Summary:

- Accenture gets Sell rating today, seen as great opportunity to profit from the March price dip.

- Valuation is higher than sector average, dividend yield lower than sector average, share price well above 200 day SMA.

- Net income YoY positive growth, capital & liquidity situation healthy.

noel bennett

Research Brief

As an analyst tracking stocks in the tech, financial, and innovation sectors, today I wanted to cover global managed solutions provider Accenture (NYSE:ACN), a business that traverses all of those segments.

More importantly, as a former Accenture subcontractor at one of their Austin Texas clients in the digital space, I know firsthand the value proposal that these “external consultants” offer to large enterprises in the US & European markets.

In fact, I would imagine many people outside of corporate America are not aware just how many temporary company roles & projects are staffed by Accenture or one of its cooperants. For example, not everyone at Google (GOOG) or Microsoft (MSFT) actually is an employee of those firms, in fact many are not but are contractors. The consulting/contracting/MSP space is a multi-million dollar business segment.

But is this firm a value buy for investors, at this time? That is the question I hope to answer with today’s analysis.

Some notables to mention about this company, from its official website: 738K worldwide employees, 9K clients across 120 countries, its federal government contracting division Accenture Federal Services won a $380MM contract to modernize IT operations for US Customs & Border Protection, announced in March.

Ratings Methodology

Our goal is to find undervalued stocks of companies with solid financial fundamentals, that pay competitive dividend yields. Our key industry focus is tech, financials, insurance, innovation.

To simplify my rating of an equity, I have broken it down into whether I would recommend or not recommend based on these individual factors:

- Valuation.

- Dividend Yield.

- Net Income Growth.

- Capital & Liquidity.

- Share Price vs Moving Average.

If I recommend on all 5 categories, it is a “strong buy”, 4 categories is a “buy”, 3 is a hold, and less than that is a sell rating. Then I compare my rating to the consensus ratings from Seeking Alpha & Wall Street.

Valuation: Not Recommended

Some time ago, I used to watch a show called Shark Tank which was big in the US and Canada, and one of the hosts, fellow Croatian-American Robert Herjavec, would often make investment decisions on a startup based on the valuation presented to him by that startup. Some of the valuations, if I recall, were largely overinflated.

When analyzing established, large global firms like Accenture, I too think about valuation and whether the market is currently overvaluing that company’s stock, since I am thinking about a good buying point to enter a position.

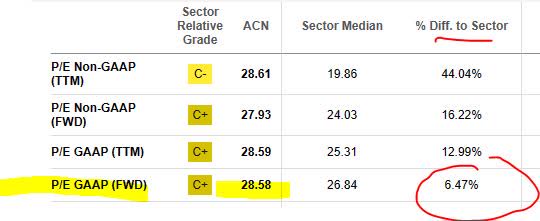

To simplify things, I look at the GAAP-based forward price to earnings ratio (P/E) and the forward price to book ratio (P/B), taken from Seeking Alpha data.

As of August 2nd data, I am concerned that with a P/E of 28.58 this stock is over 6% above its sector average on this metric. So, I would be paying almost 29x earnings for this stock right now, whereas the sector average is closer to 27x earnings, still a very high valuation.

My target is to find a stock that is at or below the sector average on price-to-earnings, so somewhere below 26.00. In this case, I do not recommend this stock on the basis of P/E ratio. I welcome your feedback in the comments section on why you think this sector’s average is priced at almost 27X earnings and whether you think this is justified or not?

Accenture – P/E ratio (Seeking Alpha)

Further, the other metric I look at is the price relative to book value, and with a P/E of 8.00 it not only earned a grade of “D+” from Seeking Alpha but is almost 74% above the sector median of 4.60. I like it at a 3x or 4x price to book at most, keeping it below average. However, I cannot justify an 8x price to book on this stock for my readers, so it is not recommended.

Accenture – P/B ratio (Seeking Alpha)

Dividend Yield: Not Recommended

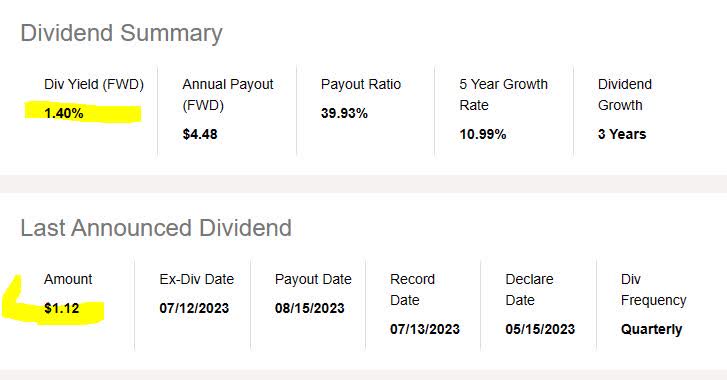

This is one of those stocks that does not get a lot of attention with a dividend yield of just 1.40%, considering that I recently covered bank & insurance stocks with yields above 5%.

