Google’s search revenue remains dominant, growing from $70B in 2017 to almost $50B in the last quarter alone.

AI-driven competitors like ChatGPT and Perplexity are gaining traction, potentially disrupting Google’s market share in the search engine space.

Google’s global market share has declined slightly, but it remains the leader.

Although Google is losing market share, they earn more money per user and benefit from the growing world population.

Ole_CNX

I have already written several articles examining individual aspects of Alphabet (NASDAQ:GOOG) in depth. In the past, I covered DeepMind andWaymo and already analyzed Google’s and YouTube’s market share 2 years ago. I will probably write an update on the company’s “other bets” sometime soon.

Today, I will examine the still most significant revenue driver: The search segment. Is the AI thread real? I believe it is, and there are signs that Google is losing market share. However, the company also continues to profit from rising global internet users and more revenue per user. Therefore, given its current position and financial power, it is likely that the company will remain a leader in the AI age as well.

History of Google

In the late 1990s, Larry Page and Sergey Brin at Stanford University laid the foundation for one of the most successful companies of our time. Based on the PageRank algorithm, they found a new mechanism to index and rank the exponentially increasing number of web pages at that time. Unlike other methods at any time, their method not only took into account the content of the website but also inbound and outbound links. This made it possible to deliver significantly better results, and as a result, Google became synonymous with internet searches.

about.google/our-story

Equipped with new financial resources after the IPO in 2004, the company expanded into many other areas, creating services such as Google Maps and Gmail and, in 2006, acquiring YouTube. In 2007, the company once again recognized the opportunity and acquired the developer of the Android operating system early in the smartphone boom.

The creation of the Google Chrome operating system followed in 2010. Since then, the company has successfully interconnected its services and integrated them into the everyday lives of billions of people. Today, it seems almost difficult to live without any of the company’s products. It is certainly possible but involves considerable effort and research, which most people will probably not want to do. From this perspective, the company has an immense moat.

How important is this division today?

