Summary:

- Amazon’s market cap was at a peak level when Jeff Bezos stepped down in July 2021.

- Since Andy Jassy took over, Amazon has lost almost half of its market valuation.

- By Buffett’s $1 test, Jassy’s scorecard is in the negatives so far, in stark contrast to Bezos’ spectacular scorecard ($19+ of stock price gain for every $1 retained earnings).

- This article examines Jassy’s scorecard more closely to argue that his miserable scorecard is largely caused by macroscopic forces.

- He’s an effective CEO and has been making the right calls. I am optimistic his strategies will show results given more time.

Michael M. Santiago/Getty Images News

Thesis

Jeff Bezos officially stepped down as the CEO of Amazon (NASDAQ:AMZN) CEO in July 2021 and passed the baton to Andy Jessy. From hindsight, the timing of the transition set Jessy up in a very tough spot. Amazon’s market cap was near a peak level when Bezos stepped, hovering around $1.7 trillion. Since Andy Jassy took over, AMZN’s market valuation plummeted together with the rest of the market. As of this writing, its market cap sits at $955 billion, almost only half of the peak level compared to the time of the transition.

As a result, by Buffett’s $1 test, Bezos boasts a spectacular scorecard. As to be determined in a later section, Bezos delivered an average of $19.28 in market cap gain in the last 10 years of his regain for every one dollar of retained earnings, far exceeding the threshed of $1 that Buffett deemed as a passing grade. While Jassy’s scorecard is in the negatives so far.

Therefore, the purpose of this article is to examine Jassy’s scorecard more closely. And based on such examination, I will argue that Jassy’s miserable scorecard is largely caused by macroscopic forces. He’s an effective CEO and has been making the right calls. To name a few of his key strategic moves, he is shifting capital investment toward AWS, its cloud computing unit, and slowing down retail expansion plans. After all, Andy Jassy was the boss of the cloud-computing unit before assuming the CEO role. He is finding ways to slash costs and recently shut down its subsidiary fabric.com (which sold fabrics for almost 30 years). Since he took over, Amazon also announced the acquisition of One Medical to accelerate its presence in the healthcare industry.

Overall, I see these moves as the right ones for AMZN to deal with both the immediate inflationary pressure and also to maintain high growth rates in emerging areas such as AWS and healthcare. Especially, he has been emphasizing R&D efforts and has been showing excellent R&D yield since he took over, as to be detailed next.

