Summary:

- AWS is a powerhouse in the hyperscale cloud space, with a unique background and significant investments in chip development.

- Amazon has built strong long-term relationships with customers and continues to innovate in the cloud computing industry.

- AWS is now a substantial portion of AMZN’s overall valuation.

Noah Berger

Introduction

The world continues moving to the cloud and AWS (NASDAQ:AMZN) still sees advantages as they were the first to develop solutions for external partners on a wide scale. Microsoft (MSFT) Azure and Google Cloud (GOOG) (GOOGL) came in years later such that these 3 offerings complete the hyperscale cloud space. Now the space is more mature and it will be difficult for new competitors to emerge moving forward. My thesis is that AWS is a powerhouse.

There have been clarifications from management since my February article where I noted Amazon’s efficiency in meeting cultural objectives. CEO Andy Jassy’s 2022 shareholder letter was published after my February article and it gives investors a great deal of information about the importance of Amazon’s chip development efforts.

Unique Background

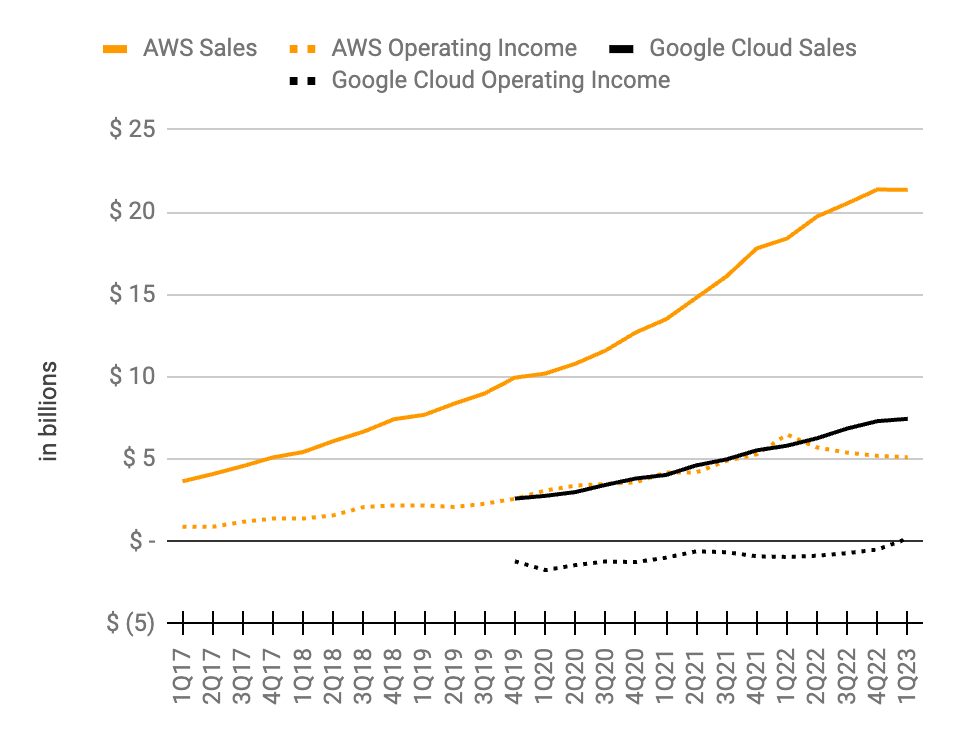

AWS was not alone in terms of having massive infrastructure years ago but they were the first company to develop solutions for external partners on a massive scale. Any company wanting to join AWS, Azure and Google Cloud in the hyperscale cloud space these days should be willing to suffer cumulative operating losses of more than $10 billion over the first 3 to 4 years; this is a tremendous barrier to entry. AWS was the pioneer in the cloud business and they have always enjoyed better economics than Google Cloud who entered the business in a meaningful way about 4 years later. We see below that AWS had a superior operating margin to Google Cloud at similar revenue levels. Specifically, 1Q21 for Google Cloud revenue was roughly comparable to 1Q17 for AWS revenue and the quarters match up somewhat well going up to 1Q23 for Google Cloud and 1Q19 for AWS. Said another way, Google Cloud had operating losses of nearly $13 billion on revenue of $61 billion in the 3.5 year period from 4Q19 to 1Q23. AWS, on the other hand, had positive operating income of over $15 billion on revenue of nearly $58 billion in the 3.5 year period from 4Q15 to 1Q19:

Operating income & revenue for AWS & Google Cloud (Author’s spreadsheet)

Again, Google Cloud had cumulative operating losses of nearly $13 billion from the last 3.5 years and it would probably be even worse for a new company entering the hyperscale cloud space at this time. As such, I don’t see new competitors on the horizon.

