Summary:

- AGNC Investment faced challenges with hedge rolls and interest rate cuts, leading to negative economic returns in Q2-2024.

- Despite maintaining dividends, AGNC’s tangible book value loss outweighed returns, with a record amount of equity issued.

- We tell you why there are better choices than AGNC, even for those sticking with preferred shares.

Let Me Hit That Sell Button For You. BraunS/E+ via Getty Images

On our last coverage of AGNC Investment Corp. (NASDAQ:AGNC) we felt the company’s income would be stressed as hedges rolled off. We also thought the interest rate cuts would not materialize as quickly as the market was seeing, and that added another layer of caution.

We would expect this to ultimately weigh on AGNC as its spread income will be pressured as hedges run out. The REIT has also derived benefits from the MOVE index moving lower and the spread between MBS and Treasuries partially unwinding. At this point, risks are firmly to the downside. We maintain this at Hold and would consider moving to Sell over $10.00.

Source: The REIT Does What It Does Best In Q1 2024.

With the stock having released another set of results and having crossed our magical threshold, we decided to take another look.

AGNC Investment Q2 2024 Results

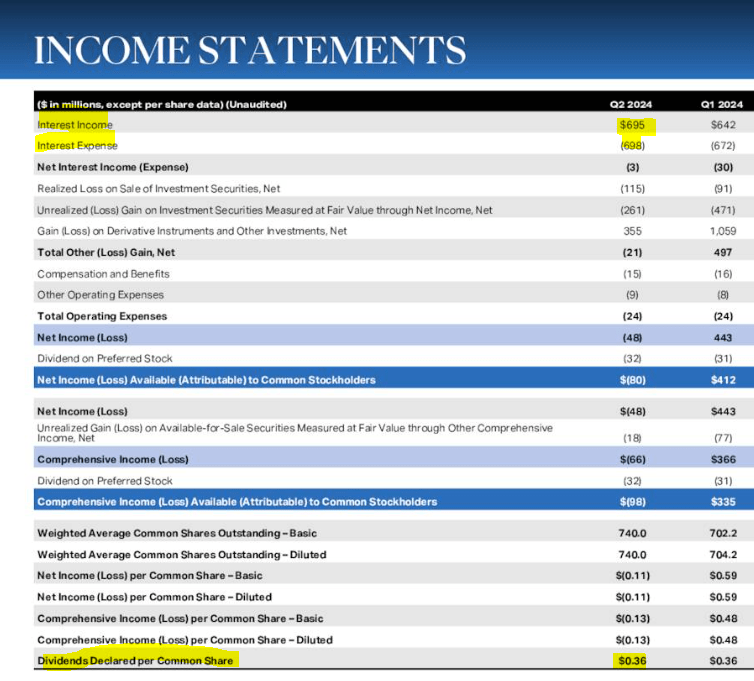

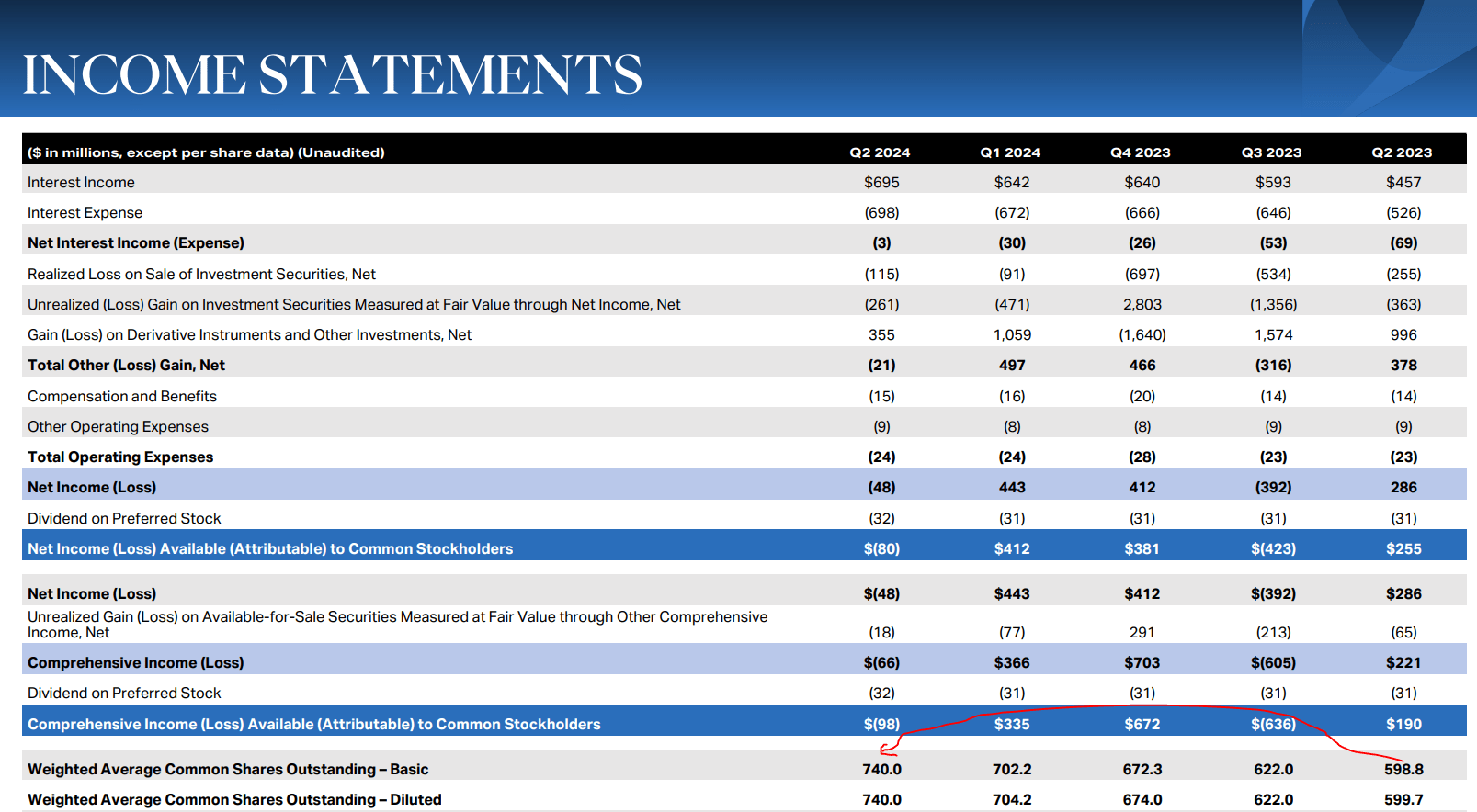

AGNC’s interest income rose smartly quarter over quarter, but we also saw a good-sized jump in interest expense. Notable in the picture below is that the net interest income number was negative in both quarters of this year. That, of course, flies in the face of the chronic bull chirping that there has never been a better time to be a mortgage REIT.