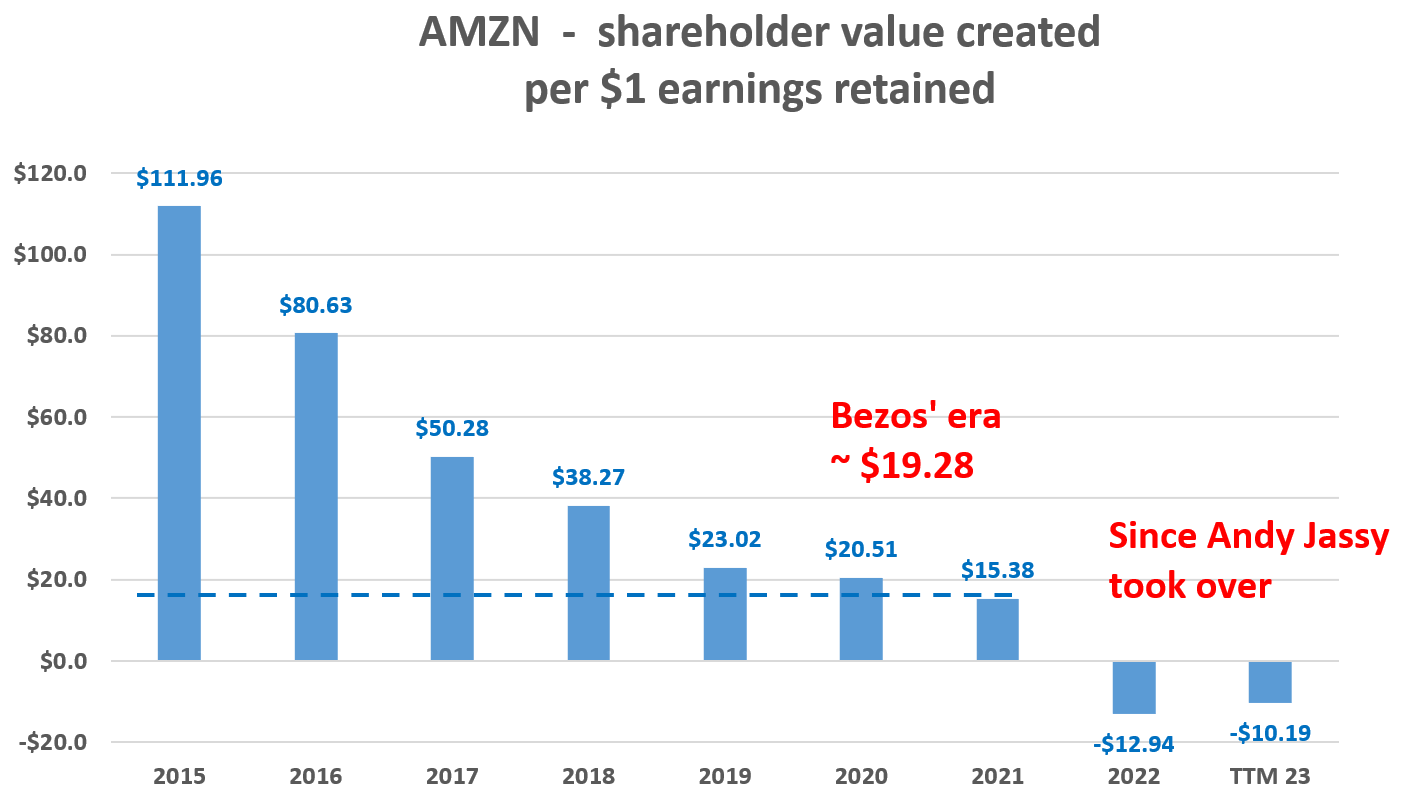

Scorecards for Bezos and Jassy on Buffett’s $1 test

Buffett’s $1 test is a subjective yardstick to measure CEO performance. By this test, a CEO should at least grow a company’s market cap (“MC”) by at least $1 for every dollar of retained earnings. And the chart below shows the scorecards for Bezos and Jassy. As seen from the chart, AMZN has been creating an average of $19.28 of MC gain per $1 of earnings retained during the last 10 years of Bezos’ leadership between 2011 and 2021. Note that the plot started in 2015 because I took a five-year running average, a typical treatment in Buffett’s $1 test. Thus, as a result, the plot actually included data all the way back to 2011.

Then Jassy took over in 2021, the most unfortunate time (at least for the sake of the $1 test scorecard) as you can see from the following chart. AMZN’s market cap was near a peak during the transition. And it has lost almost ½ of its market cap since Jassy took over. As a result, Jassy’s score is in the negatives, a stark contrast to Bezos’ flying colors.

Next, I will explain why I see a discrepancy between Jassy’s scorecard from the market versus the scorecard that he should receive. Such a discrepancy suggests an overaction in my view.

Source: Author based on Seeking Alpha data Source: Author based on Seeking Alpha data

The scorecard Jassy should have received

I view the issues that caused Andy Jassy failing scorecard to be largely macroscopic market forces (like record inflation and global supply chain disruptions) beyond anyone’s control. Not saying that macroscopic forces are not his problems. In the end, a CEO’s job is to deal with every and any sort of problem. Just saying that these problems are not his own making. And furthermore, I see he is making the right moves to deal with these issues.

