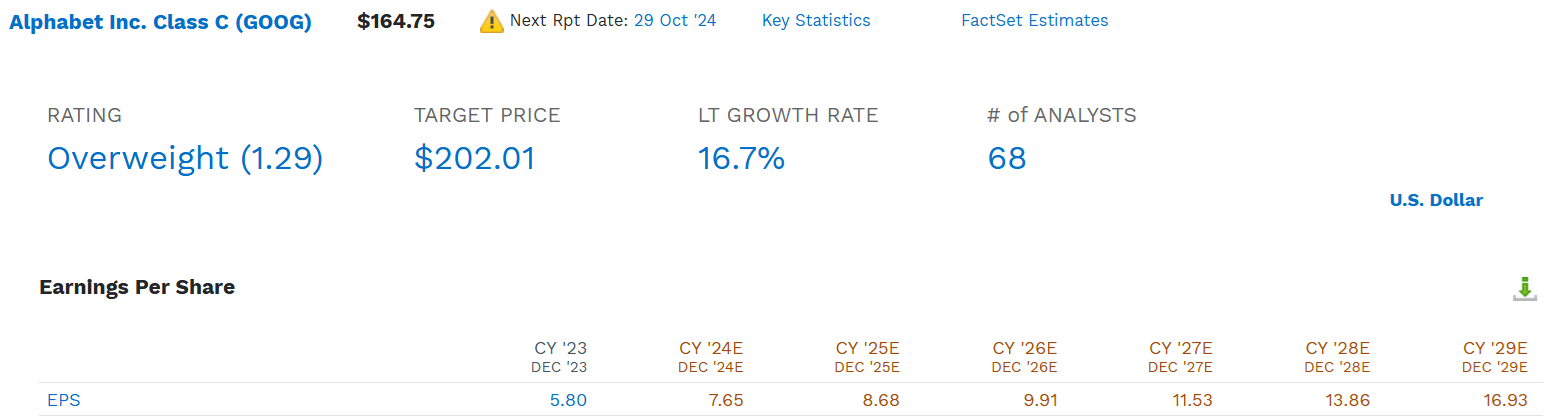

Analysts expect 16% to 17% long-term growth from GOOGL, with estimates ranging from 3% to 22.3% CAGR.

The median of 16.7% is after the Justice Department announced it would try to break up GOOGL.

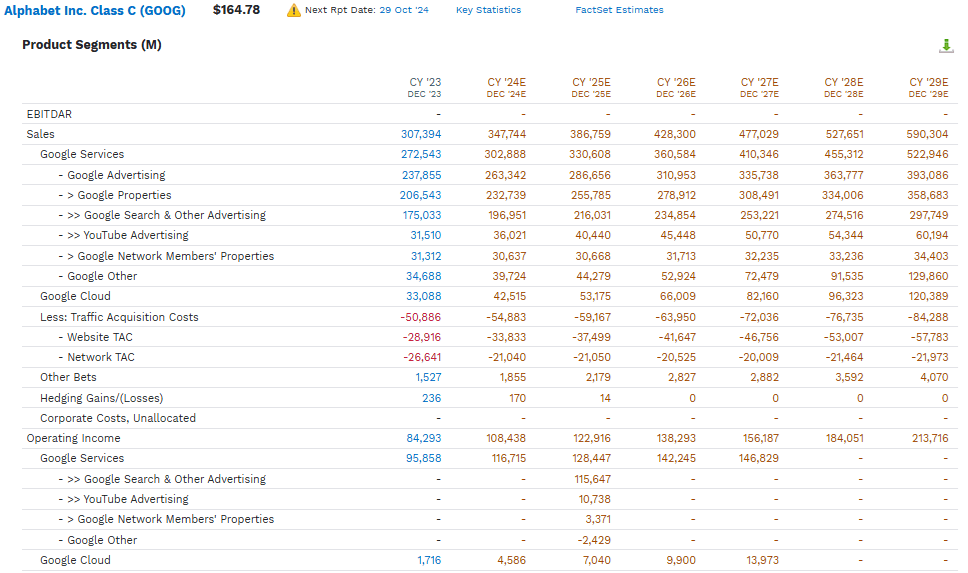

Medium-Term Growth Consensus

| Year | Sales | Free Cash Flow | EBITDA | EBIT (Operating Income) | Net Income |

| 2023 | $307,394 | $69,495 | $120,517 | $84,293 | $73,795 |

| 2024 | $347,744 | $76,707 | $147,474 | $108,438 | $95,810 |

| 2025 | $386,759 | $93,217 | $168,202 | $122,916 | $107,219 |

| 2026 | $428,300 | $113,911 | $190,690 | $138,293 | $119,723 |

| 2027 | $477,029 | $134,263 | $214,272 | $156,187 | $137,554 |

| 2028 | $527,651 | NA | $250,612 | $184,051 | $165,897 |

| 2029 | $590,304 | NA | $291,745 | $213,716 | $198,480 |

| Annualized Growth 2024-2029 | 11.5% | 17.9% | 15.9% | 16.8% | 17.9% |

| Cumulative 2024-2029 | $2,757,787 | $418,098 | $1,262,995 | $923,601 | $824,683 |

