Summary:

- AGNC Investment Corp. focuses on Agency MBS and offers high dividend yields, making it attractive for income-seeking investors.

- Preferred stocks of AGNC, especially AGNCP, present undervalued opportunities compared to their floating-rate counterparts like AGNCM.

- Using swap rates and future cash flows in a method of evaluation proven in the past, AGNCP is identified as a better investment relative to AGNCM.

- Sophisticated investors should consider relative valuation and future cash flows, not just current yield, to find undervalued securities.

wildpixel

Co-authored by Relative Value

Overview

Mortgage REITs (mREITs) use private capital to invest in residential and commercial mortgages, mortgage-backed securities (MBS), and related assets, and in this way provide essential liquidity for the real estate market. The general idea of the mREITs is to generate revenue on the spread between the interest on the mortgages/MBS they invest in and the cost of the equity and debt they finance with. They are structured in such a way to leverage the long-term yield of their underlying securities. By law and IRS regulations, REITs have to distribute at least 90% of their taxable profits in the form of dividends to their shareholders. As a direct result, these types of companies offer high distribution yields that attract a lot of income-seeking investors.

With this short article, we want to draw your attention to AGNC Investment Corp. (NASDAQ:AGNC) – an mREIT that focuses its business on buying agency MBS – and, more importantly, its preferred stocks. We will do the math and pinpoint the mispriced one among these exchange-traded securities. As a general rule, the mREIT-issued fixed-income financial products receive a lot less attention than the common stocks. This sometimes creates mispricings and hidden opportunities to profit for anyone ready to do a little bit of digging.

Investing in every company bears some risks and in the case of mREITs, we can summarize them to interest, credit, prepayment, and rollover. As shareholders, we should believe that a corporation is doing everything within its power to mitigate these risks, or we simply stay away from it. What is within the power of the investors is to diversify the positions taken in a company they already like. An important aspect that should never be forgotten is that preferred stocks stay higher than the common ones in the capital structure of the companies and thus provide a safer exposure to the business. Moreover, the companies need to pay their preferred stock dividends before they can make common stock distributions.

The company

AGNC is a leading internally managed mortgage REIT that invests predominantly in Agency residential mortgage-backed securities (Agency MBS) guaranteed by a U.S. Government-sponsored enterprise (GSE), such as Fannie Mae and Freddie Mac, or a U.S. Government agency, such as Ginnie Mae, on a leveraged basis. We may also invest in other types of mortgage and mortgage-related securities, such as credit risk transfer securities (CRT), non-Agency residential and commercial MBS, and other assets related to the housing, mortgage, or real estate markets that are not guaranteed by a GSE or U.S. Government agency.

As a leading provider of private capital to the U.S. housing market, we enhance liquidity in the residential real estate mortgage markets and, in turn, facilitate homeownership in the U.S. Our principal objective is to generate favorable long-term stockholder returns on a risk-adjusted basis with a substantial dividend yield component. We generate income from the interest earned on our investments, net of associated borrowing and hedging costs, and net realized gains and losses on our investment and hedging activities. We fund our investments primarily through collateralized borrowings structured as repurchase agreements, which typically offer highly attractive financing rates due to the high investment quality of our Agency MBS assets.

