Summary:

- ADBE remains the market leader in Application Development and Graphic SaaS markets, as observed in its ability to increasingly monetize existing users and grow new adoptions.

- The management’s lower than expected FY2025 guidance may be attributed to a sandbagging strategy, as observed in the top/ bottom-line beats over eight consecutive quarters.

- While the aggressive share repurchases may have impacted its balance sheet health, ADBE remains profitable enough to do so, with it also directly being accretive to its adj EPS growth.

- For now, its overly discounted valuations continue to offer opportunistic investors with a rich upside potential, despite the maturing growth profile.

- Combined with the bounce observed from the November 2024 support levels of $470s and the robust uptrend support from the September 2022 bottom, ADBE looks compelling indeed.

Deagreez/iStock via Getty Images

ADBE Is Inherently Undervalued – Offering Opportunistic Investors With A Rich Upside Potential

We previously covered Adobe (NASDAQ:ADBE) (NEOE:ADBE:CA) in September 2024, discussing the market’s skepticism surrounding its double beat FQ3’24 performance and robust FY2024 guidance, as the stock returned most of its Q3’24 price gains.

Despite the deteriorating balance sheet, there was no denying the SaaS company’s high growth trend, as observed in the growing ARR/ multi-year backlog and increasingly richer gross profit margins, resulting in our reiterated Buy rating then.