(Source: FactSet)

GOOG is expected to generate $825 billion in profit through 2029 on almost $3 trillion in sales, growing 11% to 12% annually.

Medium-Term Margin Consensus

| Year | Free Cash Flow Margin | EBITDA Margin | EBIT (Operating) Margin | Net Margin |

| 2023 | 22.6% | 39.2% | 27.4% | 24.0% |

| 2024 | 22.1% | 42.4% | 31.2% | 27.6% |

| 2025 | 24.1% | 43.5% | 31.8% | 27.7% |

| 2026 | 26.6% | 44.5% | 32.3% | 28.0% |

| 2027 | 28.1% | 44.9% | 32.7% | 28.8% |

| 2028 | NA | 47.5% | 34.9% | 31.4% |

| 2029 | NA | 49.4% | 36.2% | 33.6% |

| Annualized Growth | 5.6% | 3.9% | 4.7% | 5.8% |

(Source: FactSet)

GOOGL’s margins are expected to continue rising despite much higher growth spending.

That’s partly due to the rapid growth of Google Cloud, which only recently became profitable.

(Source: FactSet)

As GOOGL increases Google Cloud’s economies of scale, pre-tax profits are expected to rise from $1.7 billion in 2023 to $14 billion by 2027.

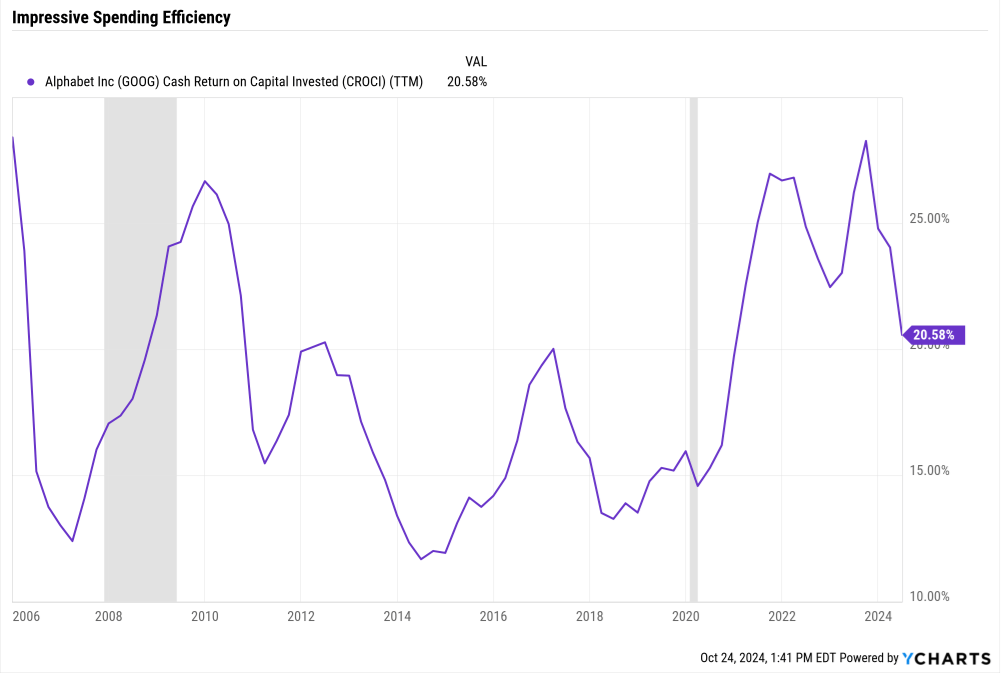

Ycharts

GOOGL’s free cash flow return on invested capital is 21% over the last year, including all the extra A.I. spending.

In other words, if GOOGL spends $100 billion on growth, the following year, it would be expected to earn $21 billion in additional free cash flow.

