Summary:

- ABBV has outperformed expectations, with Humira remaining the market leader with 98% share despite the LOE and biosimilar headwinds.

- Combined with Elahere’s recent US FDA approval with a projected TAM of $17.9B, we believe that the management may continue to deliver robust shareholder returns ahead.

- However, we expect to see ABBV’s balance sheet to moderately deteriorate from current levels, as the ImmunoGen and Cerevel acquisitions close.

- Combined with the US FDA approval of Simlandi as a direct interchangeable biosimilar, we believe that there may be moderate headwinds to Humira’s sales in 2024.

- As a result, we prefer to maintain our previous Hold rating here, though existing shareholders may continue subscribing to their ongoing DRIP program to regularly accrue more shares on a quarterly basis.

izusek

We previously covered AbbVie Inc. (NYSE:ABBV) in January 2024, discussing why its M&A activities had proven to be more promising than those of its peers, attributed to the lower price tags and higher potential returns by the next decade.

While the same balance sheet headwind persisted, it was apparent that the biotech company boasted a relatively robust immunology portfolio, which continued to be its top-line driver no matter Humira’s Loss Of Exclusivity [LOE].

Then again, those tailwinds had contributed to the stock’s baked-in premium valuations and optimistic stock rally, with us preferring to wait for a moderate pull back before buying in when the stock yields 5% or more.

In this article, we shall discuss how ABBV has outperformed expectations, with Humira remaining the market leader despite the LOE and biosimilar headwinds.

Combined with its pipeline’s recent US FDA approval, we can understand why the market continues to award the stock with the stable FWD P/E valuations, further aided by the robust shareholder returns.

Despite so, we prefer to prudently maintain our Hold rating here, with there likely to be moderate headwinds to Humira’s sales in 2024 as a directly interchangeable biosimilar is approved by the US FDA.

