Summary:

- AbbVie released its Q322 earnings today. Revenue of $14.8bn slightly missed analysts expectations.

- Earnings per share increased by 24% on a diluted basis and 29% on an adjusted basis however.

- Management did not provide specific guidance on the impact Humira’s loss of exclusivity in 2023 would have on it revenues.

- I would not be too concerned about Humira however as there are ready made replacements performing superbly and an intriguing product pipeline.

- In this post I look at 5 key aspects of the Q322 earnings and attempt to show why there are more positives than negatives.

z1b

Investment Thesis

AbbVie (NYSE:ABBV) stock has been falling in value today after a mixed set of Q3’22 earnings – at the time of writing, the traded price is $148, and the market cap is $261bn.

Having spent some time analysing the earnings press release, sales figures, and earnings conference call, in this article I look on five key areas of focus, and outline why the positives generally outweigh the negatives, and why investors buying this mini-dip may be rewarded in the long term.

ABBV Earnings – Headline Figures

First of all let’s take a look at the headline earnings data. Net revenues came in at $14.812bn, which is +3.3% on a reported basis and +5.4% operationally. Whilst the revenue growth missed analysts’ expectations, on an earnings per share (“EPS”) basis, diluted EPS increased by 24% to $2.21, and adjusted EPS was calculated as $3.66 – up 29% year-on-year.

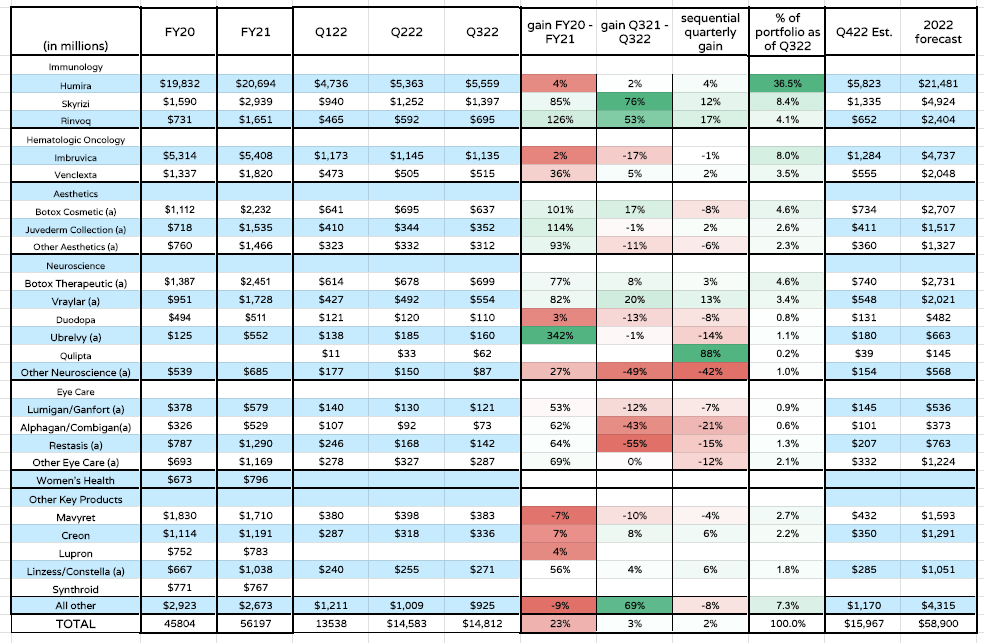

To help readers get to grips with the results by division and drug, I have created the following table.

AbbVie recent revenues by product / division. (my table)

Source: my table with data taken from AbbVie

There is a lot of data to unpack here. Essentially, I have included FY20 and FY21 revenue by product data, followed by the first three quarters of 2022 as reported. I then show percentage revenue growth between 2020 and 2021, then between Q321 and Q322, followed by the sequential percentage gain.

I then show what percentage of total revenues each product accounts for, and then, using the guidance supplied by management in Q222 for $58.9bn of revenues across the whole of 2022, plus revenues earned across the first three quarters, and percentage of total revenues, I fill in the gaps and create estimated Q4 and FY22 revenues figures for each product.