AGNC Q2-2024 Presentation

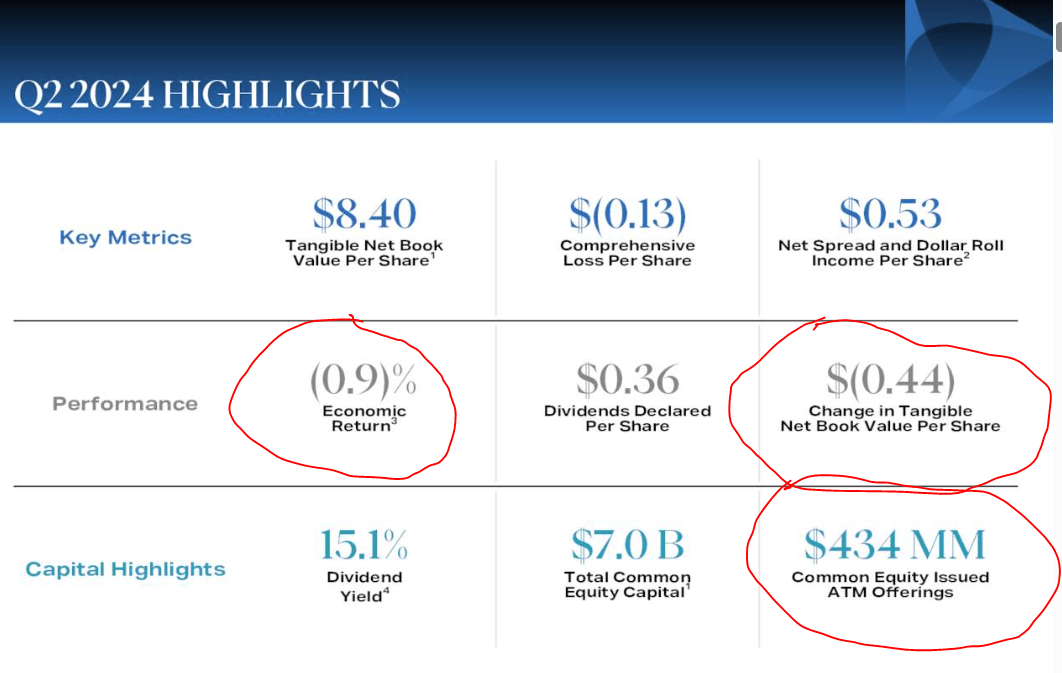

As shown above, the dividends were maintained. But what was the real return for the company? Well, you have to just ask AGNC as they actually tell you that in their very first slide called “Q2-2024 highlights.” According to them, economic return was negative 0.9% for the quarter. 36 cents of dividends were offset with 44 cents of tangible book value loss. What was truly remarkable was that we got here with AGNC issuing yet another record amount of equity.

AGNC Q2-2024 Presentation

$434 million of additional equity at a premium to NAV. Those curious as to what AGNC has been doing for the last five quarters, just need to examine the shares outstanding. As long as you hold this company at a premium, there is absolutely nothing else they like to do more than sell your stock. If that does not tell you how they feel about the current valuation, nothing will.

AGNC Q2-2024 Presentation

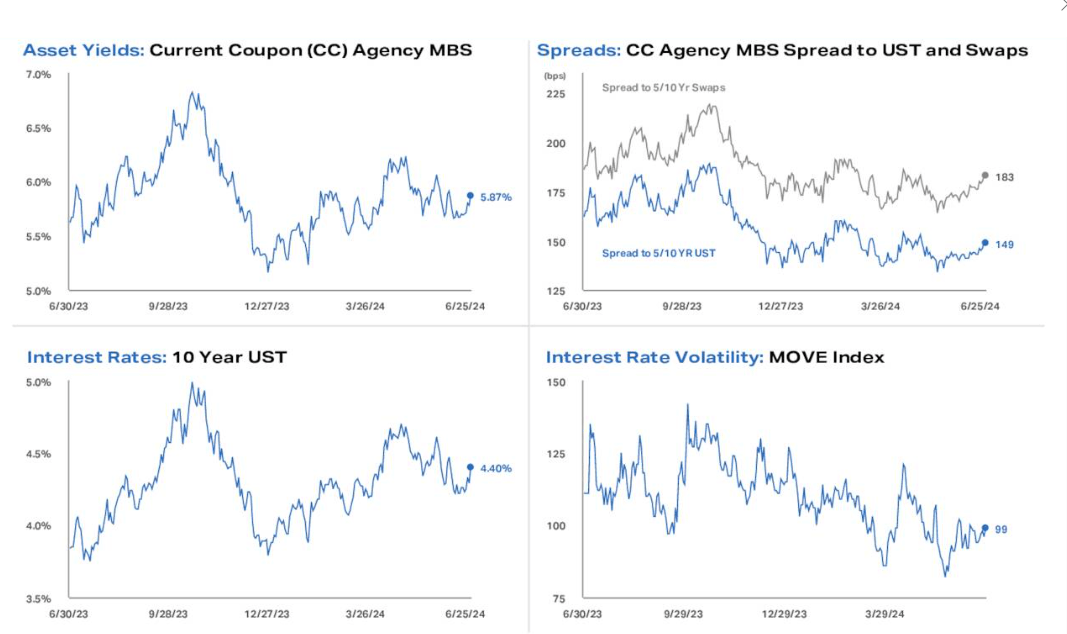

So all-in-all, it was another poor quarter from a book value perspective. Market conditions were fairly calm in Q2-2024. Spreads that generally influence matters for AGNC, were rather well-behaved. Mortgage Backed Spreads to 10 year Treasuries have risen a bit, but even these declined if you measure from the end of Q1-2024 to the end of Q2-2024.

AGNC Q2-2024 Presentation

So in the midst of relatively perfect conditions, AGNC could not make any money, at least as measured by their foremost metric, economic returns.

