Summary:

- Altria Group stock has performed reasonably well recently.

- Altria needs to execute its smokeless transition well to lift its well-battered valuation further.

- Structural headwinds on its legacy tobacco segment are likely priced into its attractive valuation.

- Income investors should also find the stock’s almost 9% dividend yield attractive.

- I argue why continued pessimism in MO is unwarranted, as its price action is also increasingly bullish.

FotografiaBasica

Altria Needs To Execute Its Smokeless Transition Well

Altria Group’s (NYSE:MO) stock has performed reasonably well since my previous bullish article in March 2024. I kept my Buy rating, as I assessed a less hawkish Fed should provide more robust valuation support. As a result, even though Altria’s Q1 earnings release saw a net revenue decline of 2.5%, investors weren’t unduly concerned. Furthermore, Altria reaffirmed its full-year guidance, indicating Wall Street was too pessimistic. Altria underscored a potentially more robust second half, suggesting a growth inflection is in the works.

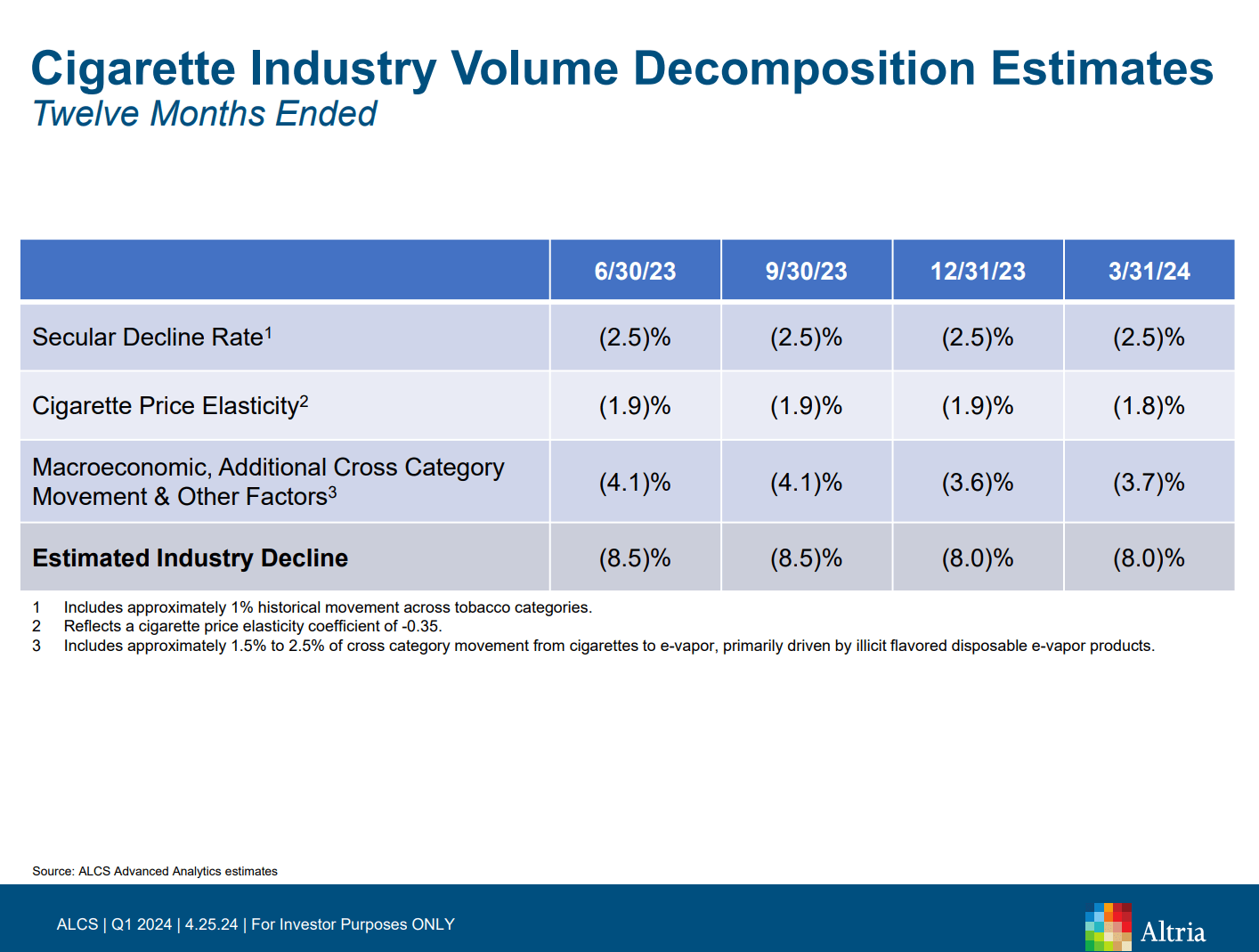

Cigarette industry volume decomposition estimates (Altria filings)