The first two things that likely jump out are firstly the fact that Humira – AbbVie’s auto-immune mega-blockbuster – still accounts for 36.5% of total revenues, and secondly that sales of Humira’s long term replacements, Skyrizi and Rinvoq, are soaring.

I will discuss the Humira situation in more detail below, but as bad as the fall in Humira sales in 2023 may be – the product loses its patent protections next year and must compete against cheaper generic versions of itself – it will be offset to a large extent by growing sales of Skyrizi and Rinvoq.

Away from Immunology – which accounts for very nearly half of all AbbVie’s revenues – it was a disappointing quarter for one of AbbVie’s key drugs, Imbruvica. This leukemia drug’s sales have been negatively affected by a ~20% reduction in new patient starts since the pandemic, management says.

CEO Rick Gonzalez suggested on the Q322 earnings call that AbbVie is “reducing our view of the total size of the addressable patient population”, for Imbruvica, blaming “the recent unfavourable change to the NCCN guideline preference for Imbruvica in CLL, as well as increasing existing and new competition”. It isn’t great news for Imbruvica, but Venclexta had a solid quarter, and there are label expansions opportunities in play for the younger drug.

Despite the impressive year-on-year growth of Botox revenues, AbbVie’s aesthetics division has also been suffering slightly on a sequential basis. Management blamed the difficult economic environment – in times of financial difficulty, demand for non-essential surgeries typically falls.

Results within neuroscience were mixed. Vraylar has been an unqualified success for AbbVie, and the atypical antipsychotic indicated for Schizophrenia and bi-polar disorder looks set to break $2bn of revenues in FY22. Parkinson’s therapy Duodopa may have reached its ceiling of ~$550-$600m sales per annum (although there may be a replacement coming to market soon), and although chronic migraine therapy Qulipta’s revenue growth has been strong since its September 2021 approval, Ubrelvy – another migraine therapy – sales appear to have plateaued.

The Eye Care division seemed to badly underperform in Q322, down >25% annually and ~15% sequentially on average, but AbbVie did not discuss its performance during the Q3 earnings call. I would put the underperformance down to the difficult economic environment, just as management did with aesthetics, and I would expect the division to recover under more positive trading conditions.

Finally it’s worth noting that AbbVie no longer reports on its Women’s health division – a point of interest perhaps given it generated $673m and $796m in 2020 and 2021 according to historical revenue breakdowns.

There are three main reasons why I would view these results as a positive overall. Firstly, the outstanding performance of Skyrizi and Rinvoq. Secondly, the temporary nature of the aesthetics and eye care underperformance – these divisions can come back strongly as prevailing economic pressures ease. And finally, AbbVie has done a good job of increasing profitability – just as it promised to do when completing its ~$66bn acquisition of Allergan back in 2020.

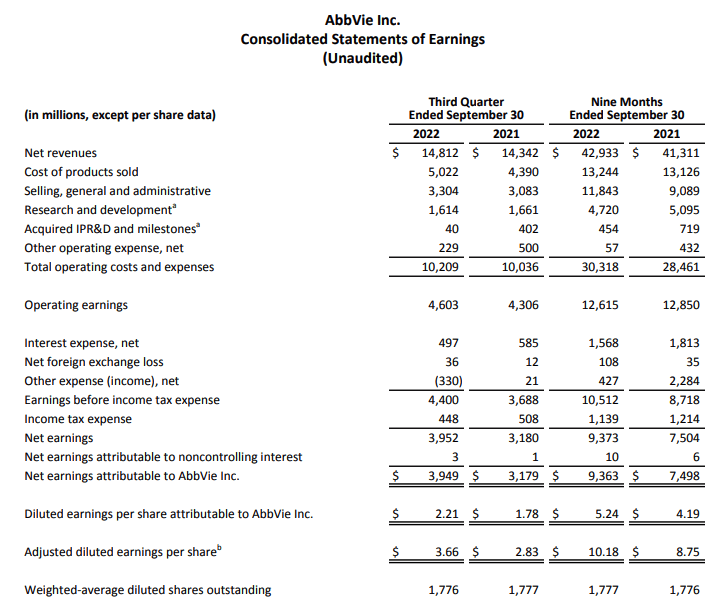

AbbVie 9m income statement for 2022 (AbbVie)

As we can see, net earnings across the first nine months of 2022 are a substantial 25% higher than in 2021, with adjusted earning per share of $10.20. Although AbbVie may have narrowed its FY EPS guidance – from $13.76-$13.96, to $13.84-$13.88, that implies a forward Price to Earnings (“PE”) of ~10.5x, which is a very healthy ratio. The average PE across the Big Pharma sector is closer to 23x.