Outlook

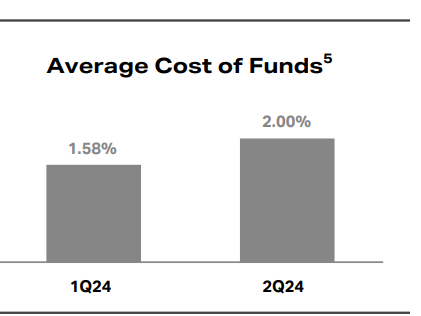

For AGNC, the impact of hedge rolls is beginning to become apparent. Average cost of funds in the slide below (which includes impact of hedges) had the largest jump in a long time. That cost went from 1.58% to 2.00%.

AGNC Q2-2024 Presentation

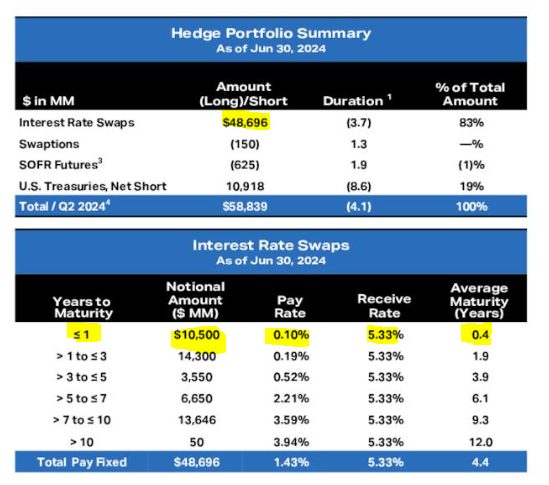

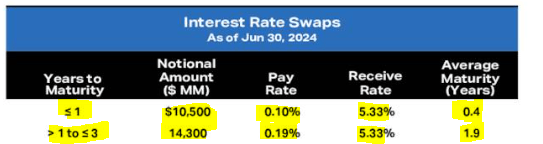

And this number is not close to being done. Even accounting for the rather unusual turn of events where the Federal Reserve is likely to cut just before the upcoming election. That cut will have a marginal impact relative to the hedges that are rolling off. We have highlighted the total amount of interest rate swaps and the ones rolling off well before 2024 ends.

AGNC Q2-2024 Presentation

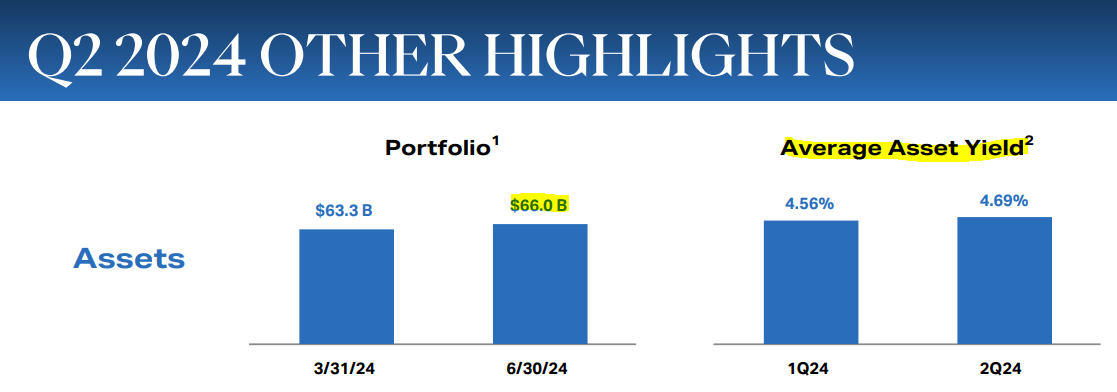

AGNC’s portfolio is currently at $66.0 billion and yields less than their cost of funding excluding hedges.

