Summary:

- 3M investors who ignored MMM’s peak pessimism have performed remarkably.

- MMM has consolidated well along the $100 level. Selling enthusiasm has also been lacking.

- 3M’s new leadership team must execute well in the second half to meet its FY2024 guidance promulgated previously.

- MMM’s attractive valuation has likely baked in execution risks, providing more time for the company to deliver.

- I argue why the MMM’s rally is far from over as it continues on its stellar turnaround opportunities.

jetcityimage

3M: Investors Looked Past Peak Pessimism

Industrial stocks like 3M Company (NYSE:MMM) have performed well recently, as the sector rotation has bolstered the sector. Investors have remained calm even as MMM revised its dividend per share payout downwards. As a reminder, the dividend revision is necessary for 3M to reignite a healthier recovery trajectory as a “reset” from spinning off Solventum (3M’s previous healthcare business).

As a result, the company’s decision to downgrade its payout ratio to about 40% of adjusted free cash flow is considered appropriate. It helps the company maintain financial flexibility as it looks to reinvest in the higher growth and more profitable business segments. In addition, it also allows the company to pay down more debt over time, reducing its adjusted EBITDA leverage ratio. Therefore, I assess that buying sentiments on MMM have remained resilient as investors look past the previous challenges, buffeting the material sciences’ leader.

I last covered MMM in a bullish article in early May 2024. I presented my thesis on why the company is still in its early turnaround stages. The legal liabilities and challenges that battered the company are also expected to feature less prominently moving ahead. Coupled with the spinoff of Solventum, 3M can refocus on opportunities in secular growth vectors in the transportation and electronics business.

Outgoing CFO Monish Patolawala will leave the company on July 31 as the next CFO for Archer-Daniels-Midland Company (ADM) on August 1. However, the market hasn’t reacted adversely to MMM’s CFO departure, suggesting confidence in new CEO Bill Brown’s stewardship. Notwithstanding the significant legal and business model challenges that previously impacted confidence in 3M, MMM has notched a total return of almost 28% over the past year. Therefore, it’s increasingly clear that income investors who wanted to bail have already left. I assess that MMM’s relative undervaluation to its industrials peers should continue underpinning its recovery, bolstered by the resilience of the US economy.

3M: Second-Half Growth Inflection Is Key

The company will report its second-quarter earnings scorecard on July 26. In MMM’s Q2 earnings release, investors will likely look toward management’s commentary about the health of the US economy and the impact on its diversified businesses. 3M’s automotive OEM business was a growth enabler in Q1, delivering a 13% YoY revenue increase. It was underpinned by the strength in its automotive electrification segment, which surged 30% YoY. I assess that the resilience of the US economy through 2025 and the expected interest rate reductions by the Fed from September 2024 should help sustain MMM’s buying sentiments.

Moreover, MMM’s scale allows the company to capitalize on “cross-platform utilization.” As a result, it has allowed the company to leverage its leading product innovation across several business verticals to “solve problems in another space.” Hence, I assess significant synergies for the company, as it allows 3M to “maximize the utility of core technologies across different industries and applications.”

Therefore, I believe it should undergird the strength of the company’s moat and profitability. It should help the company fend off near-term challenges, allowing more time for the new leadership to justify improved execution for a potential valuation re-rating.

2024 is expected to be a reset year as the company laps the spinoff of Solventum through early 2025. Wall Street will likely focus on whether management anticipates material changes to its outlook, as communicated in Q1. Accordingly, the company “anticipates adjusted organic growth ranging from flat to up 2%” for FY2024. In addition, 3M also expects a stronger second half, attributed to seasonality factors. As a result, we should expect Brown and his team to provide more confidence in meeting the more robust adjusted EPS growth guidance (15% increase) through the rest of the year.

MMM quarterly earnings estimates (Seeking Alpha)

For Q2, MMM is expected to deliver an adjusted EPS of $1.68. As seen above, the company is expected to lap four quarters of spinning off Solventum, directly affecting comparisons. As a result, investors are urged to focus on assessing potential changes to the company’s midpoint adjusted EPS guidance of $7.05 for FY2024 as key to its determining investor sentiments.

Adjusted operating margin is expected to be lower at 19.7% before an improvement to 21.3% in Q3, in line with expectations of more robust second half performances. Therefore, investors have likely anticipated a more constructive H2 outlook as the base case.

MMM: Valuation Is Still Cheap

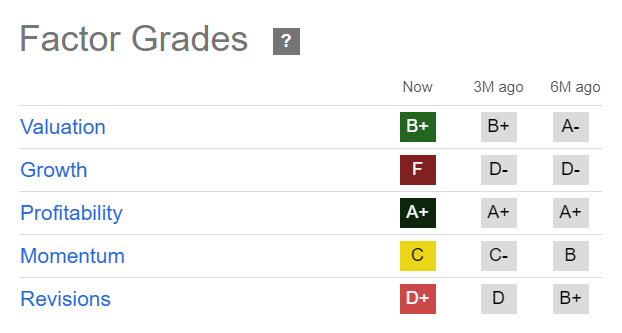

MMM Quant Grades (Seeking Alpha)

MMM is still valued relatively attractively, with a “B+” valuation grade. Its forward-adjusted EPS multiple of 14.6x is markedly below its sector median of 19.7x. The company’s solid profitability (“A+” profitability grade) should help assure investors to stay invested as we emerge from the legal challenges and dividend cut fears that afflicted its recovery.

