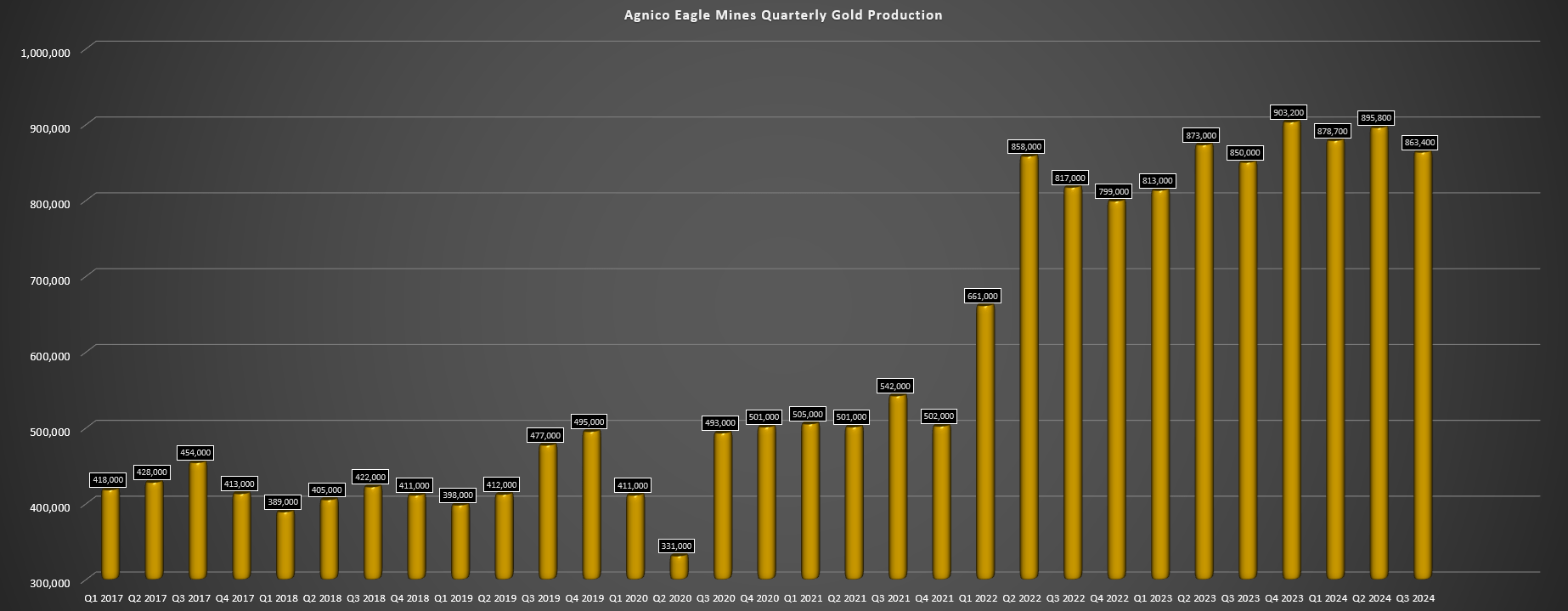

Agnico Eagle Mines Limited reported another blowout quarter in Q3 ’24 with 2% higher production to ~863,400 ounces and solid cost control with just a 2% increase in cash costs year-over-year.

This impressive cost control combined with record gold prices allowed the company to enjoy an 1100 basis point increase in AISC margins and a 600%+ increase in free cash flow.

Even more importantly than any quarterly result, the company’s pipeline continues to improve each quarter with consistent exploration success across the portfolio of key assets.

In this update, we’ll dig into Agnico’s Q3-24 results, recent developments, and why it continues to be the premier way to gain exposure to gold assuming the stock is bought on sharp pullbacks.

Claude Laprise

The Q3 Earnings Season for the VanEck Gold Miners ETF (GDX) began last week, and two of the world’s largest gold producers have now reported their results. Fortunately, Agnico Eagle Mines Limited (NYSE:AEM) fared far better than the world’s largest gold producer, reiterating its cost guidance and plans to land within its guidance range despite a near 3% headwind from the much higher gold price (higher royalties) on its operating expenses. This was related to its budget for 2024 being at $1,800/oz gold. In fact, Agnico’s cash costs were up only 2% year-over-year and are sitting below its guidance midpoint ($897/oz vs. $900/oz) heading into Q4, while all-in sustaining costs are tracking well against guidance.

The above point is critical for investors both in the sector and new to the sector because while so many companies promise leverage to the gold price, investors often end up with the opposite. This is because we often see share counts rising far faster than production and an inability to keep a lid on costs, which means that the inevitable bull moves in gold/silver don’t deliver the expected bottom-line results. Hence, perhaps the most important takeaway from Agnico’s Q3-24 results was as follows, which was confirmation that it delivered the leverage its shareholders hoped for where so many others have come up short, evidenced by a ~1,100 basis point increase in AISC margins year-over-year.

“Our focus on operational performance, cost control and capital discipline has allowed us to deliver the leverage to record gold prices to our shareholders.”

– Agnico Eagle Q3-24 Results.

Just as importantly, while other diversified producers like Coeur Mining, Inc. (CDE) and First Majestic Silver Corp. (AG) have been printing shares at break-neck speed through ATM issuance and overpriced acquisitions, Agnico has focused on quality when it acquires but still done so counter-cyclically, allowing it to consistently grow its per share metrics and production per share. And with the gold price setting records, Agnico is in the enviable position that it doesn’t have to rush out and do M&A, sitting on the best pipeline in its history with multiple 200,000-450,000 ounce opportunities at existing sites or in existing camps, or with the ability to leverage off existing infrastructure.

Hence, while other producers will be forced to pay up to stay relevant and continue to show “growth,” Agnico can sit back and reduce its share count opportunistically, ensuring shareholders see the benefits of its growth across all of its key per share metrics. In this update, we’ll dig into Agnico’s Q3-24 results, recent developments, and why it continues to be the premier way to gain exposure to gold assuming the stock is bought on sharp pullbacks.

Meadowbank Operations – Company Video

All figures are in United States Dollars unless otherwise noted. G/T = grams per tonne (of gold or silver). GEOs = gold-equivalent ounces. SEOs = silver-equivalent ounces. AISC refers to all-in sustaining costs. LOMP = life of mine plan. TPD = tonnes per day.

Q3 Production & Sales

Agnico Eagle (“Agnico”) reported quarterly production of ~863,400 ounces of gold in Q3-24 (+2%) at cash costs of $921/oz (+2%) and AISC of $1,286/oz (+6%). These increases in costs were more than offset by a 29% increase in its average realized gold price to $2,492/oz (Q3-23: $1,928/oz) and with a far stronger Q4-24 on deck given that gold has averaged ~$2,680/oz, more financial records can be expected, in addition to a further tick higher in margins to 53% or higher assuming gold prices don’t collapse into year-end. As for sales performance, Agnico sold ~856,000 ounces of gold in the quarter for record revenue of ~$2.16 billion, trouncing its previous record of ~$2.08 billion set in the previous quarter (+4% sequentially).

Agnico Eagle Quarterly Gold Production – Company Filings, Author’s Chart

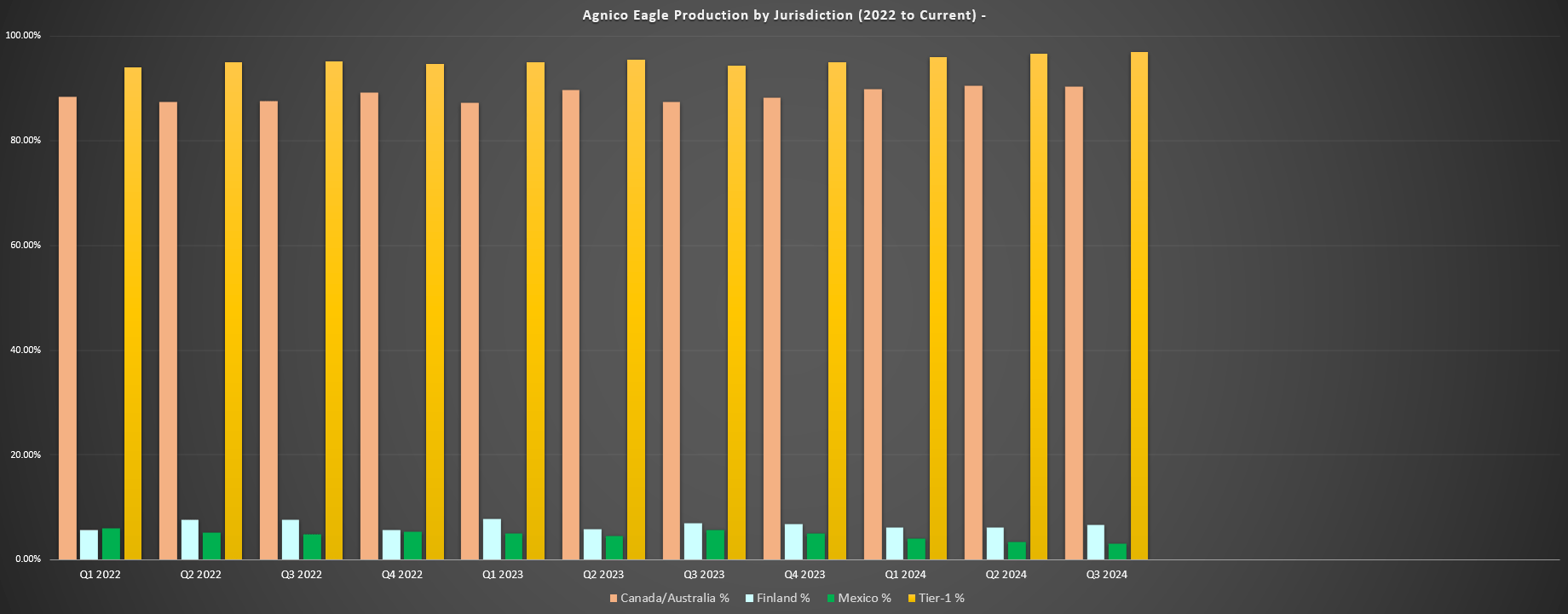

Agnico Eagle – Quarterly Production by Jurisdiction – Company Filings, Author’s Chart

As the charts above highlight, Agnico grew quarterly production year-over-year despite being up against tough comps as Canadian Malartic transitions to a primarily underground operation (Odyssey) and lapped elevated grades (Q3-23: 1.22 G/T of gold), a steeply declining grade profile at Fosterville which was to be expected as high-grade Swan Zone reserves are depleted, and a shift to residual leaching at La India. Plus, it accomplished this while increasingits proportion of production coming from top-ranked jurisdictions. In fact, production from Finland, Canada, and Australia (Tier-1 ranked jurisdictions) made up ~97% of total gold production, up 300 basis points from ~94% in the year-ago period.

