Summary:

- Current penetration represents <2% – huge growth runway.

- Strong direct traffic and organic search and brand awareness.

- Unique community of individuals hosts.

- Long-term stay brings higher margin potential.

ferrantraite/E+ via Getty Images

Airbnb (NASDAQ:ABNB) is the leader in Alternative Accommodations and experiences. I believe their community of individual hosts and strong brand differentiates them from travel peers. The emerging trend of long-term stays would boost Airbnb’s profit margins and expand the entire travel accommodation market size.

Growth Drivers

Huge Underpenetrated Market: Airbnb estimates its current total addressable market to be $3.4 trillion, including $1.8 trillion in short-term stays, $210 billion in long-term stays, and $1.4 trillion in experiences. Coupled with a notably underpenetrated market size, the global travel market is growing at an above GDP rate. Airbnb’s current market penetration represents less than 2% of the share. As such, there is a huge runway for Airbnb’s growth over the next decade.

In terms of competition, most Online Travel Agencies (OTA) provide traditional hotel accommodation (Marriott, Hilton, Accor, Wyndham, and InterContinental, for example). These OTAs are not the real competitors for Airbnb. Instead, Booking.com (BKNG) is expanding its traditional hotel business into the alternative accommodation industry. Expedia (EXPE) entered the alternative accommodation market via the acquisition of VRBO in December 2015. However, Airbnb has the first-mover advantage with a very strong brand. I believe Airbnb’s technology and supplies are superior to their peers, and it is hard for Expedia and Booking.com to compete against Airbnb in the alternative accommodations space.

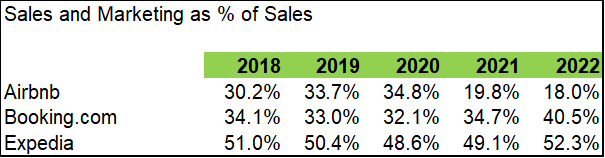

Direct Traffic and Organic Search: One of the main expenses for Online Travel Agencies is sales and marketing. They have to spend billions of dollars on Google, Facebook, and other social media platforms to attract traffic.

The table below shows the sales and marketing expenses as a percentage of sales. Both Booking.com and Expedia spend almost half of their sales on sales and marketing. According to Airbnb’s disclosure, 80% of their website traffic comes from direct and organic search. In contrast, Booking.com and Expedia only have 60% direct traffic. In other words, Airbnb has the highest brand awareness among these travelers. With a high ratio of direct traffic and organic search, Airbnb spends much less than its peers.

Corporates Annual Reports

In Q1 FY23’s earning call, Airbnb indicated their sales and marketing expense as percentage of sales would remain the same in FY23.

In late 2019, Airbnb’s costs were rising, and growth was slowing. They spent a huge amount of money on performance marketing, which was basically selling their products as a commodity. Their product was looking less different from their competitors. When the COVID occurred, they lost 80% of sales in eight weeks, and they shut down all marketing spending. Interestingly, when the travel market rebounded, Airbnb’s business came back to almost the same level as before, with much less marketing expenses. Currently, they spend much less on performance marketing, and most of their expenses are focused on their products/services. They have had 600,000 articles about Airbnb. These efforts have put Airbnb in a much better shape today.

Unique community of individuals Hosts: 90% of Airbnb’s hosts are individuals. Airbnb can capitalize on the personal experience provided by these unique individual hosts, as opposed to a standard hotel service. Customers can find unique properties, differentiated amenities, as well as local insights from these individual hosts.

Airbnb is putting in a lot of effort into the experience market. In Q4 FY22’s earnings call, Airbnb expressed that they were beginning to ramp up their Airbnb Experience business and expect to launch more products/services over the coming years. In my opinion, Airbnb Experience may not bring notable direct sales to Airbnb, but it would enhance the stickiness and loyalty of Airbnb’s customers. Airbnb Experience would make the Airbnb platform unique and boost their sales indirectly.

Furthermore, Airbnb Experience could become more relevant with AI technology. In Q1 FY23’s earnings call, Airbnb disclosed that they are building AI into their products. Airbnb is working with OpenAI ChatGPT, and Airbnb will embed ChatGPT into their app. The AI-powered product will be launched next year.

