Summary:

- Amazon’s 3Q23 revenue of $143.1 billion exceeded expectations and was at the high end of guidance.

- Operating income of $11.2 billion beat guidance by 32%, with outperformance in multiple areas, including North American Retail and AWS.

- The company also provided an update on its generative AI traction.

- Prime Video’s traction remains encouraging, and it looks like it can be a large and profitable business on its own.

Daria Nipot

Today, I will be reviewing the opportunity for Amazon (NASDAQ:AMZN).

Given that this is the second consecutive quarter of strong margin improvement for Amazon, I also revised my financial forecasts for the company and the corresponding intrinsic values and price targets were also revised higher.

3Q23

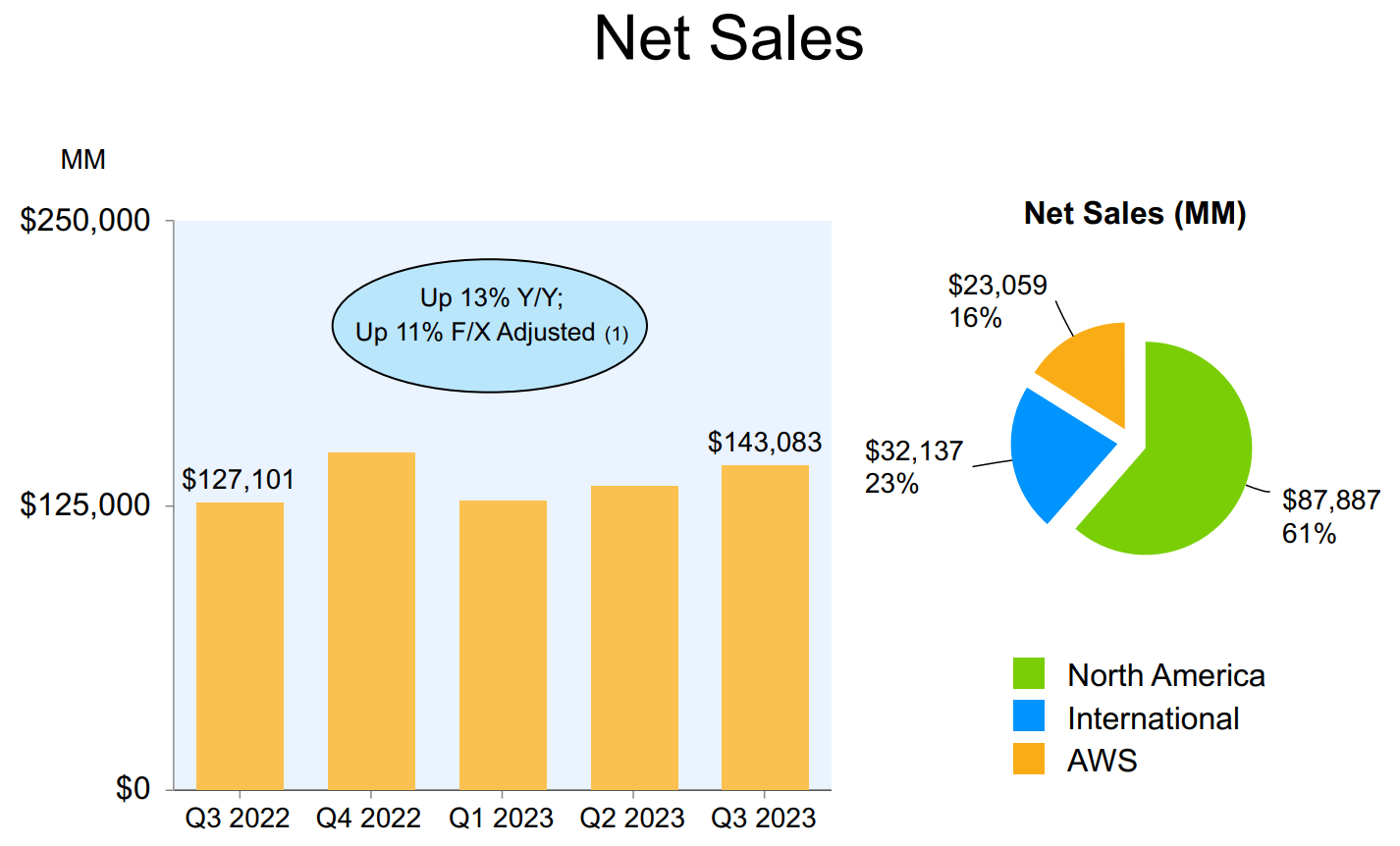

3Q23 revenue came in at $143.1 billion, up 13% from the prior year and 11% on a constant currency basis. This was 1% above consensus and at the high end of the guidance of $138 billion to $143 billion.