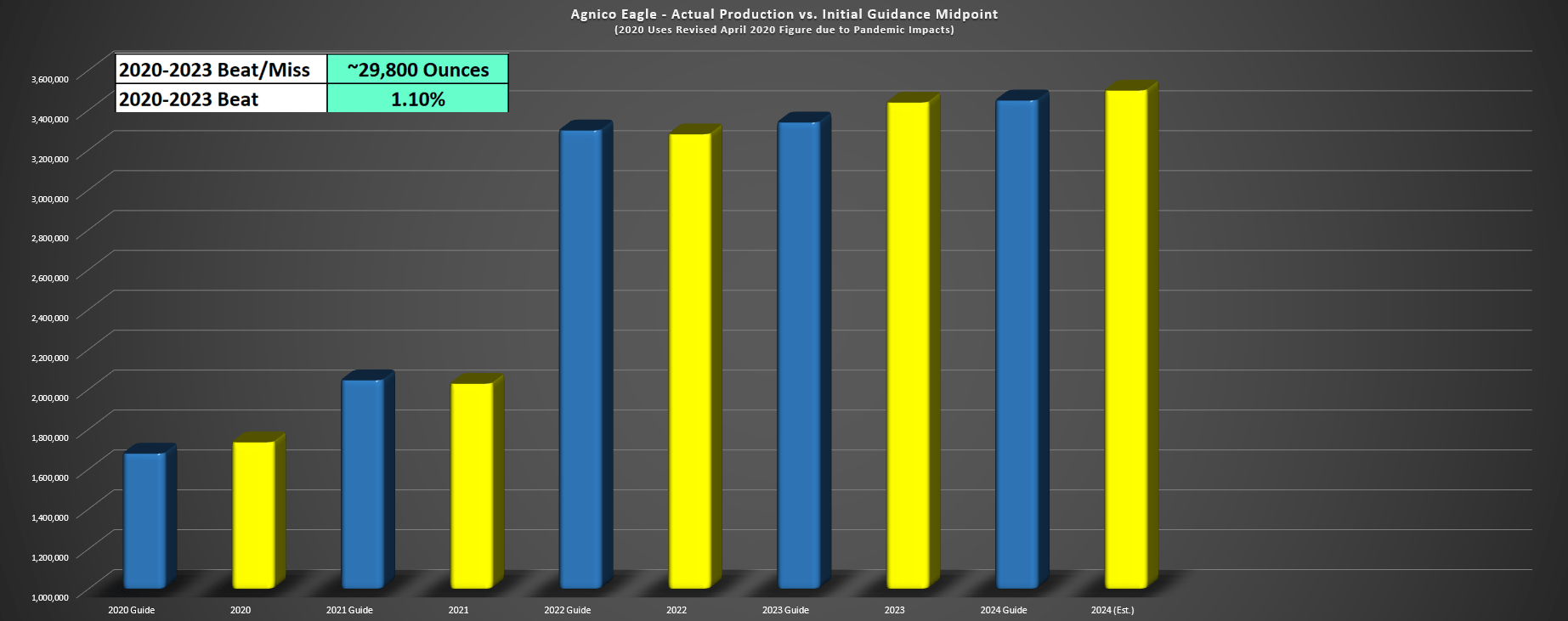

Agnico Eagle Actual Production & 2024 Est vs. Guidance Midpoint – Company Filings, Author’s Chart & Estimates

As for year-to-date progress relative to its guidance, Agnico’s year-to-date production is sitting at ~2.64 million ounces of gold, tracking quite well against its initial guidance midpoint of 3.45 million ounces. In fact, the company is sitting at 76.5% of its initial guidance midpoint, suggesting a decent likelihood of a beat vs. this guidance midpoint with annual production likely to land at or above 3.5 million ounces of gold. And while several other million-ounce producers have failed to consistently deliver on guidance, Agnico is on track for another beat vs. its midpoint, complementing an average beat of ~30,000 ounces, or 1.1% in the 4-year period from 2020-2023.

Mine Site Performance

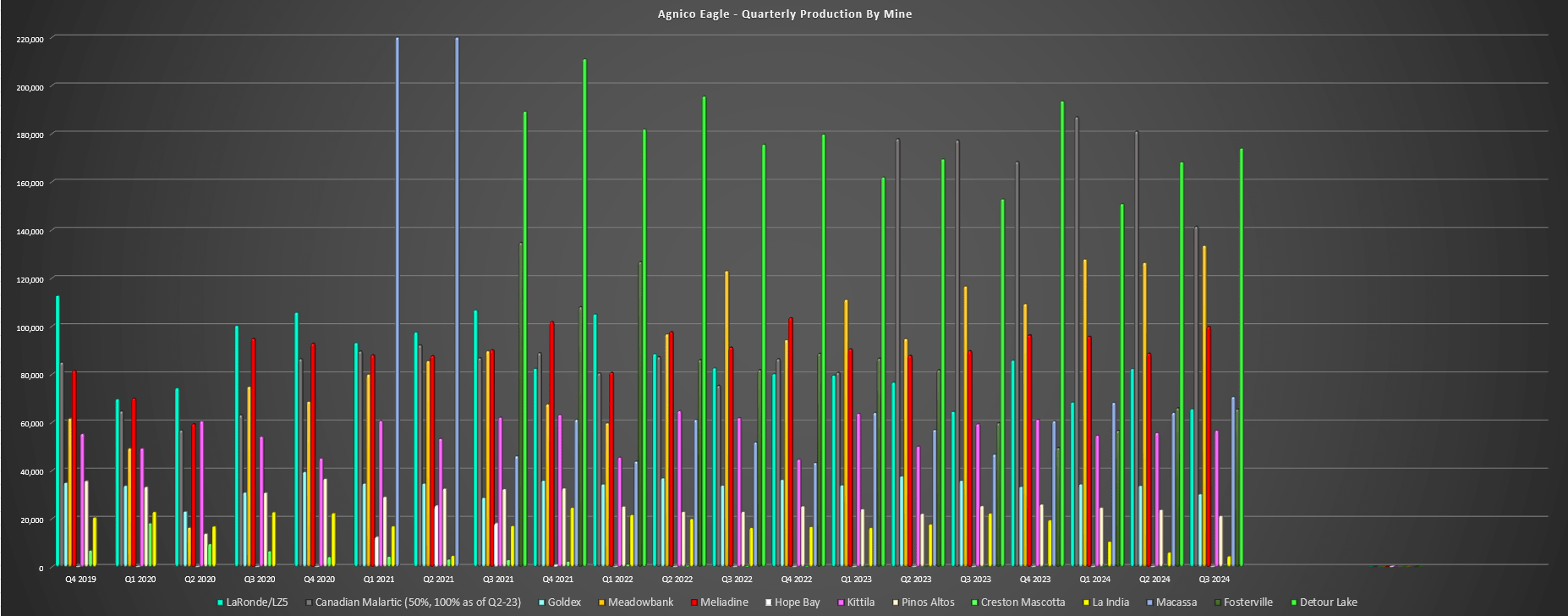

Looking at performance across Agnico’s mine sites in Q3-24, higher gold production was helped by production growth at four key assets, with these being Meliadine, Meadowbank, Macassa and Detour Lake. This was offset by lower production at Canadian Malartic due to difficult comps and related lower grades which were to be expected in H2-24, lower output at Goldex, slightly lower output at Kittila, and lower output at its smaller Mexican mines.

Agnico Eagle Quarterly Production by Mine – Company Filings, Author’s Chart

Starting with its LaRonde Complex, production came in at ~65,600 ounces of gold at $1,135/oz cash costs, roughly flat year-over-year but at higher costs. This was related to higher throughput of ~687,000 tonnes processed but at lower grades (3.2 G/T of gold vs. 3.43 G/T of gold), with lower grades being in line with plans and shutdowns in the quarter taking a little longer than expected (11 days of downtime at LaRonde Mill, 17 days of downtime at LaRonde Mine related to the ore handling system). Agnico noted that rehabilitation in the West Mine area was completed in Q3 after the June seismic event, impacting production in the period, with LZ5 picking up some slack (albeit at lower grades).

The other positive developments in the period aside from rehabilitation work being completed were that the LaRonde Complex has greater operational flexibility with the LZ5 plant restarted, and with planned shutdowns completed, we should see a solid Q4-24. Meanwhile, Agnico continues to increase automation at LaRonde which has exceeded targets to date. In fact, over 1,700 TPD were moved year-to-date from automated scoops/trucks, an impressive feat which ultimately helps to make it a safer mine for its team members and aid in extending the mine life.

LaRonde Complex – Company Website

Moving west to its highest-grade Macassa Mine, the mine may not be its largest, but it put together an impressive performance in Q2-24 with its best quarter to date since the Kirkland Lake Gold merger. This was evidenced by production of ~70,700 ounces of gold (+51% year-over-year) at cash costs of $750/oz (Q3-24: $850/oz), driven by higher throughput at higher grades. In fact, with ~134,000 tonnes processed at 16.84 G/T of gold in Q3-24 (Q2-23: ~112,000 tonnes at 13.35 G/T of gold), Agnico noted that the bottleneck has shifted from the mine to the mill, with work ongoing to help beat the 1650 TPD milling rate with its current infrastructure.

Digging into the much better quarter, Agnico noted that higher production was related to productivity from a larger workforce, new ventilation infrastructure and the #4 shaft completion, higher equipment availability, plus additional ore from the Macassa Near Surface deposit. As for current work on site, Agnico shared that its new paste plant was now 70% complete and on track for commissioning in H1-25. Elsewhere, on the exploration front, the company hit 5.7 meters at 7.7 G/T of gold at 245 meters depth and 1.9 meters at 11.8 G/T of gold at 251 meters depth at its Amalgamated Kirkland deposit which sits much shallower than its current mining area at Macassa, pointing to potential further resource growth at this high-grade complex (Macassa, Macassa Near-Surface, AK).

