Summary:

- AbbVie has outperformed the S&P 500 since my previous update in early July, urging investors to buy despite market pessimism.

- AbbVie’s prelim-Q2 earnings update likely spooked some investors to sell their shares at the lows. However, the company’s robust actual Q2 performance helped calm undue fears.

- Investors unduly concerned about Humira’s biosimilar erosion are not paying enough attention to the company’s well-diversified portfolio.

- Analysts’ estimates suggest AbbVie’s adjusted EPS could bottom out in FY23, indicating the worst is likely over.

- I make the case for why ABBV’s recent surge has normalized its valuation and is no longer as attractive. However, investors are urged to keep their exposure and ride the recovery.

JHVEPhoto

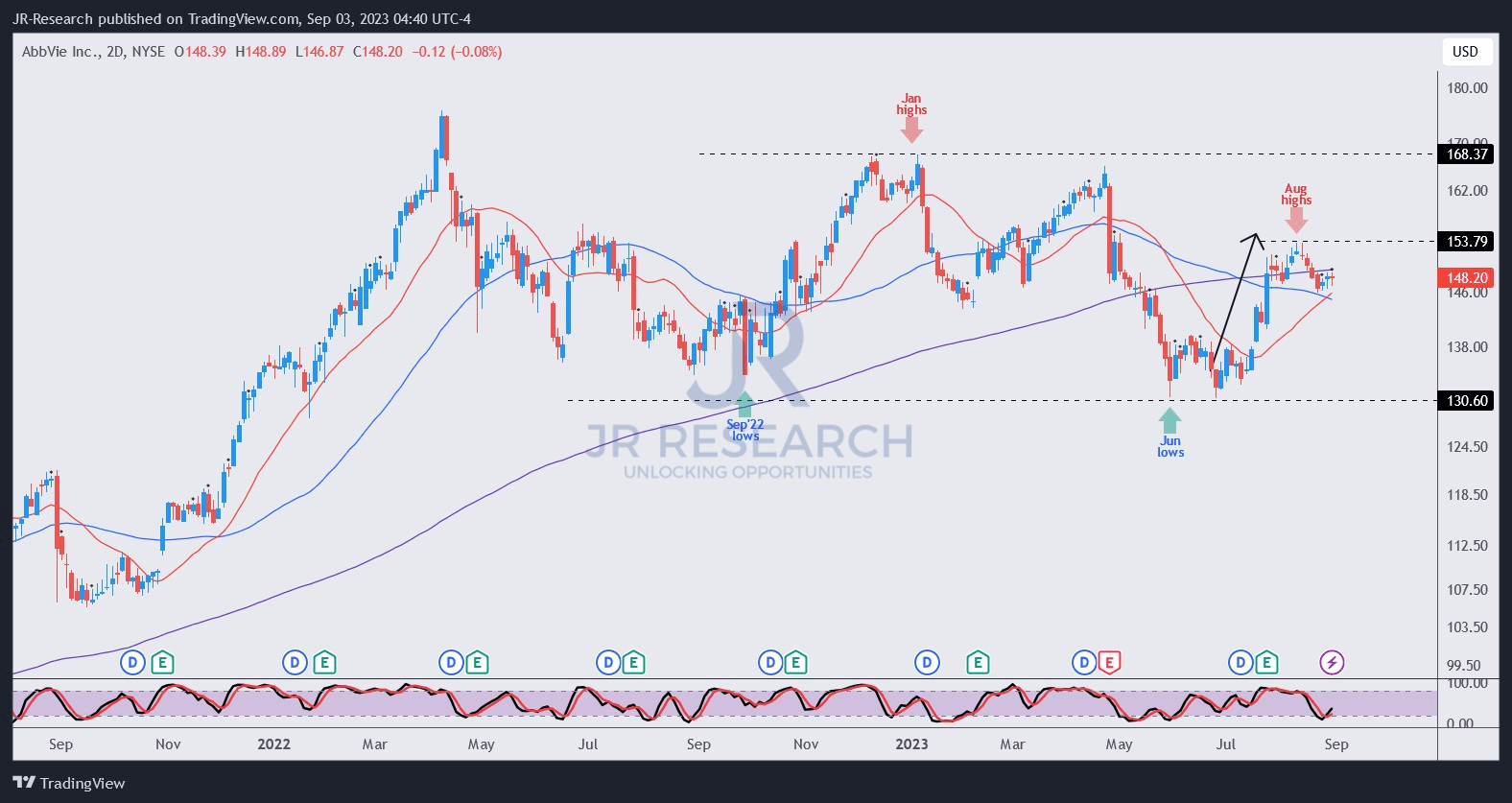

AbbVie Inc. (NYSE:ABBV) investors breathed a sigh of relief as ABBV has recovered remarkably from its June 2023 lows despite posting a prelim-Q2 earnings release in early July that likely spooked some investors.

However, ABBV dip buyers held those lows robustly, demonstrating to unconvinced investors that the market had already priced in significant pessimism. In my early July update, I encouraged investors to buy more shares, discussing why I saw buyers accumulating quietly. I maintained my conviction that ABBV’s “June bottom remains robust, forming a bear trap or false downside breakdown.” As such, investors who failed to observe ABBV’s buying momentum and sold at its June lows didn’t manage to participate in its recent upward surge.

Accordingly, ABBV has risen nearly 10% on a total returns basis, outperforming the S&P 500’s (SPX) (SPY) 3% rise over the same period since my previous article. I believe the optimism is justified, as I argued previously that ABBV was “no longer significantly overvalued” at its early July lows.

AbbVie upped the ante in its Q2 earnings release by raising its full-year guidance, corroborating the robust growth drivers in its ex-Humira portfolio. Humira posted a revenue decline of 25% in Q2 due to intensifying biosimilar competition. However, AbbVie’s immunology portfolio held up well, attributed to the spectacular performance of Skyrizi and Rinvoq, as both posted revenue growth exceeding 50%.

In addition, management’s commentary suggests the company increased its confidence in a better-than-anticipated outcome despite the biosimilar entries, which led to an improved outlook. In addition, the company also saw a strong performance from its aesthetics portfolio, particularly in the international markets, highlighting the resilience of its well-diversified portfolio.