Net sales (Amazon)

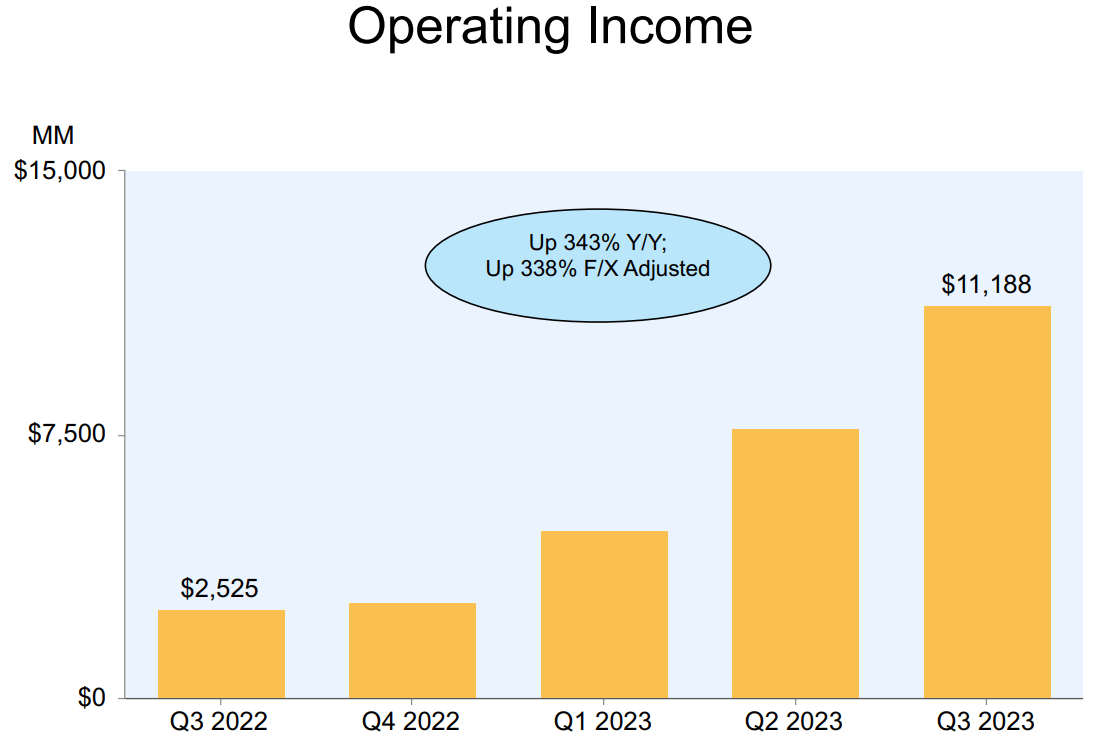

Operating income came in at $11.2 billion, or 7.8% margin.

This was a very significant beat as it came in 32% higher than the high end of the guidance of $5.5 billion to $8.5 billion, with outperformance coming from multiple areas, including North American Retail, International Retail and AWS. North American retail and AWS margins came in at 4.9% and 30.3%, compared to expectations of 4% and 24% margins.

In particular, the key drivers of the improvement in margin was largely due to continued reductions in its cost to serve, advertising growth and improved leverage on fixed costs, along with improvements on the working capital and inventory efficiency front.

Operating income (Amazon)

As a result, GAAP EPS came in at $0.94, 59% higher than consensus of $0.59.

North America retail revenue came in at $87.9 billion, growing 11% from the prior year on a constant currency basis. This was 2% higher than the consensus expectations.

International revenue came in at $32.1 billion, up 11% from the prior year on a constant currency basis, beating consensus by 0.5%.

In particular, demand trends look healthy by line item.

Online stores, 3P Seller Services and Advertising revenue grew 6%, 18% and 25% on a constant currency basis, exceeding consensus expectations by 1%, 3% and 4% respectively. The better-than-expected and re-acceleration of the advertising revenue was likely the key contributor to the better-than-expected operating income. The only soft spot was Physical Stores revenue which grew 6% on a constant currency basis and it was 1% below consensus.