Source: Company’s website

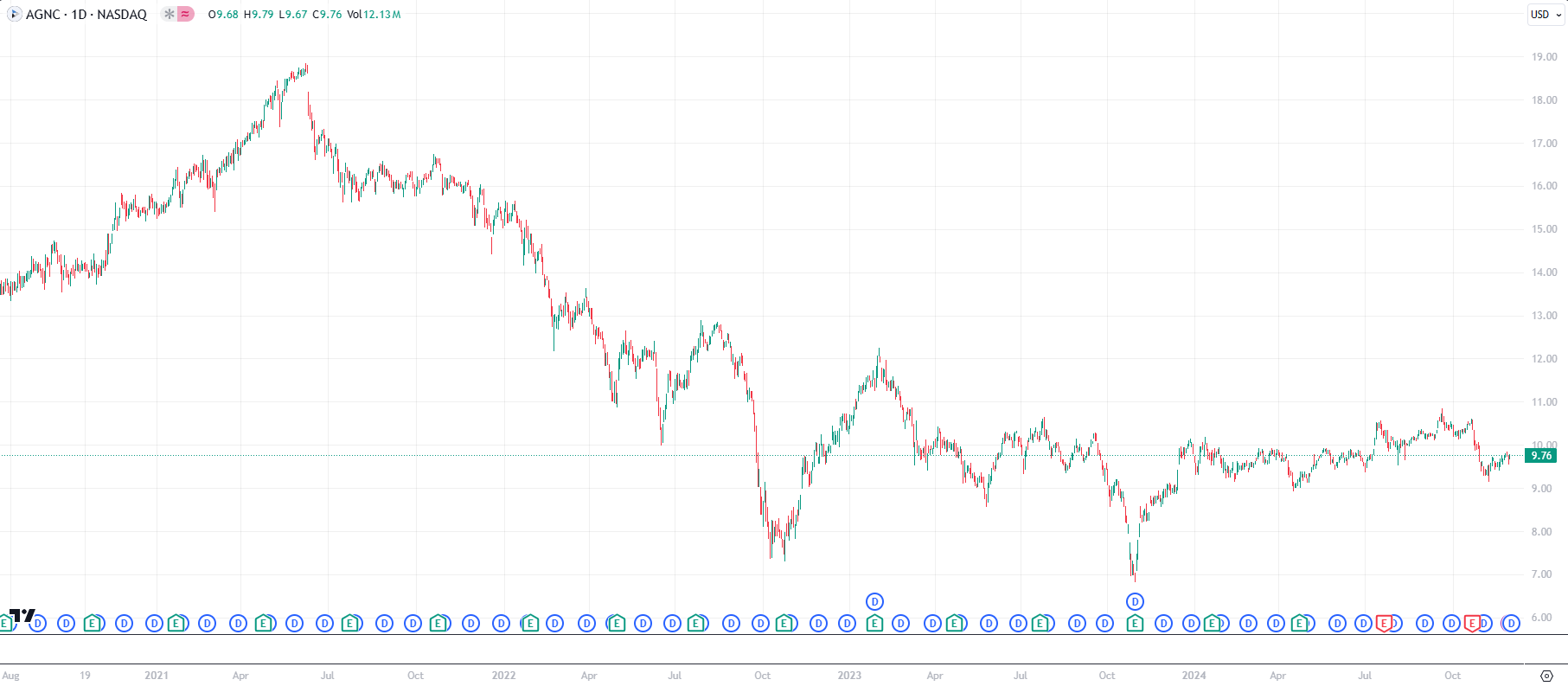

Below, you can see a daily price chart of the common stock, AGNC:

AGNC common stock price (TradingView)