Macassa Underground Operations – Kirkland Lake Gold

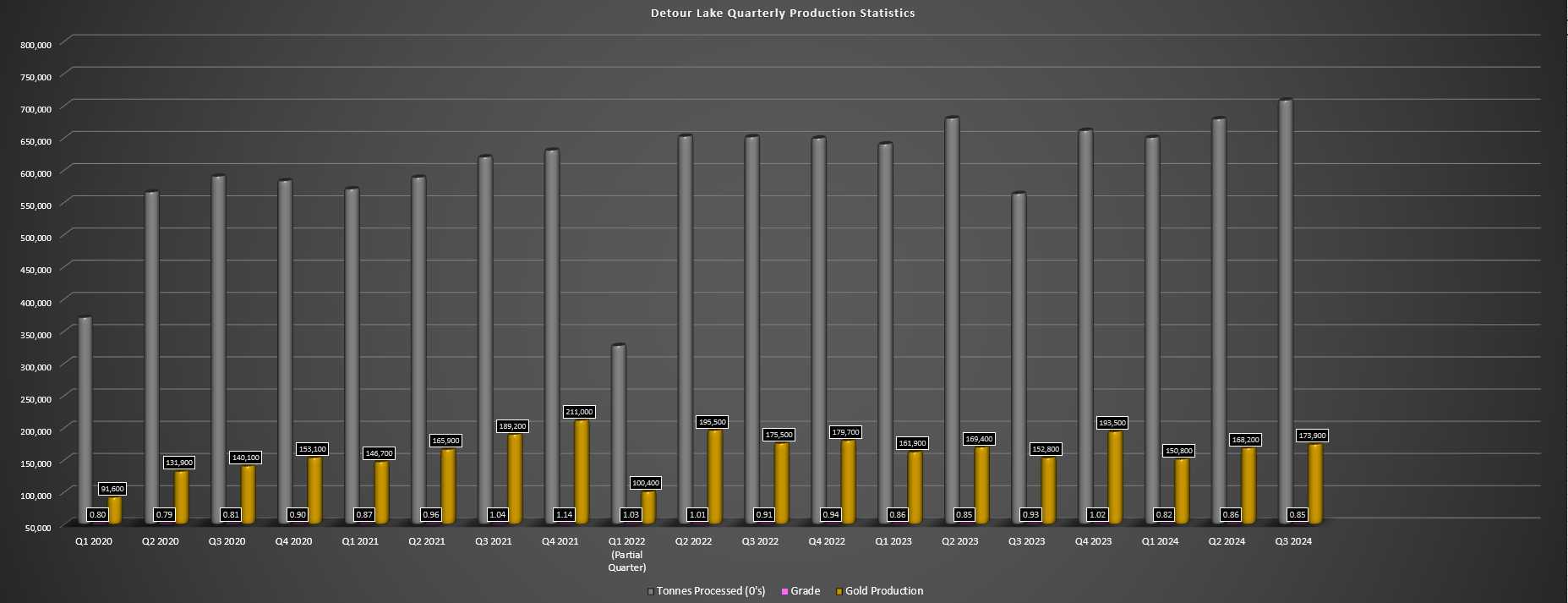

Moving north to Detour Lake, this Tier-1 scale asset had another incredible quarter, producing ~173,900 ounces of gold at cash costs of $779/oz. This was driven by record quarterly throughput of ~77,000 TPD that beat its target of ~76,700 TPD, with an annualized milling rate of ~28.1 million tonnes per annum in the quarter. Unfortunately, this did not translate to record production due to lower grades at 0.85 G/T of gold, but this asset is still tracking to deliver just shy of its goal of ~690,000 ounces based on its guidance midpoint, with ~493,000 ounces produced year-to-date.

Detour Lake Production & Operating Metrics – Company Filings, Author’s Chart

As for the improved performance, Agnico stated that record throughput was driven by higher mill run-time (93%) than planned and the replacement of the defective grinding media in the SAG mill as well as the installation of a new ball mill discharge grizzly on line 2. The company hopes to continue increasing throughput on the back of additional initiatives that include a new ball mill discharge grizzly on line 2, an SAG discharge box upgrade, and the installation of variable speed drives to the secondary crushers.

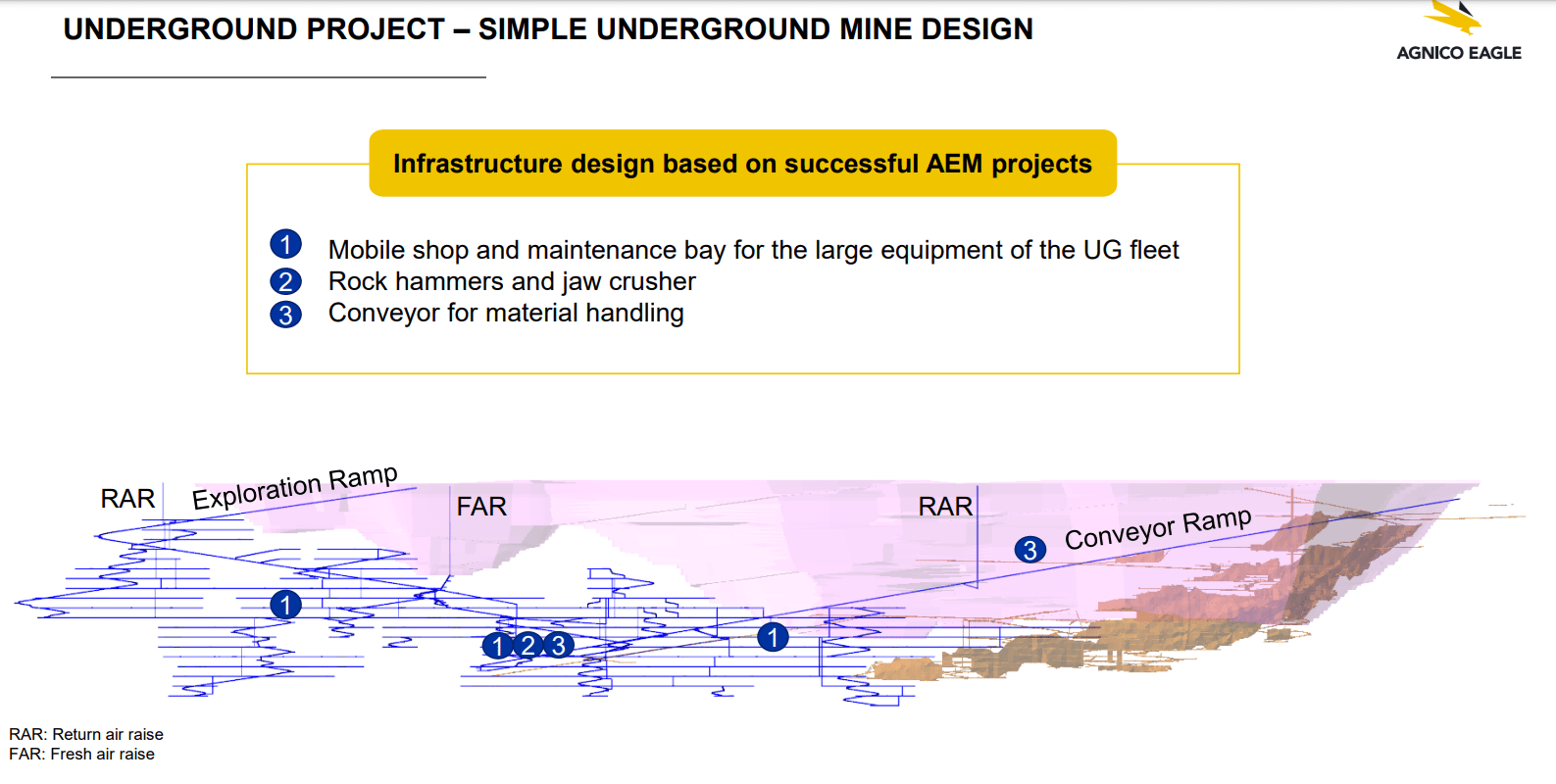

As for tackling lower recovery rates, recoveries improved in Q3-24 with the replacement of defective grinding media in the SAG mill, but fell short of plans in Q3 due to abnormal carbon breakage in the CIP circuit which appears to be remedied since then. Finally, Agnico shared that it enjoyed the highest daily tonnes mined from the open pit to date in 2024 with the commissioning of a new Komatsu rope shovel that offers higher capacity and improved truck availability. Overall, these initiatives continue to position Detour Lake for closer to 750,000 ounces in 2025 and 2026 ahead of a potential increase to 1.0 million ounces per annum in 2030 if it approves its Detour Underground Expansion.

Given that the IRR on this expansion and mill optimization is sitting closer to 30% at spot gold price levels which might actually end up being conservative looking out to 2030 closer to project completion, this is certainly looking like a low-risk expansion that’s likely to be approved. In fact, recent drilling at Detour Lake continues to deliver exceptional results, with a highlight intercept of 18.9 meters at 15.0 G/T of gold in the interpreted high-grade corridor, as well as other high-grade intercepts like 34.5 meters at 6.0 G/T of gold, 4.1 meters at 67.8 G/T of gold, and 4.2 meters at 18.8 G/T of gold, in addition to higher-grade intercepts near surface and near the planned exploration ramp, like 24.6 meters at 2.5 G/T of gold and 20.3 meters at 3.1 G/T of gold.

Potential Detour Underground Project – Company Website

Moving back to Quebec for Canadian Malartic, production was ~141,400 ounces at $1,025/oz cash costs, down sharply from ~177,200 ounces in Q3-23. However, as noted previously, the mine was lapping difficult comparisons with average grades of 1.22 G/T of gold in the year-ago period and the expectation was for lower grades this quarter. Plus, underground production came in slightly lower than planned due to a delay in mining high-grade stopes. On a positive note, this mine was still a cash cow in the period and year-to-date with ~509,000 ounces produced which continues to track towards a beat vs. its guidance of 630,000 ounces at the mid-point.

As for progress on development, Agnico noted that Odyssey South’s development is ahead of plan, helped by teleoperated and automated equipment. Meanwhile, its main Odyssey ramp is sitting at 873 meters and shaft sinking remains on schedule at a depth of 839 meters. Finally, surface construction began on schedule in Q3-24, and it continues to be a very busy period for drilling at Odyssey to potentially inform the addition of a second shaft down the road, with ~146,000 meters of drilling completed in the first nine months of 2024 alone.

Moving to Nunavut, Meliadine had a strong quarter as well, producing ~99,800 ounces of gold (+11% year-over-year) at lower cash costs of $877/oz. The strong performance was driven by record quarterly throughput with the completion of the Phase 2 Mill Expansion to 6,000 TPD ahead of schedule, translating to ~533,000 tonnes processed at 6.08 G/T of gold in the period. As for other developments, Agnico noted that it hopes to receive permits for the amendment to its Type A water license in Q1-25. Meanwhile, on the exploration front, the company released solid results from Tiriganiaq at depth, with an impressive intercept of 5.2 meters at 30.5 G/T of gold roughly 100 meters from existing resources, and another hit of 5.0 meters at 12.8 G/T of gold closer to the central portion of the deposit.

As for Meadowbank, the mine produced its 5 millionth ounce of gold in what has been a massive success for the company between Meadowbank and Amaruq since beginning commercial production in Q1-2010. During Q3, the mine was one of Agnico’s top contributors with production of ~133,500 ounces (+15% year-over-year) at cash costs of $910/oz, benefiting from higher throughput, recoveries, and grades, with ~1.08 million tonnes processed at 4.19 G/T of gold. Like Meliadine, the mine also reported a record mill throughput of ~11,700 TPD and this impressive Q3 performance was despite difficult weather conditions that affected haulage in the period.

