Summary:

- Amazon has outperformed the market and is expected to see growth reacceleration in its retail and AWS businesses.

- Q2 2023 earnings exceeded expectations, with revenue increasing by 10.9% YoY and EPS beating estimates.

- The company’s retail sales are recovering as in-store shopping demand returns to normalized levels, and its advertising business is also seeing good growth.

- AWS is also benefiting to recent innovations in generative AI.

- Margin outlook is positive, and valuations are reasonable.

HJBC

Investment Thesis

Amazon.com, Inc. (NASDAQ:AMZN) has outperformed the broader markets since my previous bullish article where I talked about the company’s potential reacceleration in growth. In line with my expectations, the company posted good last quarter results and saw a reacceleration in Online Store sales growth rate after tough last few quarters. I believe the company’s retail business should continue to see growth re-acceleration while AWS’ growth rate is also expected to bottom soon and recover from there. Moreover, long-term secular demand trends from Artificial Intelligence (AI) and generative AI should accelerate the migration of businesses worldwide to cloud services from on-premises solutions in order to improve efficiency and productivity. This should help growth reaccelerate in the AWS segment in the coming years.

On the margin front, the company is poised to benefit from sales leverage, moderating inflation, cost-saving measures, and mix benefits due to an increase in AWS sales (which has a higher margin profile). Furthermore, Amazon is currently trading at a discount compared to its historical averages based on the forward P/E, P/S, and EV/EBITDA ratio. This, combined with the long-term revenue and margin growth prospects, makes the company an attractive investment. Hence, I continue to have a buy rating on the stock.

Q2 2023 Earnings

Recently, Amazon.com, Inc. reported better-than-expected results for its second quarter of 2023. Revenue increased by 10.9% YoY to $134.4 billion and surpassed the consensus estimate by $2.96 billion. EPS was $0.65 as compared to -$0.20 in the previous year’s quarter and beat the consensus EPS estimate by $0.34. Operating margin increased by 310 basis points YoY to 5.7%. The increase in revenue was a result of good demand for essential products in the retail business as well as improved customer satisfaction due to increasing delivery speed. The EPS and operating margin increased as a result of sales leverage and cost-saving benefits.