As a reminder, Altria’s Q1 earnings release in late April highlighted the challenges facing the US tobacco leader. It’s mired in a secular declining tobacco industry, with revenue exposure concentrated in the US market.

Furthermore, Altria’s premium positioning has also been affected by macroeconomic headwinds that impact consumer spending. In addition, even lower-income customers have not been spared, as they faced increasing pressures attributed to “inflation, debt, and high interest rates.”

Consequently, given these challenges, I assess that execution risks of a second-half growth inflection cannot be taken for granted. I’ve also assessed substantial uncertainties surrounding the timing and extent of the Fed’s interest rate cuts. Therefore, the market will likely remain cautious about a steeper valuation re-rating in MO stock.

Altria Must Contend With More Intense Competition

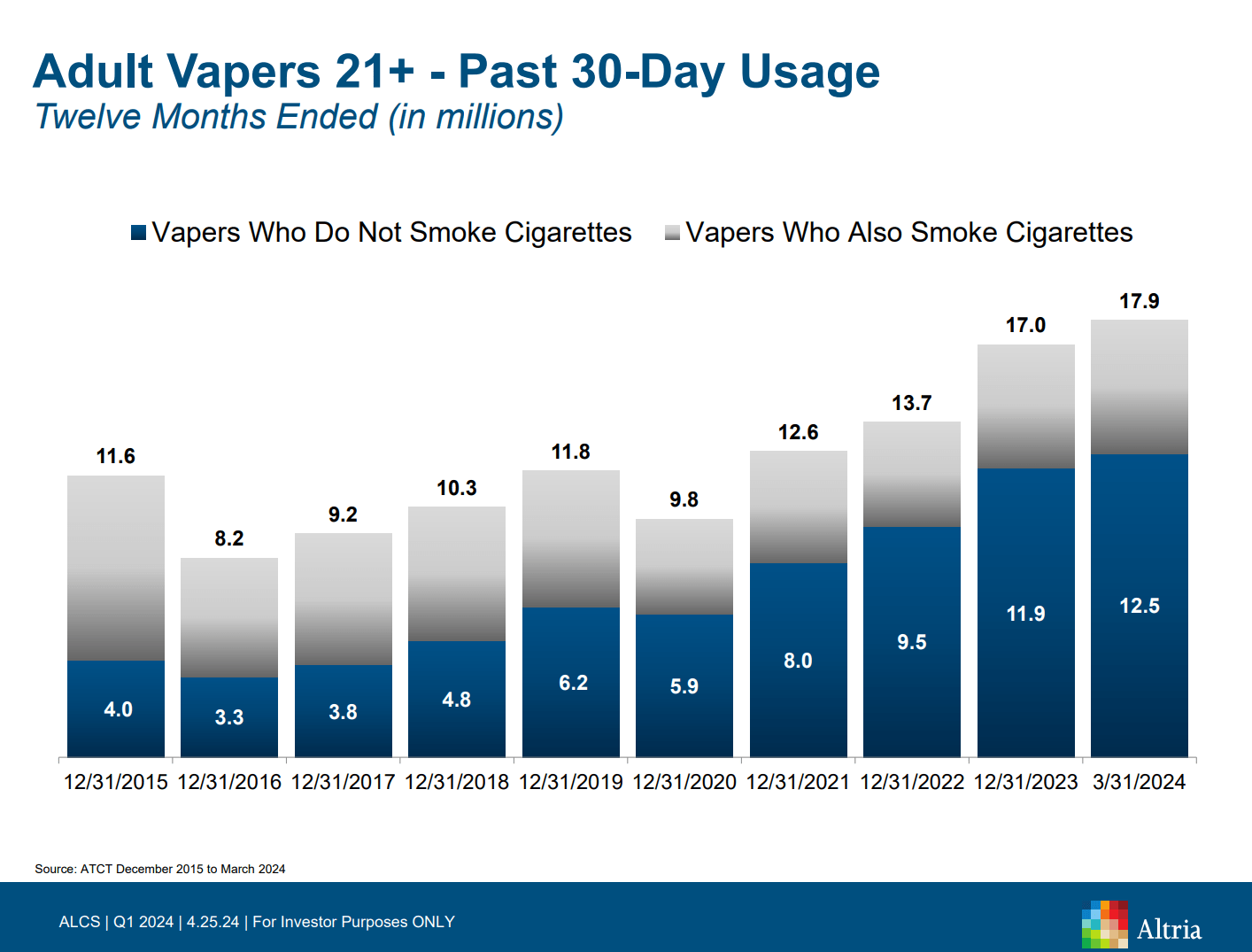

Adult vapers past 30-day usage metrics (Altria filings)

Therefore, the market needs Altria to demonstrate better execution in the smokeless segments as investors evaluate MO’s ability to transition its legacy business. While the vaping trend seems to favor Altria, the company still needs to contend with illegal flavored vaping products from China. Accordingly, while the market has expanded quickly, these illicit products “account for half of the market share.” As a result, I’m not surprised that Altria management reiterated its call for the US FDA to take more decisive enforcement actions in its crackdown.

Interestingly, Altria filed a “supplemental Premarket Tobacco Product Application” in its bid to “commercialize and market the NJOY ACE 2.0 device.” Altria believes the Bluetooth-enabled safeguards on the device will help “prevent underage use.” Consequently, Altria aims to assure regulatory concerns about underage use “while providing flavored options for adult smokers and vapers.” Hence, it could help Altria achieve stronger competitiveness against its illicit-flavored peers in the market, helping to improve confidence in Altria’s smokeless transition opportunities.