The Humira Situation

Although Humira’s looming patent expiry is obviously not good news for AbbVie, the reality is that the Pharma has managed to preserve the drug’s exclusivity for nearly a decade longer than expected. Management has also been raising the price of Humira annually to try to cope with falling revenues in Europe, where the drug lost its patent protections in 2018.

As such, it is time for the Humira chapter of AbbVie’s young life to end – the drug has been largely responsible for the >325% rise in AbbVie’s share price since it was spun out of Abbott Laboratories in 2012 – and for a new chapter to begin, ushered in by the Allergan acquisition, and with new assets leading the way.

AbbVie is not going to entirely abandon its roots however since Skyrizi and Rinvoq are both indicated for a number of auto-immune conditions – plaque psoriasis, psoriatic arthritis, and Crohn’s disease in Skyrizi’s case, and rheumatoid arthritis, atopic dermatitis, ulcerative colitis and ankylosing spondylitis in Rinvoq’s case.

The burden rests on these two drugs more than any others in AbbVie’s portfolio if the Pharma is going to thrive in a post-Humira world – and so far the signs are very encouraging. In fact, although originally pegged for joint peak sales of ~$15bn, based on performance to date, management’s expectation now seems to be that the two drugs’ peak sales could eclipse Humira’s >$20bn per annum return.

One of the reasons that AbbVie stock is falling today is because analysts had expected more concrete guidance from management around what Humira’s sales will look like in 2023, which management did not provide. Interestingly, however, CEO Gonzalez did state, in relation to Humira:

So while it’s possible 2023 could outperform our guidance regardless of the shape of the erosion curve, we don’t anticipate 2024 earnings will be lower than the initial 2023 EPS guidance given the momentum and growth from another year of our ex-Humira portfolio, which is expected to more than offset any incremental Humira erosion in 2024.

I understand this to mean that whatever FY23 guidance AbbVie does provide, it expects performance to improve in 2024, so we now know that the worst case scenario will occur next year, and that things are expected to improve from 2024. Such performance – if achieved – speaks to good stewardship in my view – Humira is the world’s best selling drug after all – and it also means that investors who keep the faith and don’t sell on fears about Humira may be rewarded in the long run.

The Long Term Outlook

Of course, AbbVie needs to be more than its immunology division if it wants to maintain a good top and bottom line growth trajectory, and the Pharma could probably benefit from bulking out divisions less impacted by an economic downturn, to mitigate the risks implied by aesthetics and eye care.

The good news is, my research tells me that AbbVie could commercialise as many as 10 new drugs in the next 3-5 years – two more in the immunology division, easing the burden on Skyrizi and Rinvoq, three more in hematological oncology, plus one more targeting lung cancer, at least one more aesthetics product, two more neuroscience and one or possibly two more in eye care.

I won’t break down all of these new drugs in this post but I will share likely approval dates and peak sales revenues in my next post.

Suffice it to say that the valuations of pharmaceutical companies are often dictated by the products they are about to release rather than those already on the market – how else can you explain the fact that Eli Lilly’s (LLY) market cap valuation is higher than Pfizer’s (PFE), despite the former forecasting for ~$29bn of revenues in FY22, and the latter forecasting for ~$100bn?

The good news in AbbVie’s case is that my research tells me the company’s pipeline is robust, and by bulking out its immunology and oncology divisions it can secure its place amongst the Top 5 US Pharma’s – whilst its eye care pipeline drug RGX-314 – being developed with partner Regenxbio – is an exciting wildcard prospect – eye care markets in the indication of Wet and Dry Advanced Macular Degeneration are worth >$10bn – $20bn per annum.