AGNC Q2-2024 Presentation

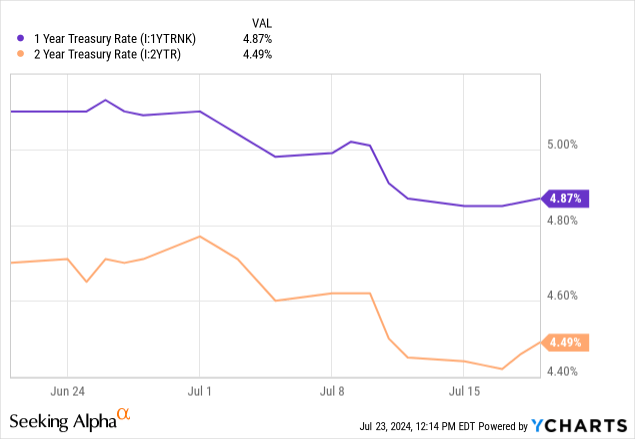

So as we move into 2025, you will see some further compression in their earning ability. The bulls may be banking on aggressive rate cuts. That may or may not happen. The Fed dot plots are not at all aggressive in their outlook for rate cuts. Without looking at the dot plots, you can get a sense of where the market is at, but looking at the 1 and 2 year Treasury rates.

The 1 year incorporates the probabilities of rate cuts over the next 12 months, and the 2 year does the same over the next 24 months. They are both projecting a floor rate of around 4%. That, if true, will be brutal once the second tranche of hedges runs out.

AGNC Q2-2024 Presentation

AGNC Stock Valuation

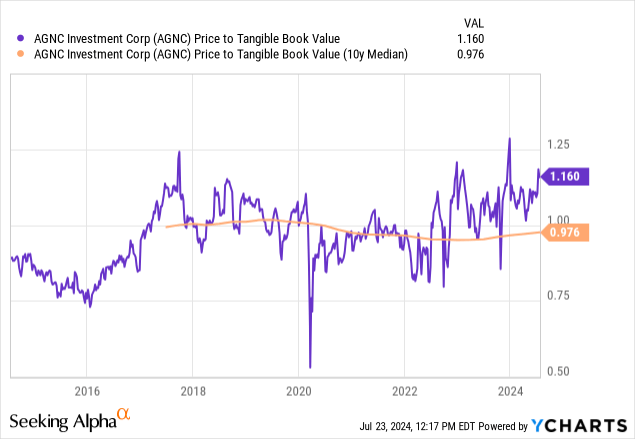

Under all of this poor spread income potential, lies a rather expensive valuation. AGNC trades at a solid premium to tangible book value. Not only is it high, it is also far above the 10-year median.

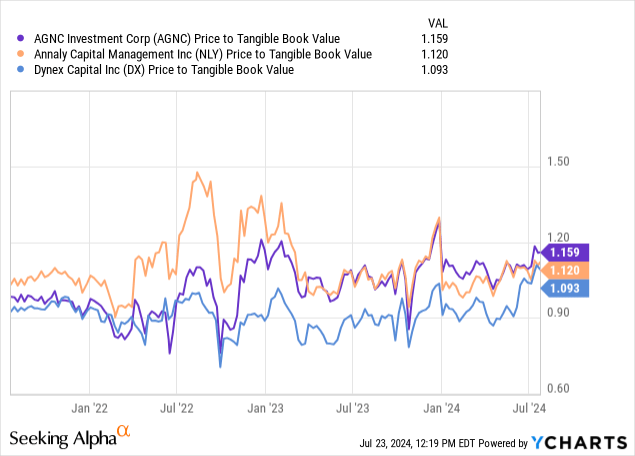

One interesting development here has been that all three have rallied higher.

But AGNC remains the most expensive out of the bunch. One final fact that makes this valuation worse is that the latest results have not been incorporated into this. AGNC’s tangible book value was $8.40, so the price to tangible book value is currently over 1.20X, based on Q2-2024.

Verdict

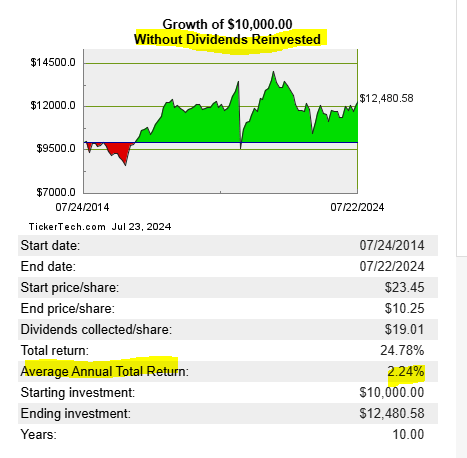

We would sell here and not look back. AGNC has delivered 2.24% over the last decade without dividends reinvested. Note that the dividends are counted, but not reinvested, in the picture below.