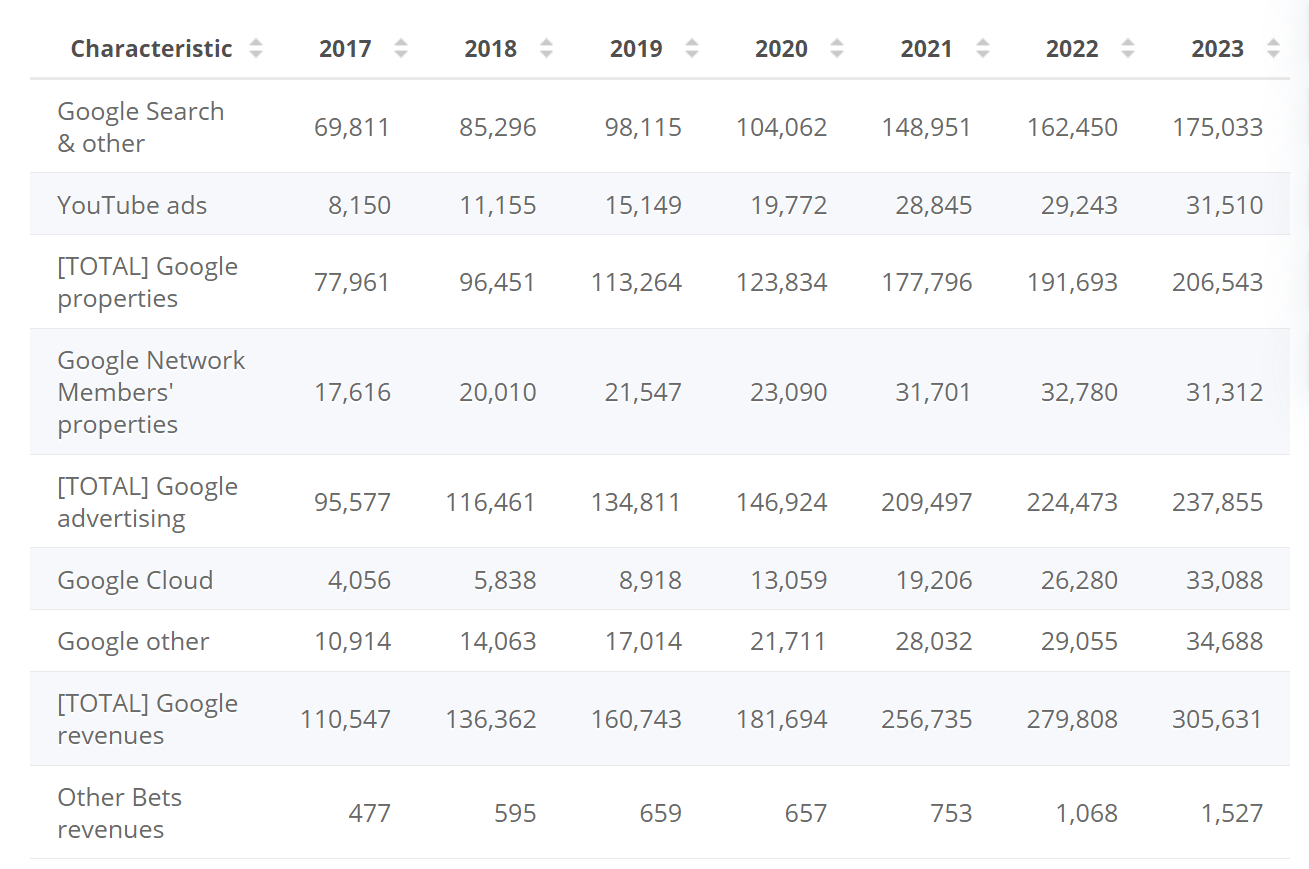

Let’s first look at the individual segments’ development since 2017. By 2023, the Google Search segment has grown 2.5x in revenue from $70B to $175B. Converting the figures shows that the Google Search segment accounted for around 64% of total revenue in 2017.

Statista

Although a lot of information I found for the research of this article indicates that Google has lost market share in recent years, and it is also clear that AI chatbots like ChatGPT are gaining in attractiveness and user numbers, this effect is still not visible in Google’s sales figures.

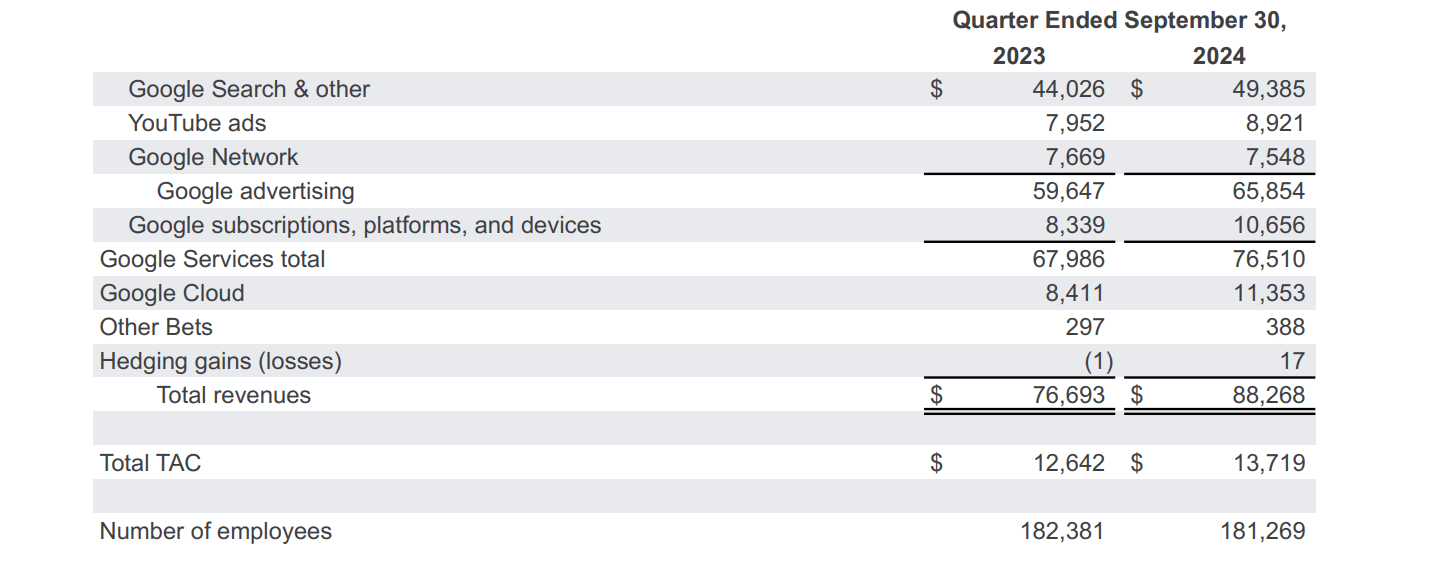

The recently published quarterly figures show strong growth in almost all areas. Google Search revenue grew approximately 12% YoY from $44B to $49.4B. Total revenue grew from $76.7B to $88.2B. This means that Google Search accounts for approximately 57% of total revenue.

