Summary:

- Accenture’s stock prices have corrected by more than 25% recently, presenting a buying opportunity for potential investors.

- Analysts project a compound annual growth rate of 12.6% for Accenture’s EPS over the next five years.

- The projection is well-supported by strong earnings catalysts like digital transformation, AI, and external acquisitions.

z1b

ACN Stock Prices Corrected For More Than 25%

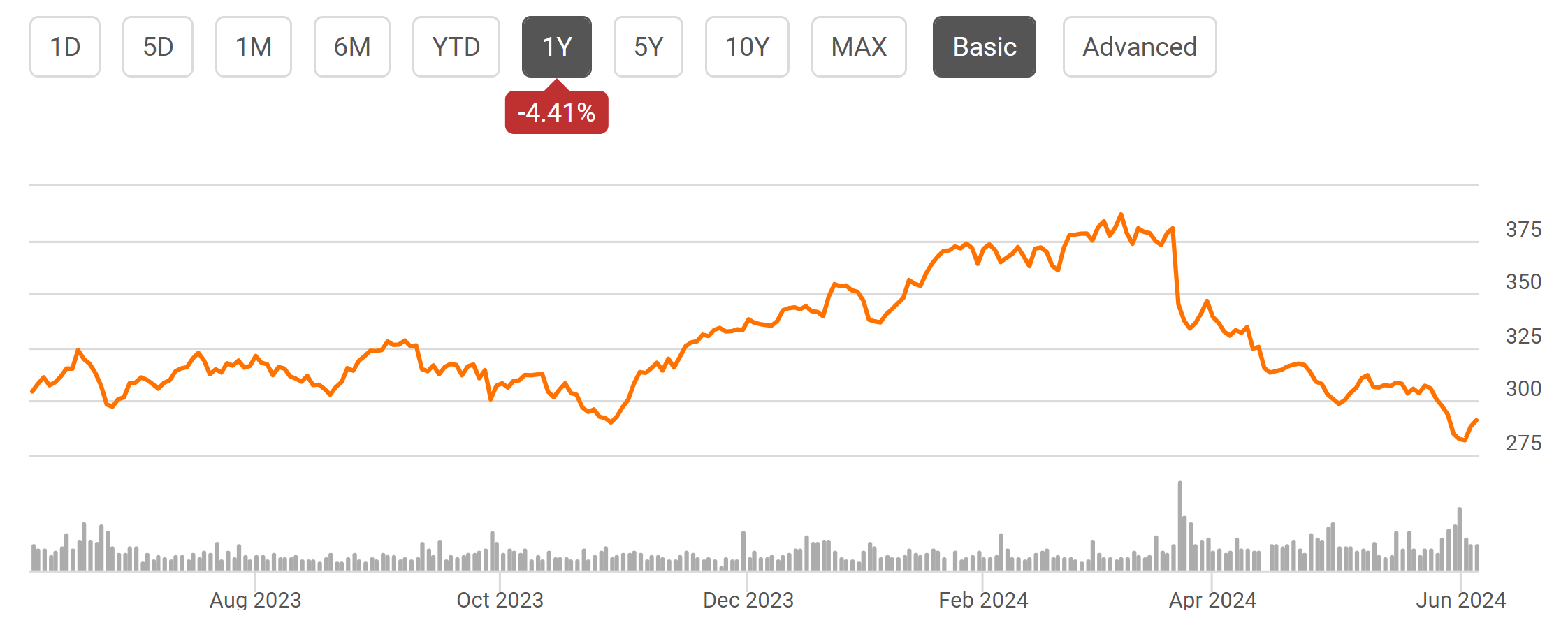

Accenture (ACN) recently suffered a large price correction, as seen in the chart below. The stock prices reached a 52-week high of around $387 in March 2024. The stock price then declined sharply to the current level of $291, translating into a loss of about 25%.

Against this background, the thesis of this article is to argue that such a decline in share price offers a solid opportunity for potential investors. There surely will be some short-term difficulties for its core business (more on this later). But looking past these temporary challenges, I see the current conditions as an opportunity to buy a wonderful business at a fair – or even discounted – price.