Amazon CEO Jassy’s 2022 letter explains that they had to invest vast amounts of capital over a decade ago in order for AWS to exist as we know it. This type of long-term thinking tends to be unique with respect to publicly traded companies (emphasis added):

In 2008, AWS was still a fairly small, fledgling business. We knew we were on to something, but it still required substantial capital investment. There were voices inside and outside of the company questioning why Amazon (known mostly as an online retailer then) would be investing so much in cloud computing. But, we knew we were inventing something special that could create a lot of value for customers and Amazon in the future. We had a head start on potential competitors; and if anything, we wanted to accelerate our pace of innovation. We made the long-term decision to continue investing in AWS.

A 2015 writeup by John Furrier @furrier explains how Amazon shifted to APIs in order to do away with entanglement and open up infrastructure to external customers:

“We’d realized in the first ten years we’d built an infrastructure competence deep in the stack – reliable, scalable cost effective data centers to grow the Amazon retail biz the way we needed to,” says Jassy. “But we’d built Amazon so quickly that a number of the pieces of the platform had become entangled.” To develop solutions for external partners, Amazon would need an effective way to communicate with them via hardened APIs, and that meant decoupling the entangled parts of the platform.

Chip Development

CEO Jassy’s 2022 letter says long-term investments have been made in chip development and he believes these investments will prove to be fruitful as they are “not close to being done innovating.”

The AWS Graviton3 chips can be a lower-cost and higher performance solution than what is available from Intel (INTC) and AMD (AMD) per a July 2022 SA article by Paulo Santos @ThinkFinance999. At the AWS re:Invent 2022 – Keynote with AWS CEO Adam Selipsky, it was shared that DirecTV uses Graviton3 instances such that costs are reduced by 20% and latency is lowered by up to 50%.

GPUs are used for machine learning and Nvidia (NVDA) has a March announcement about their collaboration with AWS in which they say AWS is a long-term partner and the first cloud provider to offer Nvidia GPUs. The growth of GPUs should continue to be substantial but machine learning workloads will be more diverse in the future per Amazon CTO Dr. Werner Vogels @Werner:

Software engineers have traditionally relied on expensive, power-hungry GPUs to do everything from model building to inference. However, this one-size-fits-all approach is not efficient – most GPUs aren’t optimized for these tasks. In the coming years, more engineers will see the benefits of moving workloads to processors specifically designed for things like model training (AWS Trainium) and inference (AWS Inferentia).

In the 2022 letter, CEO Jassy said their Trainium-based instances are up to 140% faster than GPU-based instances at up to 70% lower cost. He also talked about their inference chips (emphasis added):

We launched our first inference chips (“Inferentia”) in 2019, and they have saved companies like Amazon over a hundred million dollars in capital expense already. Our Inferentia2 chip, which just launched, offers up to four times higher throughput and ten times lower latency than our first Inferentia processor. With the enormous upcoming growth in machine learning, customers will be able to get a lot more done with AWS’s training and inference chips at a significantly lower cost.

Closing the chip development portion of his 2022 letter to shareholders, CEO Jassy says AWS is still in the early stages of its evolution and there is a chance for unusual growth in the decade ahead.

Powerhouse

AWS is now a powerhouse helping all kinds of businesses around the globe. The 1Q23 release mentions Southwest Airlines, Zurich Insurance Group, S&P Global, Snowflake, Stripe, T-Mobile, Marvell and many others:

AWS Testimonials (1Q23 release)