Leveraging AI technology, Airbnb can make their Airbnb Experience and accommodation recommendations more relevant to any consumer. To put it another way, Airbnb would know your preferences for travel destinations and accommodations before you start searching for anything.

Long-term Stay: As disclosed, 20% of Airbnb’s gross bookings are long-term stays currently. Long-term stays are the fastest-growing segment in terms of trip length. The pandemic also accelerated some inevitable growth for long-term stays.

Long-term stays mean higher margins for both hosts and Airbnb. In Q1 FY23’s earnings call, Airbnb indicated that long-term stays would be one of the biggest growth areas over the next five years. Airbnb made over a dozen upgrades to long-term stays based on affordability, and they also have new discounting tools for hosts on weekly and monthly stays. Airbnb expects more hosts to exclusively list long-term stays with Airbnb.

In addition, 62% of Airbnb’s guests are under 34 years old, and Airbnb is focusing on the next generation of travelers. These young customers are more likely to use Airbnb as the platform for long-term stays. The key thing to remember is that more long-term stays mean higher margins for Airbnb.

Near-term Headwinds

Due to high inflation, it is reasonable to assume that consumers need to cut back on some discretionary spending, including travel. Airbnb’s sales growth and booking value growth have been slowing down in recent quarters.

Airbnb Quarterly Results

Airbnb indicated that, in the current macroeconomic environment, consumers are looking for affordable ways to travel on Airbnb. Airbnb is adding more affordable accommodations to their platform. The average price of Airbnb rooms is only $67 per night.

Before the pandemic, 80% of Airbnb’s sales were coming from either cross-border or urban accommodations. The cross-border business would contribute more sales to Airbnb than other types of travel. The cross-border traveling could be very weak if high inflation persists. Despite this, the global travel market had been growing fast in the past, and I expect the growth will continue in the future.

Financials and Valuation

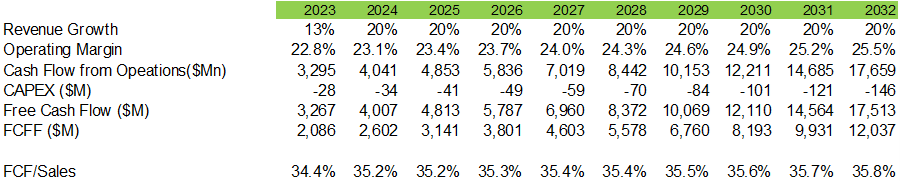

We are using a two-stage DCF model to estimate Airbnb’s fair value. In the model, we assume 20% of normalized sales growth rate, which we believe is quite conservative.

We assume they can expand their operating margin by 30bps annually and will reach 25.5% in FY32.

DCF Model, Author’s Calculation

Their free cash flow conversion was quite healthy in the past, and we assume they will deliver 35.8% in FY32.

In addition, we use 10% of WACC, and 15% of non-GAAP tax rate in the model.

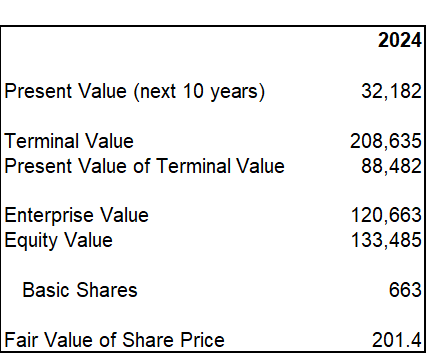

The present value of Free Cash Flow to the Firm (FCFF) over the next 10 years is estimated to be $32 billion, and the present value of terminal value is $88 billion. As such, the total enterprise value is estimated to be $120 billion. Adjusting gross debt and cash balance, the fair value of the stock price is $201, according to our estimate.

DCF Model-Author’s Calculation

Conclusion

All things considered, the huge underpenetrated market, strong brand awareness, and growing trend of long-term stays, in my opinion, will provide Airbnb with a huge runway for growth over the next decade. Their competitors are way behind them, and Airbnb would be the best player for the alternative accommodation service provider. In my view, the current stock price is significantly undervalued, and we encourage investors to buy during the weakness.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ABNB either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.