Cash, Debt, and M&A

AbbVie took on a considerable amount of debt to acquire Allergan – the first major move in its attempts to wean itself off Humira revenues – but the company has managed the debt well.

On the Q322 earnings call Vice Chairman and President Rob Michael informed analysts that:

We generated $17 billion of free cash flow in the first nine months of the year, and our cash balance at the end of September was $11.8 billion.

Underscoring our confidence in AbbVie’s long-term outlook, today we announced a 5% increase in our quarterly cash dividend, beginning with the dividend payable in February 2023. And we remain on track to achieve $30 billion of cumulative debt paydown by the end of this year, bringing our net leverage ratio to 1.8 times.

That is impressive cash flow generation – to stand comparison with any Big Pharma company – and a very reasonable cash balance, suggesting there may even be funds for an acquisition or two. Clearly, the 5% dividend hike is good news for shareholders – it now stands at $1.48 per quarter, which translates to a yield of >4%.

And finally, the debt paydown has happened rapidly and the net leverage is not excessive, although the work here is not yet done – as at Q2’22, AbbVie reported current liabilities of >$35bn and long term debt of >$62bn.

Target Valuation

For me, AbbVie remains a solid bet in the “Big 8” US Pharma sector, which consists of, in order of market cap valuation Johnson & Johnson (JNJ), Eli Lilly (LLY), AbbVie, Pfizer (PFE), Merck (MRK), Bristol Myers Squibb (BMY), Amgen (AMGN) and Gilead Sciences (GILD).

I have used detailed financial modelling to try to establish the true value of AbbVie stock – I have shared this in previous posts and plan to update again in due course – and by my calculation a fair value would be around the $180 mark, implying a 15% premium to current price.

I base this on my expectation the company can generate ~$80m of revenues by 2030, and ~$23bn of net income, with revenues and net income rising in every year after 2023, and free cash flow growing from $17.5bn to ~$32bn by 2030. For my discounted analysis, I use a weighted average cost of capital (“WACC”) figure of 9.7% – broadly the same figure I use for all of my DCF analysis of large Pharmas.

Looking ahead, $80bn revenues is an ambitious target that will not be easy to reach, plus I am forecasting that AbbVie will continue to realise operational cost savings from the Allergan deal. The road ahead is challenging for AbbVie, but Pharma’s tend to trade higher than their DCF calculated view in my experience, due to the market’s excitement about new drug launches and (often overly high) peak revenue expectations.

In other words, there is some margin for error – AbbVie could be a $65bn-$70bn revenue Pharmaceutical and still merit a $300bn valuation if its pipeline is considered promising enough, or if it has a lower debt burden, higher dividend etc.

Conclusion – No Harm In Buying This Dip

There is no such thing as a riskless investment, but the US Pharma sector certainly offers risk mitigation, diversification, a strong dividend, transparency and an essential product portfolio, which is why I tend to keep a close eye on it.

In AbbVie’s case, Q2’23 earnings could have been better, and failed to provide many answers as to what 2023 and the Humira loss of exclusivity (“LOE”) might look like. Dig a little deeper, however, and we can see that management’s carefully laid plans – the Allergan takeover, the launch of Skyrizi and Rinvoq, the debt repayment, and the product pipeline – are generally coming to fruition.

As such, now does not seem like a bad time to be buying this mini-dip. AbbVie stock had an excellent start to 2022, with the share price hitting $175, before falling quite sharply and then trading flat across the next six months. In my view, these declines are more related to the external factors – inflation, recession, and the pandemic – than internal.

Those investors that know AbbVie well can likely see the long-term growth prospects more clearly than those whose focus is solely on analysts revenue estimates, and the former will probably be satisfied with these mixed Q3’22 earnings.

Disclosure: I/we have a beneficial long position in the shares of ABBV, BMY, GILD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

If you like what you have just read and want to receive at least 4 exclusive stock tips every week focused on Pharma, Biotech and Healthcare, then join me at my marketplace channel, Haggerston BioHealth. Invest alongside the model portfolio or simply access the investment bank-grade financial models and research. I hope to see you there.