Medium-Term Growth Spending Consensus

| Year | Sales | R&D | Capex | Total Growth Spending | Growth Spending/Sales |

| 2023 | $307,394 | $45,427 | $32,251 | $77,678 | 25.3% |

| 2024 | $347,744 | $49,106 | $49,923 | $99,029 | 28.5% |

| 2025 | $386,759 | $53,821 | $53,879 | $107,700 | 27.8% |

| 2026 | $428,300 | $58,008 | $57,328 | $115,336 | 26.9% |

| 2027 | $477,029 | $64,332 | $59,552 | $123,884 | 26.0% |

| 2028 | $527,651 | $68,839 | $59,246 | $128,085 | 24.3% |

| 2029 | $590,304 | $75,488 | $61,088 | $136,576 | 23.1% |

| Annualized Growth | 11.49% | 8.83% | 11.23% | 9.86% | -1.46% |

| Total 2024-2029 | $2,757,787 | $369,594 | $341,016 | $710,610 | 25.77% |

| FCF Return On Invested Capital | 20.58% | 2030 Marginal FCF | $28,107 | ||

| 2029 FCF Consensus | $186,217 | 2030 Consensus FCF | $214,324 | ||

| 20-Year FCF Multiple | 28.54 | 2030 FCF Fair Value | $6,116,817 | ||

| Current Market Cap | $2,016,284 | Growth | 203.37% | ||

| Annualized Return Potential | 24.80% |

(Source: FactSet)

Buffett-like return potential from GOOGL is justified by incredible growth spending, good spending efficiency, and historical FCF multiples.

Reason 3: A Wonderful Company At A Wonderful Price

Dividend Kings Zen Research Terminal

GOOG is trading at a 22% discount to its 10-year average P.E.

It’s a potentially strong buy based on its quality, safety, and margin of safety.

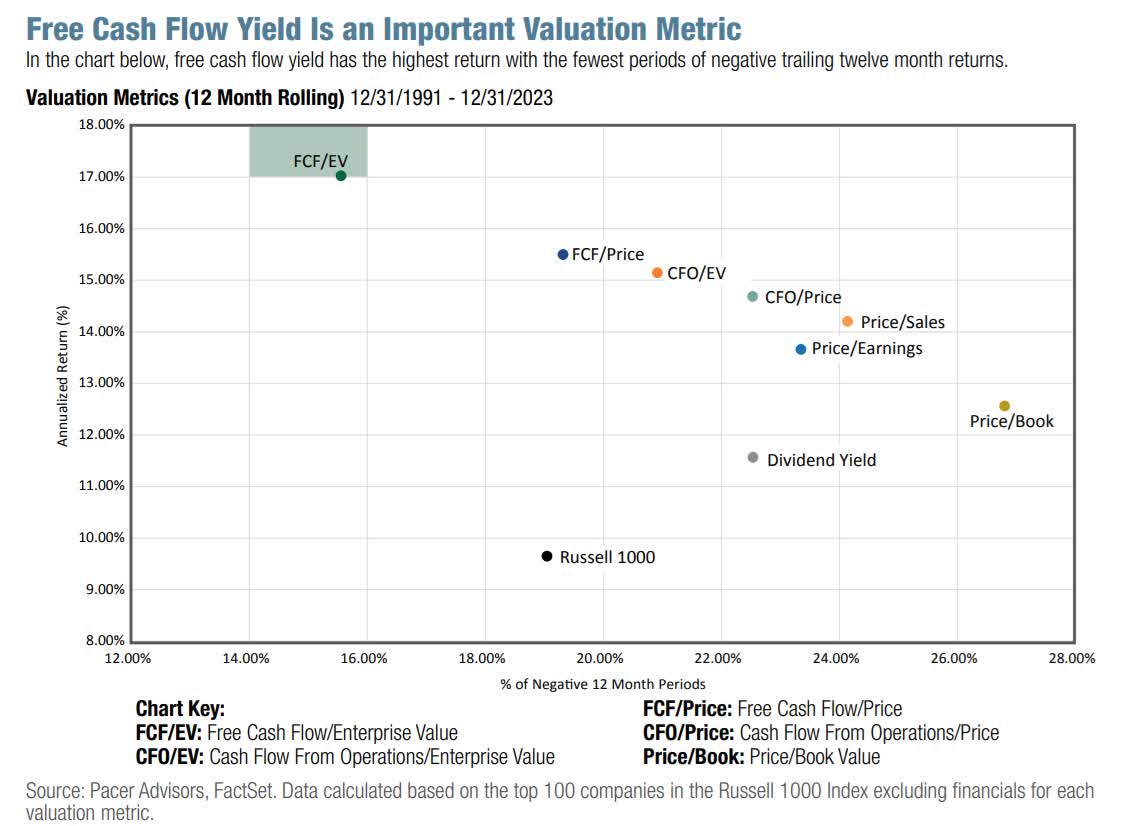

It’s trading at 32.4X EV/FCF, the most accurate valuation metric of the last 30 years.

