Summary:

- Agnico Eagle Mines stock is performing roughly in-line with the price of gold, which is a red flag for investors.

- As long as the macroeconomic environment remains supportive, I expect the stock to perform well through the rest of 2024.

- Beyond that, however, investors would need to rely on extremely optimistic assumptions in order to justify the current share price.

mikulas1/E+ via Getty Images

Agnico Eagle Mines Limited (NYSE:AEM) is among my favorite picks within the gold mining sector, and as an investor who has been bullish on gold since 2019, it was just a matter of time before I turned bullish on the stock.

Back in May of this year, however, I have made the decision to sell the stock as the nearly 70% rally resulted in most of the future upside being priced-in.

Since then, the precious metal has continued its ascent as risks for the financial system remain at multi-year highs, but AEM’s share price performance has failed to live up to the expectations. Although AEM outperformed gold on an absolute basis, the risk that investors took with the stock was not worth it relative to having a direct exposure to gold.

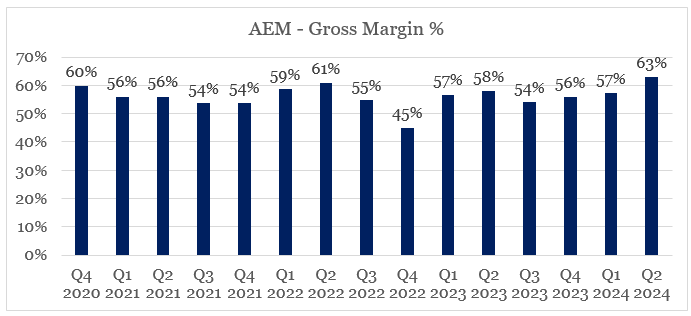

Now that AEM’s gross margins are near record-highs and sell-side analysts are rushing to adjust their price targets, I still have a hard time turning bullish on the stock.

prepared by the author, using data from Seeking Alpha

If equities continue to perform well and other macroeconomic tailwinds remain supportive for the share price of AEM, then I expect the stock to perform well in the next couple of months. Beyond that, however, I find it hard to once again turn bullish.

Short-term Tailwinds

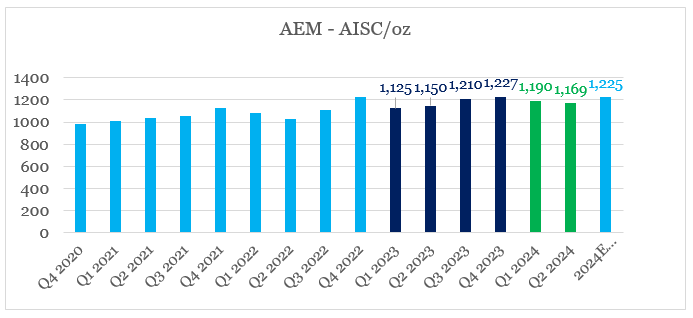

During the last reported quarter, AEM’s management retained its FY 2024 guidance of low All-In Sustaining Cost per ounce (AISC) and capital expenditures within the range of $1.6bn to $1.7bn – record low as a share of total revenue figure.

2024 gold production and cost guidance reiterated – Full year expected payable gold production remains unchanged at approximately 3.35 to 3.55 million ounces in 2024, with total cash costs per ounce and AISC per ounce in 2024 unchanged at $875 to $925 and $1,200 to $1,250, respectively. Total capital expenditures (excluding capitalized exploration) for 2024 are still estimated to be between $1.6 billion to $1.7 billion.

Source: AEM Q2 2024 Earnings Release

What that means is that, at least in the near term, as gold prices keep making new all-time highs and AISC remain low, then Agnico will be in a very good position to achieve even higher margins going forward.

In reality, however, the mid-point of the full year AISC guidance is $1,225 per ounce, which is significantly higher than the $1,190 and $1,169 reported in Q1 and Q2 of 2024 respectively.

prepared by the author, using data from earnings releases

Therefore, for the second half of 2024, AISC should come at around $1,270 if management’s outlook for the year is to be achieved.

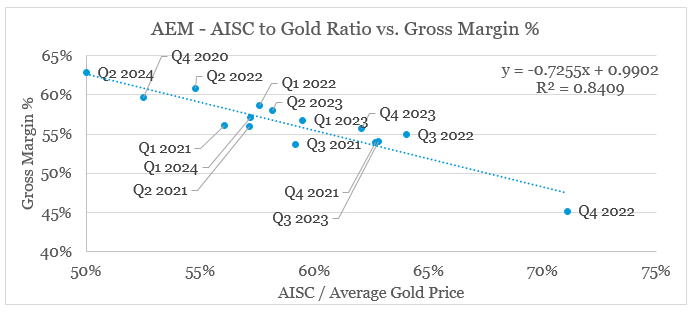

Based on that estimate and the average spot price of gold during Q3 2024 of around $2,480, we are looking at AISC to Gold ratio of roughly 51%. Then, we could use the relationship between AEM’s quarterly AISC to gold ratios and the company’s gross margin figures to forecast Q3 gross margin of slightly below 62%. Such a scenario would mark a slight decline from Q2 2024 margin and is unlikely to be well-received by the market.

prepared by the author, using data from Seeking Alpha and Earnings Releases

With gold spot prices now in excess of $2,600 per ounce, however, investors will be expecting a notable gross margin expansion in the last quarter of 2024. This might have a significant short-term positive impact on AEM’s share price during the Q3 2024 earnings release, provided that 2024 guidance remains unchanged.

