Summary:

- Affirm Holdings disappointed due to central bank delaying rate cut timeline.

- Affirm Card adoption and gross merchandise volume trends show healthy growth.

- Affirm Holdings is undervalued with potential for re-rating and long-term growth.

B4LLS

Being a bet on falling interest rates, Affirm Holdings, Inc. (NASDAQ:AFRM) has most recently disappointed expectations.

The central bank’s decision to delay the rate cut timeline also set back my investment thesis with regard to the buy now, pay later company a little bit, but I think the value proposition, for long-term investors anyways, has improved here lately.

I say this because Affirm Card adoption metrics and gross merchandise volume trends look healthy and the BNPL market opportunity remains as attractive as ever.

Though the fintech’s stock is in a holding pattern, the fintech itself is nonetheless primed for long-term growth.

My Rating History

My previous stock classification of Buy about Affirm Holdings was driven by the fintech’s partnership with eCommerce giant Amazon.com, Inc. (AMZN). Despite a QoQ drop in gross merchandise volume in 1Q24, Affirm Holdings is seeing robust growth across its most important platform metrics.

The central bank just delayed its rate cut timeline, which may postpone profit tailwinds for this particular fintech. However, with growth of BNPL services to continue, I think Affirm Holdings is a compelling, long-term growth story to capitalize on.

GMV Growth And Long-Term BNPL Market Opportunity

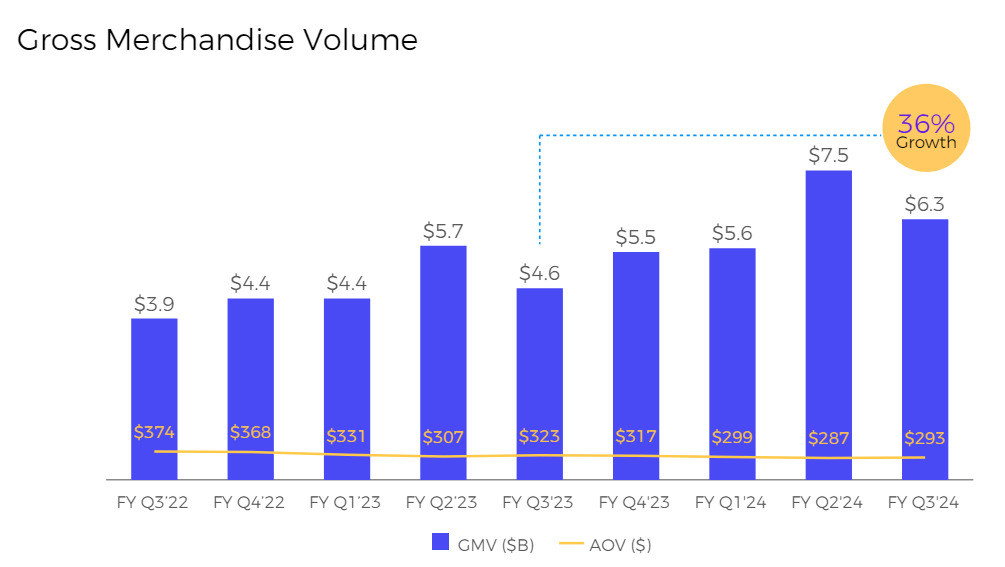

One platform metric that is important for fintechs is gross merchandise volume, which is the total amount of merchandise, expressed in dollars, that is sold through a particular website or platform.

Affirm Holdings’ gross merchandise value was up 36% in 1Q24 to $6.3 billion, and this growth was achieved despite a cyclically-driven decline in sales that typically happens after the 4Q holiday quarter. This growth in gross merchandise volumes led to a 51% jump in sales in 1Q24.