Accenture – dividend yield (Seeking Alpha)

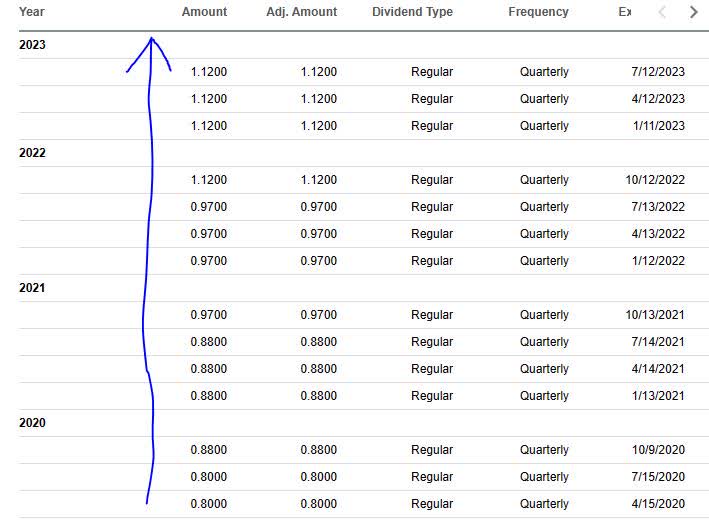

However, a positive to mention is that it is a reliable payer of quarterly dividends, and the history shows it. Since 2020, payments were regular and have increased as well. This is a good sign for dividend investors, that the company has the capacity to return capital back to shareholders each quarter.

Accenture – dividend history (Seeking Alpha)

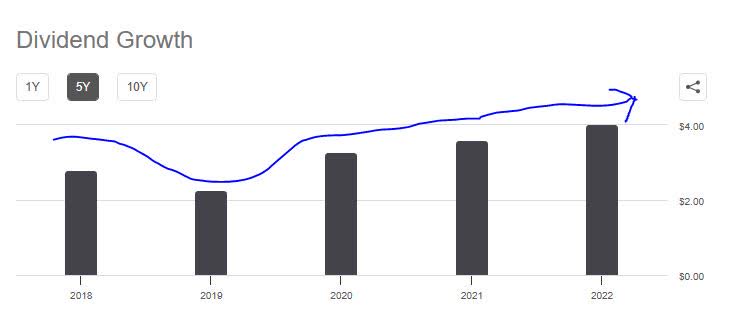

Additionally, another positive note is the 5-year dividend growth rate which has risen, despite a dip in 2019. Since then, it has been on an uptrend.

Accenture – 5 year dividend growth (Seeking Alpha)

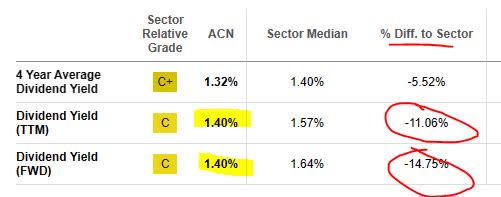

Now, for more disappointment, both the trailing and forward dividend yields for this stock are over 10% below the sector average, and that sector average is not that high to begin with. I like it at somewhere above 10% vs sector average at least, so for this stock I am looking for a yield of 1.80% and above.

Accenture – dividend yield vs sector average (Seeking Alpha)

Based on the data, I do not recommend this stock for dividend investors. Consider some alternatives like fellow managed solutions provider Cognizant (CTSH) who offers a yield of 1.76%, which appears to be almost 8% above sector average.

Net Income Growth: Recommend

This company has impressively shown a positive net income growth trend YoY, and the data shows it. Consider the income statement below, showing YoY increases in both net income and earnings per share:

Accenture – net income and EPS YoY growth (Seeking Alpha)

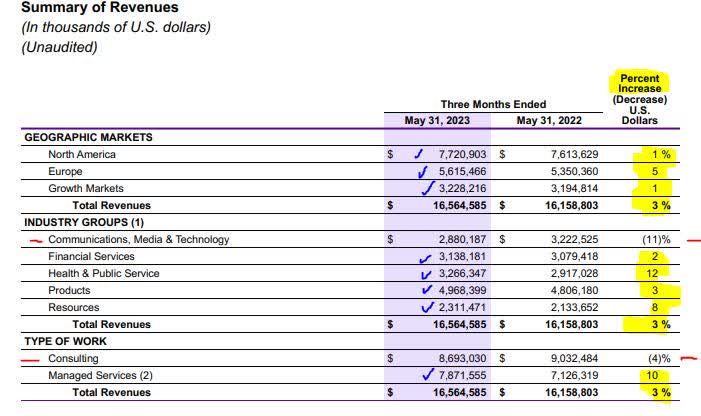

Now, I want to drill further into revenue growth drivers by region and business segment, to help me better understand what is driving this business forward from a top-line view.