Revised analysts’ estimates suggest AbbVie’s revenue decline could bottom out in FY23 before reversing upward toward a flat YoY growth in FY24. However, the headwinds on Humira’s erosion are expected to continue playing out before stabilizing between 2025-26. Hence, I assessed that while investors’ sentiments are expected to remain cautious, the worst in ABBV is likely over. Therefore, dip buyers who bought into ABBV’s June lows are encouraged to keep holding on to their positions and wait for steep pullbacks reflecting panic/market capitulation to add more positions.

Furthermore, AbbVie’s adjusted EPS is expected to reach its nadir in FY23 before inflecting upward to growth through FY26. Analysts’ estimates on AbbVie are assessed to be more cautious despite management’s confidence in achieving high-single-digit growth on average through 2030.

Investors should also consider the impact of the recent developments in the Medicare price negotiations, as the initial list of drugs was unveiled. It includes Imbruvica, which experienced a revenue decline of more than 20% in Q2.

Management’s commentary suggests it’s likely not unanticipated, as the company stressed, “Imbruvica is a product that is close to the cutoff point for inclusion in the first 10 products.” Despite that, the company telegraphed that it “anticipates being able to manage the effects through strategies such as inflation penalties, party benefit redesign, and negotiations.” Moreover, these challenges are not likely to intensify near-term challenges as the “negotiated” pricing discounts are expected to be effective only in 2026.

ABBV price chart (weekly) (TradingView)

As seen above, ABBV has surged from its June lows, corroborating my thesis that it was at peak pessimism, as investors “likely reflected substantial headwinds relating to Humira’s patent expiration.”

Therefore, astute dip buyers who ignored the market’s pessimism and capitalized on the fantastic buying opportunities have performed well.

That said, ABBV has moved closer to being overvalued again. Despite that, I anticipate investors holding on to their exposure as it continues its recovery from its hammering.

With my Buy thesis playing out, I encourage investors to keep their exposure. I will reassess another opportunity for dip buyers to re-enter moving ahead if I glean a steeper pullback.

Rating: Downgraded to Hold. Please note that a Hold rating is equivalent to a Neutral or Market Perform rating.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!