Gross Merchandise Volume (Affirm Holdings)

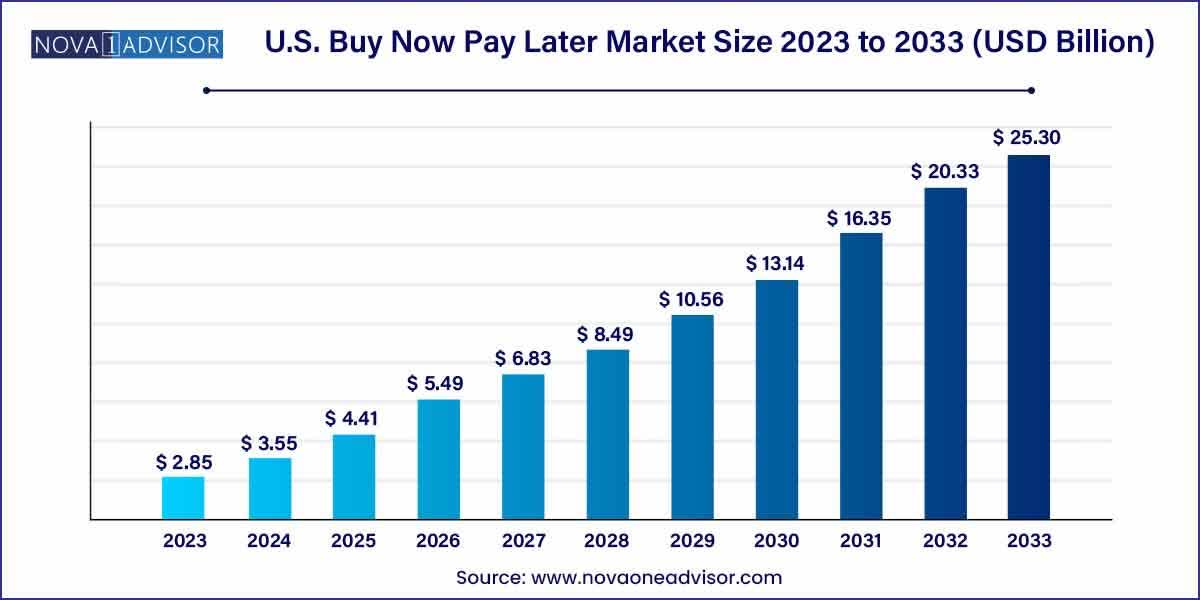

The BNPL market is primed for sustained expansion, due to growth of eCommerce transactions as well as growing adoption of buy now, pay later products like the one Affirm Holdings is offering its customers.

The U.S. market for buy now, pay later products is anticipated to grow steadily over the next decade and reach a market value of $25.3 billion by the end of 2033. This trajectory reflects a 24% per annum growth rate which is poised to profit Affirm Holdings as well.

U.S. Buy Now Pay Later Market Size (Novaoneadvisor)

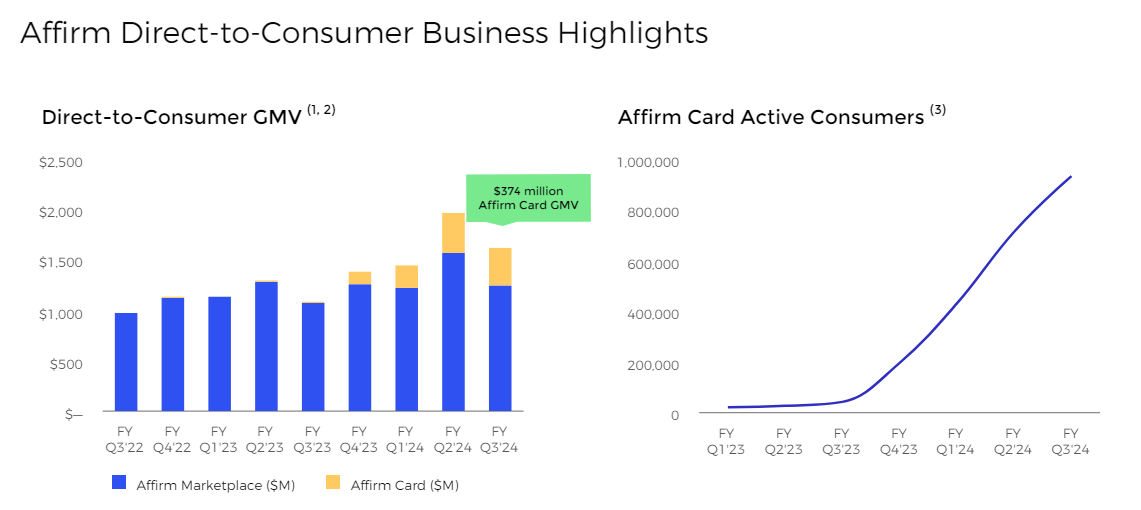

In addition to a growing market and ongoing momentum in gross merchandise volume, Affirm Holdings is having quite a lot of success with its Affirm Card. This card functions as a debit card that it connected to the Affirm app and allows customers to pay for products and services either instantly or over time.