Having sad that, however, investors looking to hold AEM beyond 2024 will be looking for some more clearance regarding 2025. More specifically, for AEM to continue to perform well against the broader equity market, we will need the following:

- AISC guidance for next fiscal year to remain at or near current levels;

- Gold price to remain at least flat.

So far, these two scenarios appear likely as tailwinds for low-risk assets, such as gold, remain and energy prices are still at record lows which will be a tailwind for AISC.

Limited Upside

Even if investors remain optimistic about the relationship between the price of gold and energy prices, AEM is no longer as attractive as it used to be back in mid-2022. Hence, shareholder returns are likely to be far lower than what we have seen since then.

Seeking Alpha

Firstly, AEM no longer trades at such attractive levels relative to sales, as the market is already pricing-in the recent improvement in margins. The good news is that AEM’s price/sales multiple is not anywhere close to the record highs reached in 2016, 2019 and 2020 periods (see below).

Therefore, if gold remains at its current levels and AISC guidance for 2025 is not materially different from 2024, then I see scope for AEM’s price/sales multiple reaching levels of 6 and above. This, however, would be a major red flag for me, as such high multiples are often unsustainable and prone to sharp reversals.

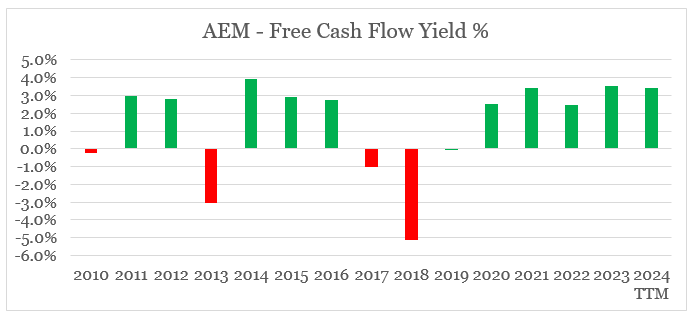

On a free cash flow basis, AEM trades at a yield of 3.4% which is attractive on a historical basis, but nothing to brag about when bond yields are in excess of 4%.

prepared by the author, using data from Seeking Alpha

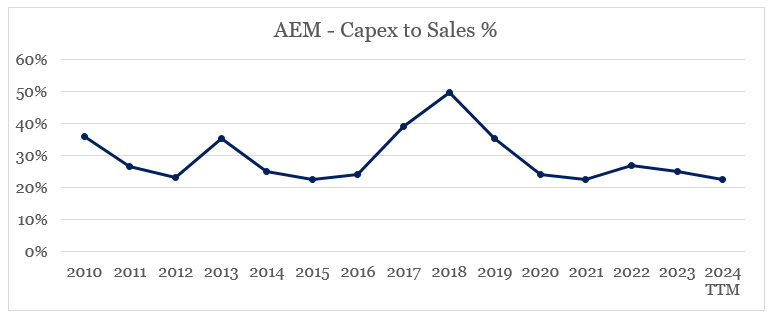

This brings us to the other risk for AEM investors in 2025 – an uptick in capital expenditures. The current capex to sales ratio is already at record lows (see the graph below) and as we saw above, AEM’s management does not expect any notable increases through the rest of FY 2024. This should provide temporary tailwinds for free cash flow, but I do not expect it to last.

prepared by the author, using data from Seeking Alpha

In recent years, AEM was able to reduce its capex relative to sales as the company capitalized on cheap valuations within the sector and a number of lucrative M&A opportunities. At present, however, the company will have to once again prioritize organic growth and rely more heavily on internally financed projects. Without a more meaningful increase in capex, gold production is likely to stall at around 3.5m ounces a year.

prepared by the author, using data from Earnings Releases

Based on all that, it appears highly likely for AEM to trade at much lower free cash flow yields going forward, which in my view would be a major drag on shareholder returns in 2025.

Conclusion

As AEM once again trades near all-time highs and the stock has almost doubled since my initial buy rating, I see fairly limited upside for 2025. Should current macroeconomic tailwinds remain, the stock could offer more upside through the rest of 2024. As a long-term investor, however, I prefer having a direct exposure to gold at the moment.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies' SEC filings. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

This idea was discussed in further detail in The Roundabout Investor. To find similar investment opportunities and learn more about how the roundabout investment philosophy could protect portfolio returns during market downturns, follow this link.

This idea was discussed in further detail in The Roundabout Investor. To find similar investment opportunities and learn more about how the roundabout investment philosophy could protect portfolio returns during market downturns, follow this link.