Summary:

- Airbnb has been sold down after management announced that marketing spend would be brought forward from 2H23 to 1H23.

- The fundamentals of the business and growth outlook are unchanged, providing an attractive opportunity for the long term investor.

- Travel demand is remaining resilient and is forecast to grow beyond 2022 levels.

- Valuation of $121.56 means ABNB is attractively valued compared to the current share price.

Jeremy Poland

Airbnb’s weak 2Q22 guidance provides the patient investor a great opportunity to buy a great company at a reasonable price. Airbnb has all the characteristics of a quality company including high margins, high returns on capital, a fortress balance sheet, a founder CEO, and solid long-term growth prospects. The reaction from the result demonstrates clearly Wall Street’s short-termism, so an investor with even a medium-term outlook, who is willing to look past the 2Q23 period to 4Q23, should be rewarded.

In this article, I will review the recent 1Q23 earnings and detail why it wasn’t as bad as the market thought. I will also assess travel demand data for 2023 with a view to expound the short-term risk that a recession may pose to travel demand globally. And I will look at how Airbnb plans to continue growing the business because this is what will underpin the valuation going forward.

1Q23 Result Was Strong But Guidance Weak

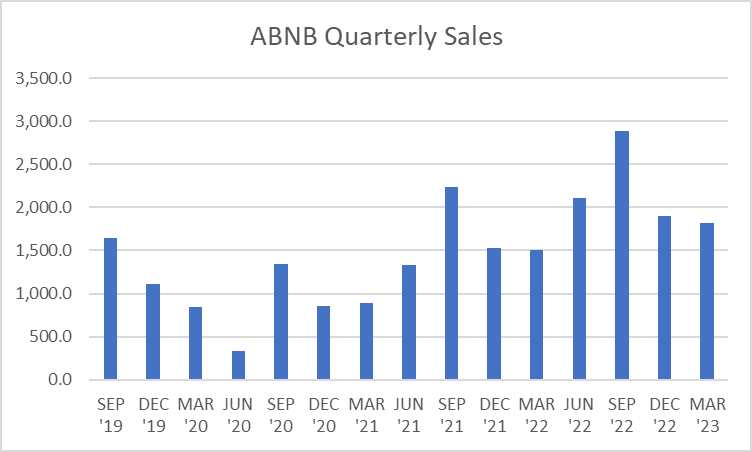

Airbnb is a very seasonal business. You cannot compare a third quarter with the first quarter of any given year because they look completely different. The simple reason is because people tend to go on holidays through the spring and summer (Q2 and Q3), and significantly less through the fall and winter (Q1 and Q4). This is demonstrated on the following chart. As a reminder, revenue is recognised when the guest checks in to their accommodation, but payment is taken at the time of booking.

Author’s analysis usuing data from FactSet

Revenue grew 20% in 1Q23 compared to 1Q22 to $1.8 billion. This was derived from a gross booking value of $20.4 billion for a take rate of 8.8%. Adjusted EBITDA was $262 million, up 14%, but all this does is strip out stock-based comp, which is a genuine expense, so excluding that EBITDA was close to breakeven.

However, net income was $117 million, up from a loss of $19 million in 1Q22. In constant currency terms, net income would have been even stronger at $156 million. The reason for the strong net income compared to EBITDA was the incredible amount of interest ABNB earnt on its enormous and growing cash pile.

ABNB reported cash, cash equivalents, and short-term investments of ~$10.6 billion (and $1.8 billion in debt). Add to this $7.76 billion in restricted cash held for customers and you have enormous interest-earning potential. Of course, there is an offsetting liability to this $7.76 billion of restricted cash, but the interest it earns is certainly material. This $10.6 billion provides ABNB with huge optionality. They have earmarked $2.5 billion for further buybacks after recently completing a $2 billion buyback program. If the share price remains attractive, I could see this being extended.

ABNB is also hugely cash generative, producing $1.6 billion of operating cash flow and $1.6 billion in free cash flow, with a mere $6 million being spent on capital expenditures. Indeed, in the trailing 12 months ABNB only spent $25 million on capex because all of their product development costs are expensed. Not a cent of it is capitalised. This makes the financial results even more impressive (and keeps the balance sheet tidy too).