Seeking Alpha

To be perfectly clear, despite the large correction, the company’s valuation is by no means cheap in absolute terms. As you can see from the chart below, which summarizes ACN stock’s valuation grade, its TTM P/E ratio is 24.46 on a non-GAAP basis and is at a slight premium to the sector median (by about 6.63%). However, In the remainder of this article, I will explain that the premium is well justified, and the valuation is very reasonable relative to its growth potential, especially given the ACN’s initiatives in the emerging AI market. Also note that its current valuation is at a sizable discount relative to its own historical averages.

Seeking Alpha

ACN Stock: EPS And Growth Outlook

The market has a robust projection for its EPS growth, as you can see from the following chart, which shows the consensus EPS estimates for ACN stock in the next 5 years. Based on the chart, analysts expect ACN’s EPS) to grow at a compound annual growth rate (“CAGR”) of 12.6% over the next five years. This translates to a growth of EPS of $12.15 for fiscal year 2024 to $19.55 in FY 2028. At this projected growth rate, ACN’s forward P/E ratio is expected to decline rapidly from the current level of 23.95x to only 14.89x by 2028.

Seeking Alpha

I see very good catalysts to support the above growth projection. The top two catalysts in my mind are its AI initiatives as aforementioned and also bolt-on acquisitions. I anticipate generative AI to support ACN’s long-term growth prospects. Generative AI has advanced to a degree that many of ACN’s clients (and ACN itself too) can leverage it to create new content, such as audio, code, images, and text. Bookings at ACN for this new technology have been doing excellent in my view, with $1.1 billion in the first half of fiscal 2024 (compared to $300 million in all of fiscal 2023). Looking further out, ACN plans to double its AI workforce to 80,000 by the end of fiscal 2026. This investment positions ACN well to support projects with big-name clients, in my view. A possible example is Best Buy, where ACN could use AI expertise to reinvent the customer experience, improve employee experience, and reduce operating costs.

Besides AI, I see acquisitions as another strong growth driver. ACN boasts a strong balance sheet and strong cash flow. I anticipate it to keep leveraging these strengths for bolt-on acquisitions. In fiscal 2024 alone, ACN has spent a total of $2.9 billion on 23 bolt-on deals by my counting. These deals include Insight Sourcing, Navisite, Impendi, and OnProcess Technology. ACN has been quite savvy in these acquisitions to augment this core area and accelerate its growth. For example, it recently acquired Teamexpat and several other firms to strengthen its embedded software expertise (more details are quoted from the news release below).

Accenture (NYSE: ACN) has acquired Teamexpat, an embedded software specialist for complex high-tech products and systems, headquartered in Eindhoven, the Netherlands… Other acquisitions Accenture has made to strengthen its embedded software, digital engineering and smart, connected products capabilities include international engineering services firm umlaut, German embedded software company ESR Labs, and Dutch product design and innovation agency VanBerlo.

ACN Stock: Dividends In Focus

Another sign of fair (or slightly discounted valuation) is its dividends. The chart below shows ACN’s dividend yield compared to its historical average in the past 5 years. As you can see, ACN’s current dividend yield is 1.71%, it is not only far higher than the average dividend yield over the past five years (1.34%) but also among the highest levels in this period. Moreover, the dividends feature superb safety (thanks to its strong balance sheet and cash generation as aforementioned), growth, and consistency as you can see from its dividend grades. Given the safety and consistency of its dividends, I consider the dividend payouts a reliable indicator of its true owner’s earnings in the long term and yield a more reliable valuation indicator than accounting P/E ratios.

Seeking Alpha Seeking Alpha

Other Risks And Final Thoughts

There are also a few other upside risks worth mentioning. As a global leader in the IT consulting space, the strong U.S. dollar makes ACN’s international services cheaper and thus more competitive than domestic players. ACN is also a consistent buyer of its own stocks. As you can see from the chart below, the net common buyback yield is about 1.4% on average, actually higher than its cash dividend payouts, another indication of its strong financials.