Valuation

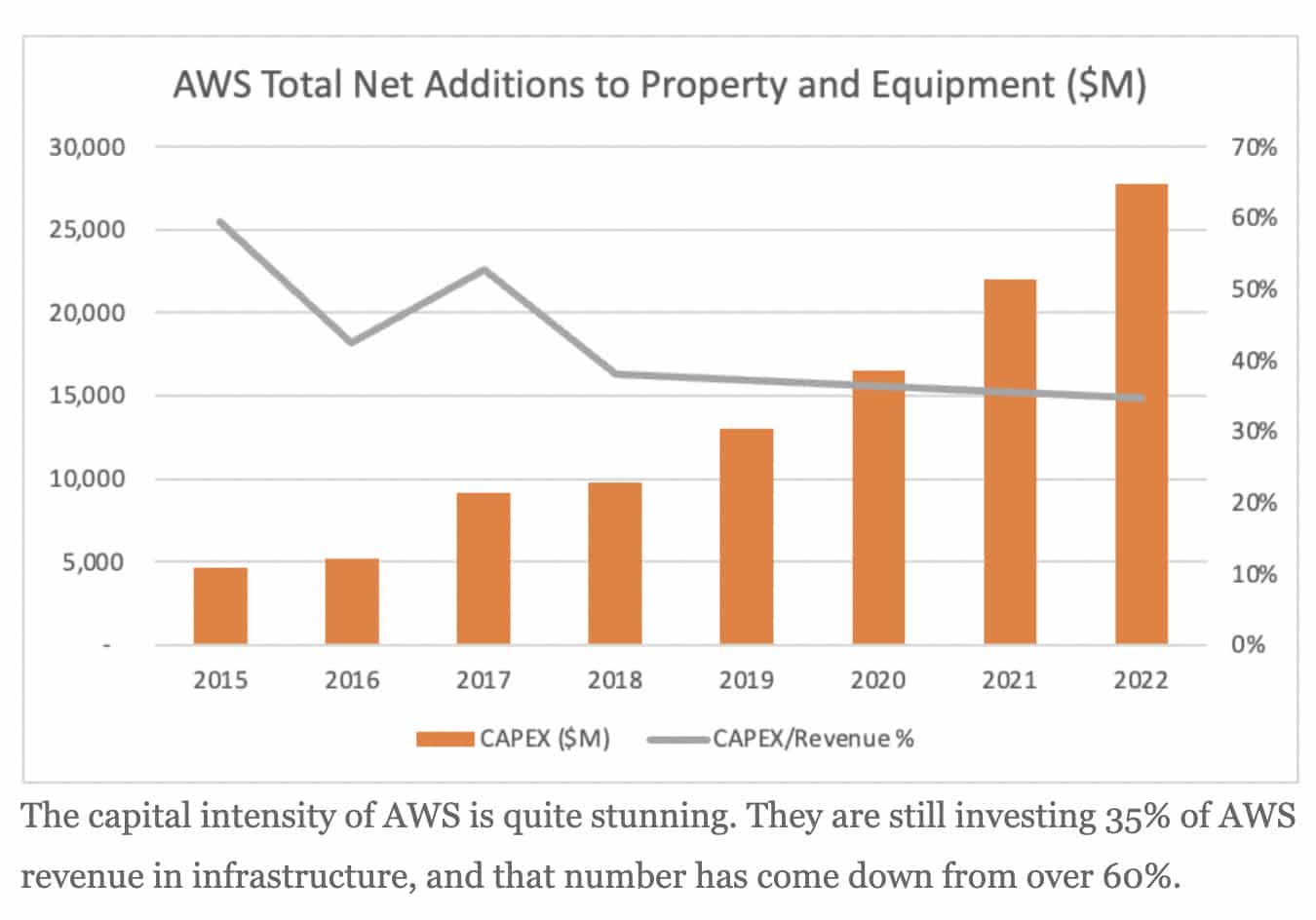

We see operating income for AWS broken out in filings but we don’t directly see the numbers needed to determine free cash flow (“FCF”). In other words, we don’t directly see operating cash flow and capex for AWS. Even if we saw these numbers directly, we would also want to know the breakdown between maintenance capex and growth capex in order to think about adjusted FCF. One thing we do know is that the capex is substantial although it isn’t as high a percentage of revenue as what we see from TSMC (TSM). The TSMC 2022 20-F shows how capital intensive it can be to manufacture semiconductor chips. In 2022, they had capex of $35.2 billion which was almost 48% of their $73.7 billion revenue. Hyperscale cloud companies like AWS are capital intensive as they have to buy copious quantities of these chips. Charles Fitzgerald @charlesfitz shows the amount of capex at Amazon devoted to AWS. It was over $15 billion in 2020, over $20 billion in 2021 and over $25 billion in 2022. It wasn’t until 2018 that AWS capex dropped to be about 40% or less of AWS revenue on a consistent basis:

AWS capex (Charles Fitzgerald)

Trailing twelve month (“TTM”) operating income for AWS from the 1Q23 10-Q and the 2022 10-K was $21,446 million or $5,123 million + $22,841 million – $6,518 million. This came from $83,009 million or $21,354 million + $80,096 million – $18,441 million in TTM revenue. Investors don’t like to see the temporary decline in AWS operating income in 1Q23 but they can be mollified by the fact that long-term relationships are being strengthened with customers. The AWS operating margin was about 30% from 3Q18 to 2Q22 but it has been closer to 25% from 3Q22 to 1Q23. CEO Jassy said in the 1Q23 call that more than 90% of the global IT spend is still on-premise. I’m more optimistic about AWS than in the past given the chip development possibilities and I believe AWS is worth 22 to 25x TTM operating income implying a range of $470 to $535 billion.

Beyond AWS, Amazon has a powerful marketplace and CEO Jassy’s 2022 letter explains that third-party (“3P”) now accounts for 60% of unit sales. Due to their vast marketplace, they generated nearly $38 billion in advertising revenue in 2022. I think the non-AWS components of Amazon combine to be worth about 2 Walmarts (WMT). The 10-Q for Walmart through April 30, 2023 shows 2,692,835,112 shares outstanding as of May 31st such that the market cap is a little over $403 billion based on the June 6th share price of $149.78. As such, I think the rest of Amazon is worth about $805 billion. This puts my total valuation range at $1,275 to $1,340 billion.

The 1Q23 10-Q shows 10,260,353,688 shares as of April 19th. Multiplying this by the June 6th share price of $126.61 gives us a market cap of $1,299 billion. The market cap skews a bit towards the lower side of my valuation range and I think the stock is a buy for long-term investors.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN, GOOG, GOOGL, TSM, VOO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.