Summary:

- Amazon suffered in the recent selloff due to recession fears, despite strong Q2 results.

- AWS-led operating income growth supports Amazon’s valuation and future growth potential.

- Market slide presents opportunity for long-term investors to buy Amazon at a more moderate valuation multiple.

4kodiak/iStock Unreleased via Getty Images

Amazon Inc. (NASDAQ:AMZN) suffered, together with other tech companies, through a brutal selloff in the last couple of days, with selling pressure exacerbating on Friday and Monday. The cause of this selloff was a bad labor market report for the month of July that invoked recession fears, which fully burst out into the open on Monday.

Amazon, however, presented quite respectable results for its second quarter last week. I think the market is overlooking, if not discounting, the strength of the earnings release as the market went into full-on panic mode yesterday.

Level-headed investors can take advantage of the panic selling, as I think that Amazon will be able to thrive even during a possible recession.

My Rating History

Amazon’s ramping momentum in both eCommerce and AWS fundamentally underpinned my Strong Buy thesis in April. The market selloff, which started on Friday and accelerated on Monday on general recession fears, is an opportunity for long-term thinking investors to either start a position, or double down on one, in my view.

Amazon’s profit multiple compressed by 20% since July, which is when the stock traded as high as $200. The main reason to buy here is that I think Amazon’s eCommerce and cloud businesses are poised to continue to flourish, even during a recession, and I think that the risk/reward relationship, as far as the valuation is concerned, has greatly improved.

Sizable Profit Beat, AWS-Led Operating Income Uplift

Amazon reported better-than-anticipated earnings for its second quarter, with its profits of $1.26 per share topping the Street estimate of $1.03 per share.

Earnings And Revenues (Tipranks)

All things considered, it was a rather decent second quarter for Amazon, with North America eCommerce enjoying 9% YoY sales growth and International eCommerce growing net sales 7% YoY.

Most importantly, AWS, Amazon’s cloud segment, enjoyed 19% YoY growth and thus grew about twice as rapidly as the company’s largest segment, North American eCommerce.

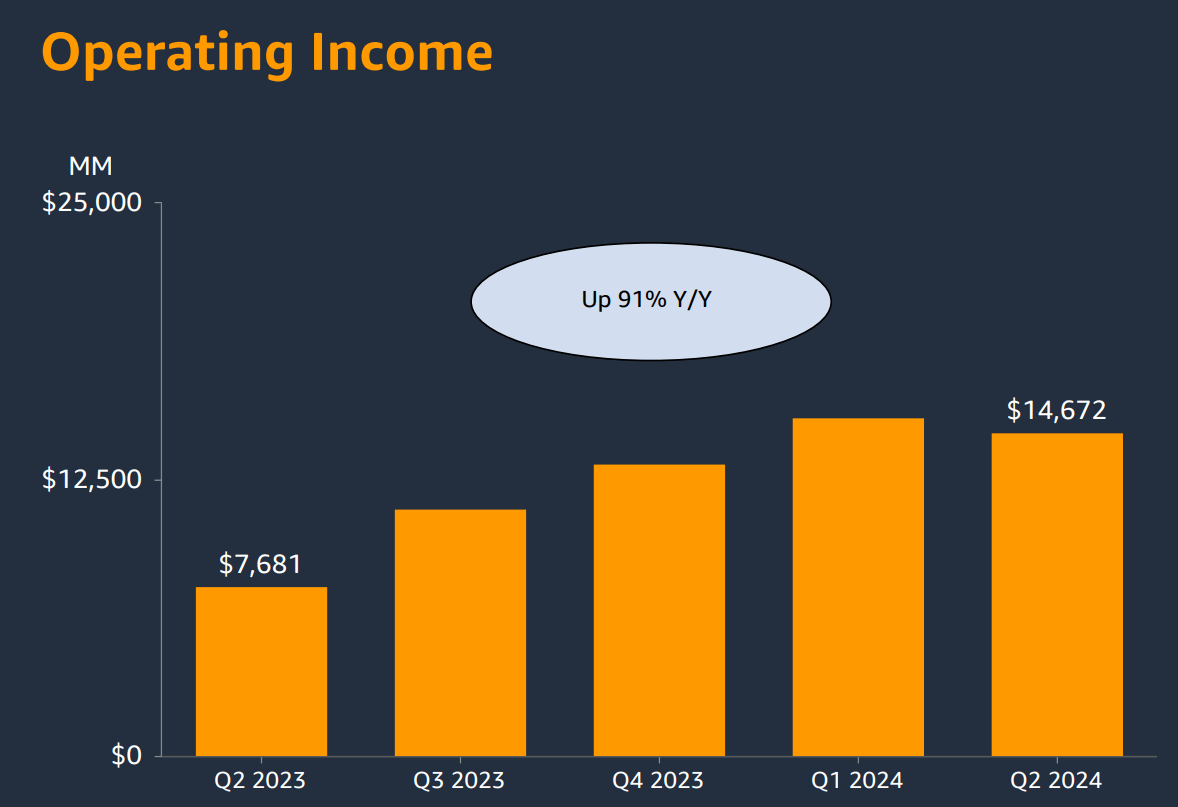

Thanks to robust growth in cloud, Amazon is enjoying skyrocketing growth in its operating income, which, I thought, was the most relevant information in Amazon’s second quarter earnings.