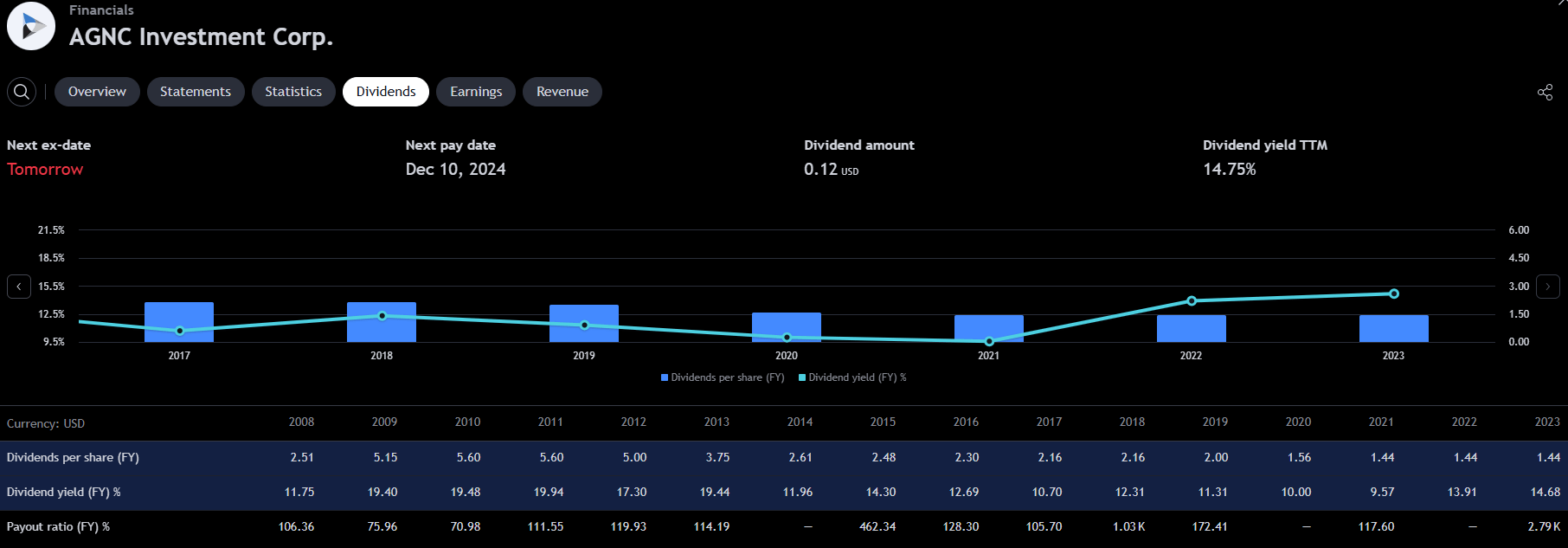

For the past couple of years, the company has been paying a steady yearly dividend of $1.44 in the form of monthly distributions of $0.12. The last dividend cut AGNC did was in April 2020 after the Covid crisis. The graph below shows the earlier yearly distributions of the company.

AGNC common stock dividends (TradingView)

With a current price of $9.76 for the common stock, the dividend yield calculates to be 14.75%. As an absolute value, the company is paying around $1.13 billion in dividends a year. For comparison, the dividend expenses for all the outstanding AGNC preferred stocks for the past four quarters is around $125 million.

In addition, AGNC has a market capitalization of around $8.64B and is the second-largest mortgage REIT, only lagging behind Annaly Capital Management, Inc. (NLY).

Mortgage REITs by market cap (stockanalysis.com)

AGNC preferred stocks

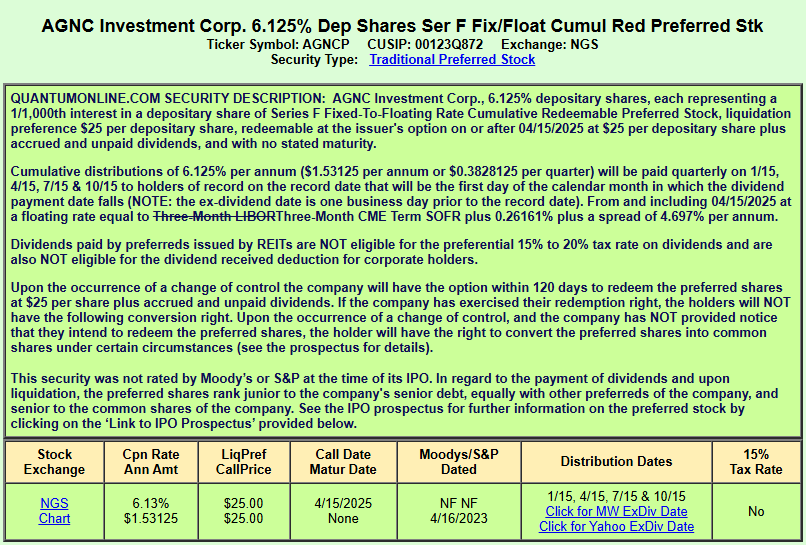

The main accent of this short article will be the 3-month SOFR-based fixed-to-floating exchange-traded preferred stocks of AGNC. These four securities are created similarly – after IPO they trade for five years with fixed yearly coupons and at their corresponding call date their distribution becomes tied with a spread to the 3-month LIBOR (3-month SOFR after the transition in 2023).

AGNCP details (quantumonline.com)

At the moment of writing the article, three of these preferred stocks are trading with floating rates past their call dates – AGNCM, AGNCN, and NASDAQ:AGNCO. NASDAQ:AGNCP is the last one that is still trading with a fixed distribution until its call date on 4/15/2025. All the important metrics of the four securities are shown in the table below. As the issues are pretty similar, from the same company, we can compare them effectively and try to find out whether there is an undervalued one on a relative basis.