Pacer Funds

Its PEGY ratio (EV/FCF Divided By Yield + Growth Consensus) is 1.89.

- S&P is 4.0X.

- Dividend aristocrats 4.4X.

It offers a 30% upside in the next year, which would be 100% justified by today’s fundamentals.

Risk Profile: Why Alphabet Isn’t Right For Everyone

GOOGL has three main risks to be aware of.

- Regulatory and Legal Challenges: Alphabet faces increasing regulatory scrutiny, particularly concerning antitrust issues. The U.S. Department of Justice has filed a lawsuit against Google for monopolizing digital advertising technologies, which could result in significant fines or operational changes if resolved unfavorably (or even breaking it up).

- Technological Disruption: The rapid advancement of A.I. technologies, such as OpenAI’s ChatGPT, threatens Google’s core search business. This disruption could significantly impact Alphabet’s revenue streams, as search-related advertising constitutes a significant portion of its income (77%).

- Market Competition: Alphabet competes with other tech giants like Amazon and Facebook in advertising, cloud services, and hardware markets. Intense competition could pressure margins and slow growth in these areas.

GOOG being broken up is not a risk to investors since any spinoffs would unlock value.

- YouTube could be worth $455 billion today (more than Netflix (NFLX)).

However, the risk of a breakup is that the value of GOOGL’s business and algos is based on data.

That’s likely why GOOGL management hasn’t broken up the company already.

For example, YouTube benefits from connecting to Gmail, which benefits Google Cloud enterprise customers.

In a world where data is king, access to the most data is a significant competitive advantage.

If GOOG is forced to break up and then cut off each part of the empire from the data of the other parts, then GOOGL’s wide moat could deteriorate quickly.

And that’s just one example of the significant risks it faces.

Long-Term Risk Management: Excellent

S&P has spent 25 years building the most comprehensive risk management model ever.

S&P

Each risk metric uses the No. 1 rated company in the industry (for that risk) as 100%.

So, every rating is compared to the industry’s gold standard company, which best manages that risk.

Then, the average of all the risk metrics creates an optimal risk management score that estimates “how close to perfect as is possible for a company in this industry to have.”

S&P rates over 13,000 companies for risk management, allowing us to see a percentile score that compares a company’s risk management to any other rated company, even in different industries.

| S&P LT Risk Management Score | Rating |

| 0% to 9% | Very Poor |

| 10% to 19% | Poor |

| 20% to 29% | Suboptimal |

| 30% to 59% | Acceptable |

| 60% to 69% | Good |

| 70% to 79% | Very Good |

| 80+% | Exceptional |

| Alphabet | 67% |

| Global Percentile | 89% (top 11% of global companies) |

(Source: S&P)

Context Makes All The Difference: Just How Good Is Alphabet’s Risk Management?

| Company | Average S&P LT Risk Management Percentile |

| British American Tobacco | 100% |

| Alphabet | 89% |

| Nvidia | 88% |

| T.C. Energy | 88% |

| Foreign Dividend Stocks | 87% |

| Strong ESG Stocks | 87% |

| Dividend Kings Top Buy List | 83% |

| My Top 5 Blue-Chip Bargains For October | 81% |

| 7% Yielding Low Volatility Aristocrats | 81% |

| Ultra SWAN List | 79% |

| Low Volatility Stocks List | 75% |

| Chevron | 75% |

| Enbridge | 74% |

| US Stocks | 73% |

| Dividend Kings | 71% |

| Hypergrowth Stocks List | 68% |

| Dividend Aristocrats | 67% |

| Monthly Dividend Stocks | 51% |

| Amazon | 50% |

(Source: Dividend Kings Zen Research Terminal, S&P)

GOOG is the 152nd best company at managing its risk in the DK 500 Master list. And as you can see, GOOG’s long-term risk management is exceptional.

Combined with its AA+ credit rating, this should give long-term income growth investors confidence that any investment made today is highly unlikely to lose money in the coming decades.