The ABBV Investment Thesis Remains Interestingly Enduring

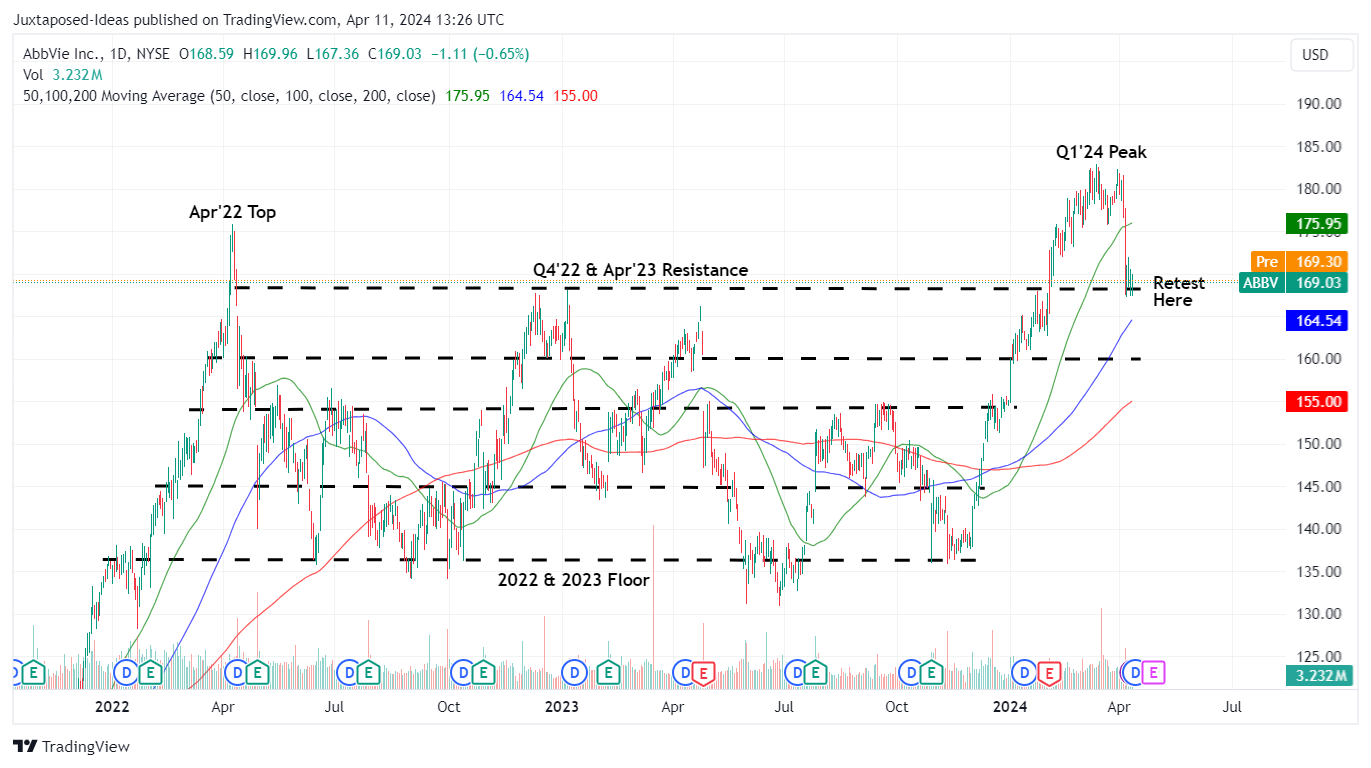

ABBV 2Y Stock Price

TradingView

For now, ABBV has dramatically lost much of its recent gains, thanks to the lowered FQ1’24 and FY2024 earnings guidance, while appearing to be well supported in its previous resistance levels of $160s.

For context, the management has originally offered an FY2024 adj EPS guidance of $11.15 at the midpoint (+0.3% YoY) in February 2024, including a $0.32 dilutive impact from the ImmunoGen and Cerevel Therapeutics acquisitions, with FQ1’24 adj EPS guidance of $2.28 (-18.2% QoQ/ -7.3% YoY).

By April 2024, ABBV has lowered its FY2024 adj EPS guidance to $11.07 (-0.3% YoY) and FQ1’24 guidance to $2.20 at the midpoint (-21.1% QoQ/ -10.5% YoY), with most of the bottom-line headwinds attributed to acquire in-process R&D and milestones expenses.

The latter is unsurprising indeed, since the management has went on an aggressive acquisition spree over the past few years, with the newest being Landos Biopharma, Inc. (LABP) for $137.5M – for an ulcerative colitis therapy candidate with a projected TAM of $10.8B by 2030.

This builds upon the other acquisitions and partnerships discussed in-depth in our previous article.

It is apparent by now, that ABBV is attempting to further beef up its pipeline, as Humira records a drastic decline in net global sales to $14.4B in FY2023 (-32.1% YoY) as the LOE expires by early 2023.

This patent loss has drastically affected the pharmaceutical company’s FY2023 revenues to $54.31B (-6.4% YoY) and adj EPS to $11.11 (-19.3% YoY), likely attributed to Humira’s lowered average prices by -37.9% on a YoY basis, from $48K in 2022 to $29.8K in 2023.

While this strategy has allowed Humira to retain its leadership with 98% market share, it is apparent that the therapy may no longer be a top/ bottom line driver moving forward, naturally explaining the management’s intensified pipeline efforts above.

With most of ABBV’s new partnerships bearing upfront cash payments and milestone related payments, on top of the expensive acquisitions, it is unsurprising that we may see some impact on the pharmaceutical company’s balance sheet ahead.

For now, ABBV reported a relatively healthy balance sheet with moderating net debts of -$39.38B and net-debt-to-EBITDA ratio of 1.49x in FQ4’23, compared to -$49.93B/ 1.58x in FQ4’22 and -$23.05B/ 1.41x in FQ4’19.

While this number may be higher than the Biotechnology sector average ratio of 0.45x, it is still decent compared to its direct peers, Merck (MRK) at 1.42x, Pfizer (PFE) 4.26x, and the General Drug Manufacturers at 2.04x.

With the ImmunoGen deal recently completed in February 2024 and ABBV set to report FQ1’24 earnings on April 26, 2024, readers may want to pay attention as to how the management has opted to finance this deal, due to the expensive borrowing costs at the moment.

On the other hand, the ImmunoGen deal has already delivered an US FDA approval for Elahere as a treatment for ovarian cancer in March 2024, with it to be directly accretive to the company’s long-term financial performance given the projected TAM of $17.9B by 2031, well worth the $10.1B price tag.

This also builds upon the pharmaceutical company’s growing pipeline, with over 50 programs in mid to late stage clinical trials and $7.67B in R&D expenses in FY2023 (+17.8% YoY), implying the management’s determination to deliver new growth opportunities.