Travel Spending Remains Strong Globally

With a possible recession on the horizon, a concern might be that ABNB could come under some strain if discretionary spending declines. Especially after 2022 being the year of “revenge travel”, one might think that 2023 might be a quieter year for travel. This does not appear to be the case. At least not yet. I want to share some data that overwhelmingly points towards strength in travel in 2023.

According to the US Travel Association, March 2023 travel spending was 4% higher than March 2019, albeit slightly below the February 2023 level. In addition, although still 25% below March 2019 levels, March 2023 was the biggest month for overseas arrivals since the onset of the pandemic. This is in line with forecasts by the Economist Intelligence Unit, which expects “Global tourism arrivals [to] rise by 30% in 2023, following 60% growth in 2022, but they will still not return to pre-pandemic levels.”

A survey reported by Forbes Advisor showed that 87% of Americans surveyed either plan to travel more (49%) in 2023 than in 2022 or as the same amount (36%). In Australia, a survey conducted by Luxury Escapes reported that 9 in 10 respondents planned either domestic or international travel in 2023.

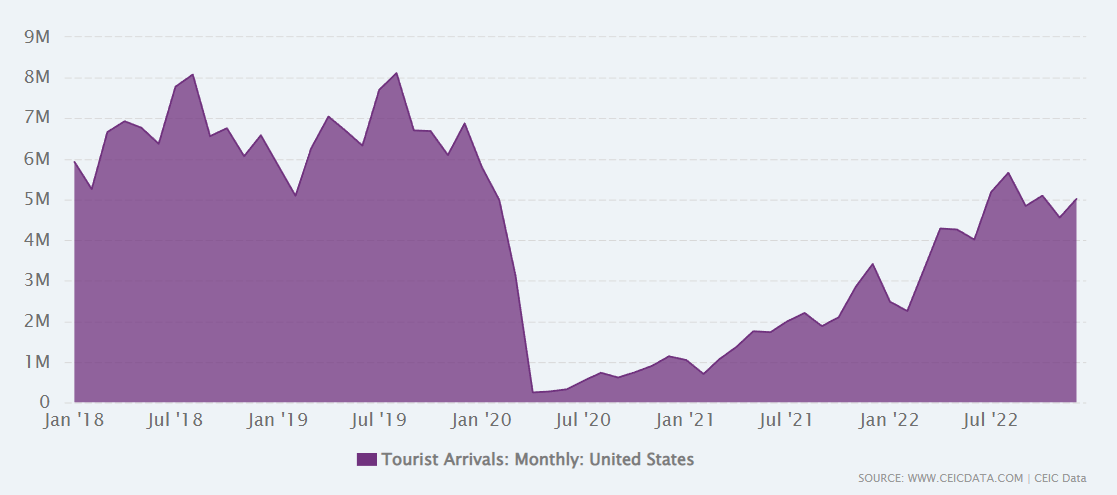

For the US, air passenger arrival data is only current up to December 2022, but the trend is strong and points to continued recovery.

CEIC

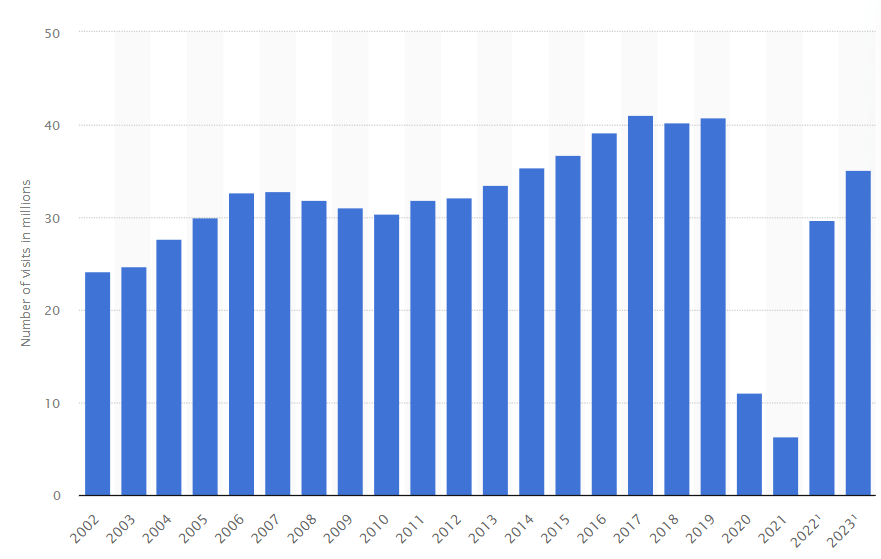

Statista forecasts arrivals in the UK to grow in 2023 on 2022.