Investor presentation

Overall, the company is becoming less dependent on the search business, which is a promising trend. 57% of revenue is still a lot, but it is steadily decreasing, and given the growth figures of YouTube and Google Cloud, as well as the potential of the “other bets” like Waymo, this trend will likely continue.

Challenges and emerging competition

Are you using ChatGPT or other chatbots for questions that you used to ask Google? This is definitely the case for me, and when I ask around in my circle, it seems very common that people partially replaced Google with AI. Let’s start a mini-survey; just post a comment below this article: Has ChatGPT already taken a piece of Google’s share for you?

According to a report by the research institute eMarketer, Google could receive less than 50% of the total online marketing budget for the first time next year. It seems like the competition is as intense as ever and coming from many different angles.

A forecast by market researchers at eMarketer is causing discussion in the advertising industry. According to the forecast, Google’s market power in online advertising could fall below 50 percent next year after a long period of dominance. This is still a big lead over the number two, Amazon, which is expected to account for around 22% of advertising revenue in 2024, but it is still a major upheaval. Google’s share has been falling for years.

Our way of interacting with information might transform within the next years. One of my past articles was even called “Google Seems To Be Outdated.” In my view, traditional Internet search is relatively slow and inefficient. Google indexes websites and ranks them according to what it believes will deliver the best results based on the search term. Users usually have to click through several websites to find the information they’re looking for. AI-driven information retrieval eliminates the need to click through and presents the information directly, even in a conversational manner if desired.

At the moment, however, there are still many cases where an internet search makes more sense. However, I believe this will change at the latest when the age of robotics dawns and people start to own personal robot assistants. Then it will probably be possible to talk to them almost like with other people. Why should I search for information on my cell phone when I can simply ask my personal assistant? I don’t think this scenario is science fiction; it will probably start within this decade.

Of course, Google is still the biggest player in the search market, and that won’t change quickly, but there is serious competition for the first time ever. This follows a pattern we have already seen many times in history, described by Clayton Christensen in his famous book “The Innovator’s Dilemma“:

In business theory, disruptive innovation is innovation that creates a new market and value network or enters at the bottom of an existing market and eventually displaces established market-leading firms, products, and alliances. (…)Disruptive innovations tend to be produced by outsiders and entrepreneurs in startups, rather than existing market-leading companies. The business environment of market leaders does not allow them to pursue disruptive innovations when they first arise, because they are not profitable enough at first and because their development can take scarce resources away from sustaining innovations (which are needed to compete against current competition). Small teams are more likely to create disruptive innovations than large teams.

AI applications and alternative ways of obtaining information are gaining popularity; here are some examples.

Perplexity

Perplexity looks and feels like a fusion of Google and ChatGPT: A search engine on the surface but empowered with AI- capabilities.

According to Similarweb data, Perplexity’s website is quickly gaining traction, growing from about 55M monthly visits in August to 91M in October 2024. As far as I know, this counts only visits on Perplexity.ai and does not include mobile apps. This would mean that the actual usage far exceeds those numbers. During the same time, its website country rank in the US grew from 912 to 601. Furthermore, about 52% of users are 34 years old or younger.

