Summary:

- Emraclidine’s failure in phase 2 trials is a significant setback for AbbVie’s neuroscience pipeline.

- This was a very surprising outcome after very strong phase 1b results and the success of competitor Cobenfy in clinical trials in schizophrenia patients.

- Emraclidine was the main reason AbbVie acquired Cerevel for $8.7 billion, and I expect a substantial impairment charge on this deal.

- Bristol-Myers Squibb’s Cobenfy comes out as the major beneficiary and will extend its leadership in the muscarinic drug class.

- Despite this setback, AbbVie is diversified enough to take the hit and continue to deliver long-term shareholder value.

J Studios

AbbVie Inc. (NYSE:ABBV) announced today that emraclidine failed in both phase 2 trials in schizophrenia patients. This is a shocking outcome and among the most surprising I have seen in quite some time considering the strong treatment effect of key competitor in the muscarinic drug class, Bristol Myers Squibb Company’s (BMY) Cobenfy (also known as KarXT), and the previous very strong phase 1b results of emraclidine itself. AbbVie is still analyzing the data from the two trials, but it is safe to say that this is a significant setback for the neuroscience pipeline and that we will be seeing a significant impairment of the $8.7 billion acquisition of Cerevel Therapeutics because emraclidine was the key asset gained through that acquisition.

Even if emraclidine is not a complete write-off, this sets back AbbVie’s muscarinic pipeline by at least several years, depending on the next steps. However, this does not break the investment thesis on AbbVie as the company is diversified enough to carry on and continue to deliver long-term shareholder value.

What went wrong in emraclidine’s phase 2b trial?

The muscarinic space was very hot in recent years, especially after the $14 billion acquisition of Karuna Therapeutics by Bristol Myers Squibb and the $8.7 billion acquisition of Cerevel Therapeutics by AbbVie. Our Growth Stock Forum model portfolio company Neurocrine Biosciences, Inc. (NBIX) played a fast-follower role by in-licensing a broad muscarinic portfolio from Nxera Pharma back in 2021 (it was called Sosei Heptares at the time and later changed the name to Nxera), and it recently delivered its own underwhelming dataset with NBI-568, although that one was not a complete failure like emraclidine delivered for AbbVie.

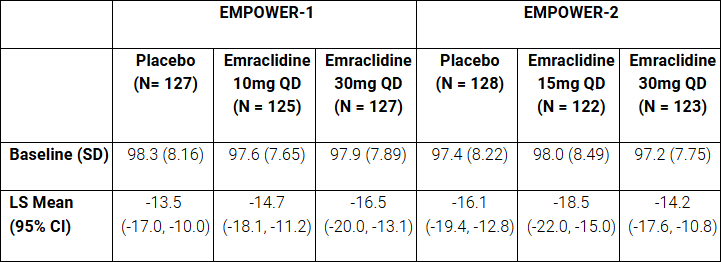

So, what went wrong with emraclidine? It had an excellent phase 1b dataset with a very strong treatment effect on the primary endpoint that was statistically significant compared to placebo, and it even looked better across trials to Cobenfy with a placebo-adjusted difference on the PANSS score between 11.1 and 12.7 compared to 8.4 to 9.6 for Cobenfy, according to its FDA label.

Cerevel 2021 press release

One possibility is that Cerevel conducted the phase 2 trials poorly, and the indication of that is the very high placebo response which was in the mid-teens compared to high single-digits in the phase 1b trial and in the phase 3 trials of Cobenfy.

As a reminder, the acquisition of Cerevel closed only three months ago and AbbVie merely inherited these two trials toward their end. We cannot know at this point, and it is always easy to blame trial conduct or an unusually high placebo response rate, and the next steps taken by AbbVie will tell us whether they think this was the issue.

AbbVie

The other possibility is that emraclidine does not work. Even if we take into consideration the high placebo response, emraclidine itself did not perform well. There was no dose response in the second trial, and the reductions in the PANSS score for three of the four dose arms were well below the reductions Cobenfy delivered in its two phase 3 trials, and below the reductions emraclidine delivered in the phase 1b trial.

Based on the available phase 1b and phase 2 data, I am not entirely sure, but would subscribe to the idea that, at best, emraclidine does not work as well as Cobenfy, or (more likely) that it does not work at all.

The key difference between emraclidine and Cobenfy is that emraclidine is a selective allosteric M4 agonist which means it acts on M4 indirectly and enhances the M4 receptor’s response, while Cobenfy is a selective and direct agonist of two muscarinic receptors – M1 and M4. The other difference is that emraclidine’s effects are limited to the central nervous system and that Cobenfy has trospium add-back therapy to deal with the muscarinic gastrointestinal side effects.

