Summary:

- Following an eye-watering rally earlier this year, the SMCI stock has now flipped to YTD declines as it faces continued implications of ongoing accounting woes.

- In the latest turn of events, SMCI’s auditor, Ernst & Young, has resigned from the engagement. This casts further uncertainties on when investors can expect SMCI’s delayed 10-K filing.

- In the meantime, SMCI bulls continue to believe that the company’s accounting problems and delayed 10-K filing are isolated issues from its technological advantage in capturing AI opportunities.

- However, SMCI’s delayed 10-K filing alone (even if without material misstatements) has adverse cascading effects on its operations, which are fast approaching yet remain underappreciated by the market at current levels.

JHVEPhoto

The Super Micro Computer stock (NASDAQ:SMCI) has traded down by more than 40% after Ernst & Young (EY) resigned from the audit engagement on October 30. The stock has lost more than 40% of its value over the past two days, effectively erasing all of its year-to-date gains of more than 4x at its peak in mid-March. EY’s resignation marks the latest development in SMCI’s ongoing accounting woes. The company announced the delayed filing of its FY2024 10-K on August 30th, citing issues in assessing the “effectiveness of its internal controls over financial reporting as of June 30, 2024”. It is also currently being probed by the Justice Department on allegations of accounting rule violations.

Unfortunately, it is not SMCI’s first rodeo involving accounting and disclosure deficiencies. As we have discussed in a recent analysis, the company was fined $17.5 million by the SEC in 2020 for “prematurely recognizing revenue and understating expenses from at least fiscal year (FY) 2015 through FY 2017”.

In the meantime, SMCI bulls remain confident in the company’s technological advantage amid the ongoing AI transformation. The basis of the argument is that SMCI’s ongoing accounting woes and auditor resignation have no direct interference with the company’s day-to-day operations and its mission-critical role in enabling next-generation AI developments.

However, we see three significant imminent risks facing SMCI’s operations as a direct result of its ongoing financial reporting uncertainties, which should not be overlooked – 1) delisting risks; 2) liquidity risks; and 3) fundamental risks.

All of which could lead to substantial market share loss for SMCI amidst intensifying competition in the AI server market, and yield an unfavourable fundamental impact to the company’s outlook. As a result, we believe the immediate risks facing SMCI remain substantially skewed to the downside, with the stock likely to face further volatility ahead.

Delisting Risks

As a result of SMCI’s delayed FY2024 10-K filing, the company has received a “Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard” from Nasdaq in mid-September. The notice stipulates that the company must submit a remediation plan within 60 calendar days from the date of which the notice was received. If the plan is accepted, then Nasdaq could grant an extended filing period of “up to 180 calendar days from the filing’s due date” for SMCI’s listing to regain compliance.

The SEC requires large accelerated filers like SMCI to submit their Form 10-K within 60 days after their fiscal year-end. For SMCI, that deadline was August 30, which coincided with the company’s announcement of its delayed filing. Add 180 calendar days on top of that, SMCI has until the end of February 2025 – or about four months from now – to file its FY2024 10-K before being delisted from Nasdaq, on failed compliance with listing rules.

That may sound like a long time from now, with the expectation that Nasdaq will grant the 180-day extension. But with EY having resigned from the engagement, SMCI faces a long road from finding a new external auditor to having its books and internal controls reassessed to ensure that its financial statements are fairly presented without material misstatements.

A year-end audit engagement is a lengthy, year-long process that starts with risk assessment procedures to identify the scope of financial accounts required for independent assessment. Then the remainder of the year is spent on designing the assessment procedures, determining the population and/or sample of accounts to be assessed, and performing the required assessments to determine if the financial statements are fairly presented and free from material misstatements.

The two to three months after the company’s fiscal year-end are typically a time crunch to have the audit finalized. The process is often deemed “busy season” for external auditors, given the compressed timeframe to review financial figures disclosed in the company’s year-end earnings press release, while also completing every audit assessment remaining in the engagement before the SEC filing deadline – even with reliance on work already performed throughout the earlier parts of the year. Suddenly, four months does not sound like a long time after all, given the extent of work SMCI still has to go through successfully in order to stay compliant with Nasdaq listing rules.

In addition to the lengthy audit process, SMCI might also have difficulty finding an appropriate external auditor to take up its year-end audit. Specifically, auditor turnover does not happen frequently amongst large, established public companies. Close to 40% of S&P 500 constituents have kept the same auditor for more than five decades. Meanwhile, less than a tenth of companies have been found to “change auditors every decade”.