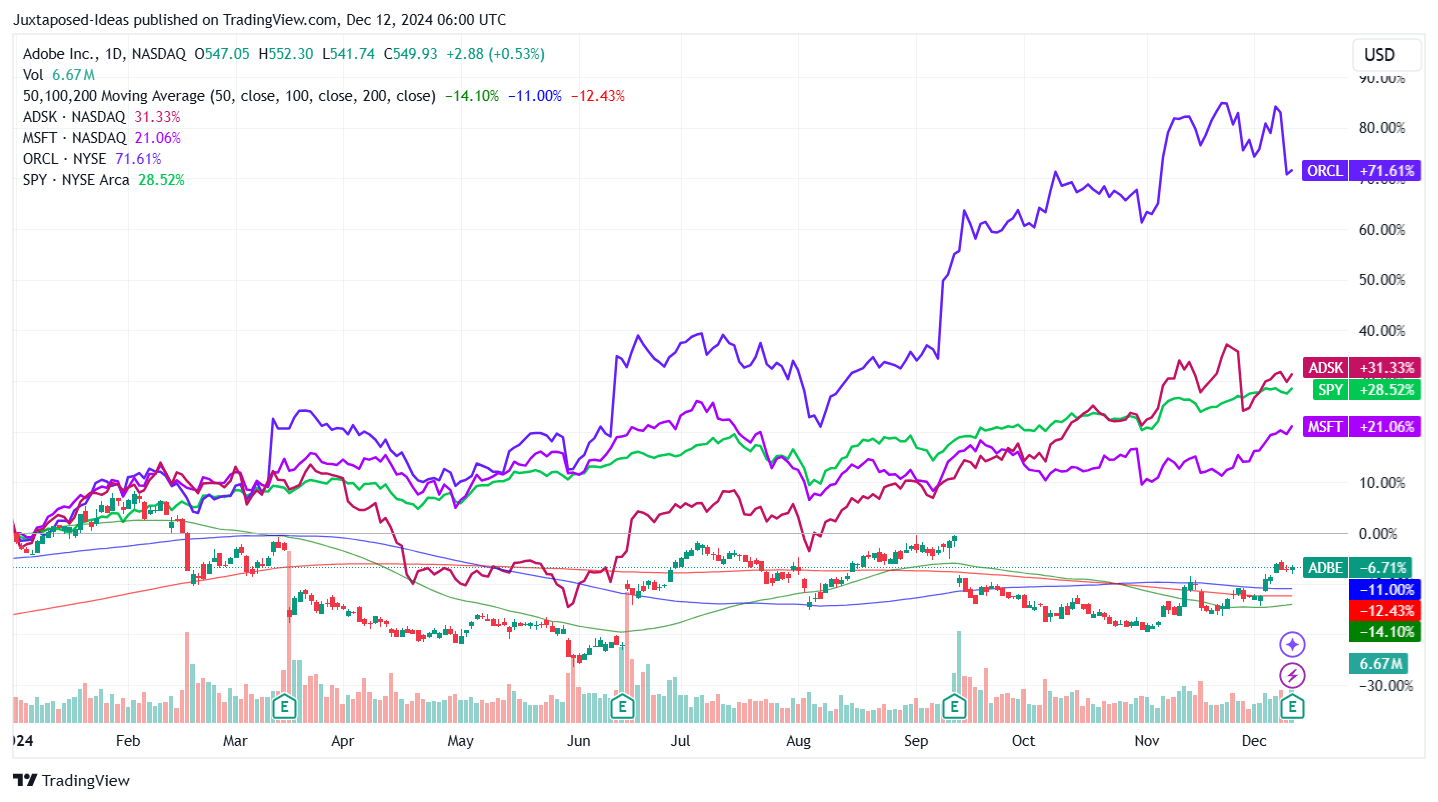

ADBE YTD Stock Price

Trading View

Since then, ADBE has further retraced by -9% at its worst, before recovering to retest the next resistance levels of $560s, with its unloved status naturally triggering its underperformance compared to the wider market and the enterprise SaaS peer group.

The market’s pessimism surrounding its prospects are surprising indeed, given that ADBE remains the undisputed leader in the Application Development category with 58.92% in market share and the Business Process Management (Graphics) Software with 42% in market share.

Given its market leadership, it is unsurprising that the SaaS company continues to lead the mindshare in the market, as observed in the consistently growing multi-year Remaining Performance Obligations [RPO] of $19.96B (+10% QoQ/ +15.9% YoY).

At the same time, ADBE has also been able to expand its monetization opportunity and profit margins as they grow in operating scale, as observed in the richer gross profit margins of 89% in FY2024 (+1.2 points YoY/ +4.2 from FY2019 levels) and adj net income margins of 38.4% (+0.4 points YoY/ +3.9 from FY2019 levels).

These three very important metrics continue to underscore why the market has been overly critical about the SaaS market’s prospects.

This is especially since ADBE’s native integration of Adobe Firefly on its flagship applications has been highly successful, with 16B of cumulative generations by the latest quarter (+4B QoQ/ +11.5B YoY), thanks to the multi-modal AI abilities across imaging, vector, design, and video.

This is on top of Document Cloud’s sequential doubling in AI Assistant conversations and growing users at 650M (+25% YoY), with it underscoring why its well-diversified offerings have been increasingly adopted by designers/ students and advertising/ marketing agencies, along with enterprises and federal governments.

If anything, ADBE’s freemium approach has also delivered robust results, partly aided by the strategic partnerships with numerous partners including, ChatGPT, Google (GOOG), Slack (CRM), Wix (WIX), Box, Hubspot, and Webflow.

Combined with the SaaS company’s choice to proceed with an ethical Firefly platform (and naturally, commercially safe creative content), it is unsurprising that these efforts have triggered the growing user adoption, improved monetization, and RPO expansion.

Most importantly, ADBE has hinted at higher ARPUs ahead, attributed to the “new higher priced Firefly offering that includes our video models as a comprehensive AI solution for creative professionals” along with the “accelerating the adoption of freemium offers,” with it likely to be top/ bottom-line accretive in the intermediate term.