The attractiveness of the Affirm Card is that customers don’t pay interest or fees, which makes it a viable alternative to other card offers, particularly those from credit card companies.

The number of Affirm Card customers has surged since the product was debuted two years ago, and the user count for the Affirm Card is on track to exceed the 1 million mark in the short term.

Affirm Card momentum and growth in GMV are prime reasons why I think that the fintech has re-rating upside in the long-run.

Affirm Direct-To-Consumer Business Highlights (Affirm Holdings)

Sub-Optimal Profit Situation Could Be Resolved During The Next Down-Cycle In Rates

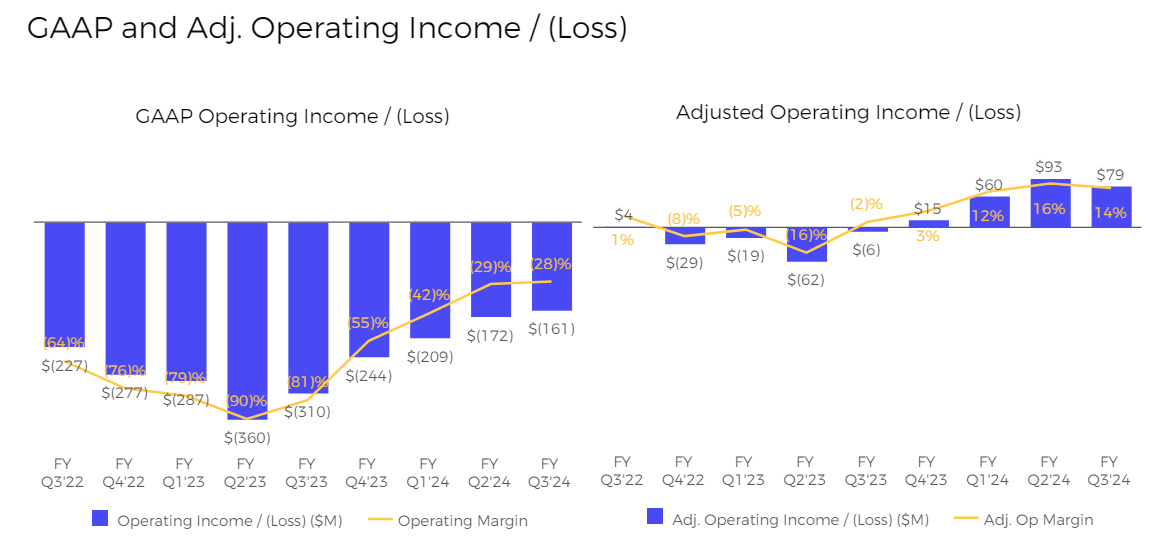

A big problem for Affirm Holdings, that in my view has so far prevented a re-rating to the upside, is that the fintech is not profitable and struggling with high costs. The company has implemented stringent cost cuts during the last up-cycle in interest rates, but is still falling short in the profitability department.

In the last quarter, Affirm Holdings produced $79 million in operating income, but only on an adjusted basis. On a GAAP basis, the fintech is still facing a steep uphill climb.

With that said, though, if the profit situation on a GAAP basis were to improve, then Affirm Holdings could be rewarded for achieving a critical inflection point.

GAAP And Adjusted Operating Income (Affirm Holdings)

Affirm Holdings Is A Steal

While 2023 was a transition year for Affirm Holdings amid an aggressive central bank drive to raise short-term interest rates, 2024 is a rebound year for the fintech and sales projections as well as 1Q24 sales momentum look healthy.