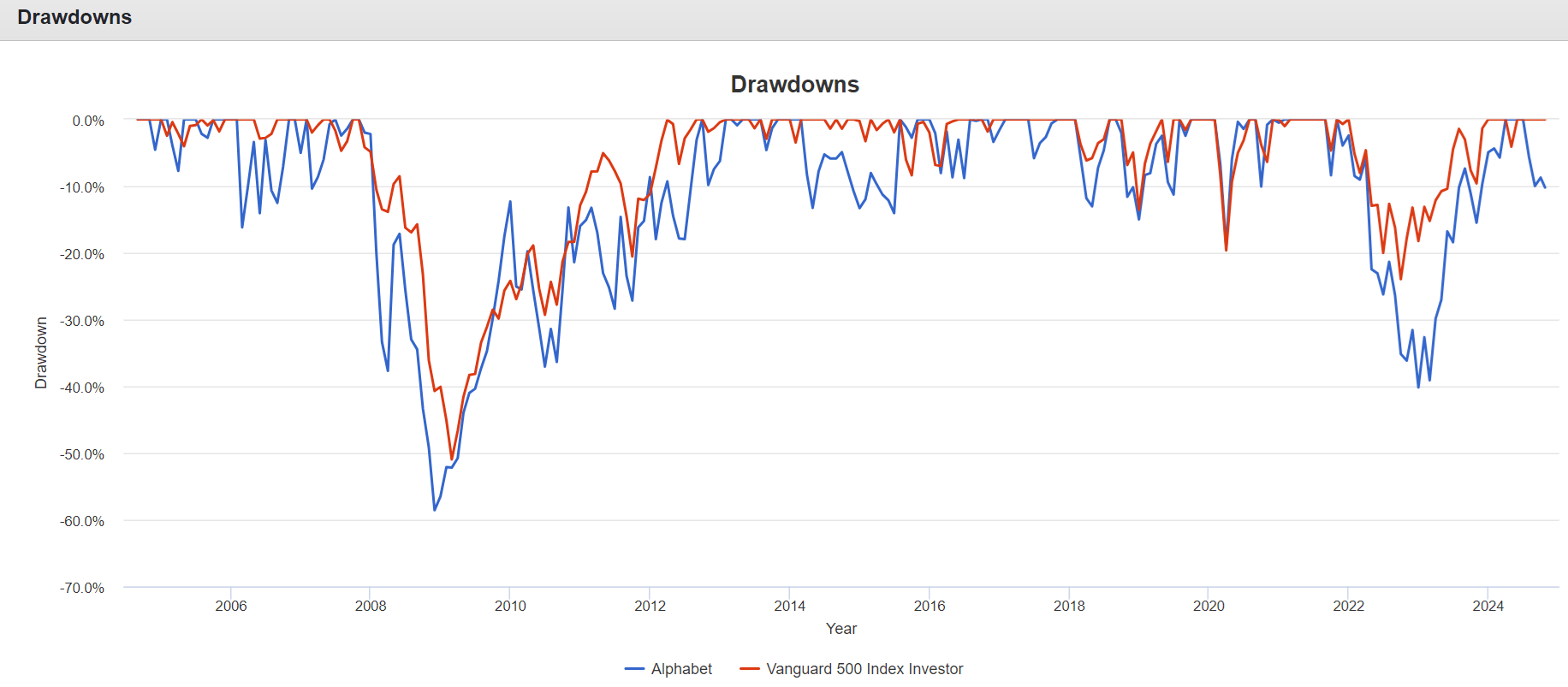

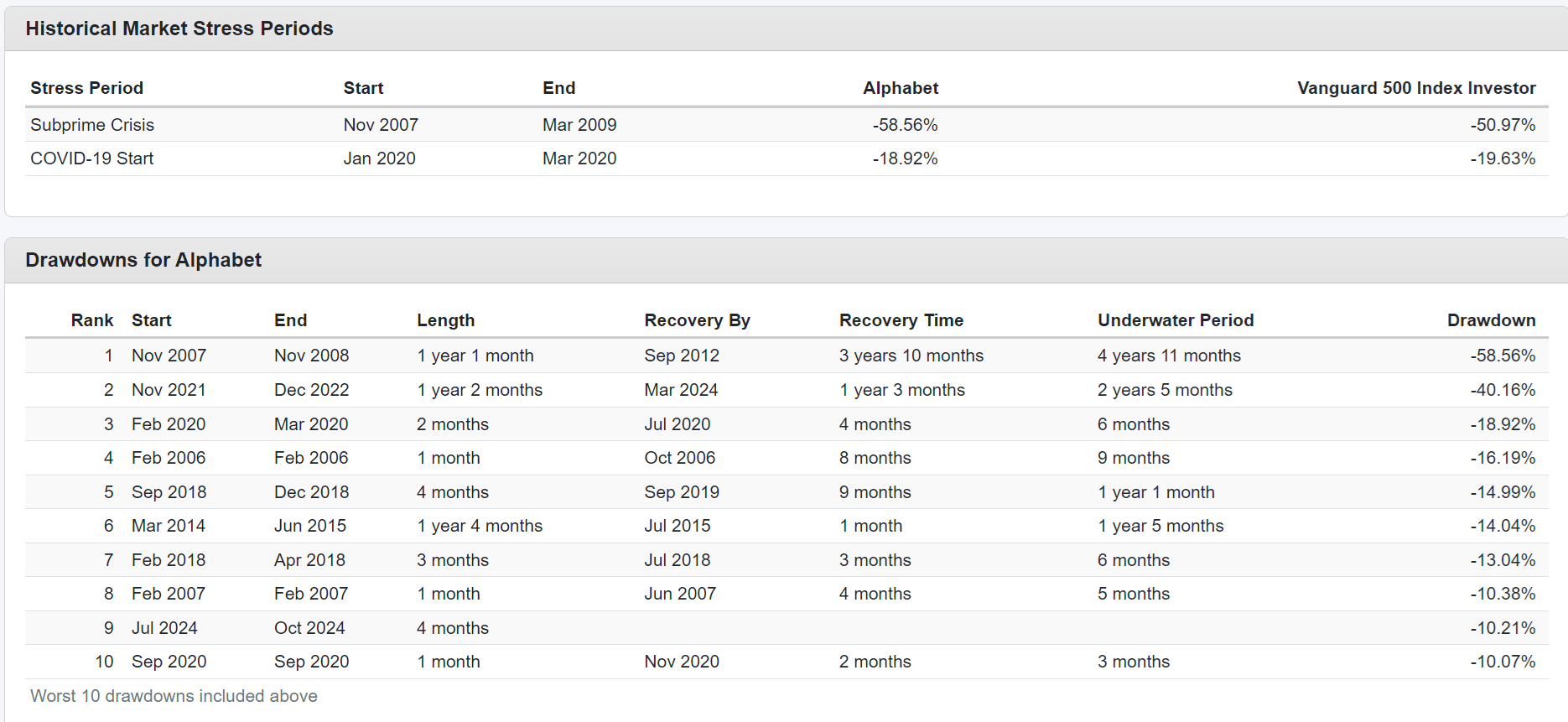

Historical Volatility Profile: The Kind of Volatility You Should Be Prepared For If You Own GOOGL

Portfolio Visualizer

Portfolio Visualizer

GOOG is capable of frightening bear markets.

5 Worst Years Since 2004 IPO

| Year | Return | Return |

| 2008 | -55.51% | -37.02% |

| 2022 | -38.67% | -18.23% |

| 2014 | -5.97% | 13.51% |

| 2010 | -4.20% | 14.91% |

| 2018 | -1.03% | -4.52% |

| Average | -12.47% | 1.42% |

| Median | -5.09% | 4.50% |

(Source: Portfolio Visualizer)

When GOOG is down, the market is usually flat, and in bear markets, it often falls much more than the market.

5 Best Years Since 2004 IPO

| Alphabet | Vanguard 500 Index Investor | |

| Year | Return | Return |

| 2005 | 115.19% | 4.77% |

| 2009 | 101.52% | 26.49% |

| 2004 | 88.33% | 10.37% |

| 2021 | 65.17% | 28.53% |

| 2023 | 58.83% | 26.11% |

| Average | 85.81% | 19.25% |

| Median | 88.33% | 26.11% |

(Source: Portfolio Visualizer)

In 2008, GOOGL fell over 50%. And it broke even the following year, with a 102% rally, 4X better than the S&P.

- The upside of downside volatility.

5% Worst Months Since 2004 IPO

| Alphabet | Vanguard 500 Index Investor | ||

| Year | Month | Return | Return |

| 2008 | 11 | -18.48% | -7.17% |

| 2008 | 1 | -18.39% | -6.02% |

| 2022 | 4 | -17.67% | -8.73% |

| 2008 | 2 | -16.50% | -3.25% |

| 2006 | 2 | -16.19% | 0.26% |

| 2010 | 1 | -14.52% | -3.60% |

| 2008 | 9 | -13.55% | -8.91% |

| 2020 | 3 | -13.18% | -12.37% |

| 2022 | 12 | -12.54% | -5.77% |

| 2022 | 9 | -11.91% | -9.22% |

| 2006 | 5 | -11.04% | -2.90% |

| 2011 | 8 | -10.39% | -5.45% |

| Average | -14.53% | -6.09% | |

| Median | -14.04% | -5.90% |

(Source: Portfolio Visualizer)

The average 5% worst months for GOOG is a 15% decline.

