Summary:

- 3M’s stock jumped over 9% after agreeing to a tentative settlement of at least $10 billion for water pollution claims.

- MMM plans to exit the PFAS business by 2025, which currently brings in $1.3 billion in net sales.

- The fair market value for 3M is much higher than the current market cap if we factor in even $30 Billion in litigation costs and no PFAS income.

jetcityimage

Headline

Fresh off the presses, 3M Company (NYSE:MMM), just got some positive news regarding their PFAS case:

3M’s stock jumped more than 10% on Friday morning after Bloomberg News reported the company agreed to a tentative settlement of at least $10 billion with a variety of U.S. cities and towns to resolve water pollution claims tied to “forever chemicals.”

To be fair, the update from the courtroom pundits also goes on to point out that more costs should be in the pipeline regarding this case. It is also not inclusive of the earplug case, which is ongoing. 3M Company is a dividend king and one of the most stable cash-flowing companies in the DJIA outside of their unknown litigation costs. Let’s take a look at how cheap MMM stock might be after deducting some litigation cost assumptions combined with the exit of 3M’s PFAS business come 2025.

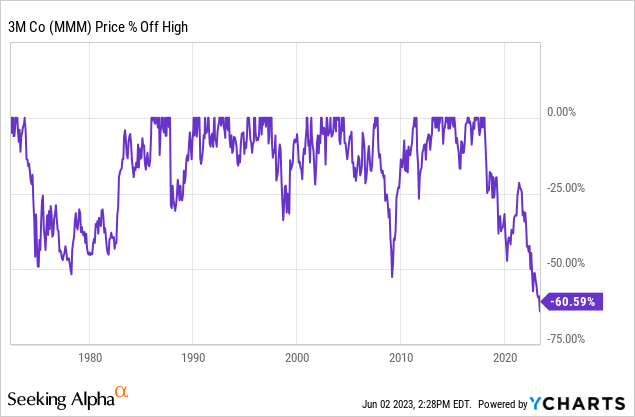

The chart

60% down could mean lots of gains ahead should 3M resolve its litigation issues. This Dow blue chip is currently trading at a market cap of only $52 Billion.

What they do

3M is a diversified technology company with a global presence in the following businesses: Safety and Industrial; Transportation and Electronics; Health Care; and Consumer. 3M is among the leading manufacturers of products for many of the markets it serves. Most 3M products involve expertise in product development, manufacturing and marketing, and are subject to competition from products manufactured and sold by other technologically oriented companies.

Valuation model

I’m going to be taking a look at 3M today using a Buffett owner earnings discounting model. This model is a unique discounting method that hunts for quality stocks that have an equilibrium between Depreciation and Amortization versus their CAPEX. When management is running efficiently, the large capital outlays come in the beginning and it shouldn’t take tons of extra capital to invest and keep profitable thereafter.

You’d be surprised how many companies have capital expenditures far in excess of depreciation and amortization. This is the opposite of a well-run business. We should say such a business is highly competitive and has a low to no moat nature. Dividend aristocrats and kings tend to exhibit a very close equilibrium between the two aforementioned items and a moat because of this.

Litigation costs

First and foremost, this analysis can’t be as straightforward as punching in the numbers on the checklist. I’m going to make a maybe not-so-conservative assumption here and assume that there are $30 Billion in litigation costs to carry forward. Let’s view what happened with the recent Johnson & Johnson (JNJ) case to see how the structure of the payments is laid out:

Johnson & Johnson said on Tuesday that it had agreed to pay $8.9 billion to tens of thousands of people who claimed the company’s talcum powder products caused cancer, a proposal that lawyers for the plaintiffs called a “significant victory” in a legal fight that has lasted more than a decade.

The proposed settlement would be paid out over 25 years through a subsidiary, which filed for bankruptcy to enable the $8.9 billion trust, Johnson & Johnson said in a court filing. If a bankruptcy court approves it, the agreement will resolve all current and future claims involving Johnson & Johnson products that contain talc, such as baby powder, the company said.

Basically, a trust is set up for the payout to occur over 25 years. I would assume something similar here. With that in mind, $30 Billion over 25 years would be a litigation cost of $1.2 Billion a year.

PFAS 2025 Exit

Another deduction we have to put into our model is the PFAS exit. The company plans to exit the business completely by 2025, here is what the business was bringing in according to 3M Company:

- Net sales of $1.3 Billion

- EBITDA margin of 16%

- Equivalent to $208 million in EBITDA

- A $163.32 Million a year loss in net income assuming an EBITDA to Net Income conversion of 79.7%. 79.7% is the most recent EBITDA to Net Income conversion rate for 3M Company.