AWS

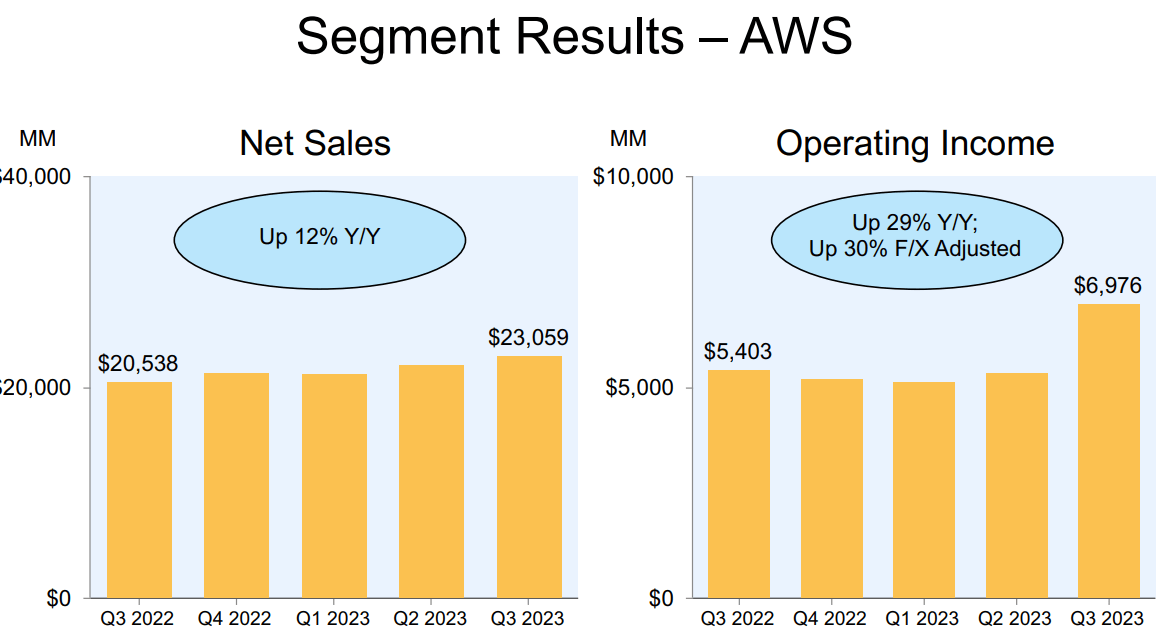

AWS showed signs of stabilization as revenue was up 12% from the prior year on a constant currency basis to $23.1 billion, 1% below consensus.

AWS operating margins came in at 30.3%, beating expectations.

AWS segment results (Amazon)

Guidance

4Q23 revenue was guided in the range of $160 billion to $167 billion, 2% below consensus at the midpoint and it assumes 40 basis points of favorable impact from foreign currency movements.

4Q23 operating income guidance was in the range of $7 billion to $11 billion, somewhat in-line with consensus expectations of $8.5 billion.

The guidance could prove to be conservative.

On the call, we will be focused on AWS demand and progress with its GenAI offerings, benefits of Amazon’s newer regionalized fulfillment network, insights around Buy with Prime and Supply Chain by Amazon, and views into overall OI margin expansion.

AWS

AWS growth rate continued to stabilize in 3Q23.

In terms of commentary, AWS saw elevated cost optimization when compared to the last year but management commented that they are starting to see this trend stabilize as more companies are looking to deploy net new workloads.

While the pace of completing deals has been slow in 2023 due to an uncertain macro backdrop, AWS has seen the pace and volume of closed deals accelerate and in particular, AWS saw strong new deals signed in the last couple of months.

I think we will see 4Q23 AWS re-accelerate from 3Q23 as management commented that there were several new deals that were signed in September but only goes in effect in October. These deals when combined is higher than the total deal volume for all of 3Q23 and they will only be reported in the reported numbers for 4Q23.

In terms of AWS customer commitments and expansions in 3Q23, BMW Group chose AWS to power its automated driving platform, NatWest expanded its partnership to accelerate the use and co-creation of AI products, and Occidental chose AWS as its preferred cloud provider, amongst others.

As a result, the deal momentum that AWS is seeing is encouraging, especially for 4Q23. Deal signings are always lumpy and the revenue happens over several years but we like the recent deal momentum we’re seeing.

Generative AI

Amazon also provided an update on its generative AI traction.

As mentioned earlier, the company has three layers at which it is investing in and each layer presents a huge opportunity set for the company.

At the lowest layer, Amazon is working on custom silicon for training and inference with its Trainium and Inferentia chips respectively. These are the compute used to train large language models (“LLMs”)and produce inferences.

At this lowest layer, Anthropic chose AWS as its primary cloud provider and will use Trainium and Inferentia to build, train and deploy its future LLMs and also collaborate on the future development of Trainium and Inferentia technology.

At the middle layer, which the company thinks of as large language models as a service, Amazon Bedrock was recently made generally available.

Amazon Bedrock offers access to leading LLMs from third party providers like Anthropic, Stability AI, coherent AI and from Amazon’s own LLM, Titan.

Amazon Bedrock will be adding Meta’s Llama 2 model, which is the first time it is being made available through a fully managed service, and also Anthropic models will also be added to Amazon Bedrock.

And Bedrock has added several new compelling features, including the ability to create agents which can be programmed to accomplish tasks like answering questions or automating workflows.