From the exhibit below, one can see that the business has geographic diversification, and its three markets all saw YoY revenue growth. It’s also diversified across multiple industry groups, and all except one saw YoY revenue growth. Although its consulting practice saw a 4% drop YoY, its managed services segment grew.

Accenture – revenue growth (Accenture – Q3 exhibit)

These are all positive tailwinds for this stock, but notably to mention in this specific industry is the concept of “bookings”, or forward-looking value of contracts signed with clients. I think this firm will continue to dominate in the managed services space.

According to their earnings release, “managed services new bookings were $8.32B, or 48% of total new bookings.”

I expect continued growth in net income in the next earnings call, so I would certainly recommend this stock in this category.

Capital & Liquidity: Recommend

When talking about this category, I want to see a company that is capable of returning capital back to shareholders.

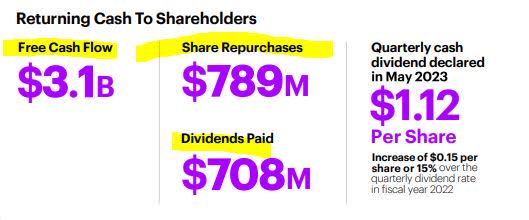

From their most recent quarterly infographic, for what was their fiscal quarter Q3, you can see that this company boasts of $3.1B in free cashflow, $789MM in shares repurchased, and $708MM paid out in dividends:

Accenture – return to shareholders (Accenture – quarterly infographic)

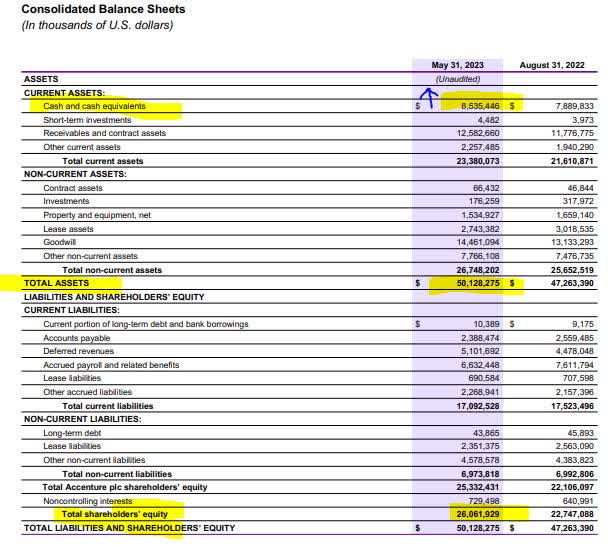

Further, let’s take a closer look at the balance sheet, which shows this being a cash-rich company. We are talking about $8.5B in cash & equivalents, along with total assets of $50.1B, total liabilities of around $24B, and positive equity of $20B, after the most recent fiscal quarter. Interestingly, they saw a YoY increase in cash, too.

Accenture – balance sheet (Accenture – FYQ3 release)

As CEO Julie Sweet commented during the earnings release, the result “demonstrates the rigor and discipline with which we run our business.”

With that said, I certainly would recommend this company in the category of capital and liquidity, as the data backs it up.

Stock Price vs 200 Day SMA: Not Recommended

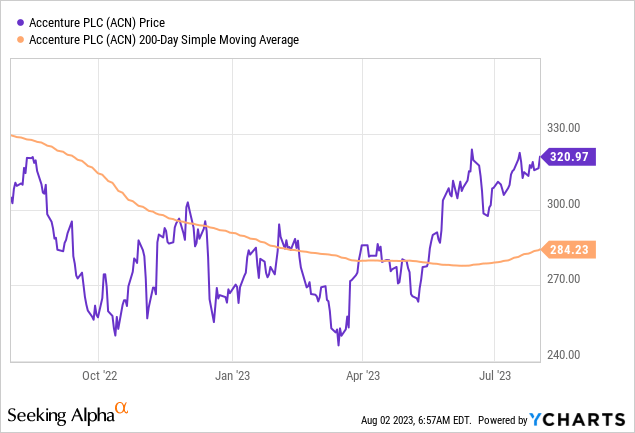

As of the writing of this article, before market open on Wednesday August 2nd, shares were at $320.97, per the yChart below.