Statista

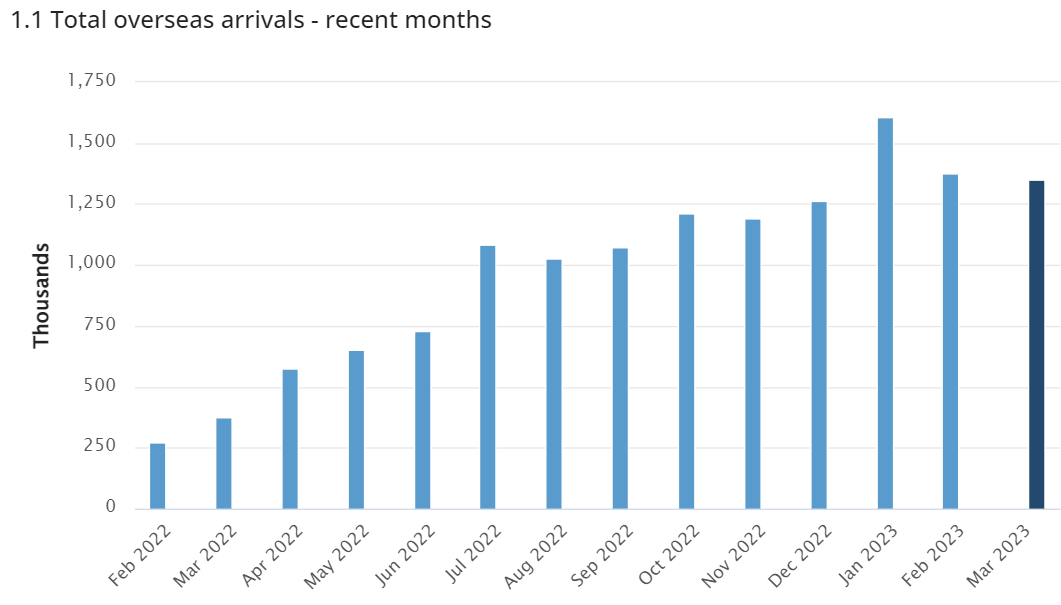

The Australian Bureau of Statistics on the other hand has more current data showing that arrivals in March 2023 were as strong as February, and departures were stronger. Though it should go without saying that Australia is a much smaller market both in terms of global travel and on the Airbnb platform, making up less than 10% of bookings on Airbnb.

Australian Bureau of Statistics

Looking at Europe, which is a key geography for Airbnb given the level of cross-border travel within the bloc as well as it being a popular destination for international travellers. The European Travel Commission is expecting 2023 to be a bigger year for European travel than 2022, “despite global pressures such as high inflation, the war in Ukraine and consequent energy crisis, and the looming economic recession“. Further “international travel to Europe is forecast to reach pre-pandemic levels in 2025“. This will be boosted by the opening of Asia-Pacific countries, which opened later than many in the northern hemisphere.

This is especially relevant because the Asia-Pacific was flagged as a key focus for ABNB by CEO Brian Chesky on the 1Q23 call, as the COVID rebound was delayed there compared to the northern hemisphere, and believe it will be the fastest-growing region in the world in the next 5 years.

Considering the two above quotes from the ETC, even if travel demand falls in the short term, there is still some way to go until the industry returns to pre-pandemic levels, which is all upside for a business like ABNB.

Recent Results from ABNB Peers Also Strong

Recent results in the travel space seem to corroborate the above data. In their recent 2Q23 result release, Visa (V) reported cross-border travel payment growth was 17.5% (excluding China and Russia) or 32% if you exclude cross-border European travel.