The feedback from customers about Amazon Bedrock has been positive as it enables customers to build and scale enterprise-ready generative AI applications.

Finally, at the top layer which includes all the applications that run on the LLMs, Amazon CodeWhisperer, its generative AI coding companion, has received early traction and is becoming more powerful with the launch of its new customization capability. Amazon CodeWhisperer also just launched the ability of the coding companion to be familiar with customers’ proprietary code bases, which has been one of the top requested feature for coding companions.

As AWS is the market leader in cloud infrastructure and thus has the largest number of customers and data, I expect that this will bring about some form of advantage as customers would want to build their models around the data stored with AWS.

The company also shared that the number of companies that are building generative AI applications in AWS is substantial and also growing rapidly, with some big names like United Airlines, Booking.com, Adidas, Clariant, GoDaddy, Merck, Bridgewater and Royal Philips amongst some of the names that were shared in the earnings call.

There was also traction with generative AI start-ups like Perplexity.ai, which chose to go all in with AWS, including running models using Trainium and Inferentia.

Improvement in fulfilment network

I have mentioned this multiple times, given Amazon has been working on this for some time.

Earlier in 2023, Amazon transitioned form a single national fulfillment network in the United States to 8 distinct regions.

This was one of the largest changes it made and in 3Q23, management mentioned that this has gone more smoothly and brought more benefits than initially expected.

With these regional fulfillment centers, it means that each regional fulfilment center has higher local in-stock levels and optimized connections between the regional fulfilment center and deliver stations. As a result, this has led to shorter routes and fewer touch points to get to customers.

Consequently, these shorter routes and fewer touch points also meant lower cost to serve and faster shipments.

As a result, Amazon is on track to deliver the fastest delivery speeds to Prime customers ever. According to the management, this faster delivery speeds has a direct consequence in terms of the growth in buying behavior of consumables and everyday essentials on Amazon.

I particularly like that Amazon has evaluated its entire fulfillment network and identified ways to improve efficiency and improve the entire experience for customers while lowering costs.

According to the management team, while the key change has been on the regionalization, they believe that we have not yet seen the full benefits of this and the company continues to fine-tune its placement algorithms to ensure better in-region fulfillment and increase consolidation into fewer shipments.

Another change it has done is to make changes to its inbound processes that can lower the cost to serve and increase the speed of delivery.

At the end of the day. I think the team is really working hard to find ways to improve cost and speed and they continue to find areas within the entire fulfillment network where things can be improved and then executing it in a meaningful way.

Prime Video

The progress made in Prime Video continues to be encouraging.

Prime Video remains a core part of the Prime membership value proposition as it is one of the top two drivers for customers deciding to sign up for Prime membership.

In addition, management is starting to have more conviction that Prime Video can be a large and profitable business on its own.

The company will continue to invest in content for Prime members but also offer a wide array of streaming video content as it includes channels like Max, Paramount+, BET Plus and MGM+, and more.

Amazon continues to invest in content and starting from early 2024, Prime Video will include limited advertisements. While there will be meaningfully fewer ads than the linear TV players or other streaming players, customers looking for an advertisement free option can have that for another $2.99 per month for US members.

Valuation

I revised my forecast for Amazon, in particular the margin profile upwards to reflect the recent improvements in margin and also rolled forward the 5-year forecast period to 2024 to 2028.

Likewise, my 1-year price target go up to $173, based on 30x P/E.

The 30x P/E used here is justified given Amazon’s leading position in AWS and retail segments.

Conclusion

Amazon’s fundamentals continue to improve and strengthen as we enter 2024.

AWS is showing signs of stabilization as more companies are looking to deploy net new workloads. The commentary about several new delas that were signed in September but only goes into effect in October having a total deal volume of more than that of all of 3Q23 is also encouraging.

In addition, Amazon provided more update on its generative AI initiatives as it looks to cover all three layers of the opportunity set.

In addition, a large part of the expansion of operating margins came from the improvements made in its fulfillment network. It is also encouraging to note that management believes we have not yet seen the full extent of its regionalization efforts and the team continues to evaluate all aspects of the fulfillment network to identify areas to improve.

Lastly, Prime Video continues to do well and remains a core part of Prime membership given that it is one of the top two drivers for customers deciding to sign up for Prime membership.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Outperforming the Market

Outperforming the Market is focused on helping you outperform the market while having downside protection during volatile markets by providing you with comprehensive deep dive analysis articles, as well as access to The Barbell Portfolio.

The Barbell Portfolio has outperformed the S&P 500 by 34% in the past year through owning high conviction growth, value and contrarian stocks.

Apart from focusing on bottom-up fundamental research, we also provide you with intrinsic value, 1-year and 3-year price targets in The Price Target report.

Join us for the 2-week free trial to get access to The Barbell Portfolio today!