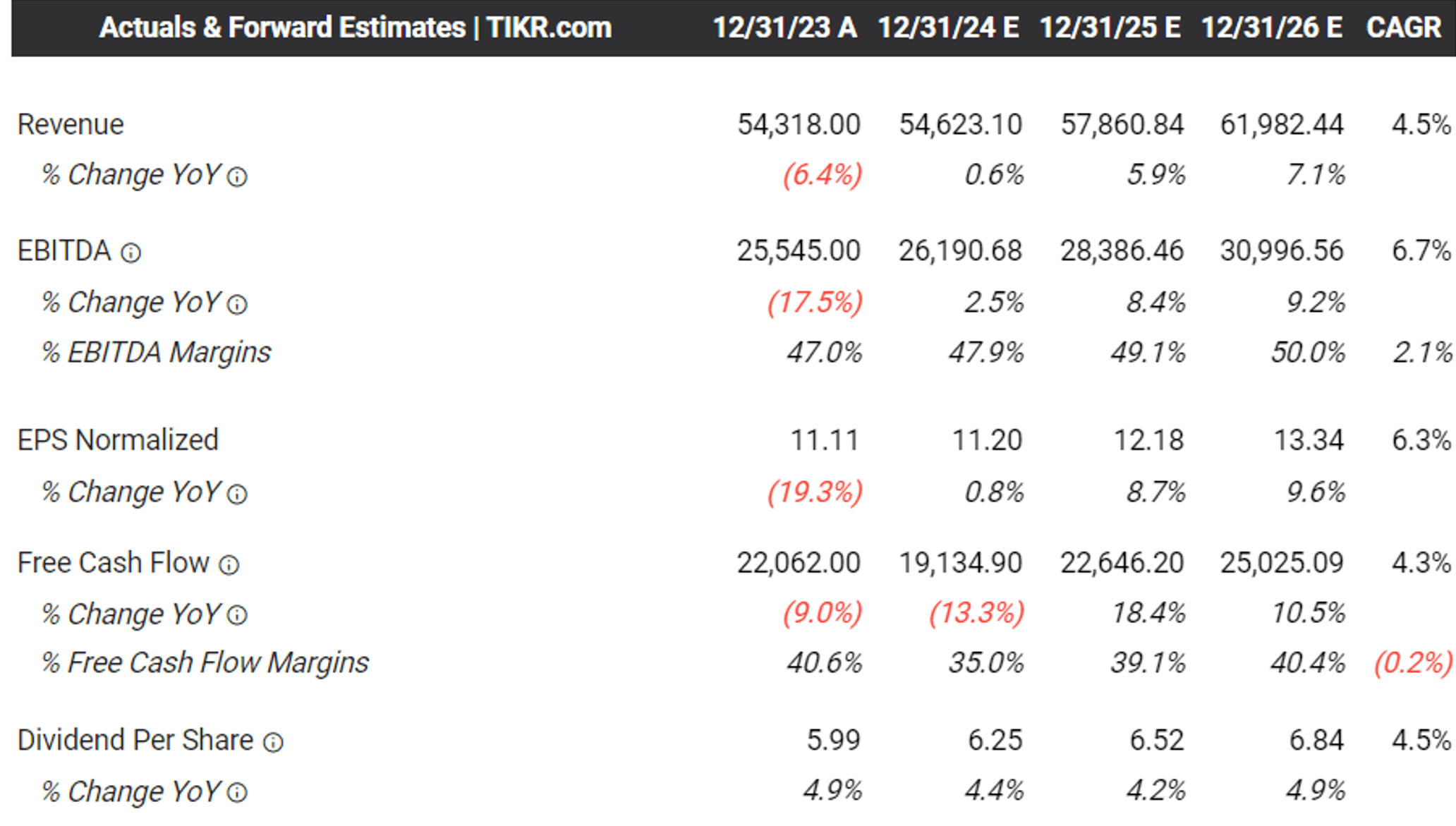

The Consensus Forward Estimates

Tikr Terminal

The same has been projected by the consensus, with ABBV expected to record a raised top/ bottom line expansion at a CAGR of +4.5%/ +6.3% through FY2026.

This is compared to the previous estimates of +2.5%/ +5.1% and the historical CAGR of +11.3%/ +12.6%, respectively, implying the market’s conviction about Humira’s LOE being a temporal headwind.