Similarweb

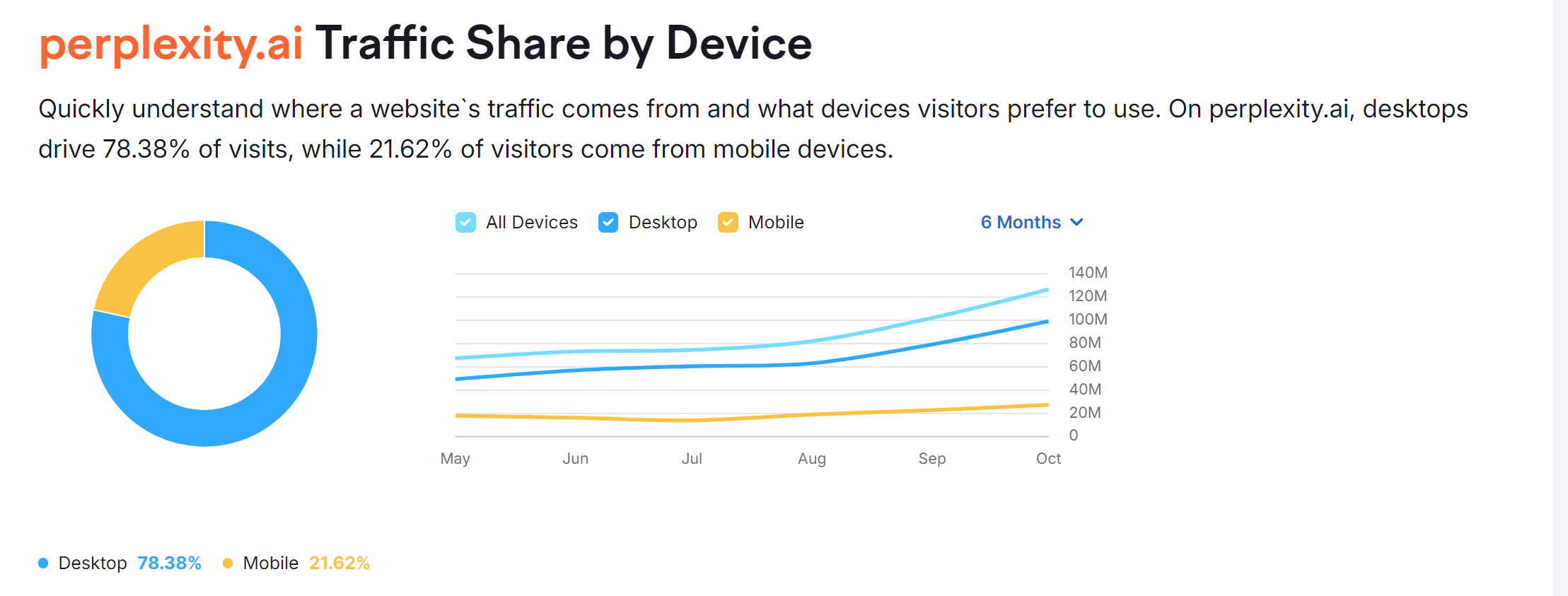

According to Semrush, traffic mainly happens on desktops and much less on mobile. This makes sense: Perplexity is a great research tool that helps deep dive into topics. It is less suitable for quick searches on phones.

Semrush

It is growing in popularity and does so quickly. In February, Nvidia CEO Jensen Huang said he uses Perplexity “almost every day.” The valuation was $3B in June, and the company is currently “in the final stages of raising $500 million in funding at a $9 billion valuation” (source).

SearchGPT

Possibly inspired by the success of Perplexity, OpenAI recently released its own Chatbot-search-hybrid called SearchGPT. It has been in beta since July and officially launched at the end of October 2024. Currently, it is only available for paying users.

OpenAI

This is a big deal because ChatGPT is by far the most popular AI platform, with weekly active users of more than 200M, which is 2.5% of the world’s population. Additionally, its mobile app was downloaded more than 110M times (and this article is even a year old).

AI apps

Both apps, Perplexity and ChatGPT, are just examples of a whole bunch of programs that can all be grouped together under AI apps. The release of GPT 3 in 2022 has caused tremendous hype and inspired billions of Dollars in investments for research and development. Thus, it’s safe to say AI is still just getting started.