Revenue Analysis and Outlook

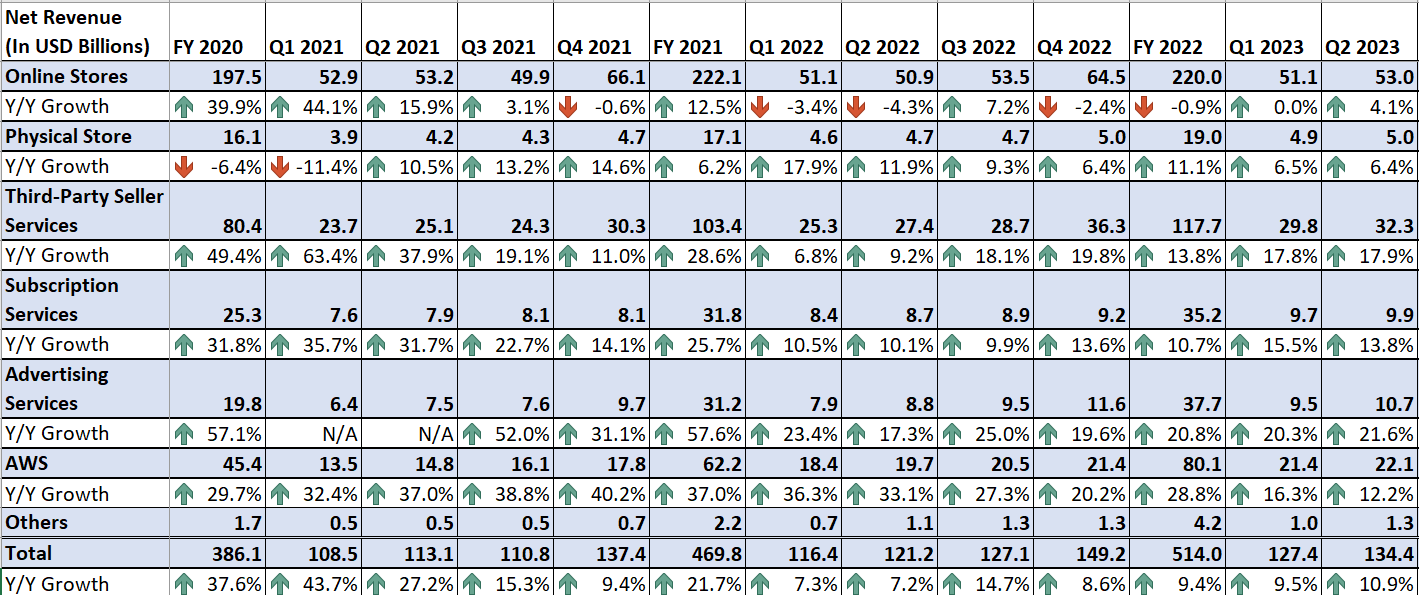

After the post-pandemic reopening, the company experienced a notable slowdown in its retail business, especially in the online store business. This was due to the pent-up demand for in-store shopping as the economy reopened, which had an adverse effect on e-commerce sales. Consumers were eager to return to physical stores, shifting their purchasing behavior from e-commerce to in-store. As a result, the company’s retail sales fell significantly below the pre-pandemic levels. However, demand for in-store shopping is gradually returning to normalized levels and consumers are getting attracted to lower and promotional price points offered frequently at online platforms as compared to in-stores in an inflationary environment. This is helping the company’s retail sales recover and also helping the overall sales growth re-acceleration. For instance, in Q2 2023, AMZN offered customers 144% more deals and coupons as compared to Q2 of 2022, which helped in increasing volume and retail sales. In Q2 2023, the company’s online store business posted a 4.1% YoY growth which is a good acceleration versus Q1 2023’s flattish YoY growth. Moreover, the company also held its prime day on July 12th-13th in the ongoing third quarter of 2023 where prime members purchased more than 375 million items due to attractive deals and offers. This should help retail sales growth in the third quarter as well.

AMZN’s Historical Revenue By Type of Activity (Company Data, GS Analytics Research)

On top of the lower and promoted price points, the company’s retail sales are also benefiting from improving customer experience through the increase in delivery speed. In my previous article, I mentioned that the company is regionalizing its distribution centers (fulfillment centers) to enhance delivery speed and implementing strategies to boost 1-day and same-day delivery sales. So far this year, Amazon has delivered more than 1.8 billion units to U.S. Prime members the same or the next day, which is nearly four times the number of units delivered at those speeds by this point in 2019. Furthermore, in the second quarter, the company introduced Amazon Day deliveries, which allow Prime members to select a specific day of the week when they want to receive their order according to their personal schedules. This should improve the customer experience even more, and help recover retail sales growth.

So, as the company focuses on improving delivery speed and introducing appealing deals on its e-commerce platforms, it should be able to offset the near-term impact of tough macros on consumer demand.

Moreover, apart from the retail business, the company’s advertising business (through which AMZN provides advertising services to sellers, vendors, publishers, authors, and others, through programs such as sponsored ads, display, and video advertising) is also seeing good growth as it growing revenue in teens to low twenties since the last year. The company is further improving its advertising services by leveraging machine learning to increase the relevancy of the ads shown to customers and improving the ability to measure the return on advertising spend for brands through an increase in click-through rate, an increase in return on ad spend, and a decrease in cost per impression. This should further attract brands to AMZN’s advertising services as they look to increase their advertising ROI to increase profitability. So, I expect advertising services to also help the sales growth moving forward.

Coming to the company’s Amazon Web Service (AWS) business, which contributes ~17% to total sales, while the business is seeing growth rate normalization as well as the adverse impact of enterprise customers’ tight budgets in an inflationary environment, I believe the business’s medium to long-term growth prospects are good. The company has emerging tailwinds from secular trends in AI and Generative AI space. In today’s world, automation of daily tasks and the increasing prevalence of artificial intelligence (AI) are becoming important for dealing with uncertainties in business and ensuring long-term profitability for industries. Additionally, the shortage of labor after the COVID-19 pandemic has also led many industries to adopt automation to enhance productivity.

While AI helps companies address market challenges and improve overall productivity, generative AI takes this capability even further. Generative AI empowers businesses to work faster and more creatively, resulting in a significant boost in efficiency for both back-end and front-end operations, leading to meaningful increases in productivity. Moreover, with the world progressively moving towards digitalizing processes and services, the demand for cloud technology services is rising to support the expansion of digital infrastructures as cloud services eliminate the limitations associated with building and maintaining physical data centers, providing a more flexible and efficient solution. So, AWS is well-placed to benefit from these emerging technological trends.

In the previous article, I mentioned the company’s initiatives in launching tools equipped with AI and generative AI. One such tool was Amazon Bedrock, which is a new managed service that provides customers with the simplest way to build and scale enterprise-ready generative AI applications. This tool makes it simple to gain access to leading foundation models (ultra-large machine learning models on which generative AI is based). In the second quarter, the company saw good traction for this newly offered tool backed by AI and ML. Some examples of recent wins include Omnicom, a global marketing and communications company, that opted for AWS generative AI and ML services including Amazon Bedrock, to expedite advertising campaign development. This includes automating tasks such as creative briefs, media plans, ad creation, audience segmentation, and performance measurement. Royal Philips is also utilizing Amazon Bedrock to create a generative AI application for clinical decision support, improving diagnostic accuracy, and automating administrative tasks. Additionally, 3M (MMM) Health Information Systems is leveraging AWS ML and generative AI services, including Amazon Bedrock, Amazon Comprehend Medical, and Amazon Transcribe Medical, to accelerate AI innovation in clinical documentation. Lastly, HSBC launched an AI-powered index using AWS ML services to analyze and learn from data thousands of times faster than humans. This allows the index to adapt automatically as market dynamics change and new information becomes available.