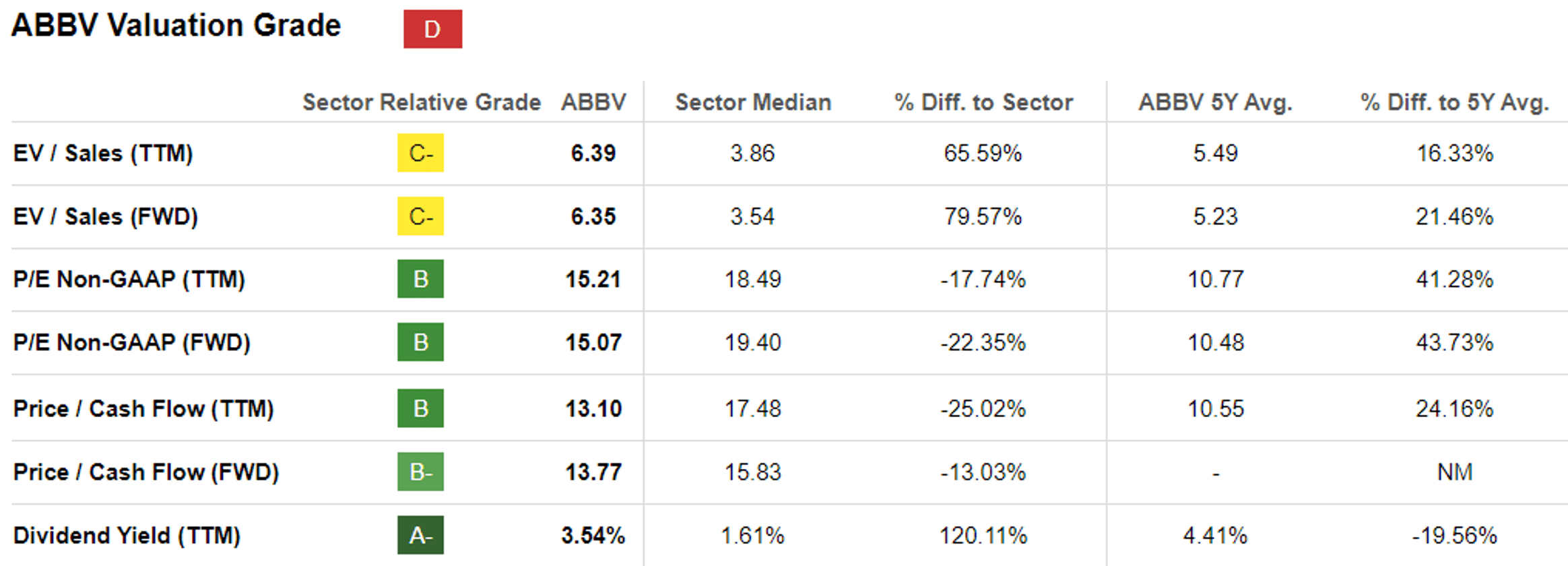

ABBV Valuations

Seeking Alpha

As a result of the promising factors discussed above, we can understand why ABBV continues to be awarded the relatively stable FWD P/E valuations of 15.07x and FWD Price/ Cash Flow valuations of 13.77x, compared to its 1Y mean of 15.21x/ 11.19x and MRK at 14.78x/ 12.56x, respectively.

The comparison with MRK is prudent indeed, since the latter faces a similar LOE headwind for Keytruda in 2028, as the management also engages on numerous acquisitions/ partnerships to balance the upcoming patent expiry.

For now, based on the FY2023 adj EPS of $11.11 (after including the 2023 acquired IPR&D/ milestones expenses) and the FWD P/E valuations of 15.07x, it is apparent that ABBV is trading near our fair value estimates of $167.40, significantly aided by the recent pullback.

Based on the consensus FY2026 adj EPS estimates of $13.34, there seems to be an excellent upside potential of +18.9% to our long-term price target of $201.00 as well.

Readers must also note that ABBV is a stock that is highly shareholder friendly, based on the 5Y Dividend Growth Rate of +8.68% compared to the sector median of +6.33%.

This is on top of the relatively stable share count and sustained deleveraging over the past few years, demonstrating the management’s competent use of the robust free cash flow of $22.06B in FY2023 (-9% YoY).

As a result of these developments, we can understand why ABBV may look tempting here, with the stock’s recent rally by +21% from the October 2023 bottom (nearly mirroring the wider market at +24%) also triggering the moderation in its forward dividend yields to 3.67%, compared to its 5Y average of 4.58%.

Combined with the interestingly durable Humira sales, we admit that we have been overly prudent in our previous Hold articles indeed.

So, Is ABBV Stock A Buy, Sell, Or Hold?

However, this does not mean that we are suddenly reversing our Hold rating to Buy now, in contrast to our recent MRK article, with the latter’s Keytruda LOE still a distance away in 2028.

While ABBV’s Humira may continue to dominate the market, its sales erosion is bound to happen with the LOE already here, especially with the ongoing PBM anti-trust probe.

This is on top of the US FDA approval of Alvotech’s (ALVO) and Teva Pharmaceutical’s (TEVA) directly interchangeable option for Humira, Simlandi, with the added benefit of being the only citrate-free, high-concentration biosimilar (less painful administration) at the time of writing.

While there has been multiple efforts by the ABBV management to beef up the pipeline along with the numerous US FDA approvals, there is no denying the painful impact from Humira’s LOE on the pharmaceutical’s top/ bottom lines in the intermediate term.

As a result, we prefer to maintain our previous Hold rating here, though existing shareholders may continue subscribing to their ongoing DRIP program to regularly accrue more shares on a quarterly basis.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.