The worst monthly decline is nearly 20%.

5% Best Months Since 2004 IPO

| Alphabet | Vanguard 500 Index Investor | ||

| Year | Month | Return | Return |

| 2004 | 10 | 47.10% | 1.51% |

| 2008 | 4 | 30.38% | 4.85% |

| 2004 | 9 | 26.60% | 1.07% |

| 2005 | 5 | 26.03% | 3.17% |

| 2007 | 10 | 24.63% | 1.58% |

| 2005 | 4 | 21.88% | -1.91% |

| 2015 | 7 | 20.19% | 2.08% |

| 2011 | 7 | 19.22% | -2.05% |

| 2006 | 10 | 18.53% | 3.25% |

| 2013 | 10 | 17.66% | 4.59% |

| 2005 | 10 | 17.59% | -1.68% |

| 2010 | 9 | 16.84% | 8.92% |

| Average | 23.89% | 2.12% | |

| Median | 21.04% | 1.83% |

(Source: Portfolio Visualizer)

Big sell-offs in GOOGL are a gift as long as the investment thesis doesn’t break.

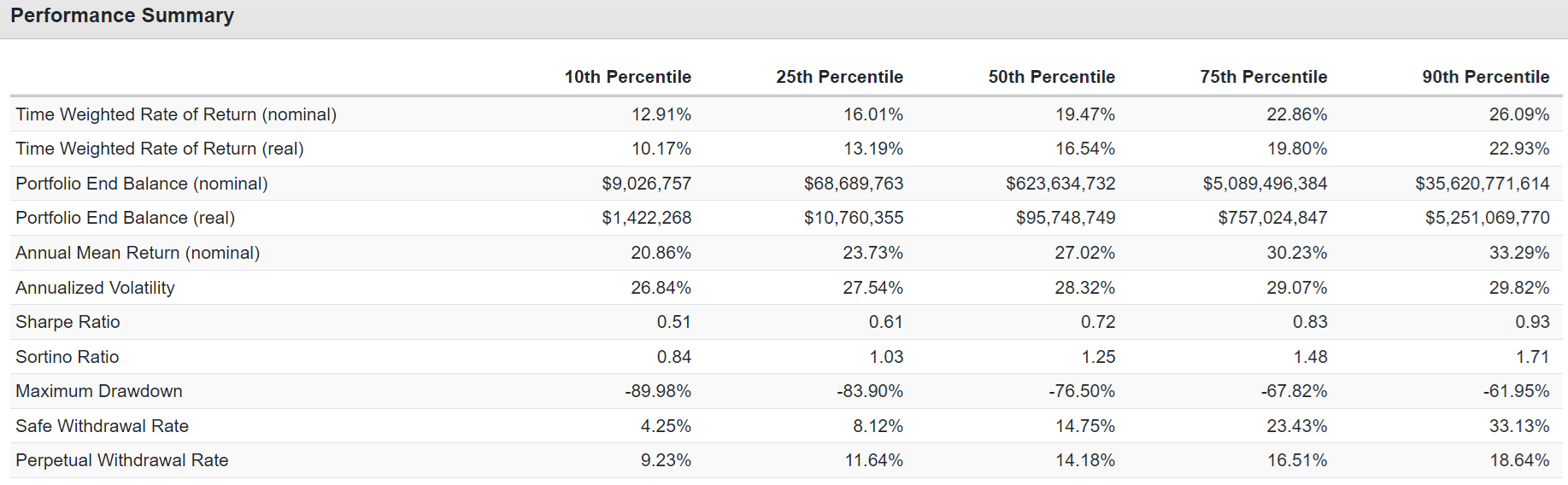

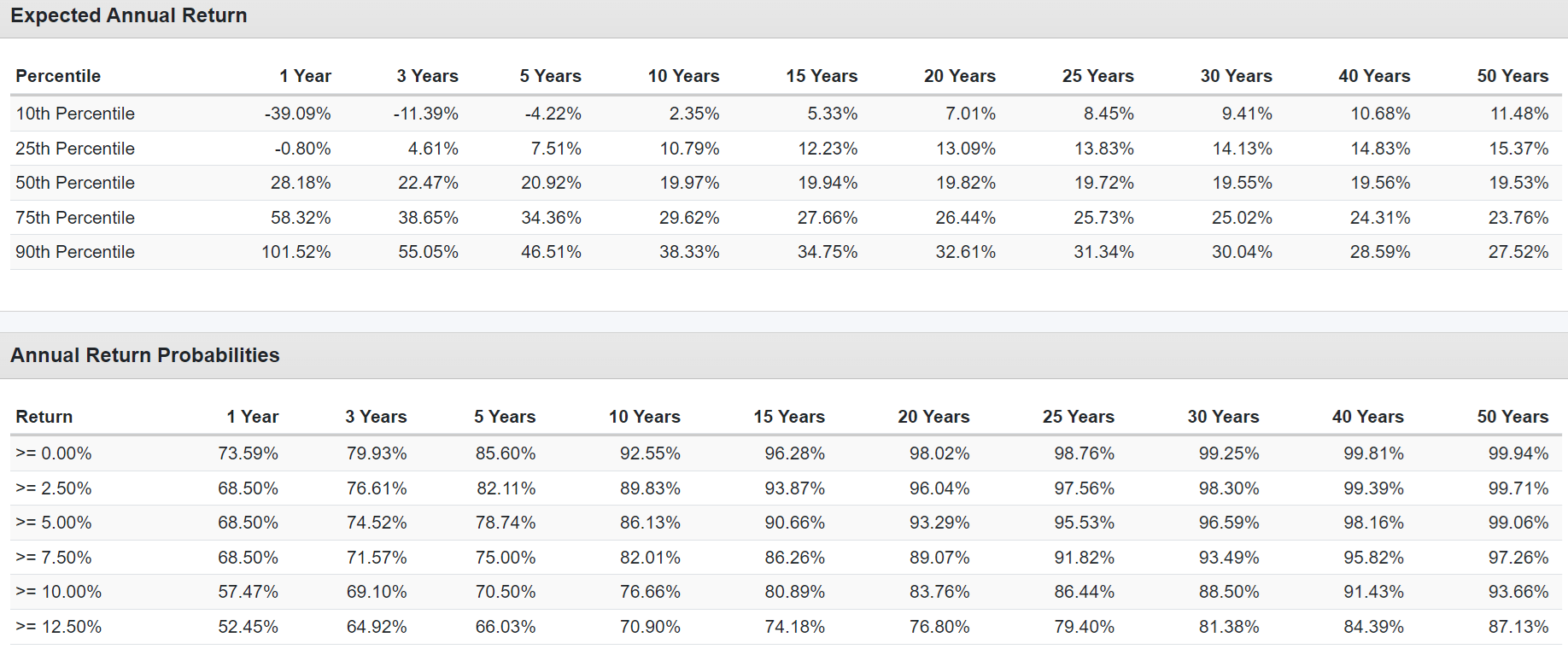

75-Year Monte Carlo 10,000 Simulation Summary (Today’s Fundamentals)

Portfolio Visualizer

GOOGL is 90% statistically likely to generate 13% to 26% returns in the future, including a potential 77% decline at some point.

Portfolio Visualizer

If today’s fundamentals persist for the next 50 years, GOOGL is 87% likely to beat the S&P’s historical 10% returns.

Bottom Line: Alphabet Is A Strong Buy Before Earnings, A Coiled Spring That’s Likely Set To Soar

GOOGL, ahead of earnings, offers impeccable quality, extraordinary value, and hyper-income growth potential.

- 0.5% yield (very low risk, 94% safety score).

- 16.7% long-term growth consensus (17.2% income growth consensus).

- 23% historical discount vs 7% S&P premium.

- AA+ credit rating (.29% 30-year bankruptcy risk).

- 89th percentile long-term risk management (top 11% of global companies).

- 30% upside potential in the next year.

- 21% CAGR return potential over the next 2 years.

- 144% upside return potential in the next 5 years (18% CAGR).

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

—————————————————————————————-

Dividend Kings helps you determine the best safe dividend stocks to buy via our Automated Investment Decision Tool, Zen Research Terminal, Correction Planning Tool, and Daily Blue-Chip Deal Videos.

Membership also includes

-

Access to our 14 model portfolios.

-

my family’s real money $3.3 million ZEUS Family Fund.

-

50% discount to iREIT (our REIT-focused sister service)

-

real-time chatroom support

-

real-time email notifications of all my family portfolio buys

-

numerous valuable investing tools

Click here for a two-week free trial, so we can help you achieve better long-term total returns and your financial dreams.