businessofapps.com

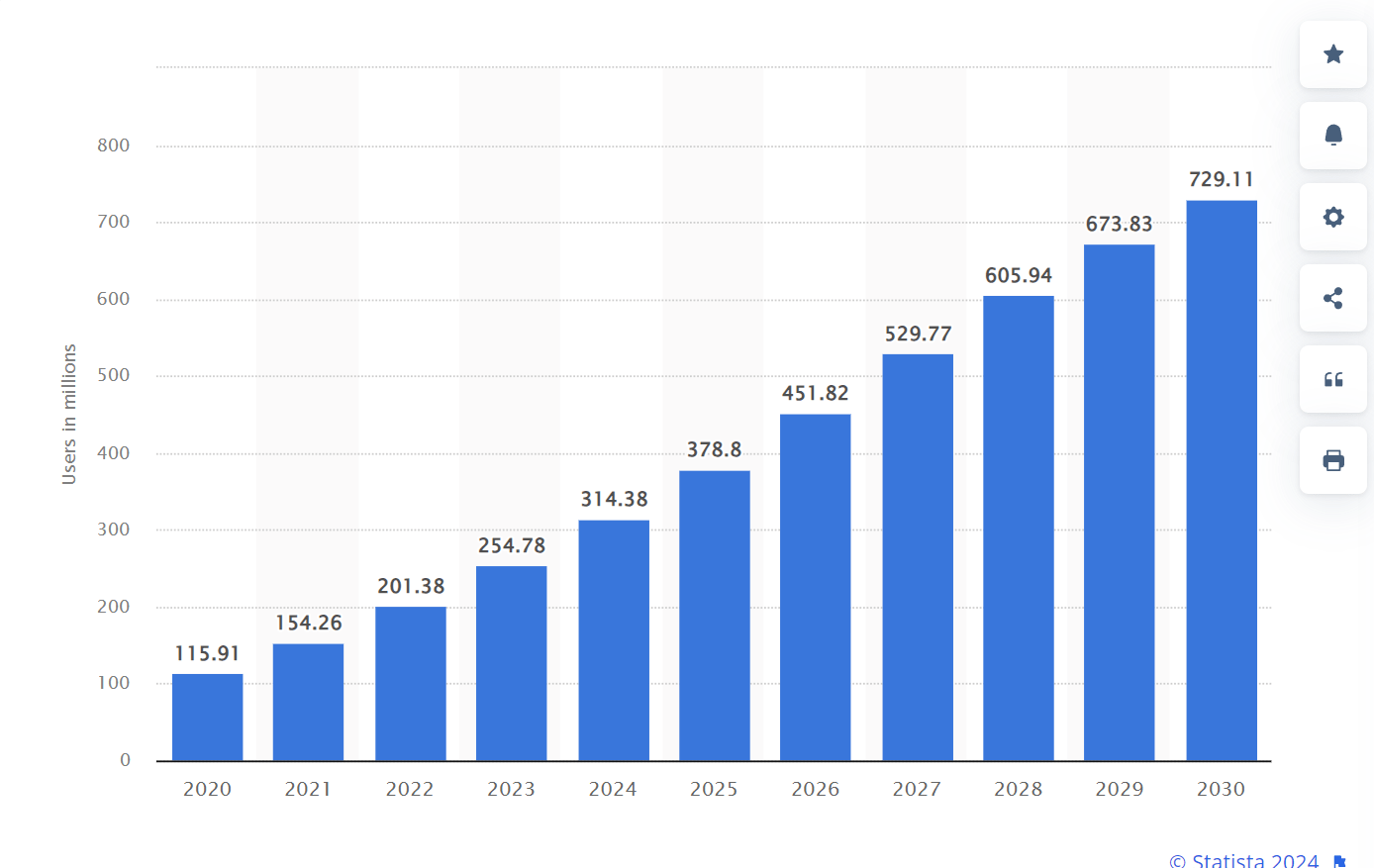

It is remarkable that such a young technology already has hundreds of millions of users and will probably have between 700 and 900M by the end of the decade. According to statista.com, these are the projections for the “Number of artificial intelligence (AI) tool users globally from 2020 to 2030”.

Statista

Is Google losing market share?

But how successful is the competition really in absolute terms? Is Google even losing market share? This question is not easy to answer because there is no one way or method to track this complex market and its development over time. But there are some clues.