Booking Holdings (BKNG) showed even stronger data, reporting gross booking value increased by 44% in the 1Q22 on the prior corresponding period (52% in constant currency). Further, the company expects gross booking volume growth to be in the “low teens” (per the 4Q22 conference call). It seemed like they were tempted to upgrade this in the most recent call but are waiting to see how the next few months pan out first.

Expedia (EXPE) reported a 20% increase in gross bookings, making 1Q23 a record first quarter. Tripadvisor (TRIP) doesn’t report gross booking value for the group, but as a proxy, revenue grew 42% over the prior corresponding period.

Marriott International (MAR) reported revenue growth of 34% but more importantly, their CEO also made the following comment in the press release, which I will quote in full:

While the global economic picture is uncertain, demand remains strong, and we are not seeing signs of a slowdown. With the faster-than-expected recovery in international markets and continued solid booking trends globally to date in the second quarter, we are raising our RevPAR guidance for the full year.

– Tony Capuano, MAR President and CEO, 1Q23 conference call

Hyatt (H) reported in their 1Q23 result that revenue was 24% ahead of 1Q19 levels, with leisure demand “showed durability” and business travel in March reaching 92% of March 2019 levels.

A key result actually came from the Australian Securities Exchange, with microcap travel agent Helloworld (HLO) reporting very strong revenue and TTV Growth off a depressed prior corresponding period, but increased their guidance for the full year (ending June 2023). In doing so, the company made the following comments:

- Leisure travel demand continues to hold up strongly despite challenging economic conditions;

- Demand for international and domestic travel continues to improve with a trend towards longer trips and longer lead times to overcome global supply constraints;

While not a huge contributor globally, these comments are reflective of the trends discussed all throughout this article.

All of this suggests that travel demand is alive and well. Storm clouds are congregating over the global economy but the travel industry hasn’t seemed to notice, as the rebound to pre-pandemic levels, funded by savings and stimulus, looks to outweigh the threat of a downturn.

This is very positive for ABNB, who has established themselves as a premier player in the online accommodation booking industry. The risk remains that competitors such as BKNG add more private listings to their platform, but at present ABNB has the brand name, the image, and the focus to provide the best experience to both hosts and guests, which is likely to lead to growth in properties and increasing numbers of nights stayed.

Airbnb’s Growth Drivers

Importantly, on top of the above trends the travel industry appears to be maintaining, Airbnb has its own drivers that should bring about growth over the next few years. I think they are worth touching on because one of the major risks with the business is the threat of competition with large players such as BKNG, TRIP, or EXP increasing their presence in short-term peer-to-peer holiday rentals. The following initiatives should help to drive growth at Airbnb:

-

Airbnb has relaunched and revamped Airbnb Rooms, which should encourage more hosts to offer a spare room and bring guests to the platform that are seeking a lower price point.

-

Dusting off the pre-COVID international expansion strategy, which has already seen great success in Brazil and Germany. Asia Pacific and Latin America are next, as these are hugely underpenetrated markets for ABNB.

-

A focus on innovation that is improving the user experience for hosts and guests in ways that are hard to replicate. Recent introductions such as the OMG! Category or AirCover should improve retention and attract hosts and guests. ABNB is also relentlessly customer-centric (and that is my description, not theirs!). This is evident in their recent May release with over 50 product improvements that could only have come from customer feedback.

Outlook

ABNB management provided some guidance on the conference call which was for revenue to be in a range of $2.35-$2.45 billion (in line with consensus of $2.4 billion) and Adjusted EBITDA to be in line with 2Q22 (implying about $711 million). This was not well received by the market and was the reason for the sell-off. Revenue was about in line with expectations (according to FactSet) but did not like the lower EBITDA expectation, even if temporary.

Adjusted EBITDA consensus was around $835 million prior to the release, with the difference largely being a result of the marketing spend that the company is bringing forward from the second half into the first half to accelerate the initiatives discussed above. They quantified this as 4% of revenue, which is approximately $95 million.

Management was clear that this is a pull forward not a blowout and they are budgeting for marketing spend (and thus Adjusted EBITDA margin) to be constant on a full-year basis. In my view, this is not an issue, especially if it has the potential to accelerate growth.