Notwithstanding my optimism, I still see significant uncertainties in Altria’s long-term smokeless thesis. Philip Morris’ (PM) return with IQOS (heated tobacco) to the US market could intensify competition against Altria. PM has faced supply challenges with its Zyn oral nicotine pouches, which have remained in high demand. Therefore, it has led to a near-term market share erosion, although the impact could be temporary. As a result, I believe the relative success of PM’s smokeless execution could affect a more robust valuation re-rating of MO stock.

MO Stock: Challenges Likely Priced In

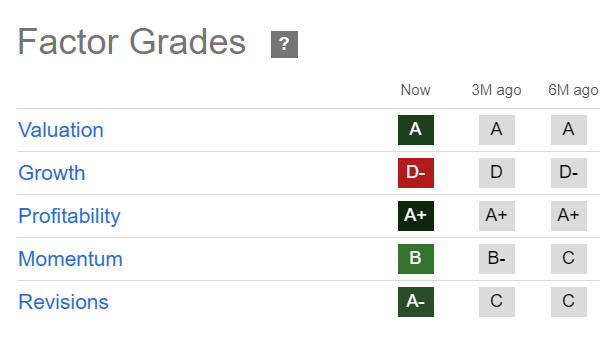

MO Quant Grades (Seeking Alpha)

However, the market isn’t dumb. MO is assigned an “A” valuation grade. Therefore, the market has likely reflected significant uncertainties on Altria’s transition thesis.

MO’s forward adjusted P/E of 8.7x is well below its sector median of 17x, indicating a discount of almost 50%. However, when adjusted for MO’s growth prospects, MO is valued at a forward adjusted PEG ratio of 2.3, at a slight premium over its sector median of 2.2.

Therefore, it’s arguable that unless Altria demonstrates more convincing execution in its smokeless transition, the market will likely remain cautious. Despite that, MO’s forward dividend yield of almost 9% should provide substantial valuation support. Furthermore, Altria’s accelerated repurchase program underscores management’s confidence in MO’s relative undervaluation. As a result, MO’s improved buying sentiment (“B” momentum grade) suggest astute buyers have likely been accumulating.

Is MO Stock A Buy, Sell, Or Hold?