The question is what price range would I consider this to be a value buy at?

To answer that, and for simplicity, I created an investment “idea” where I simply track the 200-day simple moving average “SMA” as a long-term trend indicator, and I trade within a range of 5% above or below that average.

If you look at the chart above, it follows the 200-day SMA over the last year. If the 200-day SMA is $284.23, my ideal trading range to buy at is $270.01 – $298.44, staying within that 5% buffer. If I buy at $298, I am expecting the bullish momentum to continue, if I buy at $270, I expect the price to break through the upper resistance of the 200-day SMA and continue beyond that.

Currently though, the share price of $320.97 is almost 13% above the 200-day average, which I think puts it into overbought territory, hence making it a better “sell” opportunity for those that can earn a capital gain and redeploy capital elsewhere.

To illustrate my investing idea, I created the following table:

Accenture – portfolio simulator (Albert Anthony & Co)

In this simulated investing idea above, I bought 100 shares at my target buy price of $270.01, held for 1 year to earn the full year dividend income, and sell it at my sell target of $298.44. With a capital gain and dividend income, my total return on capital invested would be 12.19%.

A risk to this investing idea is that the moving average does not go in a favorable direction after I buy the shares, and in 1 years it is much lower than is currently, which would cause a significant unrealized capital loss on this portfolio. This would require holding the shares even longer then, perhaps 2 or 3 years even. In my experience, long-term investors must be ready for periods of unrealized losses as well.

Ratings Score: Sell

As this stock won just 2 of my 5 ratings categories, I am rating it a Sell today, which is more bearish than the consensus ratings from Seeking Alpha and Wall Street, as shown below:

Accenture – ratings consensus (Seeking Alpha)

However, I want to reiterate that a sell rating is not a negative necessarily, but could be an opportunity to achieve a capital gain for those holding the stock from a much lower price point they got in at. On the buy-side, however, it doesn’t seem like a value buy right now for taking a new position in this stock.

If you look at the yChart again, if someone happened to get in during the March dip into the $250 price range, and sells it now, that’s a $70 per share profit, or a 28% return.

Risks to my Outlook: Artificial Intelligence

A risk to my bearish outlook on this stock would be bullish sentiment among investors and other analysts that are convinced the artificial intelligence space will be a growth bonanza for this company now and going forward. This growth driver of new business could make my outlook on this stock seem overly cautious.

This was highlighted by another SA analyst, Hunter Wolf, who gave this stock a strong buy rating in his June article,

the adoption of AI will further accelerate cloud migration, benefiting Accenture. Taking lessons from their successful foray into cloud services, Accenture is making investments to establish an early lead and position themselves for the opportunities that lie ahead.

All of that is a great point, however I would also mention that Accenture is one of many large players chasing the “AI” realm that clients are trying to get a grip on. In fact, a July 2023 article in US News & World Report highlighted the 10 best “AI” stocks to buy according to Bank of America (BAC), and Accenture was not on that list.

Some well-knowns were, however, and they include Microsoft (MSFT), Meta (META), and SAP (SAP), to name a few.

For instance, the article goes on to say the following about SAP:

SAP is well positioned for the “AI” era given demand for “AI” models for analyzing internal accounting, finance, human resources, supply chain and industrial process data. SAP is an “AI” leader among software-as-a-service companies.

In my opinion, although Accenture has a role to play in the artificial intelligence revolution, and has done so, it is essentially a managed solutions provider and can be benched when needed and called upon off the bench when needed, like most MSPs. It is not the only game in town when it comes to “AI”, so I am not convinced that this by itself would justify buying shares at the current price, although perhaps after a price correction and better valuation.

Analysis Wrap Up

Today’s analysis covered the following key points:

This stock got a sell rating today, which is more bearish than the consensus from Seeking Alpha and Wall Street.

Positives: YoY net income growth, capital & liquidity situation.

Headwinds: share price vs moving average, valuation vs sector avg, dividend yield vs sector avg.

A risk to my sell outlook was addressed, and that is investor bullishness on this company as an “AI” leader.

As I have shown, this is a global leader among managed services providers, has a massive client list, penetration of multiple industries, and competing in the “AI” game too. However, at the current price I think it is overpriced and could be a sell opportunity for a nice capital gain, redeploying some of that capital elsewhere.

I expect, based on this stock having beat three of the last 4 earnings estimates, that the next one is a high likelihood of beating by between $0.03 and $0.10.

This may drive a short-term bullish spike in the price, but as more investors realize it is too overvalued I think that price should pull back reasonably, closer to the 200-day SMA, presenting a better buying opportunity then as well as a better dividend yield.

Accenture – earnings beats (Seeking Alpha)

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.