AGNC SOFR-based preferreds metrics (proprietary software)

When comparing securities with floating interest rates, we choose to use swap rates. An interest rate swap is a derivative contract that typically trades over the counter and exchanges a floating interest rate payment for a fixed interest rate over a set period. One side of the contract is the payer, and the other is the receiver of the fixed rate. The swap rate represents the fixed-rate payment that the receiver requires from the payer in exchange for the uncertainty of having to pay the short-term floating rate. At the time the swap deal is undertaken, the total cash flows of the fixed-rate leg of the contract will be equal to the sum of the expected floating rate cash flows implied by the forward floating rate curve.

As all four preferred stocks we are studying today have perpetuities tied to SOFR, we are using the USD 30 Years Interest SOFR Swar Rate, which is 3.633% as of the moment the calculations are made. For each preferred stock, we exchange the SOFR rate with this swap rate when taking into account the future dividend flows after their corresponding call date.

SOFR SWAP rates (chathamfinancial.com)

To find the relative “fair” pricing of the preferred stocks to one another, we chose one of them – AGNCM as being fairly priced as it is at the moment. AGNCM is the security with the lowest float rate – 4.33% above the 3-month LIBOR, or 4.59% above the 3-month SOFR. The idea is to calculate where the last one to become a floating rate – AGNCP is “fairly” priced, considering its future cash flows if AGNCM – the lowest spread above SOFR trades at par. We will also do the calculations for AGNCN and AGNCO for completion. Using the swap rate, we determine the future cash flows for AGNCM until the last call date for the group – April 15, 2025, and the terminal value for the stock for all the payments made after that:

AGNC preferred stocks model parameters (authors spreadsheet)

For each of the preferred stocks, we determine the SWAP-adjusted coupon rate. It will be used in the following calculations of the future cash flows and the terminal value of every security.

AGNC preferred stocks SWAP adjusted rates (authors spreadsheet)

The internal rate of return we find for AGNCM is used as a discount factor for determining the present value of the rest of the preferred stocks in the set. Using the same technique for the future cash flows for each stock in the group, we calculate the preset value of every one of them:

Model calculations for AGNC preferred stocks (authors spreadsheet)

Thus, their present values represent “fair prices” with AGNCM set as a benchmark. It doesn’t matter which stock will be taken as a basis, as the calculations that follow only give us relative “fair” pricing to one another inside the group. Of course, the par price should also be taken into consideration when making this kind of assumption. The call clause is the obvious reason why AGNCN is not trading at $27.50, although we calculate its “fair” price to be some $2 above AGNCM’s.

The interesting preferred stock here is AGNCP. It is not a floating rate yet for the next couple of months but when taking into consideration its future cash flows with a discount factor the rate of return we calculated for AGNCM, it turns out to be a better investment. Our calculations show that should AGNCM be trading with a price pinned to par, then there is no reason for AGNCP not to do the same, as on a relative basis, it has more value.

A throwback to 2023

Evaluating the future cash flows and terminal value and calculating “fair” relative value for the LIBOR-based preferred stocks of AGNC and Annaly Capital Management, Inc. is something we did back in 2023. The purpose of our article back then was the same as the current one’s – to find the undervalued securities. In the table below are the prices of AGNC and NLY preferred stocks as of May 2023 with the price targets we calculated for them as “Fair Relative Price” using the same method as now in this current article.

2023 preferred stocks fair value calculations (authors spreadsheet)

Anyone interested can follow how the prices of undervalued ones back then appreciated in time. Our call from a year ago gives us additional confidence in the method we use of evaluating securities on a relative basis, using their future cash flows and the internal rate of a return of a “basis” issue as a discount factor.

Conclusion

In the search for undervalued securities with upside potential, the sophisticated investor has to always consider the whole relative valuation rather than only the current distribution yield. Observing only the high distributions without the context of the relative value can often deprive the investor of appealing opportunities to benefit from. Using a method of evaluation that proved to be right in last year’s analysis of the same products, for us, there is no doubt that AGNCP is undervalued to its already floating brother AGNCM.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AGNCP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Trade With Beta

At Trade With Beta, we also pay close attention to closed-end funds and are always keeping an eye on them for directional and arbitrage opportunities created by market price deviations. As you can guess, timing is crucial in these kinds of trades; therefore, you are welcome to join us for early access and the discussions accompanying these kinds of trades.