Valuation

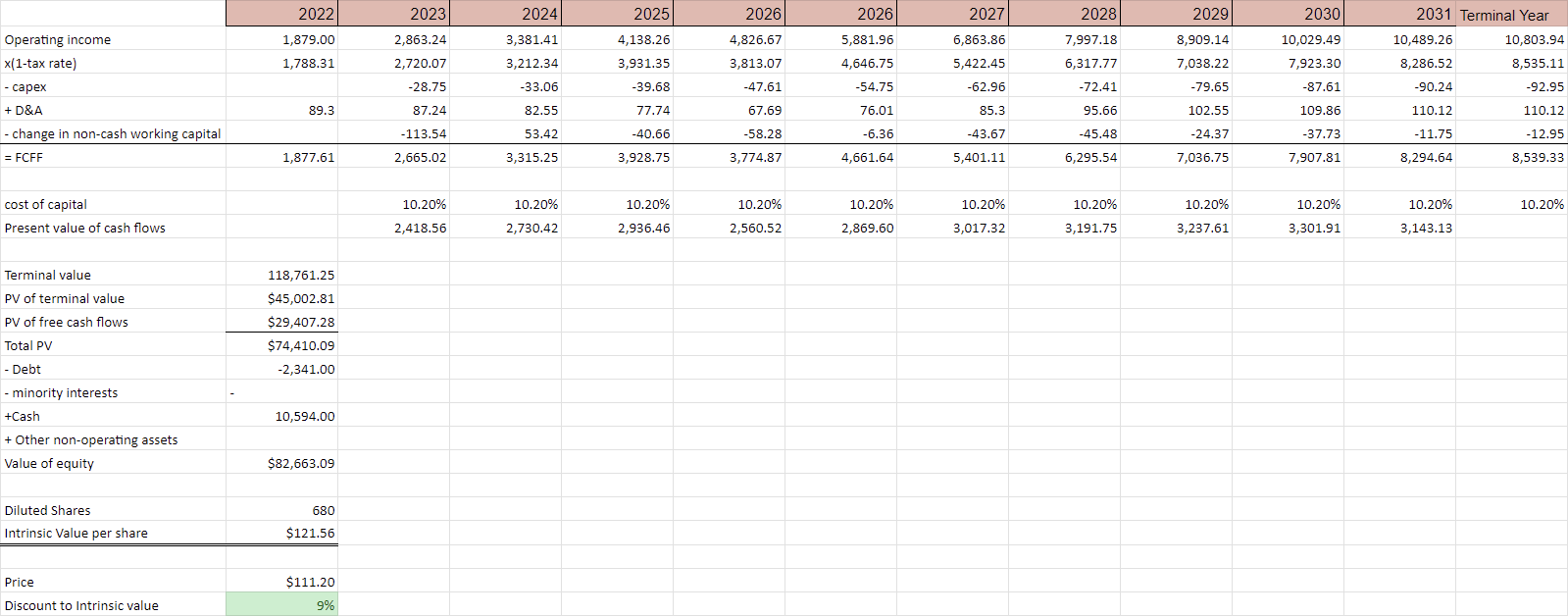

Best of all, ABNB seems reasonably valued. I am using a 10-year DCF with the following assumptions:

-

14% revenue CAGR and 16% FCFF CAGR for 10 years.

-

Levered beta of 1.2 using peer set average, risk-free rate of 10% using average long-term bond rates, and equity risk premium of 5.3% per Damodaran’s calculation, which gives a WACC of 10.2%.

-

Cost of debt of 1%, but a very small component of capital structure.

-

Terminal Growth rate of 3.0%

The below image shows a simplified free cash flow to the firm model out to 2033.

Author’s Analysis using data from FactSet

The above assumptions produce a valuation of $121.56, which provides a nice little margin of safety compared to the current share price ($111.20 at time of writing).

Conclusion

Airbnb is attractively placed in the travel industry to benefit from continued recovery from the COVID-19 pandemic. It has the cash to continue investing in its product and marketing, and has a proven strategy to increase their reach in underpenetrated markets. While a recession may be coming, travel is proving to be somewhat resilient and Airbnb is primed to benefit. Long term investors should be taking the opportunity that Wall Street’s short termism is providing. Airbnb is a buy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ABNB either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.