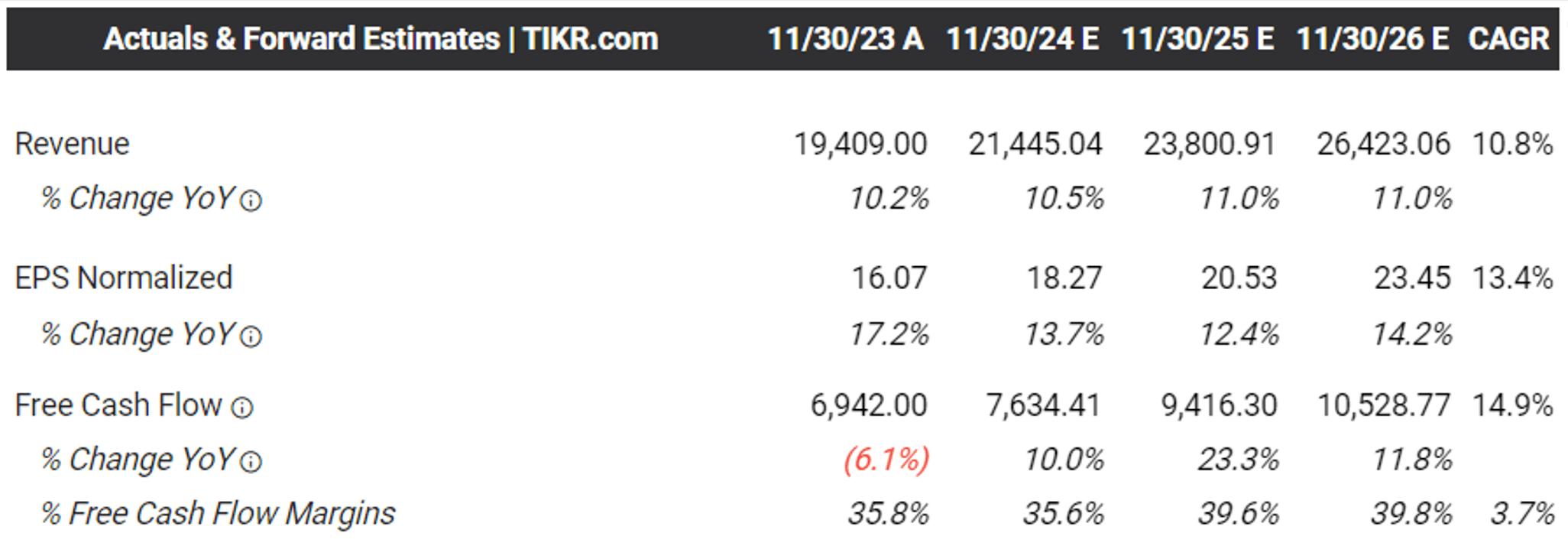

The Consensus Forward Estimates

Tikr Terminal

On the other hand, ADBE’s decelerating growth can not be denied indeed, as observed in the FY2024 revenue growth by +10.8% YoY/ adj EPS growth by +14.6% YoY and the management’s FY2025 guidance at +8.9% YoY/ +10.4% YoY, respectively.

This is compared to the 10Y historical growth rate at +17.2%/ +28.6%, with it signaling the SaaS company’s maturing growth profile, as observed in the consensus forward estimates through FY2026 above.

Despite the rich FY2024 operating cash flow at $8.06B (+10.4% YoY), ADBE’s balance sheet continues to deteriorate to a net cash position of $2.27B (-46% YoY) as well, partly attributed to the intensified share repurchase cadence at $9.55B over the LTM (+117% YoY).

On the other hand, we believe that investors may more than welcome the aggressive share repurchases compared to the overpriced (and now abandoned) Figma acquisition worth $20B, given the former’s accretive impact on its adj EPS calculation.

If anything, the consensus continues to estimate expanding Free Cash Flow generation and richer margins ahead, allowing the management to sustain their rich shareholder returns.

At the same time, readers must note that ADBE management has a habit of sandbagging their forward guidance, as observed in the consistent top/ bottom-line beats over the past eight consecutive quarters.

At the same time, the SaaS company is only experiencing a similar issue as that of large, mature enterprises, with the law of large numbers catching up to its growth profile, given the robust performance metrics discussed above.

It is undeniable that high double digit growth rates are “difficult to maintain as a business expands,” especially given that its undisputed market leadership, with any incremental share gains likely to be exponentially harder.