Agnico Eagle Operations – Company Video

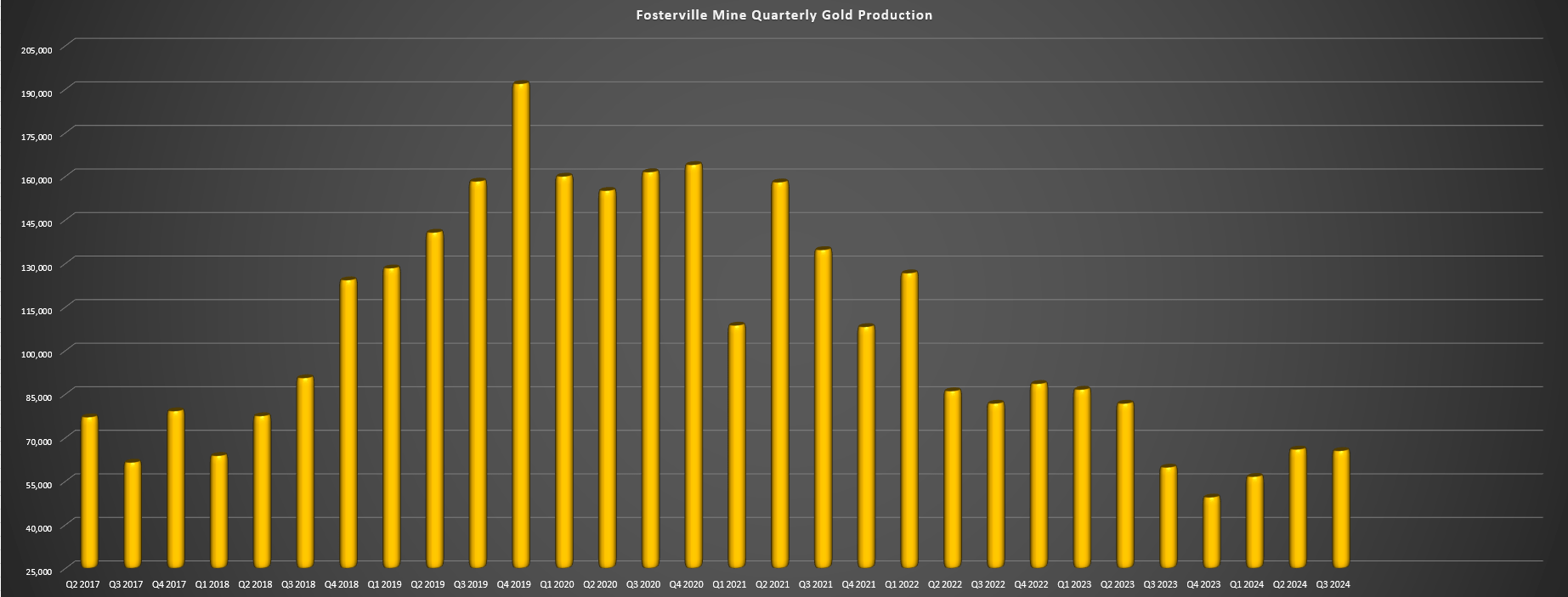

Looking at its Fosterville Mine, production increased over 10% year-over-year due to improved productivity with a quarterly record for ore mined at ~246,000 tonnes in the period. This led to the production of ~65,500 ounces of gold at cash costs of $651/oz, with ~246,000 tonnes processed at 8.61 G/T of gold. Notably, this increase in production was despite lapping much higher grades as elevated grades at the Swan Zone were depleted. Agnico noted that the improved performance was helped by better-than-planned development at Robbin’s Hill and Fosterville, and that it continues to work on maximizing throughput and lowering unit costs to offset the decline in the mine’s grade profile. The company is certainly seeing early major wins thus far on this initiative with an annualized throughput rate closer to 1.0 million tonnes per annum in Q3-24.

Fosterville Quarterly Production – Company Filings, Author’s Chart

As for its Finland operations, Kittila produced ~56,700 ounces of gold which was down slightly year-over-year on the back of lower grades which offset a higher throughput of ~544,000 tonnes. Notably, the company held the line on production costs per tonne and reported only a moderate increase in cash costs to $1,010/oz with Agnico calling out higher underground mining and maintenance expenses at Kittilas. Unfortunately, recovery rates were impacted by higher carbon and sulphur content in the ore, but on a positive note, the site has seen a 20% increase in advance rates with work on improving mine productivity that was initiated in Q2.

Finally, as for its smaller operations, its Mexican operations saw lower production year-over-year on a combined basis at ~25,900 ounces from Pinos Altos and La India as the latter mine transitioned to residual leaching. Elsewhere, Goldex saw lower production year-over-year at ~30,300 ounces but at respectable cash costs of $1,031/oz given its relatively small production profile compared to Agnico’s portfolio of primarily 300,000+ ounce assets.

Costs & Margins

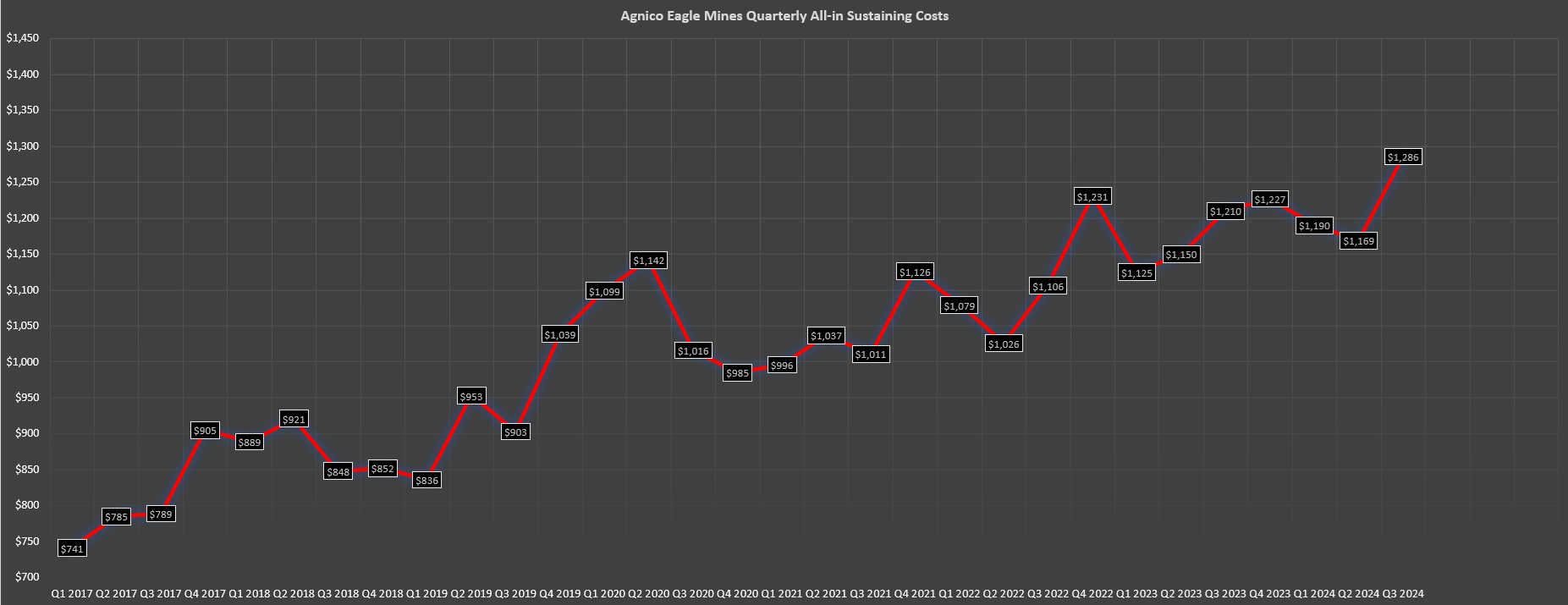

Moving over to costs and margins, Agnico reported quarterly AISC of $1,286/oz, a 6% increase from the year-ago period. While this might have exceeded some investors’ expectations, it’s important to note that sustaining capital increased materially on a year-over-year basis from ~$211 million to ~$253 million which was a large driver of higher AISC despite doing an impressive job holding the line on cash costs. Fortunately, even with the increase in AISC, Agnico is well positioned to deliver at its cost guidance of $1,225/oz (midpoint) with year-to-date AISC sitting at $1,214/oz.