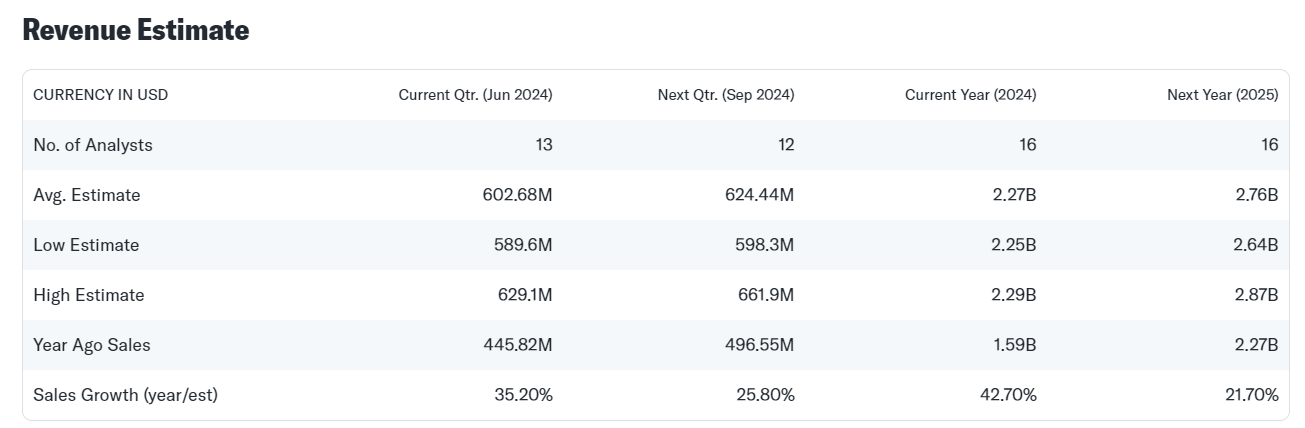

The market models sales of $2.76 billion for Affirm Holdings next year, which reflects a YoY growth rate of 21.7%. This would be about half the growth rate this year, but with the central bank delaying rate cuts, I think the real tailwinds for Affirm Holdings’ credit-dependent business could be reaped next year.

Be that as it may, Affirm Holdings is presently selling for a sales multiple of only 3.4x. Upstart Holdings, Inc. (UPST), an AI-driven lending startup is selling for 2.8x 2024 sales and SoFi Technologies, Inc. (SOFI) which has a 2.4x sales multiple.

At the start of the year, the fintech had a market value of $15 billion, which implied a sales multiple of 5.6x (implied intrinsic value of $50). In the long-run, this is an estimate I think Affirm Holdings could re-rate to, but probably only if the company managed to turn its profit situation around and the central bank started to cut rates, which would help grow demand for BNPL loans.

Revenue Estimate (Yahoo Finance)

Why The Investment Thesis Might Disappoint

Obviously, the wild card here is once again the central bank. Fed chairman Jerome Powell last week said that the central bank was essentially letting go of its original plan to cut short-term interest rates three times this year and guided for a mere single rate decrease in 2024.

Unfortunately, for rate-dependent fintechs like Affirm Holdings, this is bad news as it delays potential catalysts for consumer spending.

Buy now, pay later loans, like all other forms of personal loans, are more attractive for consumers in a low-rate environment and with the central bank delaying its rate cut timeline this month, there is a risk that Affirm Holdings will remain stuck in its present holding pattern.

My Conclusion

Affirm Holdings suffered a setback in June as the central bank pushed out its rate cut timeline, which prevents a catalyst for its business to be realized, but probably only temporarily.

With that being said, though, even without rate cuts, the fintech is profiting from handsome growth in gross merchandise volume (up 36% YoY in 1Q24), Affirm Card growth is solid and the buy now, pay later market opportunity is not getting any less attractive just because the central bank is choosing a cautious approach when it comes to slashing interest rates.

Finally, I think that the valuation multiple leaves room for decompression, particularly in light of the 20% plus sales growth rate that is anticipated for next year.

If Affirm Holdings gets its profitability situation under control and reports positive GAAP operating income, I think the growth story has a lot of upside for investors.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AFRM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.