Modified owner earnings

Now that we have our deductions to penalize 3M company for, let’s run the model:

Data courtesy of Seeking Alpha

- TTM net income is $5.45 Billion

- Plus TTM depreciation and amortization of $1.838 Billion

- Minus $1.8 Billion TTM CAPEX

- Minus $1.2 Billion litigation cost/year

- Minus $163.32 million in PFAS business income

- Equals owner earnings of $4.127 Billion

- Discounted by risk-free rate of the 10-year treasury, March 2nd, 2023, of 3.6% = $114.657 Billion fair market cap

- Discounted at a short risk-free rate of 5%, $82.55 Billion.

Buffett discounted stabilized businesses such as these at the 10-year treasury rate. I baked in a high and a low-end market cap based on the long and short ends of the risk-free yield curves. Blending the two gets a fair market cap of $98 Billion. There are 551.672 million shares outstanding as of June, 2nd 2023. This gets us to a fair value of $177.64 a share based on these assumptions.

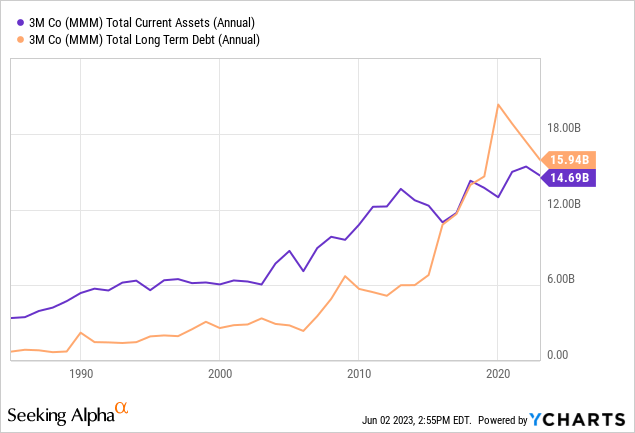

The balance sheet

Long term debt and current assets are about in equilibrium here. Not the best balance sheet but not a poor one either.

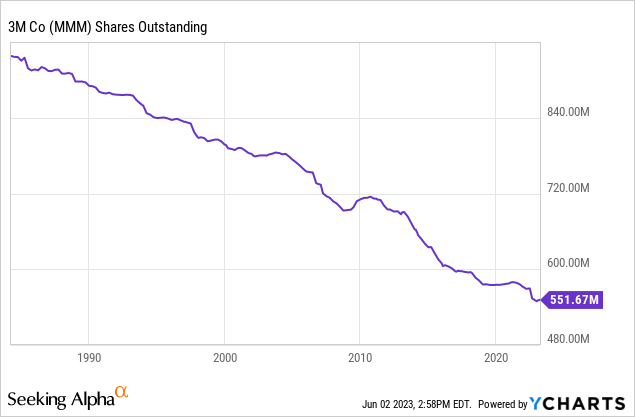

The trend in shares outstanding is outstanding. This company knows how to give back to its shareholders and continues to do so. This is how you buy back under intrinsic value.

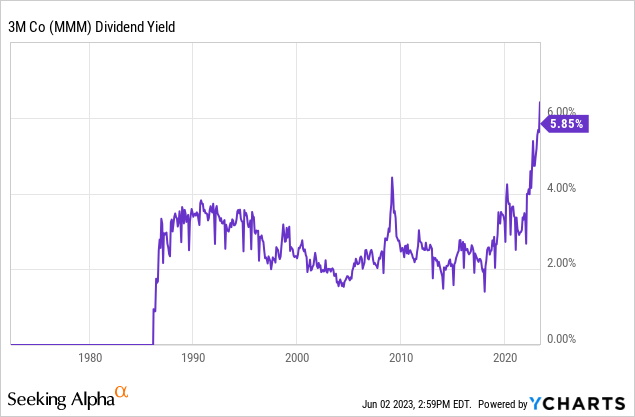

Finally, the yield. Investors right now in 2023 have never seen a better dividend yield on 3M Company. The market is risk-off on them right now, but this is history in the making. Is Mr. Market right or wrong? Even a 33% dividend cut would leave us near historically high levels.