Agnico Eagle Quarterly AISC – Company Filings, Author’s Chart

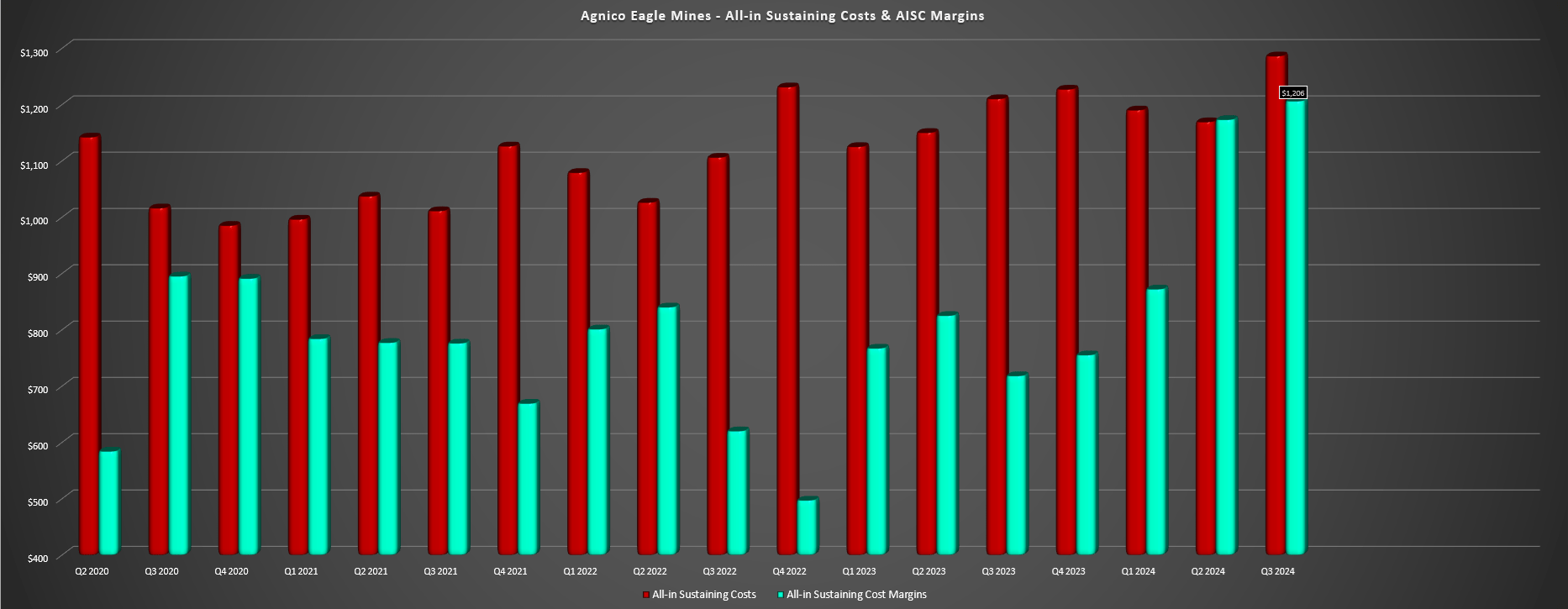

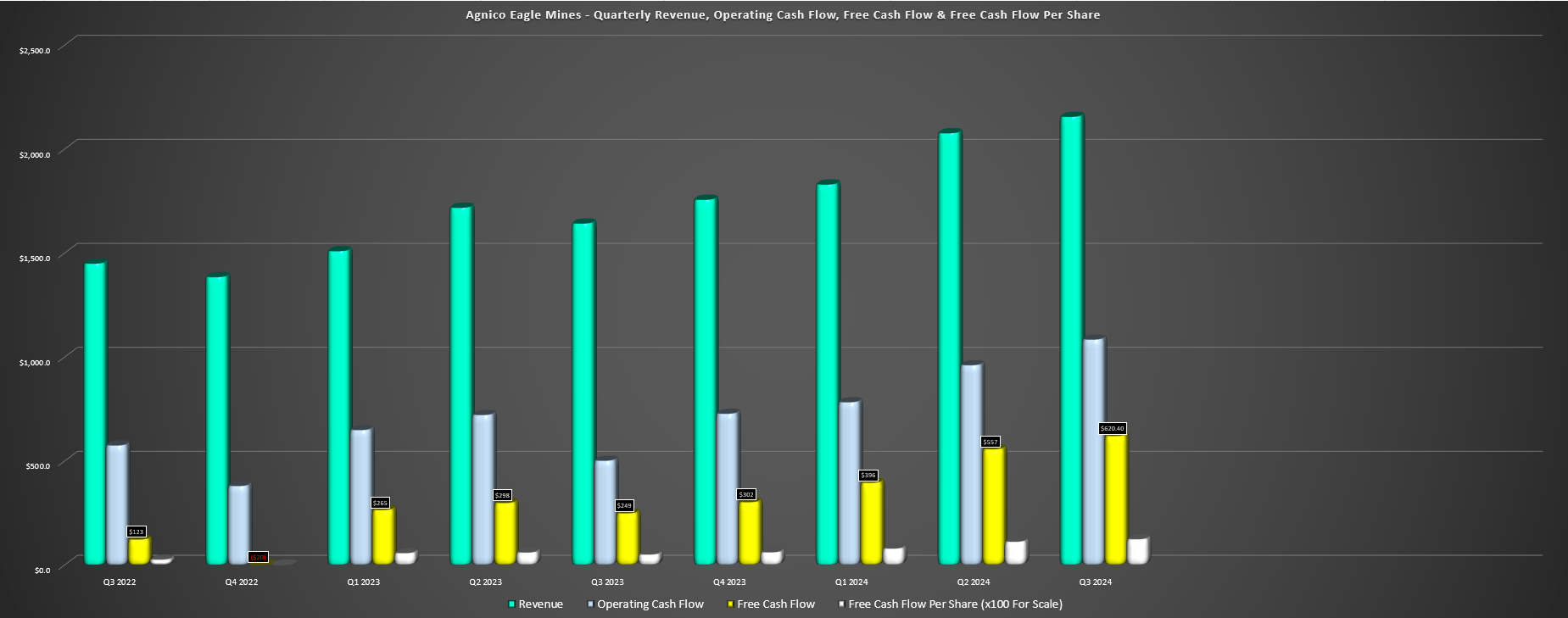

Moving to margins, we saw a massive improvement year-over-year, evidenced by AISC margins spiking to a record of $1,206/oz (48.4%) vs. $718/oz (37.2%) in the year-ago period. Notably, this will improve even further in the coming quarter, and it was this significant leverage due to strong cost control that allowed Agnico to report record financial results. This included record operating cash flow of ~$1,085 million (+116% year-over-year), record free cash flow of $620.4 million, and record free cash flow per share of $1.24 vs. 0.17 in the year-ago period (+630% year-over-year). The most impressive part about the latter statistic is that capex was actually up in the period, with PP&E of ~$486 million in Q3-24 being a minor headwind to cash flow generation.

Given the impressive financial results, Agnico elected to repay $375 million in debt and ended the quarter with just ~$490 million in net debt, down from $1.5 billion to start the year. The company also supplemented its $1.60/share annual dividend with additional share buybacks, bringing total share buybacks this year to ~1.5 million shares at an average cost of US$66.58. And while Agnico is quite conservative with its base dividend as it never wants to cut its dividend, I would not be surprised to see a special dividend announced in Q4 or Q1 to share some of these records profits with shareholders without having to take on additional risk by increasing its base dividend in case the move higher we’ve seen in gold prices turns out to be fleeting.

Unlike other producers that have missed on costs, Agnico benefits from a regional strategy and scale that makes it an employer of choice. It also benefits from a much lower contractor/employee ratio with a ratio of 1/3 for contractors vs. employees, but it shared in its Q3-24 Conference Call that it’s seeing lower contractor rates than others that have reported low double-digit inflation. Overall, this higher reliance on employees vs. contractors and what appears to be lower relative turnover gives it a competitive advantage in terms of keeping a lid on costs.

Plus, while a rise in costs was inevitable due to higher royalties related to the gold price, I wouldn’t be surprised to see Agnico Eagle enjoy another year of sub $1,250/oz AISC in 2025, allowing it to continue to move down the cost curve as most of its peers continue to report higher unit costs.

Recent Developments

Canadian Malartic/Odyssey

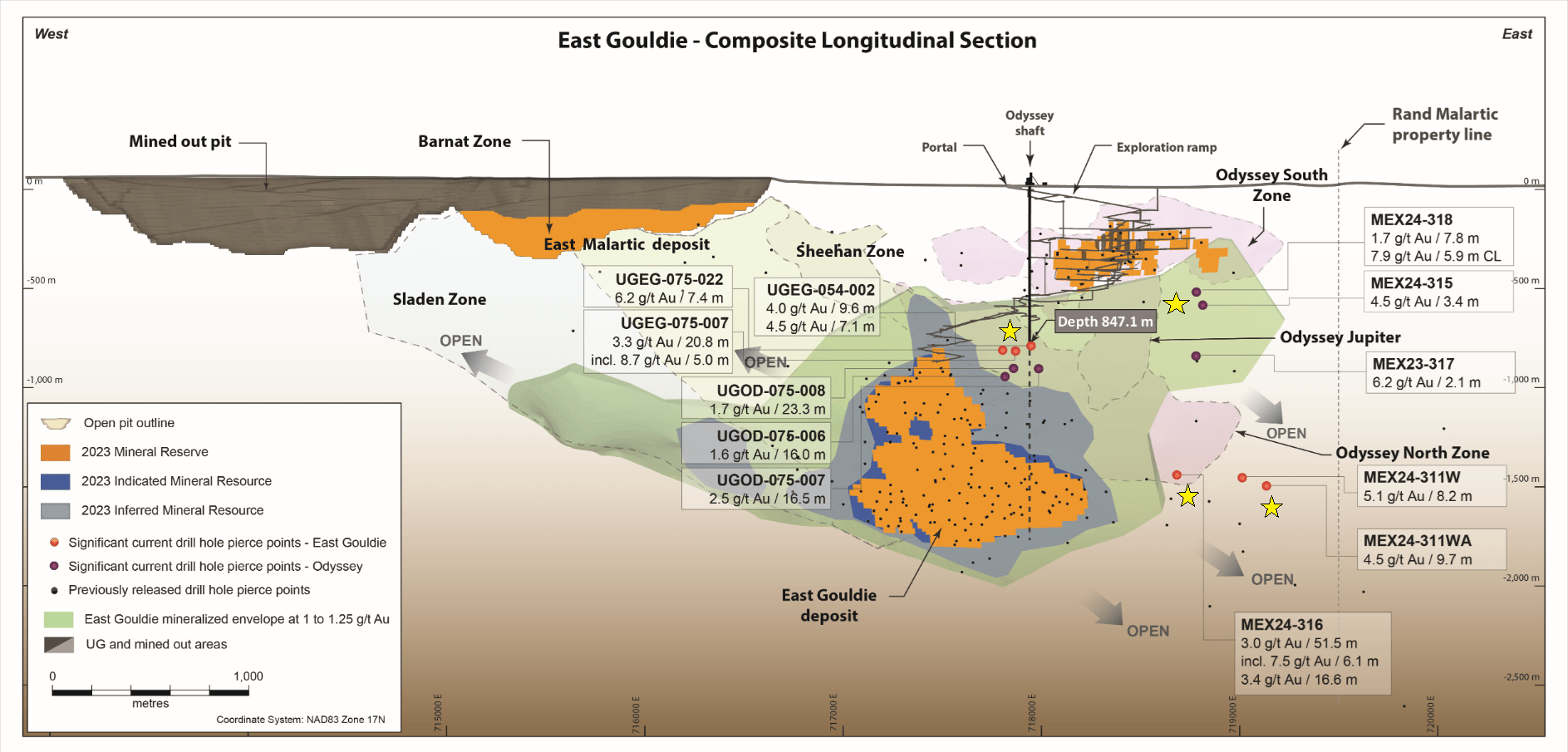

It was another quarter of significant exploration success across the portfolio for one of the sector’s most aggressive drillers, and this continued at its largest operation, Canadian Malartic. During Q3-24 as highlighted by the stars below, Agnico reported additional high-grade mineralization intersected nearly 800 meters east of East Gouldie with a thick intercept of 51.5 meters at 3.0 G/T of gold (1,349 meter depth). This intercept included 6.1 meters at 7.5 G/T of gold and an additional hit of 16.6 meters at 3.4 G/T of gold, all consistent with or better than grades of East Gouldie reserves.

Odyssey & East Gouldie Drill Highlights – Company Website

In terms of high-grade mineralization intersecting east of East Gouldie, Agnico stated the following:

“Drilling into this new portion of the deposit during the first nine months of 2024 has consistently intersected significant gold mineralization, demonstrating the potential to add mineral resources at depth to the east of the main East Gouldie orebody.”

– Agnico Eagle Q2-24 Results.

Elsewhere at Malartic, Agnico continues to hit mid and high-grade intercepts in the upper extension of East Gouldie near the Odyssey shaft, including 20.8 meters at 3.3 G/T of gold and 7.4 meters at 6.2 G/T of gold. It also continues to return impressive intercepts from Odyssey North and South, suggesting additional bonuses in the Odyssey internal zones that can be accessed easily using existing infrastructure.

Overall, this exploration success continues to support a much larger operation at Canadian Malartic longer-term and when combined with a hungry mill (60,000 TPD) that’s expected to be only one-third utilized, there looks to be the opportunity to transform Canadian Malartic into a ~1.0 million ounce operation with the combination of a potential second shaft and ore deliveries from Wasamac, with there still being significant excess capacity to handle lower-grade regional ore and/or third-party ore in the region. Hence, like its Detour Lake Mine, the future here is extremely bright with these two assets having the potential to combine for 2.0 million ounces per annum and be two of the world’s largest gold mines next to Canada, with their distinction even more rare given that they’re in Tier-1 jurisdiction vs. most others in Uzbekistan (Muruntau), Indonesia (Grasberg), Olimpiada (Russia).

