Summary:

- AbbVie shares dropped nearly 10% after its schizophrenia drug emraclidine failed in late-stage trials.

- The market reaction appears excessive and presents a buying opportunity.

- Dividend yield and robust drug pipeline are bullish going forward.

hapabapa

AbbVie (NYSE:ABBV) shares are plummeting as the company’s schizophrenia treatment drug reportedly failed to meet its primary endpoint in a late-state study. While certainly a blow, the resulting drop of nearly 10% as I write this appears to be significantly overdone, and I think investors could benefit from buying this dip.

Shares of AbbVie experienced one of their worst declines in the history of the company in Monday trading after announcing that its schizophrenia treatment drug, emraclidine, failed to meet its primary efficacy endpoint in late-stage trials. The company stated:

[Emraclidine trials] did not meet their primary endpoint of showing a statistically significant reduction (improvement) in the change from baseline in the Positive and Negative Syndrome Scale (PANSS) total score compared to the placebo group at week 6.

And Chief Science Officer Roopal Thakkar further stated:

“While we are disappointed with the results, we are continuing to analyze the data to determine next steps.”

There doesn’t appear to be much of a silver lining here for AbbVie except that the safety profile was up to snuff, so that’s good, I guess. Emraclidine was acquired in the purchase of Cerevel Therapeutics back in late 2023, which closed just 3 months ago in August for a final sum of $8.7 billion. Cerevel also has a number of other drugs in development, including for the treatment of dementia and Parkinson’s, so the acquisition isn’t a total bust yet.

But I think part of the reason we’re seeing such a significant sell-off is that it does bring into question the potential path to approval for the other drugs in the pipeline that AbbVie got from Cerevel. Now, the pharma business is always a bit of a crap-shoot for novel drug therapies, but there could be some lingering market fears that, if similar methodology was used to create these drugs, the failure of Emraclidine could signal trouble for the pipeline as a whole.

Whether that’s the case or not, the worst-case scenario doesn’t warrant the price action we’re seeing regardless. In response to the news, AbbVie has shed more than $40 billion in market capitalization, which seems excessive considering the original deal for Cerevel was a fraction of that cost and considering some analysts expected the drug to bring in around $1 billion in annual revenue. Perhaps one could claim that the drop isn’t just about the cash used for the acquisition but also about the potential market opportunity the drug could have captured. But even that would be a stretch considering Bristol-Myers Squibb (BMY), which received FDA approval for its schizophrenia treatment drug Cobenfy back in September, jumped Monday on the news but only by about $12 billion in market cap. That number seems closer to reality for me, and the fact ABBV has lost more than 3 times that value indicates the sell-off is overdone in my opinion.

I think perhaps another factor at play here is market fears over the decline of sales for Humira, which has been a cash cow for AbbVie, but has suffered as generics have entered the market. Investors are concerned over where future revenue and cash flow will come from as both have seen declines over the last 12 months, and the failure of emraclidine is just another blow to the bull narrative. A further deterioration of operating results appears to be a concern.

However, even if the market is concerned about the rest of the Cerevel pipeline and declining financials, I think investors should treat this as a buying opportunity. The stock now offers a dividend yield of more than 3.7% and is trading at just 14.5 times expected 2025 earnings, which is well below the sector average. Drug failures are just a fact of life in pharma, and anytime you see a blue-chip stock like ABBV lose $40 billion in market cap in one day from one drug that didn’t meet its endpoint, that’s likely an indication of an opportunity.

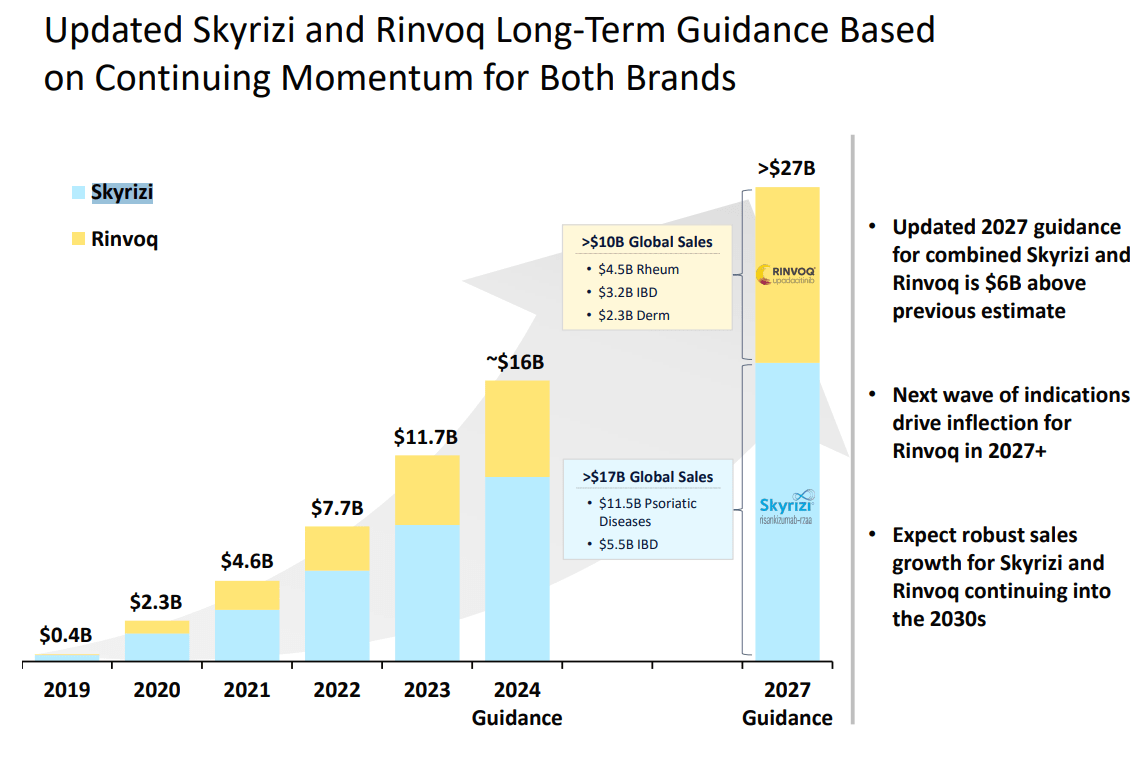

The company still has an extremely robust drug pipeline, including the expected rapid growth of Skyrizi and Rinvoq over the next few years:

AbbVie Pipeline Presentation

While the failure of emraclidine is no doubt a setback, it was not an opportunity that was worth more than 10% of ABBV’s valuation in my view.

I’m rating ABBV a Buy.

Thanks for reading!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.