Is MMM Stock A Buy, Sell, Or Hold?

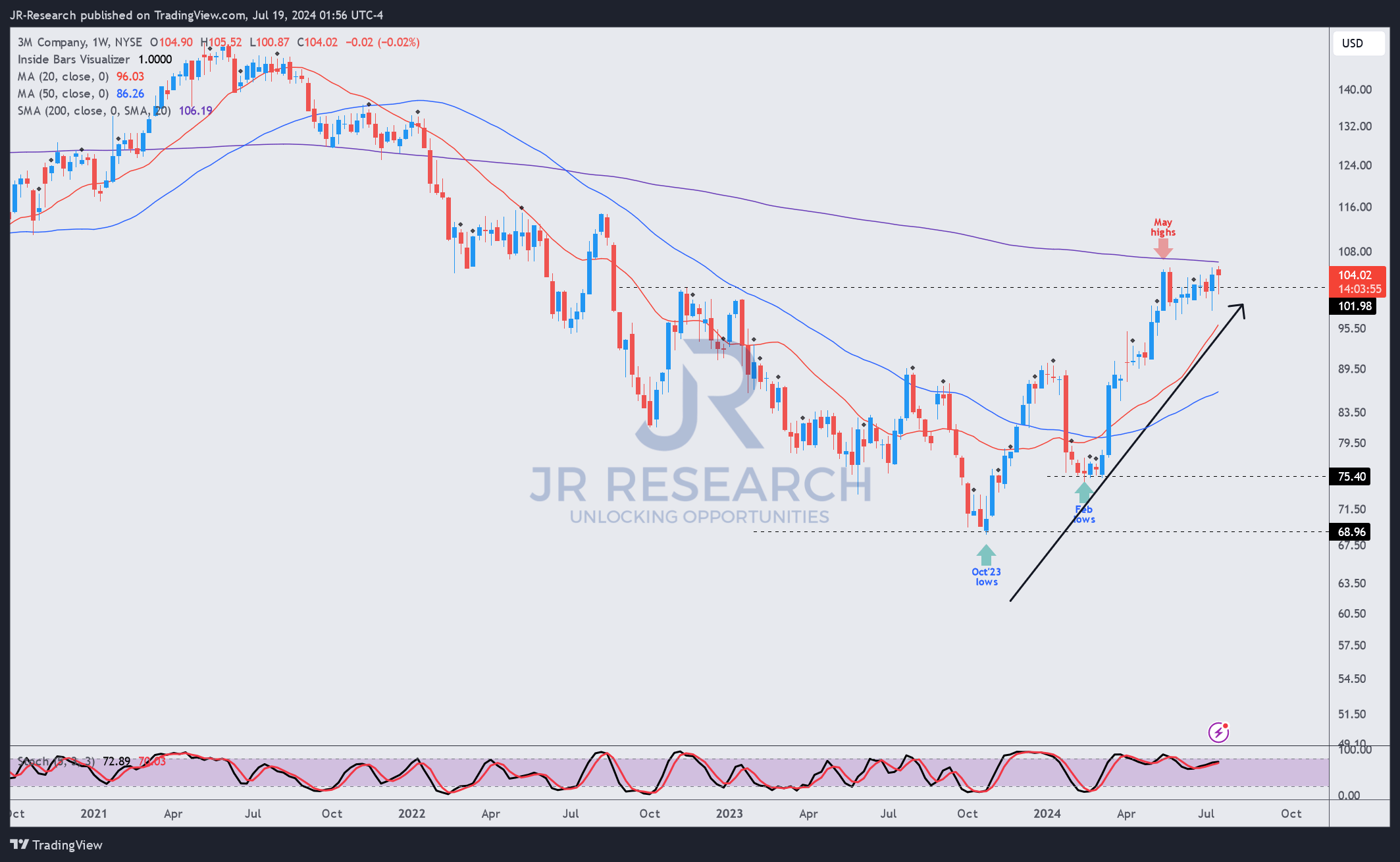

MMM price chart (weekly, medium-term, adjusted for dividends) (TradingView)

MMM’s price action is also increasingly robust. It has faced resistance just under the $105 level. However, selling intensity hasn’t impacted its buying momentum, helping the stock remain in a medium-term uptrend.

Accordingly, MMM’s bottom in October 2023 and February 2024 remain intact. As a result, dip-buying opportunities have worked out very well for investors who ignored the market’s pessimism then.

Near-term volatility could continue as MMM consolidates around the $100 level. However, a decisive breakout is seemingly likely as buying accumulation is assessed. Therefore, investors who missed adding in early 2024 should consider capitalizing on its pre-earnings consolidation opportunity before it potentially rallies further.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing, unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!