The dividend and free cash flow

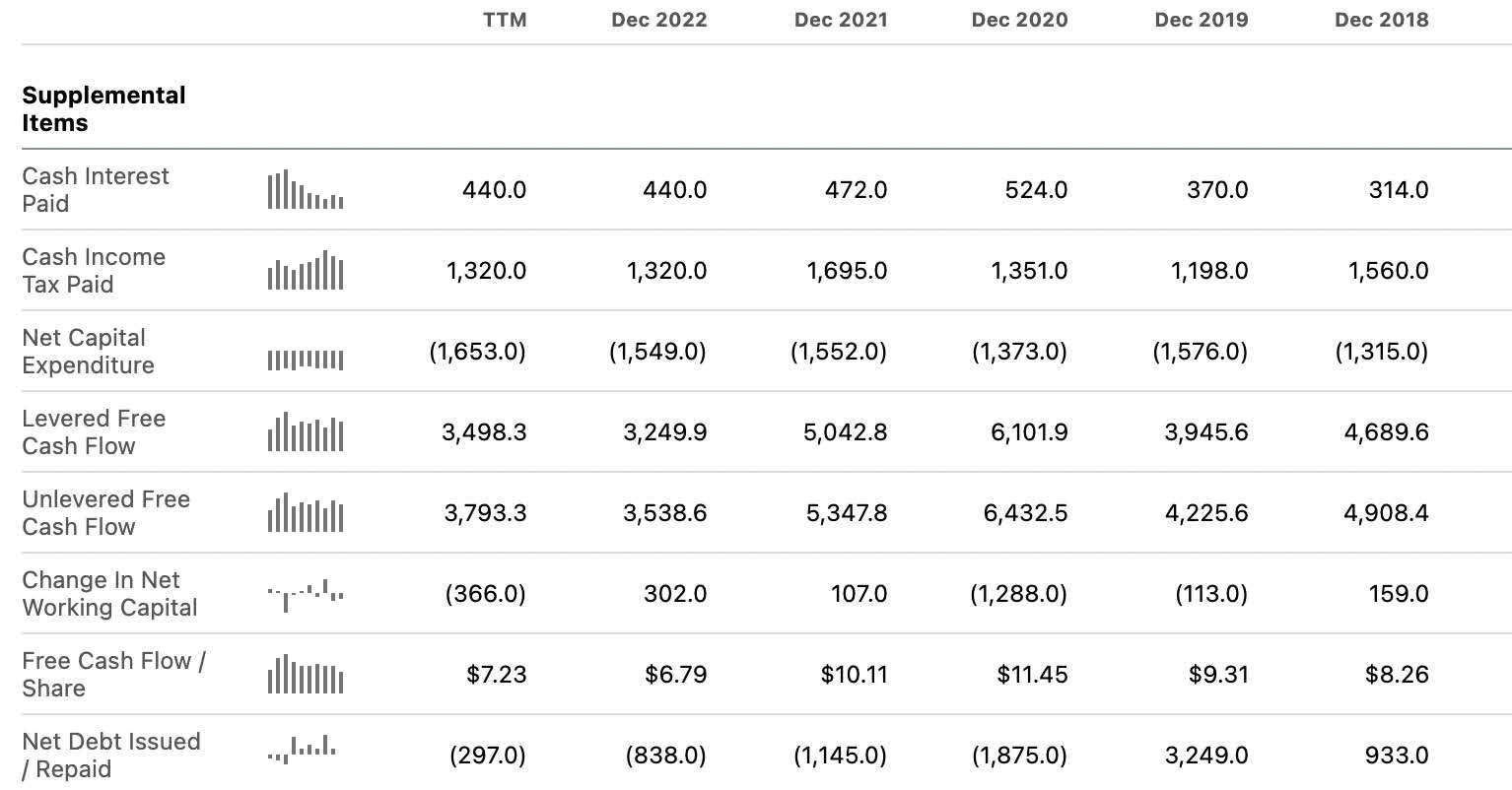

To be fair, the dividend is covered by earnings but marginally covered by free cash flow.

seeking alpha

With a $6 per share dividend and a TTM free cash flow of $7.23, that’s a payout ratio of 82%. I’m assuming buybacks need to be curbed at some point to maintain the dividend king status and preserve capital. The dividends are more important than the buybacks to preserve the share price and the moniker.

Catalysts

More revelations around the actual costs of litigation. Plain and simple, we’re up nearly 10% after finding out that part of the litigation could be capped at $10 Billion. I’m baking in $30 Billion to my equation, some were floating numbers above $100 Billion just for the PFAS portion alone. You never know where this will wind up. At least the market has been prepared for the worst for quite some time.

Conclusion

I’ve started buying again. I was simply holding my shares on DRIP for the better part of a year. I, like most, have been waiting to hear any revelations in the 3M court case. $10 Billion sounds like a lot, with more to come, but at least we’re getting some rational judgments. This is combined with the fact that any payout is probable to be paid over many years rather than a lump sum. I’m buying cautiously here and my big dividend on DRIP is doing the rest of my DCA.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of JNJ, MMM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.