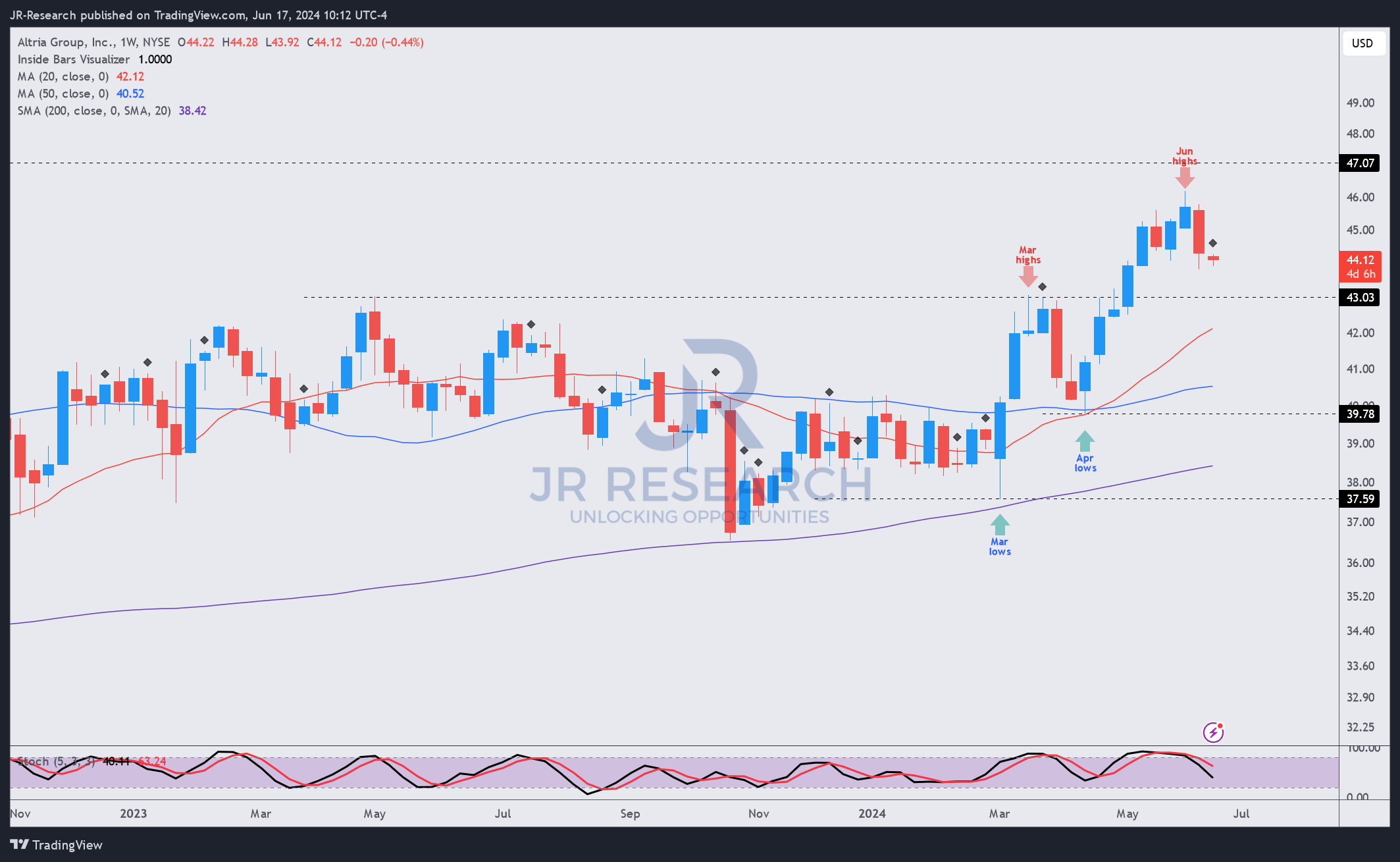

MO price chart (weekly, medium-term, adjusted for dividends) (TradingView)

As seen above, MO bottomed in April 2024 before surging to form its June high prior to its recent consolidation.

The critical resistance level that led to a selloff in April 2024 has been decisively breached, helping MO to return to a medium-term uptrend. MO’s trend bias is increasingly bullish, suggesting income and value investors are likely supporting its recovery.

Therefore, I assess that we are still early in MO’s nascent uptrend continuation thesis. As we move closer to the Fed’s potential interest rate cuts by the end of 2024, MO’s bullish bias could gain increased traction. Income investors reallocating their portfolios could also find MO’s high yields attractive, potentially driving further upside.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!