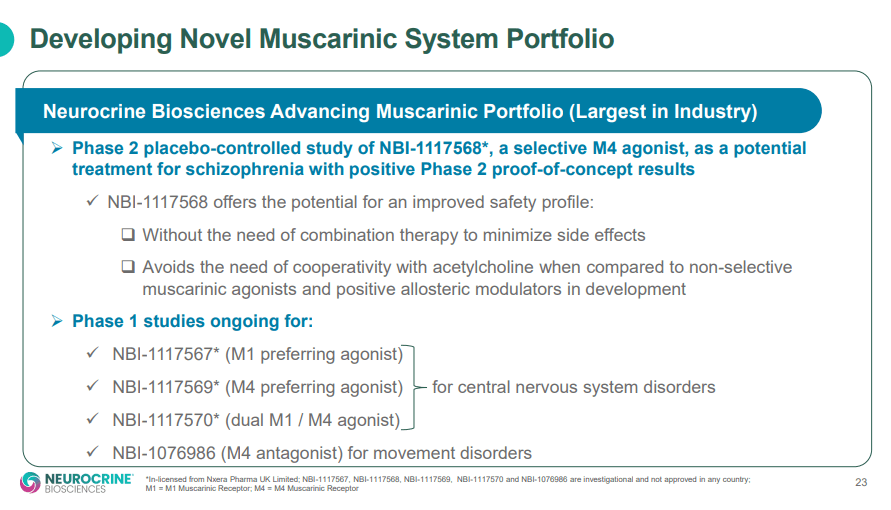

So, it is possible that allosteric modulation of M4 does not work, and competitor Neurocrine was saying this was one of its potential weaknesses since allosteric modulation of M4 required the “cooperation” of acetylcholine, the level of which varies in individuals and is reduced in older individuals. For this reason, Neurocrine is developing direct agonists, and it is now the closest to bringing a competitor to Cobenfy to the market – Neurocrine plans to start a phase 3 trial of NBI-568 in the first half of 2025.

The other possibility is that M1 agonism is required for muscarinic drugs to work and this is what Cobenfy has and emraclidine and NBI-568 do not.

As such, the failure of emraclidine casts some doubt on NBI-568 itself because investors (myself included) are now questioning if emraclidine failed because it does not have the M1 agonist component (NBI-568 is a direct agonist of M4 and does not agonize M1), or because it is an allosteric agonist. However, Neurocrine has a pipeline of muscarinic assets closely behind NBI-568, three of which are in phase 1 and all three are agonists of M1 and M4 with varying approaches – NBI-570 is an agonist of both M1 and M4, NBI-567 is M1-preferring and NBI-569 is M4-preferring.

Neurocrine investor presentation

The clear winner today is Bristol-Myers Squibb as Cobenfy will now extend its lead in the muscarinic space and there is now considerable doubt about the selective M4 approach.

Going back to AbbVie, until proven otherwise, I consider emraclidine a complete write-off.

What else is there at Cerevel?

Emraclidine was definitely the main reason AbbVie acquired Cerevel, but it is not the only asset gained through the acquisition. In the press release, AbbVie said the following:

In addition to emraclidine, through the Cerevel acquisition AbbVie gained a neuroscience pipeline of multiple clinical-stage and preclinical candidates that are complementary to the company’s existing neuroscience portfolio with leading on-market brands in psychiatry, migraine, and Parkinson’s disease.

And this is how Cerevel’s pipeline looked before the acquisition announcement.

Cerevel 2023 investor presentation

Since then, we have seen tavapadon deliver positive phase 3 results in Parkinson’s disease patients, and while I am not too excited about this candidate, it is a natural fit alongside the recently approved Vyalev and the existing Duodopa product in AbbVie’s Parkinson’s disease product portfolio and could help extract some value from the Cerevel acquisition.

The rest of the pipeline is either still unproven (darigabat) or preclinical, and this preclinical pipeline includes another M4 candidate, which could also be discontinued after emraclidine’s failure.

Overall, after emraclidine’s failure, the Cerevel acquisition does not look great, and I expect a substantial majority of the $8.7 billion acquisition to end up as an impairment charge.

Conclusion

The phase 2b results of emraclidine are very disappointing and will likely result in a substantial write-off of the Cerevel acquisition and until proven otherwise, I assume the development of emraclidine will be discontinued. The best-case scenario would be AbbVie determining the study conduct was not proper and that it decides to start a new trial, but even this scenario results in a setback of several years and a very uncertain outcome in new clinical trials.

And while I expected emraclidine to be one of the more important growth drivers for AbbVie’s neuroscience pipeline in the second half of the decade and more so in the 2030s, this is by no means an investment thesis killer for the company and I continue to see it as well-positioned to deliver long-term shareholder value. I expect the company to be able to develop or acquire new assets that will make up for the loss of emraclidine.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NBIX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article reflects the author's opinion and should not be regarded as a buy or sell recommendation or investment advice in any way.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

I publish my best ideas and top coverage on the Growth Stock Forum. If you’re interested in finding great growth stocks, with a focus on biotech, consider signing up. We focus on attractive risk/reward situations and track each of our portfolio and watchlist stocks closely. To receive e-mail notifications for my public articles and blogs, please click the follow button. And to go deeper, sign up for a free trial to Growth Stock Forum.