Seeking Alpha

In terms of downside risks, two major risks come to my mind. The first risk facing ACN (and its IT consulting peers too) is the dependence on the overall tech spending environment. A slowdown in tech spending by corporations, driven by economic factors or a shift in priorities, could significantly impact ACN’s revenue growth. This is the key factor that triggered the recent large correction in my view and the headwinds could persist longer. But ultimately, I consider these headwinds as temporary and only phases of the business cycle.

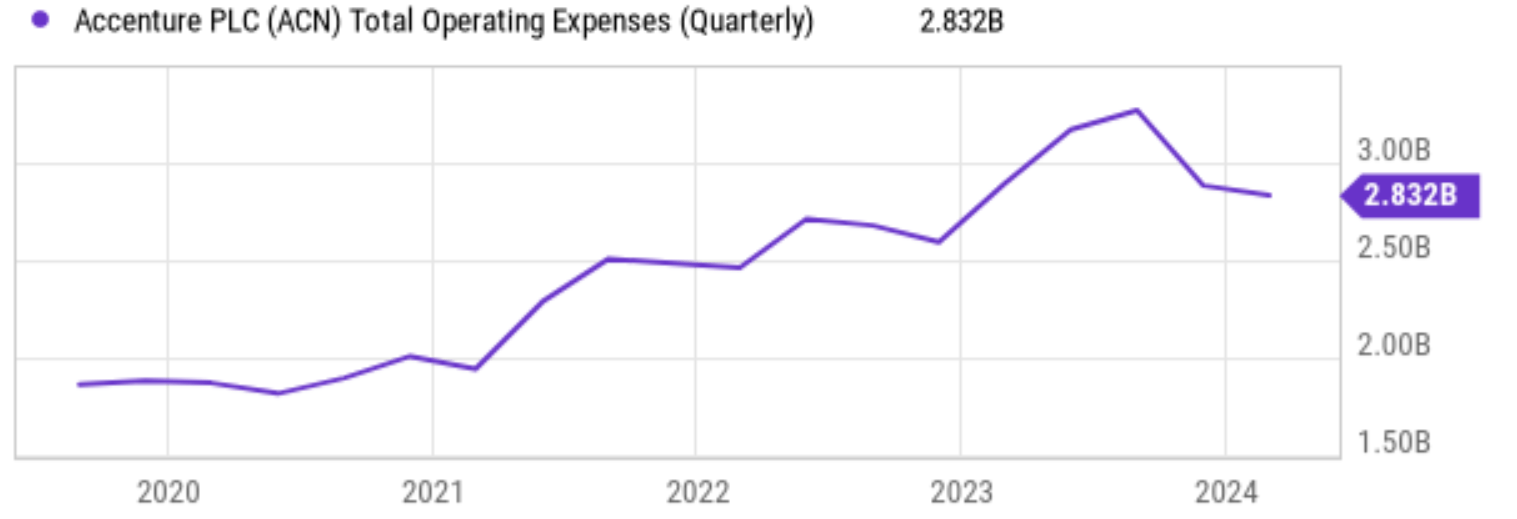

The second risk involves ACN’s ability to control costs. ACN’s operating expenses have been increasing rapidly in the past few quarters. As you can see from the chart below, the operating expenses almost doubled in the past 3 years between 2021 and 2024. Looking ahead, ACN must navigate the increasingly competitive landscape for highly skilled talent, particularly in areas like cloud computing and cybersecurity. The ability to attract talent and expand its expertise pool, while keeping costs under control is crucial for ACN to deliver on its client projects and maintain its competitive edge.

All told, my overall conclusion is that the upside far outweighs the downside. The recent price dip presents a compelling buying opportunity. The P/E is not cheap in absolute terms, even with the 25% price dip. But the valuation is very reasonable or even discounted in my view, considering the double-digit EPS growth potential, strong earning catalysts like digital transformation and AI, and external acquisitions. Additionally, the dividend yield (of 1.7%) and consistent buybacks (around 1.6% currently) provide further downside protection, all backed by superb dividend grades and a strong balance sheet.

Seeking Alpha

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.