In SMCI’s case, finding a successor to EY will mark the server maker’s third auditor within the decade. Deloitte was previously SMCI’s auditor for more than a decade, with the auditor having signed off the FY2023 10-K for the company as its last. EY was subsequently hired for the FY2024 audit before resigning from the engagement on October 30. As a result, it likely will not be a swift and smooth process for SMCI to engage a new external auditor without heightened due diligence performed by the latter. This accordingly amplifies delisting risks facing SMCI.

Liquidity Risks

Liquidity risks is one of the major problems stemming from SMCI’s delayed FY2024 10-K filing, which remains underappreciated by investors, in our opinion.

Implications on Outstanding Term Loans

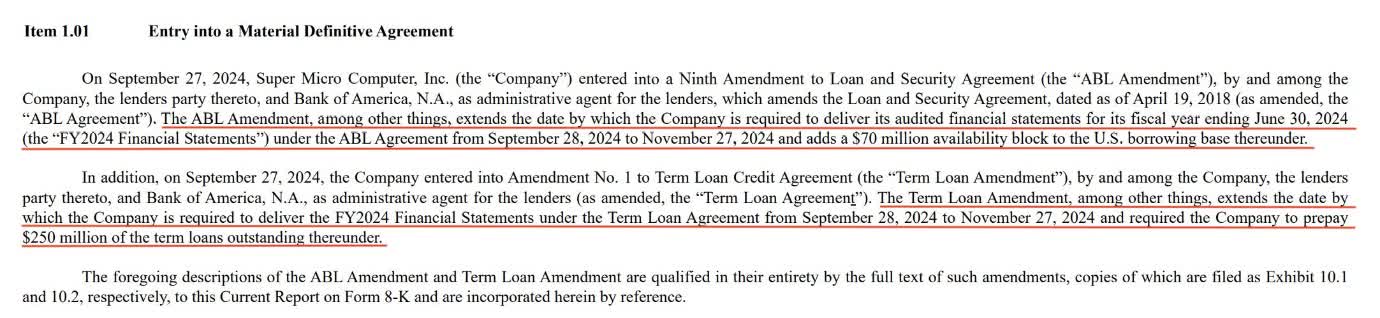

Based on the Form 8-K filed on September 27, SMCI has entered into an amended loan agreement with lenders of its outstanding term loans and credit facilities to extend its 10-K filing deadline. The company now has until November 27 to file its FY2024 10-K and prevent a breach of the amended lending terms. The extension had cost SMCI a $250 million prepayment on its $476.4 million of outstanding term loans as at June 30, 2024 – or 15% of SMCI’s cash balance as of its FY2024 year-end reporting date. A $70 million availability block was also placed on SMCI’s undrawn credit facilities.

SMCI 8-K Filing, September 27, 2024

Although management has repeatedly claimed that they do not expect “material changes” to the figures disclosed in SMCI’s August year-end earnings press release, a further delayed 10-K filing has substantial fundamental implications. While the $250 million term loan prepayment could be temporary, assuming the FY2024 10-K is filed by November 27, it remains an adverse cash implication for SMCI’s current operations, nonetheless. In the event of breach due to failure to file by November 27, SMCI may be required to repay its outstanding term loans in full.

Admittedly, SMCI has sufficient cash on its balance sheet to repay the outstanding $476.4 million of term loans and lines of credit in full. But this is likely to have an adverse impact on liquidity needed to fund ongoing operations. The amount represents almost a third of its cash on hand and 75% of its quarterly operating cash spend run-rate observed in fiscal 4Q24.

There are also likely additional adverse implications facing SMCI’s term loan agreement in the event of a delayed fiscal 1Q25 10-Q filing, which is probable in our view. The SEC requires large accelerated filers like SMCI to file their Form 10-Qs within 40 days of the reporting date. That is in about a week for SMCI, given its fiscal 1Q25 ended on September 30th. SMCI has only recently disclosed that it will press release its fiscal 1Q25 results on November 5, though whether the company plans to file the 10-Q on the same day remains uncertain. With its external auditor having resigned, it is unlikely that SMCI will be able to have its 10-Q reviewed and signed off before the SEC’s required deadline, in our opinion.

Implications on Outstanding Convertible Notes

In addition to its existing term loans, SMCI’s delayed 10-K (and potentially 10-Q) filing also levies adverse implications on its outstanding convertible notes issued in February. Much of SMCI’s cash balance of $1.669 billion reported in its FY2024 press release were generated from the $1.725 billion Convertible Senior Notes issued in February. But this liability could be at risk of being called in cash – not in shares – as a result of rippling effects from SMCI’s delayed filings of its annual and quarterly financial statements. This would result in substantial liquidity risks for SMCI – especially if it also has to pay up on the outstanding term loans.