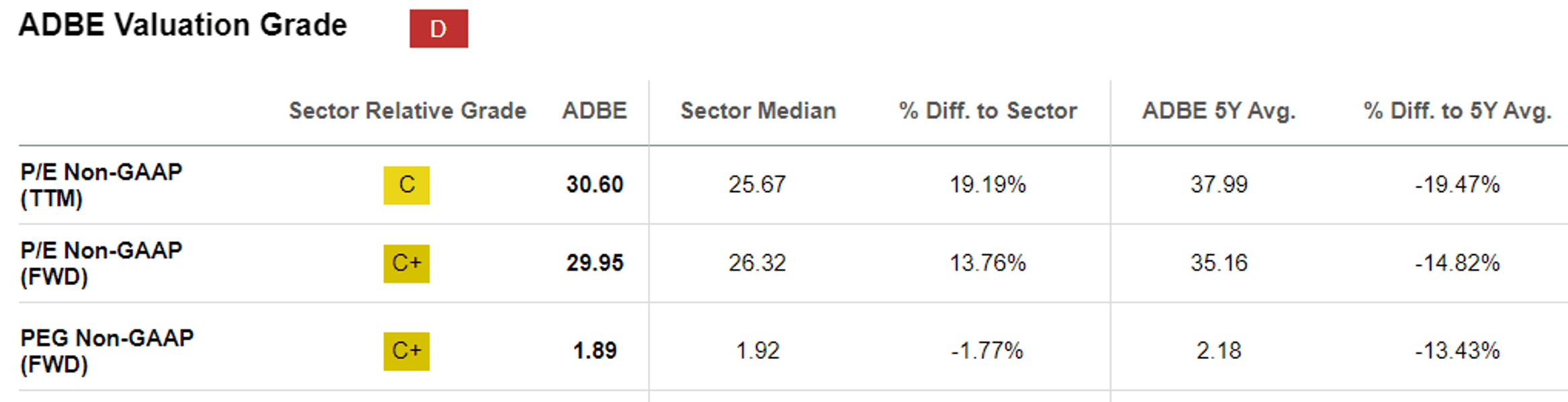

ADBE Valuations

Seeking Alpha

These are also the reasons why we believe that ADBE does not deserve to be discounted to FWD P/E non-GAAP valuations of 29.95x, compared to its 5Y mean of 35.16x and 10Y mean of 33.07x.

The same has been observed in its relatively cheap FWD PEG non-GAAP ratio of 1.89x compared to its 5Y mean of 2.18x and the sector median of 1.92x, despite the notable upgrade from the 10Y mean of 1.15x.

Even when compared to its mature enterprise SaaS market leaders, such as Microsoft (MSFT) at 2.56x, Oracle (ORCL) at 2.57x, and Autodesk (ADSK) at 1.85x, we believe that ADBE remains a compelling Buy here, despite the maturing growth profile over the next few years.