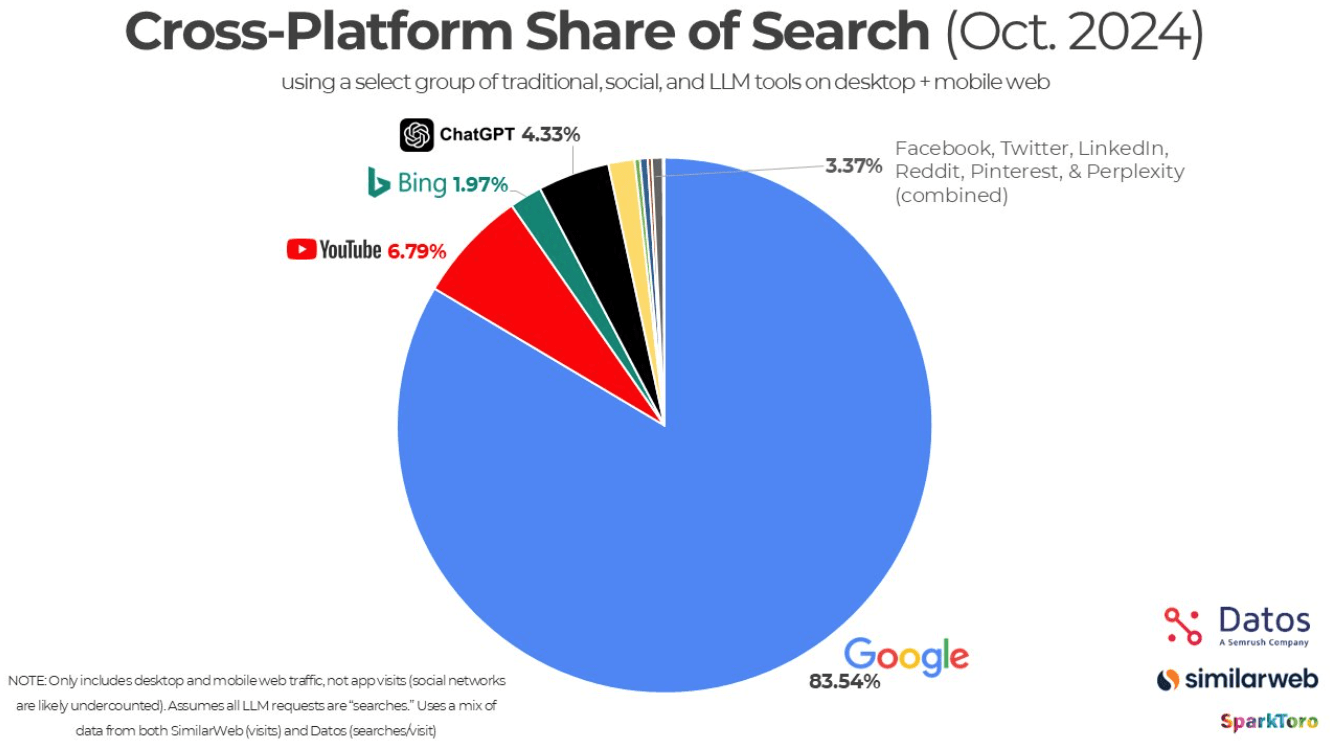

Rand Fishkin of Sparktoro posted his assumptions based on a mix of data from SimilarWeb and Datos that says ChatGPT’s current market share is 4.33% – that is from October 2024 data.

So ChatGPT is 4.33%, while Google is 83.54%, then YouTube is 6.79%, Bing at 1.97% and Facebook, Twitter, LinkedIn, Reddit, Pinterest, and Perplexity all combined is 3.37%.

Rand said on X, if we assume (1) every LLM prompt is a “search”, (2) desktop + mobile web traffic, excluding apps, is close enough, and mixing data from multiple panels is kosher, then here is the chart he shared:

Counting every LLM prompt as a search seems drastic, but let’s look at more data points. Just two months ago, an article on Yahoo Finance reported on a survey of 1,300 Americans.

8% said they are using ChatGPT as their go-to search engine. That’s up from just 1% a few months earlier. Google Search remains the leader with 74% of surveyed users relying on its results, but that is down from 80% in the earlier survey.