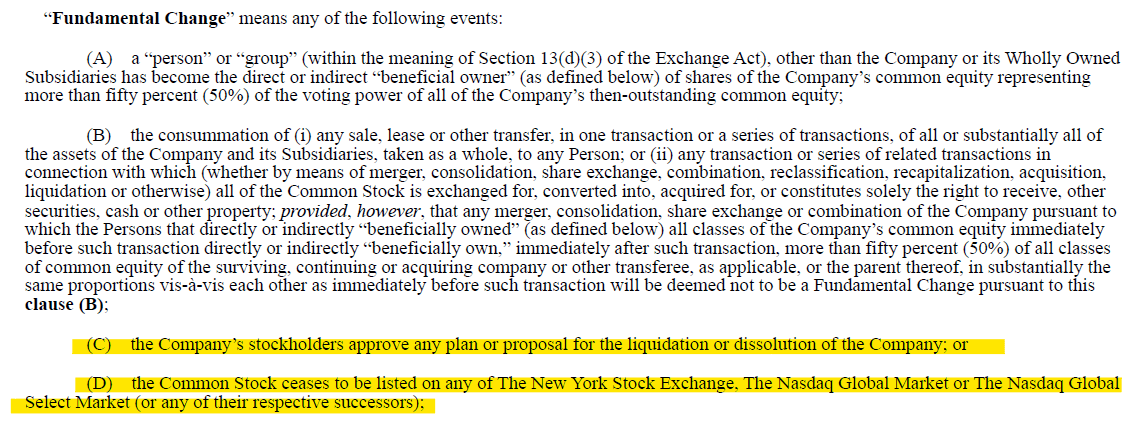

The indenture on the convertible notes states that holders may demand SMCI to repurchase for cash upon a “fundamental change” event:

Subject to certain exceptions, holders may require the Company to repurchase, for cash, all or part of their Convertible Notes upon a “Fundamental Change” (as defined in the Indenture) at a price equal to the principal amount of the Convertible Notes being repurchased plus any accrued and unpaid special interest and additional interest, if any, up to, but not excluding, the “Fundamental Change Repurchase Date” (as defined in the Indenture).

Source: SMCI Form 8-K, February 22, 2024

A fundamental change event, as defined in the indenture on the convertible notes, includes a delisting of SMCI’s shares and a liquidation event – which are imminent risks based on the earlier section of our analysis.

SMCI 8-K Filing, February 22, 2024

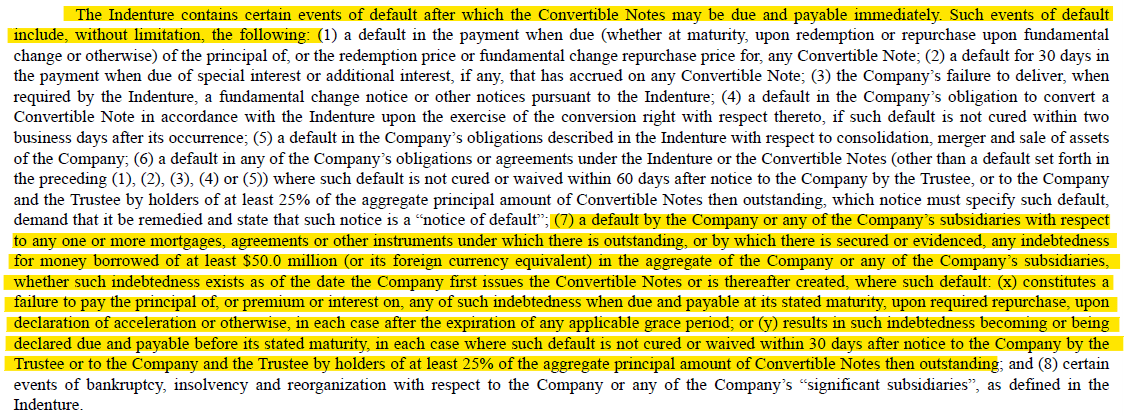

The indenture also stipulates that the convertible notes “may be due and payable immediately” under certain conditions of default. This includes default and/or premature payment required on outstanding loans of at least $50.0 million – another probable risk for SMCI that can be triggered given the adverse implications of its late 10-K filing on the $476+ million of outstanding term loans.