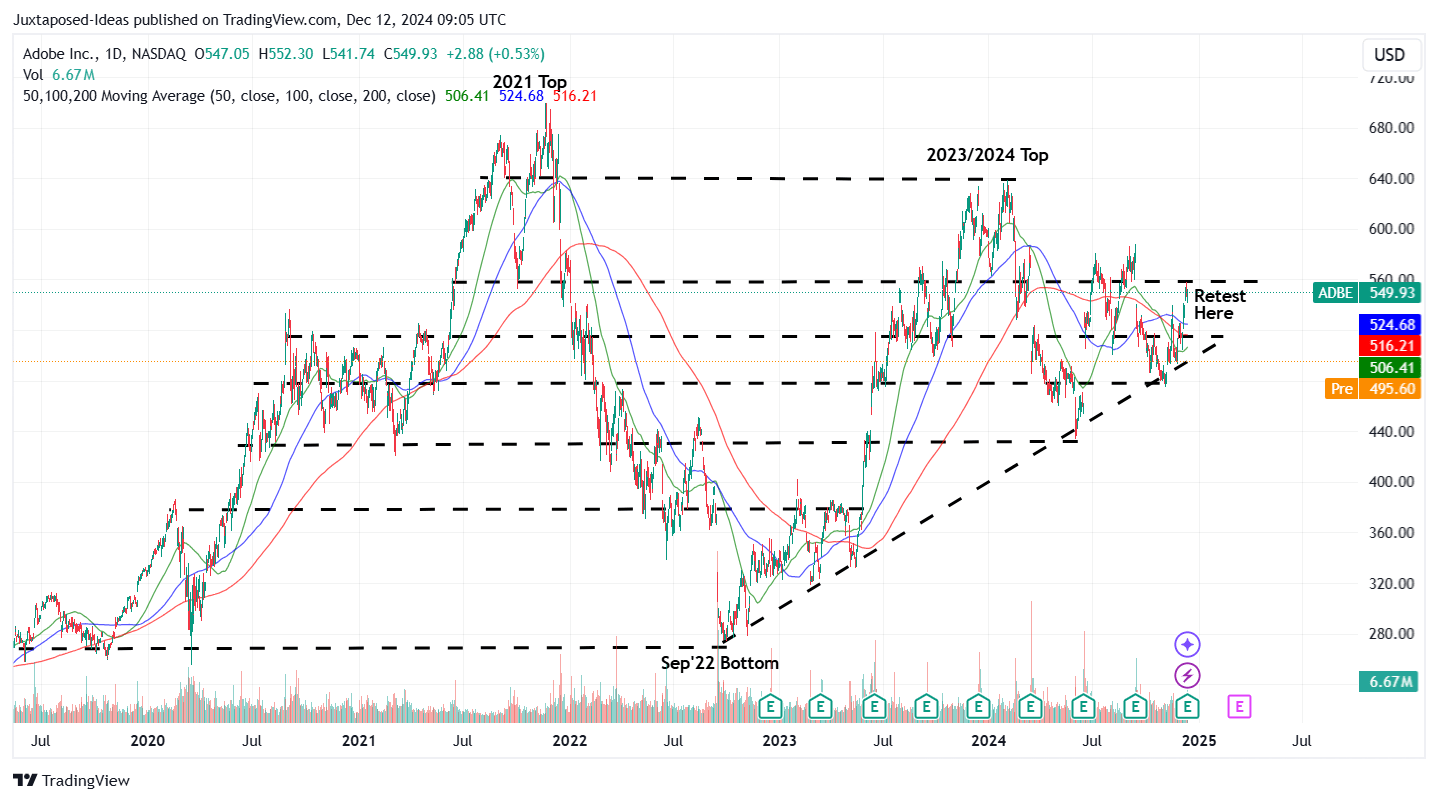

So, Is ADBE Stock A Buy, Sell, or Hold?

ADBE 5Y Stock Price

Trading View

For now, it is apparent that ADBE has had a volatile YTD stock price performance, as the market remains unconvinced about its AI monetization opportunity along with its decelerating growth profile.

For context, we had offered a fair value estimate of $514.70 in our last article, based on the management’s FY2024 adj EPS guidance of $18.26 and the 1Y P/E mean of 28.19x.

Based on the management’s FY2025 adj EPS guidance of $20.35, it is apparent that ADBE is trading attractively below our updated fair value estimates of $573.60.

Based on the consensus FY2026 adj EPS estimates of $23.45, there remains an excellent upside potential of +20.1% to our base-case long-term price target of $661.00. If not higher at +40.7%/ $773.80, respectively, assuming an upward re-rating in its FWD P/E valuations nearer to its 10Y mean of 33x.

This is on top of its robust shareholder returns, with -3.4% of its shares already retired over the LTM and -8.2% since FY2019 while boosting its adj EPS growth as well.

Combined with the bounce observed from the November 2024 support levels of $470s and the robust uptrend support from the September 2022 bottom, we are reiterating our Buy rating for the ADBE stock.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.