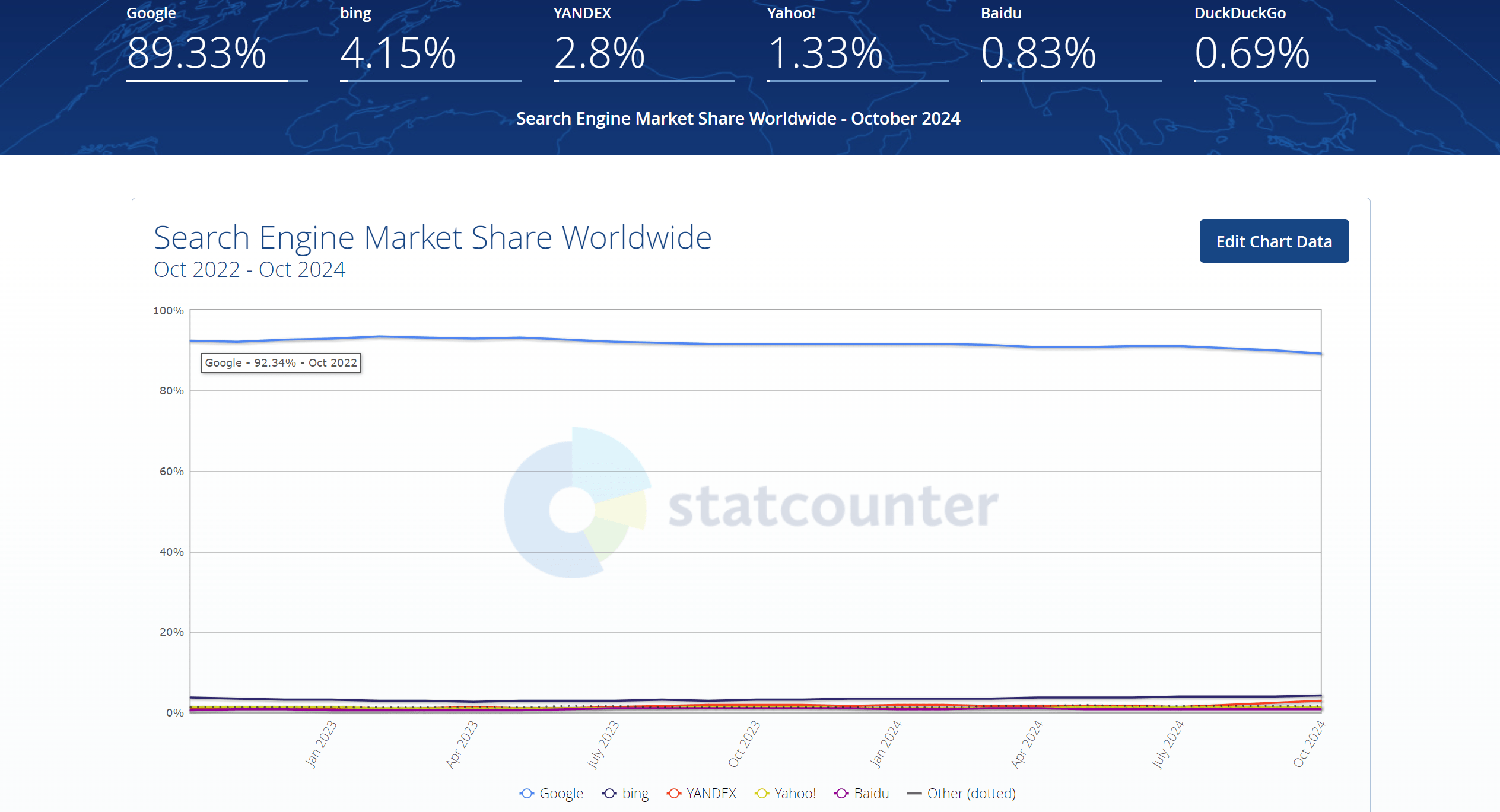

But it’s not just about losing market share to chatbots; according to Statcounter, Google is also slowly losing market share worldwide to other search engines such as Bing, DuckDuckGo, and Yandex.

Two years ago, in October 2022, Google’s global market share was 92.3%; today, it is only 89.3%-a loss of 3% in two years. This may not sound like much, but every percent that Google loses corresponds to billions of dollars in ad revenue. Nevertheless, I don’t want to make the situation more dramatic than it is, as Google is still the absolute number one in this area.

Statcounter

However, it becomes a little more worrying if you only look at the figures for desktop searches, where Google is only at 79% and Bing at 12%. In most countries, Google has a higher market share than in the USA, where the market share for desktop searches is only 77%, but mobile still dominates at 95%.

Google fights back with its own AI

Of course, Google recognized these dangers and quickly raised the alarm about the emerging competition. As a result, it has significantly expanded its efforts to avoid being left behind technologically. Google now offers its own AI platform called Gemini. Thanks to its worldwide reputation, large data, and considerable financial resources, it is very well-placed to eventually take the lead in the AI race.

Still, it’s a whole new playing field, and Google themselves say they have no moat in this area, but neither has the competition. Overall, Gemini has significantly less traffic and mobile app downloads than ChatGPT.