SMCI 8-K Filing, February 22, 2024

In the event that SMCI is required to repay its term loans early, it would face the additional risk of having to repay its recently issued convertible notes in cash as well. Such a situation would likely require SMCI to engage in further financing activities, but not without substantial difficulties, in our opinion. The combination of recurring accounting woes and regulatory scrutiny, alongside the rare occurrence of its auditor’s resignation, makes it unlikely for SMCI to engage in additional financing without having to comply with substantially unfavourable terms to compensate for its prospective lenders’ and/or investors’ heightened risk exposure. In the worst-case scenario, SMCI may even face doubts to its ability to continue as a going concern, in our opinion.

Fundamental Risks

Another rippling effect from SMCI’s delayed 10-K filing due to accounting-related issues is stifled demand. Although SMCI’s management does not anticipate any material misstatements to its FY2024 results, nor adverse implications to its day-to-day operations, the cascading effects of its delayed 10-K filing could deter end-market uptake of its AI server solutions.

As discussed in a recent analysis, we believe SMCI’s existing and prospective customers and partners are likely already diversifying some of their server orders to other vendors, such as Dell (DELL), as an act of due diligence in light of recent events. This is consistent with chipmaker Nvidia’s (NVDA) repeated endorsement for Dell during analyst conferences and other keynotes in recent months. The diversification of market share away from SMCI would essentially void our previous views that its proprietary direct liquid-cooling (DLC) solution for rack-scale plug-and-play AI servers could be a positive catalyst for the stock.

Related risks of stalled uptake are corroborated by SMCI’s recent progress updates. A press release from early October had stipulated that the company has shipped over 100,000 GPUs per quarter and deployed over “2,000 Liquid Cooled Racks” since June 2024. Yet, this figure did not differ materially from what was already reported in the 8-K filed a month earlier:

We have shipped approximately 2,000 DLC liquid-cooled AI racks to customers, which we believe is more than 75% of the entire DLC liquid-cooled AI server market this calendar year.

Source: SMCI Customer and Partner Letter, Update from CEO Charles Liang, September 3, 2024

More importantly, the materialization of impending liquidity risks discussed in the earlier section would also foreshadow a substantial setback to SMCI’s foray in AI servers. The company already faces profit margin compression with the increasing mix shift towards AI solutions in recent quarters. This is largely due to the lofty costs associated with next-generation GPUs currently being fitted into the AI servers, highlighting the significant capital intensity of SMCI’s business. As a result, any disruptions to SMCI’s liquidity as a result of its ongoing accounting mishaps would represent an immediate and direct risk to operations, regardless of its technical leadership.

Valuation Considerations

Given the combination of multiple compression and fundamental risks facing SMCI under the current situation, we believe it is no longer reasonable to gauge its valuation prospects under the traditional discounted cash flow method. Instead, we are considering SMCI’s cash balance reported in its FY2024 year-end earnings press release in August, as well as its market valuation at the time, as a proxy to gauge the stock’s outlook.

Immediately following the press release of its FY2024 earnings update, the SMCI stock was trading at a market cap of approximately $28.9 billion, or about 17.4x its reported cash balance of $1.669 billion. Assuming SMCI is required to repay its outstanding term loans of $476.4 million, applying a 17.4x multiple on resulting net cash of $1,193 million would yield a valuation of about $20.8 billion. This largely approximates SMCI’s market valuation today, following its steep selloff in response to EY’s resignation as its external auditor.

However, the stock faces further downside from current levels that remain underappreciated, in our opinion. The potential repayment of SMCI’s outstanding term loans before their originally stated maturities could trigger a requirement to repay its outstanding convertible notes in full of cash as well. This would result in additional liquidity implications for SMCI, and potentially cast doubt on its ability to continue as a going concern. The liquidity implications could also be further exacerbated by risks of fundamental weakness if SMCI’s ongoing accounting issues spill over to its day-to-day operations. As a result, we believe the stock could face a further downward correction from current levels.

Conclusion

Admittedly, SMCI possesses some of the most mission-critical technologies needed to facilitate ongoing AI developments. The company is currently one of the few server makers that can deploy liquid-cooled servers at scale via its proprietary DLC solution. And liquid cooling is essential in the AI era. Nvidia’s latest deployment of its Blackwell systems essentially marks the beginning of a new cohort of energy-intensive chips that will require liquid cooling to work.

However, the cascading effect of SMCI’s delayed 10-K filing, and escalated accounting uncertainties with EY’s latest resignation as its auditor introduced significant downside risks to the stock. Given the tangible impact of SMCI’s current accounting situation to its liquidity and fundamental performance, which remain underappreciated in our opinion, the stock likely faces risks of a further downward correction over the near-term.

Analyst’s Disclosure: I/we have a beneficial short position in the shares of SMCI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.