Hope Bay

“The core length intercept on those were just spectacular, solid from wall to wall, demonstrating the potential for a significant new thick mineralized area that could potentially host up to a million ounces between 10 grams and 20 grams that could have a very positive impact on future project redevelopment scenarios, considering the high-grade nature compared to the rest of the deposit and the apparent simple geometry of this new zone.”

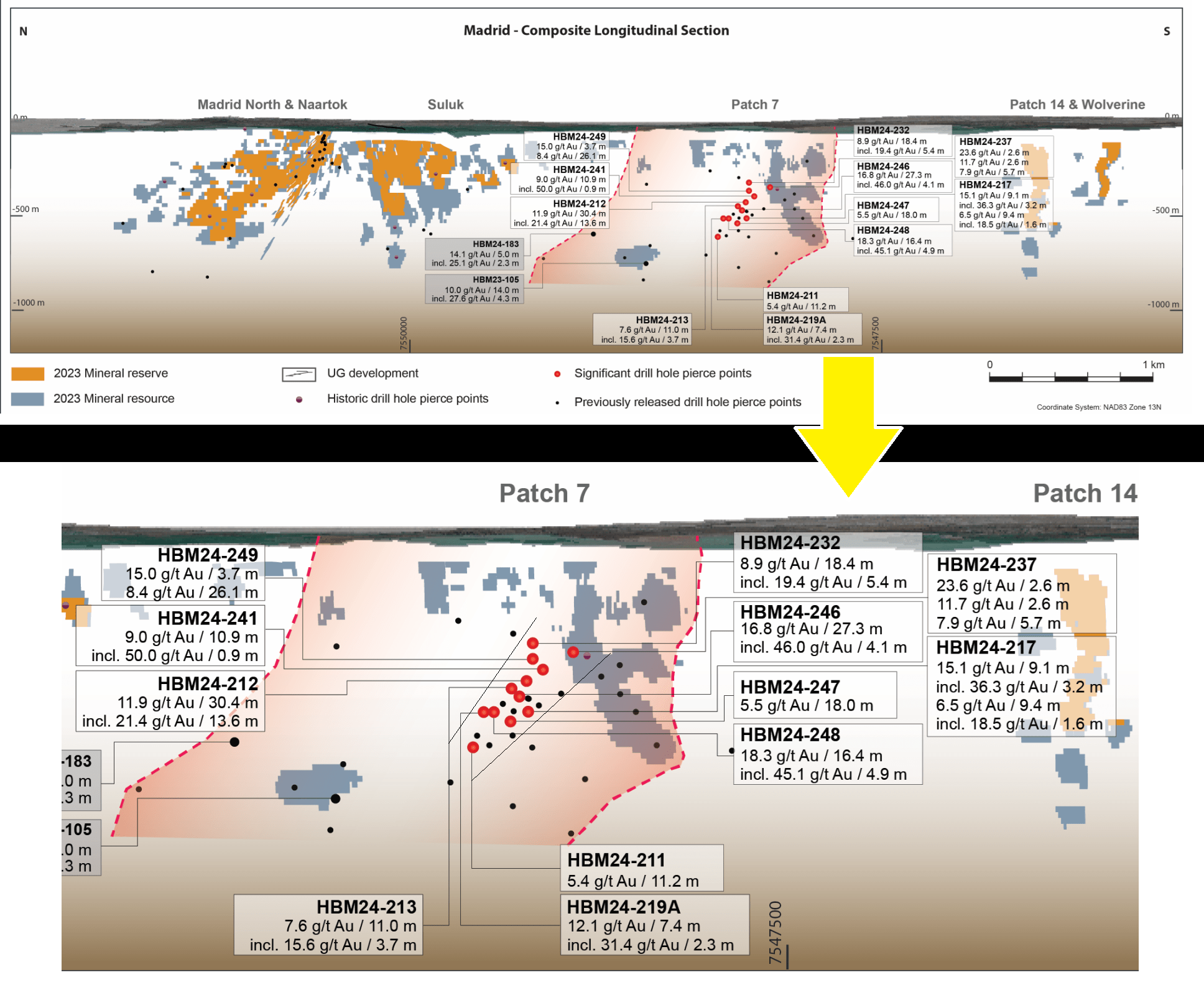

Since that statement in the Q1-24 results, Agnico’s Nunavut exploration team has continued to hit some of the best intercepts in North America from when it comes to grades over 10+ meter true widths, with the most recent intercepts including 16.4 meters at 18.3 G/T of gold (479 meters depth), 27.3 meters at 16.8 G/T of gold (436 meters depth), and 30.4 meters at 11.9 G/T of gold at 394 meters depth, just up-plunge from the extremely high-grade hit of 27.3 meters at 16.8 G/T of gold. Meanwhile, a shallower hole hit 18.4 meters at 8.9 G/T of gold at 289 meters depth. Finally, Agnico noted that drilling into adjacent sub-parallel structures intersected 10.9 meters at 9.0 G/T of gold.

Hope Bay Exploration Success & Zoom in on Patch 7 High-Grade Zone & Continuity – Company Website

It’s important to note that these holes complement an incredible hole released in Q2-24 of 25.8 meters at 17.0 G/T of gold (419 meters depth), a shallower hole with 2.8 meters at 26.7 G/T of gold, and the company has still yet to follow up on other high-grade intercepts to the north and at depth closer to the Suluk orebody. For those unfamiliar, Agnico intersected 14.0 meters at 10.0 G/T of gold in this deeper drilling (including 4.3 meters at 27.6 G/T of gold), as well as 5.0 meters at 14.1 G/T of gold.

Hope Bay Mineralization – TMac Resources

Overall, while the company was certainly successful at Doris in its first couple of years following its TMac acquisition (one of the three deposits at Hope Bay), the real success has come at Madrid which is turning into a monster. And given this success, I would not be surprised to see material growth in resources and reserves over the next two years as drilling continues to fill in this new opportunity between Patch 7 and Suluk (*).

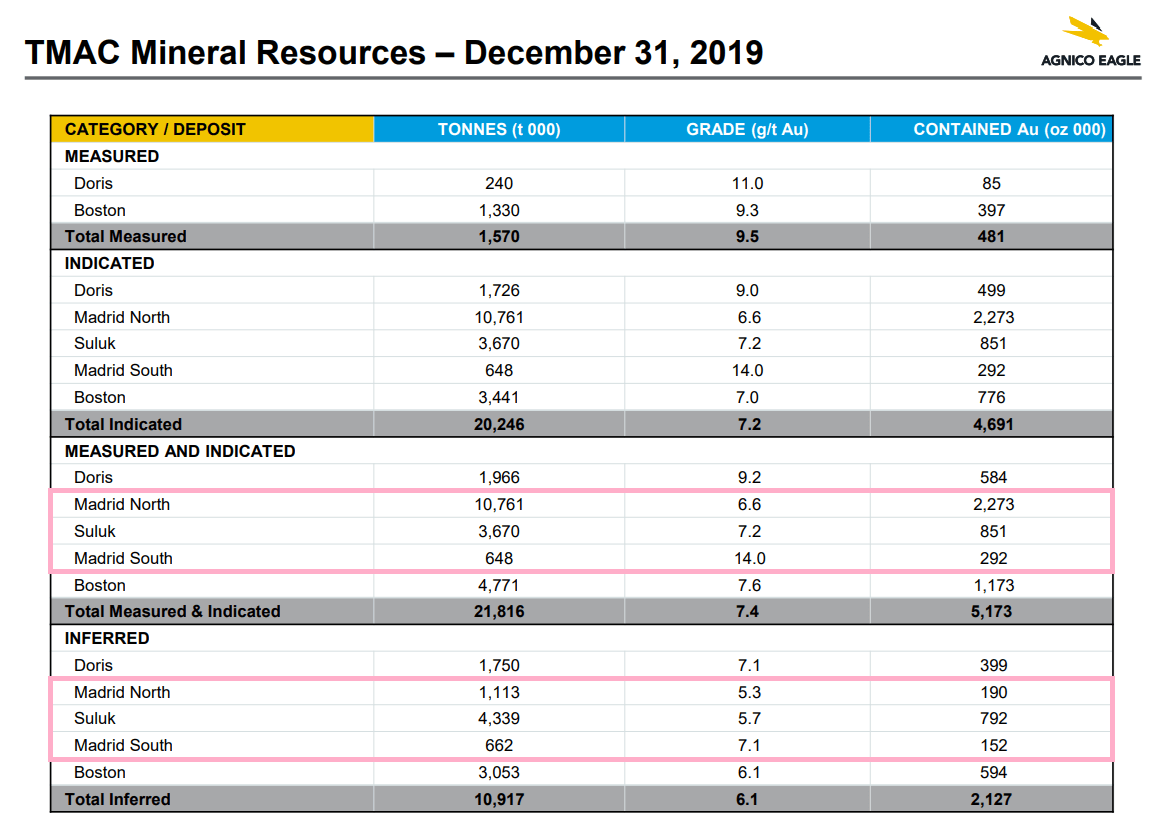

(*) Putting the grades here in perspective, we can see that if Agnico is able to prove up a 1.0+ million ounce resource at 13.0 G/T of gold here (low end of soft exploration target for grades), it would be nearly double the previous average M&I grade (2019) of ~7.0 G/T of gold. (*)

Madrid Grades (Hope Bay) 2019 – Agnico Website, TMac Resources

As for the opportunity here, it’s still early days and lots of dependent on grade and throughput when it chooses to restart Hope Bay, but I wouldn’t be shocked to see peak production at Hope Bay come in closer to 470,000 ounces given the very impressive grades and continuity in this high-grade zone at Patch 7 with the potential to significantly improve feed average feed grades with higher-grade ore from this zone, with Agnico calling Patch 7 a “game-changer” in its Q3-24 call. As it stands, a study should be available within 12 months following material resource growth at Madrid in its year-end results in Q1-25.