The Decoder

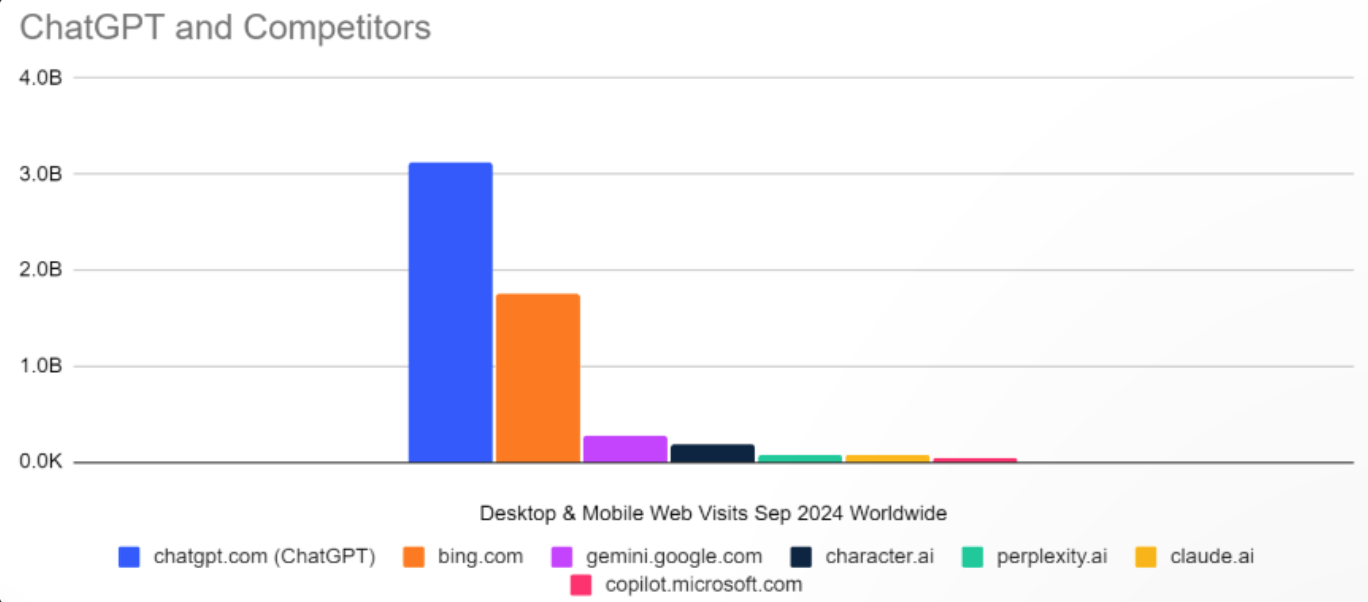

Google knows that they cannot rest on their past achievements. AI has the potential to disrupt their core business. ChatGPT and other chatbots have grown enormously fast. Yet, they seem to be still in the early adopter phase. Recently, ChatGPT achieved considerable success, overtaking Bing and Amazon in traffic for the first time.

OpenAI’s ChatGPT reached a new milestone in September 2024, surpassing Microsoft’s Bing search engine in visitor numbers for the first time. The AI chatbot saw significant growth in both web and mobile app usage. According to estimates from Similarweb, ChatGPT‘s website received more than 3.1 billion visits worldwide last month. This represents a 112 percent year-over-year increase and an 18.7 percent increase from August. (…)With over 3 billion monthly page views, ChatGPT now ranks as the eleventh most visited website globally. While still well behind internet giants like Google (82 billion visits) and YouTube (28 billion visits), it has surpassed Amazon.com’s 2.6 billion visits, excluding international domains.

Summarizing all the information in this and my previous articles, I believe what is happening is the following:

Google may slowly lose market share to competitors like other search engines, chatbots, and ad revenue to TikTok and others. However, the company is still benefiting from some structural global tailwinds:

Although the world’s population is no longer growing as fast, it is still increasing, and the number of global Internet users continues to rise, which benefits Google.

Revenue per user is most likely increasing. Data for the US certainly shows this, but a logical conclusion indicates that this is true for many countries. When there is GDP growth and a rising middle class, people have more to spend, which makes them more attractive to advertisers.

The larger the supply of people searching for products, the more advertising space they have to monetize. For years Google was adding new users and, with that, a fresh new supply of ad space. As advertisers increased spend, there was also increased supply of search behavior. Supply and demand growing at the same time kept prices relatively stable in Google’s ad space auctions.

Advertiser demand for Google user attention has increased, but since 2016 (about the time that smartphones reached mass adoption), the supply of that attention targeting data from Google users has remained about the same. And over this time, Google US Advertising revenues have grown from an estimated $152 per user in 2015 to $379 per user in 2022, tracking to about $390 per user in 2023.

Source: What Google At Peak Search Means for Marketers

Conclusion: Google remains a major force

Therefore, we do not see a negative development in the sales figures but, on the contrary, further double-digit growth. People spend more time online and on cell phones, so Google has more time to show ads. The individual user becomes worth more, and the total number of users is rising.

The company operates an extensive ecosystem of applications that reinforce each other. Considering that it is even difficult for users to completely do without Google apps, the most likely scenario seems to be that Google will continue to play a major role in society and continue to grow its revenue and income. With its resources and financial means, the company is excellently positioned to take on a leading position in the AI age, even if the pioneering role came from OpenAI.

Therefore, in view of these signs and the current, not particularly expensive, valuation of the share, I believe it is and remains a strong buy.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of GOOG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.