Amazon’s operating income skyrocketed 91% YoY to $14.7 billion, which gives the company a lot of earnings to reinvest into its flourishing eCommerce and cloud businesses. Of the $14.7 billion in operating profits, a whopping $9.3 billion came from cloud, and Amazon is making moves here to grow its operating profitability.

Among the measures that Amazon is pursuing is an aggressive growth strategy focused on international markets and the business landed new AWS agreements in the second quarter with new companies like Discover Financial Services, Eli Lilly and Company, and Experian, to name just a few.

Moving forward, AWS will be absolutely instrumental in boosting Amazon’s overall growth and since the segment also enjoyed a reacceleration of its segment growth compared to 1Q24, AWS is and will remain the best reason to own a piece of the growing Amazon brand.

Operating Income (Amazon Inc.)

Investor Fears, Market Slide And Free Cash Flow Support

Markets around the world crashed on Monday after Friday’s labor market report deeply disturbed investors and ignited panic selling. According to the Bureau of Labor Statistics, U.S. employers created only 114K jobs last month, which was much lower than the 185K estimate.

These jobs reported ignited a global selloff that led to a big multiple contraction for Amazon’s stock. The jobs report followed a very soft reading of the ISM Manufacturing Index, which measures manufacturing activity and which flashes a contraction signal as well (which is typically associated with a value of 50 or less).

ISM Manufacturing PMI Index (Forbes)

With that said, though, I am very comfortable owning and buying more Amazon stock at this time, not only because of AWS’s stabilizing growth, but also because Amazon is producing an unreal amount of free cash flow from its eCommerce and cloud segments.

In my view, companies that are swimming in free cash flow should ultimately have much less correction potential than those companies that are at the margins in terms of profit or free cash flow.

Amazon’s free cash flow in the last twelve months amounted to a whopping $53.0 billion and thanks to customer growth and momentum in AWS, the company has seen a rather substantial free cash flow uplift in the last year as well: On an LTM-basis, Amazon’s free cash flow skyrocketed 572% YoY and I don’t see this growth stopping any time soon.

Free Cash Flow – TTM (Amazon Inc.)

Amazon might even be a beneficiary of a potential recession, just as the company benefited from the Covid contraction in 2020. Recessions tend to increase economic pressure and curtail consumer spending in the short term, which the most profitable eCommerce companies can withstand, particularly a company like Amazon which can fall back on its ultra-profitable AWS segment.

More Moderate Valuation Multiple Following Market Slide

Amazon has seen a quite substantial correction in the last couple of days, which of course makes Amazon that much more appealing from a valuation angle. The market presently models $5.86 per share in profits for next year, reflecting a 24% YoY profit growth rate next year.

As I am penning this article, Amazon is selling for $161 per share, which leads us to a leading profit multiple of 27x. That same profit potential on Thursday last week cost investors 34x next year’s profits a week ago (reflecting a 20% compression in the valuation multiple.

Earnings Estimate (Yahoo Finance)

Amazon, with its profitable AWS business and eye-popping high levels of free cash flow, deserves a premium multiple, in my view. Based on Amazon’s operating income strength and growing AWS footprint, I see a 40x profit multiple as justified, leading us to an implied intrinsic value target of $215.

Of course, I would have to make allowance here if the U.S. economy were to slide into a recession, but I am not as concerned as the market seems to be about Amazon’s ability to produce consistent profit growth over time.

Why The Investment Thesis Might Not Work Out

Amazon is not immune to the effects of a recession and a softening labor market. Weaker job growth and, possibly, a contraction in the U.S. economy are going to negatively impact consumer spending in eCommerce as well as corporate spending in AWS.

With that said, though, since Amazon’s stock price has fallen from $190 to just $160 in two days, I think that the valuation multiple that is now available here improves the risk analysis and skews it in favor of Amazon.

My Conclusion

For what it’s worth, I am doubling-down on Amazon, as I think that the present market selloff is not going to fundamentally change the net sales and profit growth prospects of Amazon overnight.

Yes, there is a risk of a profit contraction in case of a recession, but Amazon has been a major beneficiary of the last recession (during Covid) as well and emerged from it with a record-high stock price.

AWS is growing like crazy and so are the company’s operating profits, which is what fundamentally sustains Amazon’s valuation.

I think Amazon is primarily a buy for investors now due to its much lower profit multiple, which does not reflect the company’s underlying growth potential.

All things considered, I think investors that establish a long position in Amazon at a time of escalating panic selling and have a 3-5 year investment horizon are getting a really solid bargain here.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.