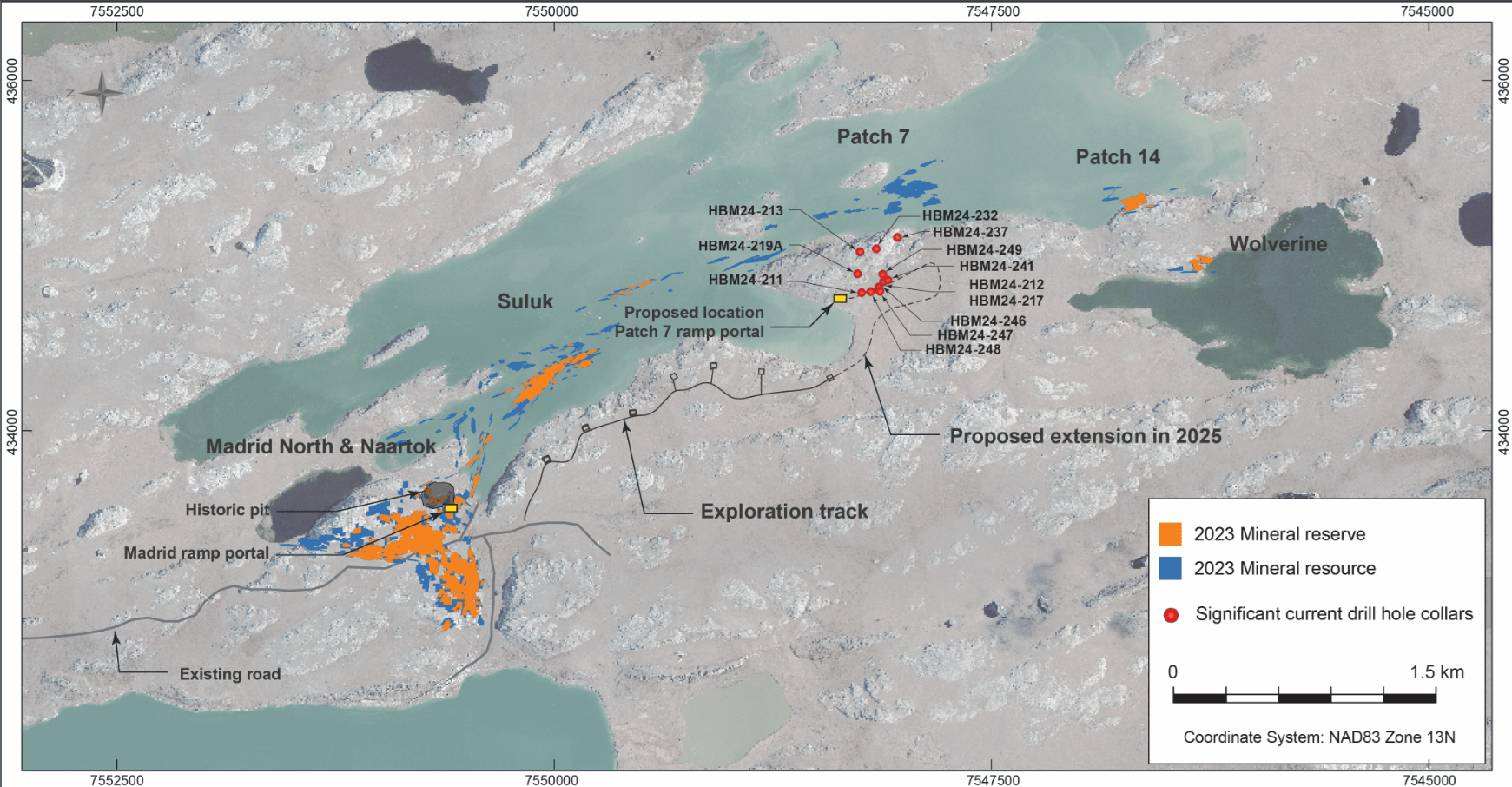

The last highlight from Hope Bay worth noting is that the company plans to drill in Q4-24 this year, which will be helped by a newly constructed 2.3 kilometer long surface exploration track which connects Madrid-Naartok infrastructure to Patch 7. Notably, this provides year-round access to this ultra-high-grade ore body to accelerate drilling and could be used for future development at Patch 7, suggesting investors will be able to look forward to more drill updates in the coming quarters from this high-grade asset.

Madrid Infrastructure & Proposed Extension (Exploration Track) – Company Website

Fosterville

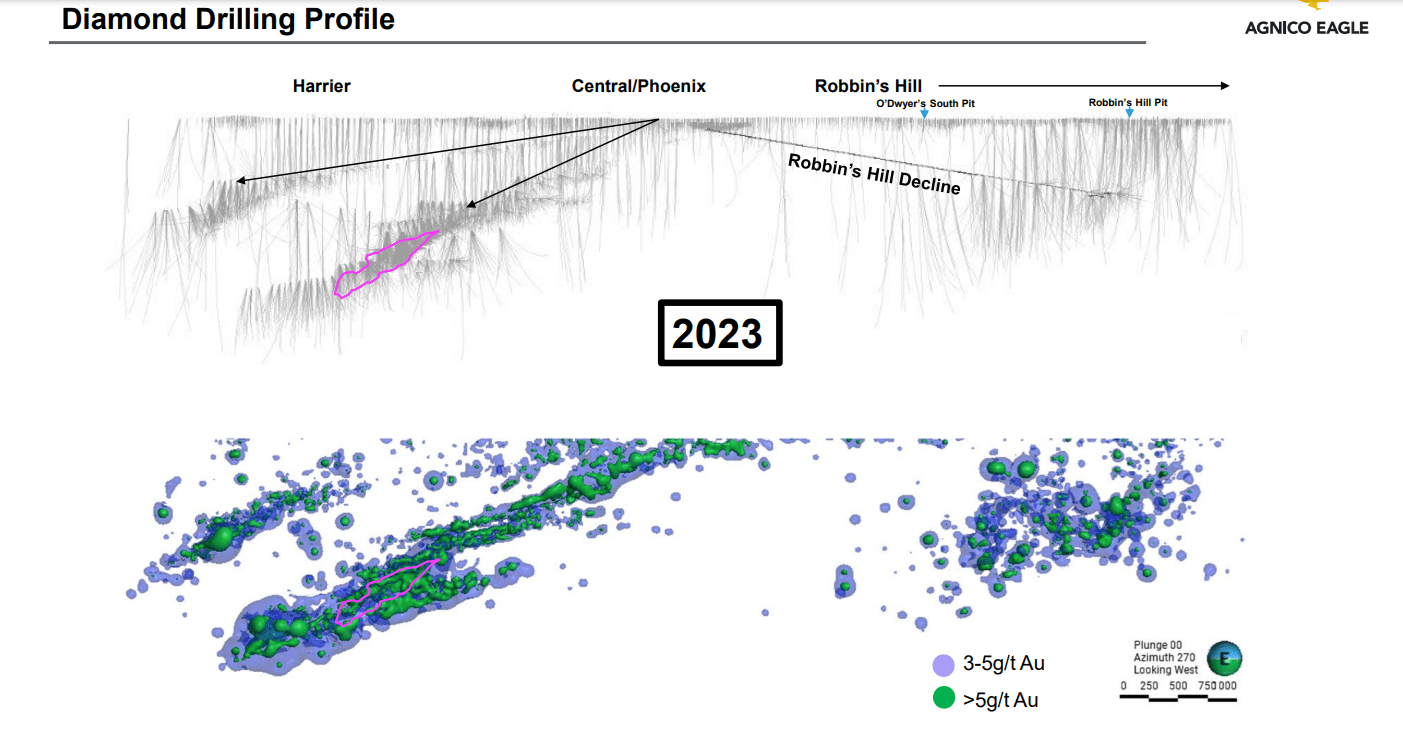

Finally, moving to Fosterville, while Agnico has yet to uncover another Swan, it continues to uncover mid to high-grade mineralization at both Robbin’s Hill and Lower Phoenix. Starting with Robbin’s Hill, Agnico hit 7.7 meters at 5.2 G/T of gold 600 meters from resources and near current infrastructure, potentially adding additional mid-grade mineralization to this rapidly growing orebody. Meanwhile, the company hit another encouraging high-grade intercept at Lower Phoenix in the higher-grade Cardinal structure roughly 100 meters down-plunge from reserves with 5.7 meters at 72.8 G/T of gold.

As for the bigger picture at Fosterville, the future of this asset wasn’t as clear at $1,900/oz gold with a declining grade profile and noise constraints that were impacting mining rates. However, even at a more conservative 6.0 G/T grade profile longer-term vs. the brief period of 30.0+ G/T ore hitting the mill and a higher gold price, 6 G/T ore is now worth ~$480/tonne at $2,500/oz gold (10% below spot) vs. ~$385/tonne when we entered the year near $2,000/oz gold. This is a significant margin relative to year-to-date operating costs of ~$173/tonne at Fosterville and the company continues to work on optimizing this asset.

Fosterville Operations & Drilling + Grade Profile – Company Website

In summary, Fosterville continues to look like it has a bright future as a ~200,000 ounce per annum asset, with it generating consistent cash flow to re-invest across the business and drill regionally and near-mine to hopefully hunt down the next Swan or mini-Swan.

Valuation & Technical Picture

Based on ~502 million shares and a share price of US$88.00, Agnico trades at a market cap of ~$44.2 billion and an enterprise value of ~$44.7 billion. This makes it one of the highest-valued names in the sector despite sitting in the #3 spot for total gold production, but it’s important to consider the company’s incredible pipeline that offers it a path to the 4.0+ million ounce mark from assets already in its portfolio. Just as importantly, most of these are high double-digit IRR opportunities like Detour Underground, Canadian Malartic ‘Fill The Mill,” Hope Bay, and Upper Beaver, and a potential opportunity at San Nicolas (one of the highest-grade VMS deposits globally), and with all of this growth focused on top-tier jurisdictions where it has a competitive advantage from a labor standpoint and strong social support.

Therefore, while Agnico Eagle may be a ~3.4 million ounce producer today, there is room to surpass the 4.0+ million ounce mark and the ability to accomplish this with relatively low risk. In my view, this is a far superior position to some peers that are venturing into more challenging jurisdictions to grow, even if they are chasing similar IRR opportunities. It’s also important to point out that it’s very difficult to put a price on consistency and capital discipline, and in a sector where capital has historically gone to die in past cycles.

Hence, Agnico deserves every ounce of the premium it gets relative to its peer group, and arguably should trade at a higher premium than in past cycles given that it’s never been more desirable to operate in Tier-1 ranked jurisdictions when so many other jurisdictions are killing the proverbial golden goose by rushing to raise royalty rates as soon as commodity prices start moving, nationalizing mines altogether, or extorting producers that have already sunk significant capital with the confidence that they will accede to these terms given their lack of alternatives.

So, how does the valuation look today?