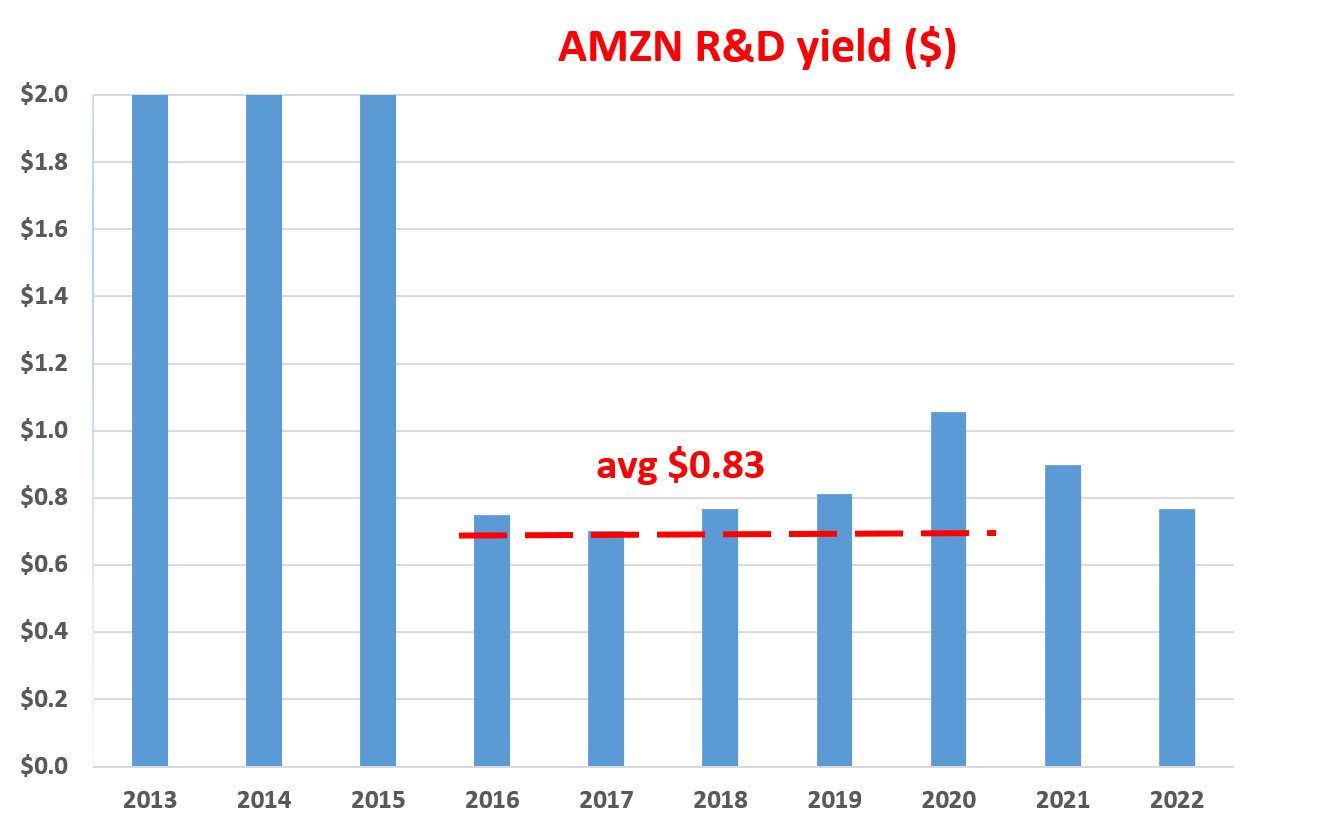

More importantly, as the leader of a tech giant, I view his strategy to shift focus toward AWS and slowing down retail expansion as a key strategy. For tech firms, I always like to run another $1 test, a variation of the original Buffett test on its CEO. This variation applies the $1 test on its R&D yield instead of MC. The details are provided in my other articles:

This variation of the $1 test calculates how many dollars of operating cash flow has been generated per $1 of R&D expenditure. In this test, I used the operating cash flow as the measure of profit. Also, many R&D projects do not produce results in a one-year period. They typically have a lifetime of a few years (say 2~3 years). Therefore, this analysis assumes a 3-year average investment cycle for R&D. As a result, we use the 3-year moving average of operating cash flow to represent a 3-year cycle.

And the next chart shows the test score for Jassy on this $1 test. The results paint a different picture as you can see. First, AMZN had not spent any meaningful amount on R&D before 2016. Plus, its earnings are also very erratic before 2016. Thus, the data points before 2016 are not that meaningful and should be ignored. Starting in 2016, AMZN began to spend meaningfully on R&D, on average ~12% of its total revenue on R&D efforts, on par with other major tech firms. Under Bezos’ leadership, AMZN’s average R&D yield dialed in around $0.83 between 2016 and 2020. And as the chart shows, since the CEO transition in 2021, Jassy has been maintaining an R&D yield that has been slightly better than this average.

Source: Author based on Seeking Alpha data

Summary of risks and final thoughts

I do not see AMZN totally out of the woods yet. Amazon posted healthy sales growth in the past quarter, largely driven by Prime membership subscription growth and AWS growth. However, its GAAP bottom line fell from a profit of $7.8 billion a year ago to a loss of $2.0 billion. The deficit was primarily due to a $3.9 billion write-down of its Rivian investment (a non-recurring loss) but also a range of other profit headwinds ranging from inflationary pressure, elevated fuel/energy cost, labor cost, and global supply chain disruptions. And in my view, these profit headwinds are still ongoing and will keep pressure on AMZN in the next few quarters.

Although, I view Jassy as an effective CEO. And he has been making the right calls to address these issues the way I see things, despite his miserable scorecard from the market. I see a completely different scorecard in terms of business fundamentals. All told, I see his strategic moves as not only the right ones to deal with the immediate issues but also to position AMZN for future growth in emerging areas such as AWS and healthcare.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Join Envision Early Retirement to navigate such a turbulent market.

- Receive our best ideas, actionable and unambiguous, across multiple assets.

- Access our real-money portfolios, trade alerts, and transparent performance reporting.

- Use our proprietary allocation strategies to isolate and control risks.

We have helped our members beat S&P 500 with LOWER drawdowns despite the extreme volatilities in both the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too. You do not need to pay for the costly lessons from the market itself.