Split History

Even this number is boosted by a very high ending valuation of 1.2X tangible book value. If AGNC suddenly went to its tangible book value tomorrow, the total returns would be under 1.5% annually, including the dividends. There is a further adjustment here, which comes from recognizing all the extra book value AGNC captured via share issuance. If you strip that out, your returns will likely approach under 1%. Of course, we have people claiming that they did not buy 10 years back. But we have been showing these charts for about 3 years and the returns, on a rolling 10 year basis, continue to look awful.

AGNC Preferred Shares

AGNC has five different preferred securities listed on the exchanges.

- AGNC Investment Corp. 6.12% DP SH PFD F (AGNCP).

- AGNC Investment Corp. 6.5% DP SH PFD E (AGNCO).

- AGNC Investment Corp. 6.875% DEP REP D (AGNCM).

- AGNC Investment Corp. CUM 1/1000 7% C (AGNCN).

- AGNC Investment Corp. 7.75% DP PFD G (NASDAQ:AGNCL).

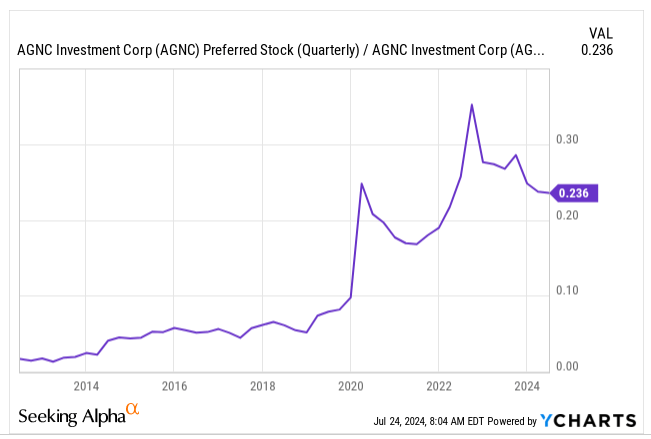

In this complex, we think AGNCL is perhaps the best. It has a stripped yield of 8.20% and it is linked in its reset to the 5-year Treasury. In a higher for longer environment, we see this as a clear victor. We have traded some of these in the past when the pricing was opportunistic. But we don’t see these as the best for “buy and hold” investors. Allow us to explain. We have previously used our favorite metric to evaluate the safety of these preferred shares. That is the ratio of the preferred equity relative to the total market capitalization.

Y-Charts

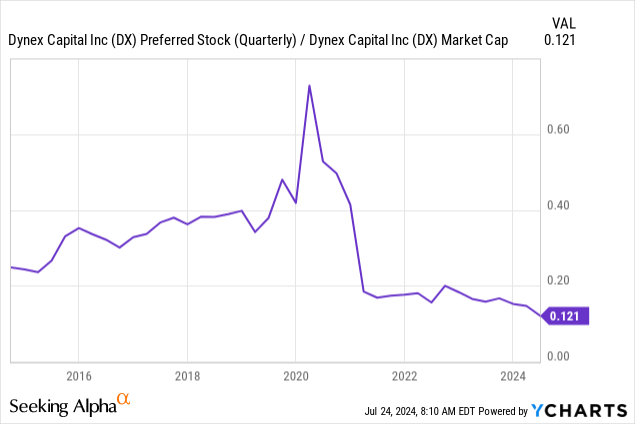

That ratio is still too high for us for AGNC. This number overstates the buffer in a way, as AGNC trades well above tangible book value, and we used market cap as a proxy for total (not per share) tangible book value. Investors may feel that we are griping on this unnecessarily, but there are firms out there, in this space, that actually meet our criteria. Below we show the same numbers of Dynex Capital Inc. (DX).

So all else being equal, we would get our preferred offerings from firms with an adequate buffer to withstand the upcoming turmoil.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking for Real Yields which reduce portfolio volatility?

Conservative Income Portfolio targets the best value stocks with the highest margins of safety. The volatility of these investments is further lowered using the best priced options. Our Enhanced Equity Income Solutions Portfolio is designed to reduce volatility while generating 7-9% yields.

Take advantage of the currently offered discount on annual memberships and give CIP a try. The offer comes with a 11 month money guarantee, for first time members.