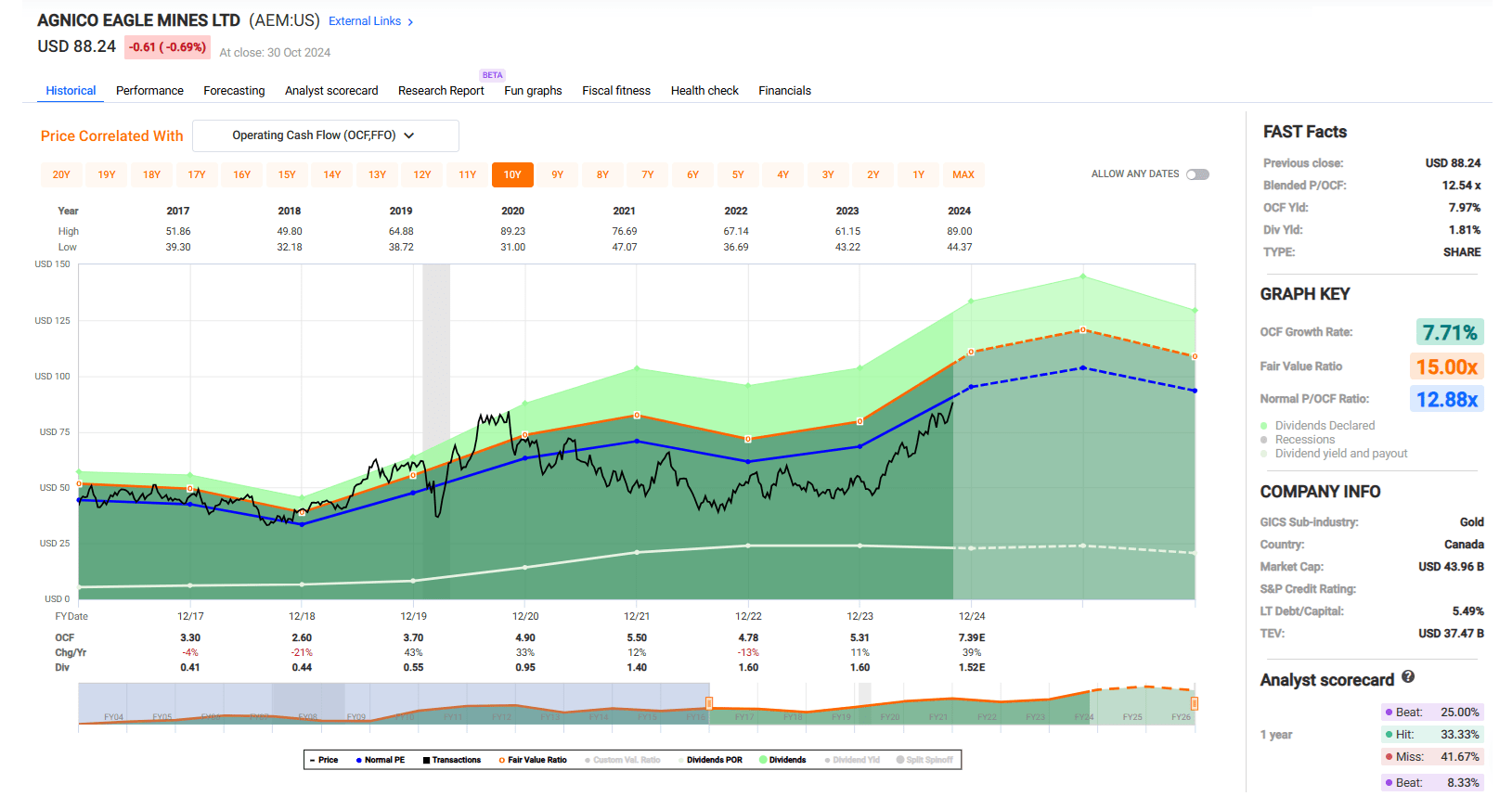

Agnico Eagle Valuation vs. Historical Multiple – FASTGraphs.com

Despite a significant move in the stock off its lows, AEM still trades below its historical multiple of ~13x cash flow (10-year average), trading at ~12x FY2025 cash flow per share estimates even using a more conservative $2,400/oz gold price assumption. Importantly, the company should end the year in a net cash position if gold prices remain above $2,650/oz, meaning it isn’t carrying several billion dollars in net debt that weighs on its valuation like some of its peers. And even using what I believe to be fair multiples of 13.5x forward cash flow and 1.5x P/NAV and a $2,400/oz gold price assumption in 2025, I see an updated fair value for AEM of US$93.00/share.

While this fair value estimate doesn’t point to much upside from current levels, it’s important to note that the sector leader often overshoots fair value in a bull market and this fair value estimate is based on a much lower gold price. In fact, I purposely use lower gold prices to take the commodity price out of the equation when figuring out fair value so that any commodity price upside is a bonus and Agnico’s fair value increases to ~US$100.00/share when factoring in FY2025 cash flow at spot levels and using the same 65/35 weighting to P/NAV vs. P/CF. Plus, as noted previously, Agnico has material growth in its pipeline looking out towards the end of the decade. Hence, we are nowhere near peak production for the company.

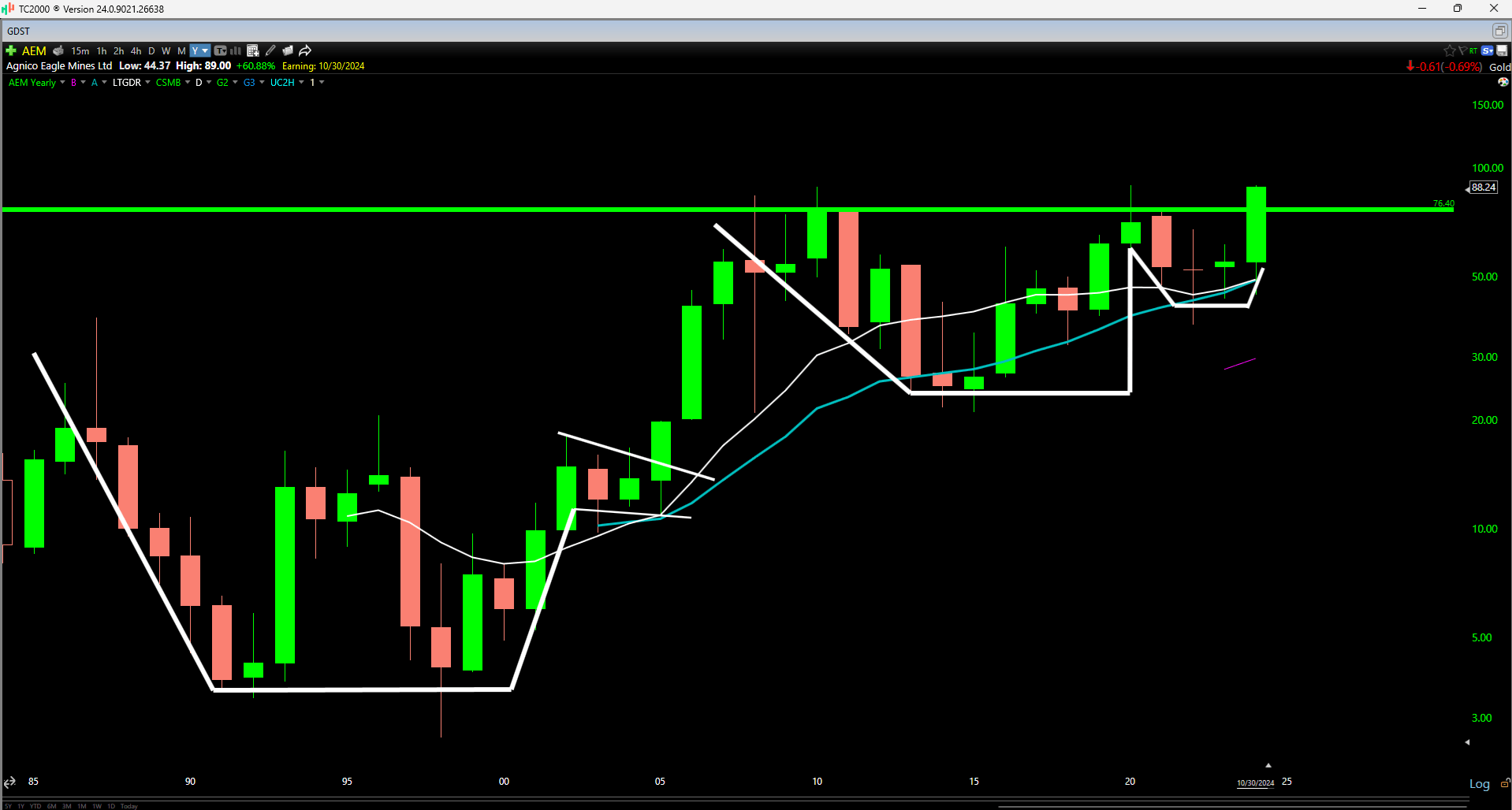

The last point worth noting is that while AEM may have less upside today than where it started the year following this period of outperformance, it continues to sport one of the best-looking technical charts among all large-cap stocks globally. In fact, as the chart below highlights, AEM is working on emerging out of a ~15-year cup and handle base, similar to the one it broke out in the middle of the past bull move in miners in 2005. And while history doesn’t have to repeat itself and this does not mean that Agnico will head higher in a straight line, this breakout is targeting a move to at least ~$120.00/share or 40% upside from current levels.

So, with a reasonable valuation and a very bullish long-term technical setup which is quite similar to the breakout we saw in gold in Q1-24, I continue to believe that any sharp pullbacks in AEM will provide buying opportunities.

AEM Yearly Chart – Worden

Summary

Agnico Eagle has clearly been one of the exceptions among the majors with a multi-year and multi-decade track record of delivering on guidance, growing per share metrics and keeping costs lean. This is certainly helped by its competitive advantage which will only further improve as it increases production even further in the Abitibi region, and it’s why Agnico Eagle continues to be unrivaled from a quality standpoint vs. other producers in the sector.

In fact, while there is no shortage of “show me” stories where it’s always a next quarter promise, Agnico continues to soar above the peer group with its teams on the ground consistently delivering. Just as importantly, its management puts those teams in a great position to be able to deliver by focusing on the safest jurisdictions with considerable geological potential, the highest quality assets overall (development/operating standpoint) and directing capital towards the best opportunities from a risk-adjusted standpoint. This can’t be overstated because even the best employees cannot overcome political instability that derails assets or challenging ore bodies that struggle to run consistently.

For this reason, Agnico Eagle continues to be a staple for any investor looking for a core holding with exposure to precious metals, and it’s unique in the sense that it’s a sleep-well-at-night investment. In fact, if one wakes up to an acquisition by Agnico Eagle, one can be confident that this deal was run through the wringer several times and will be a large net winner given the company’s near-flawless track record when it comes to creating value for shareholders.

Kittila Gold Pour – Company Video

To summarize, with one of the best-looking yearly charts among its large-cap peers (multi-year breakout), one of the best management teams in the commodity space and an outlook for increasing shareholder returns but in a disciplined manner, I continue to see AEM as the #1 name to gain exposure to precious metals and a name worthy of adding to one’s position on any sharp pullbacks.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AEM, AEM:CA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Alluvial Gold Research offers in-depth research on my favorite miners ranked in order to aid in positioning in the most undervalued miners with upcoming catalysts to drive portfolio outperformance. Subscribers also get access to my current portfolios and buy/sell alerts as well as the following:

A Proprietary Sentiment Indicator for gold/silver miners updated weekly not available anywhere else

Exclusive Research on Top Ideas

Top Takeover Targets

Buy/Sell Signals for GDX, SIL & Individual Miners

I have been able to outperform GDX consistently since its peak (180% return since August 2020 peak) with the help of timing models I’ve built & rigid stock selection.