This growing demand and customer traction for new AI tools look encouraging. To further capture this increasing demand, the company expanded its Amazon Bedrock AI tool by introducing more options. The company included Cohere as a foundation model provider in Amazon Bedrock, along with the latest foundation models from Anthropic and Stability AI. AWS also introduced agents for Amazon Bedrock, simplifying the creation of generative AI-based applications that can handle complex tasks and provide customized, real-time answers using proprietary data. Moreover, AWS is also making investments in building its Generative AI Innovation Center. This initiative aims to support customers in developing and deploying generative AI solutions successfully. The program connects AWS AI and ML experts with customers worldwide to collaborate on envisioning, designing, and launching new generative AI products, services, and processes.

I believe, Amazon’s investments in improving AWS’ AI offerings, along with favorable long-term trends in cloud technology adoption and migration, should help the company in delivering consistent growth. These efforts also enable Amazon to manage short-term end-market slowdowns effectively. So, as enterprise customers gradually return to normalized budgets with a moderating inflationary environment and discover the need for AI and generative AI and related cloud services for long-term growth, the AWS segment should see growth reaccelerate in the medium to long term. In the Q2 2023 earnings call, management also mentioned that they are seeing growth rate stabilizing in the second quarter. So, with favorable comparisons in the second half of 2023 and growth rate stabilization, I expect the AWS growth rate to bottom soon, and the tailwinds discussed above should help in reacceleration from there. Hence, I remain optimistic about the company’s overall sales growth prospects moving forward.

Margin Analysis and Outlook

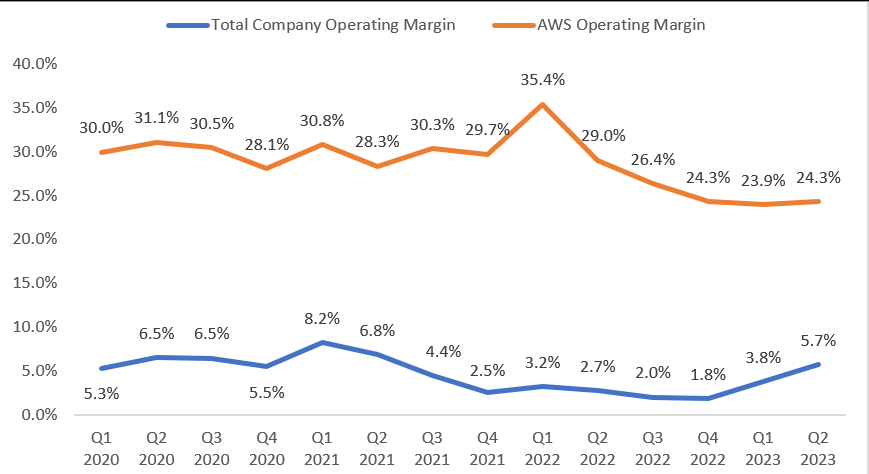

In the second quarter of 2023, the company was able to navigate FX headwinds and cost pressures from elevated investments through sales leverage and cost-saving measures. These cost-saving measures included AMZN’s efforts to regionalize the fulfillment center in order to save on delivery costs and the second quarter proved its success. In addition, improved labor productivity due to easing supply chain conditions and a favorable labor market as compared to the previous year’s quarter also helped in margin recovery. This resulted in a 310 bps year-over-year increase in operating margin to 5.7%

AMZN’s Historical Operating Margin and AWS Operating Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should be able to continue its margin recovery trajectory due to the reacceleration of the sales growth rate as discussed above in the revenue analysis. This should help the company in improving top-line leverage and support margin growth. Moreover, the company is also seeing inflation moderating with fuel prices, linehaul rail rates, and ocean rates easing from their peak levels. This should help the company in delivering margin expansion.

Furthermore, the transition of the fulfillment and transportation network in the United States from a single national network to a series of eight separate regions serving smaller geographic areas is bearing fruit. This resulted in a 19% YoY reduction in miles traveled to deliver packages to customers in the second quarter and a more than 1,000 bps YoY increase in deliveries fulfilled within the region, to 76%. Management sees the second quarter as just the beginning of multi-year cost-saving benefits and expects delivery and transportation costs to further reduce as these regional centers become efficient in their operations. Additionally, the AWS segment is the largest contributor to operating profit. So, with growth rates stabilizing and the expected re-acceleration moving forward, the company should see further support from the segment for the overall margin growth. Hence, I remain optimistic about the company’s margin growth prospects ahead.

Valuation and Conclusion

Amazon is currently trading at a P/E ratio of 66.04x FY23 consensus EPS estimate of $2.12 and a forward P/E ratio of 47.36x the FY24 consensus EPS estimate of $2.95. These figures represent a discount compared to its historical 5-year average forward P/E ratio of 189.4x. Similarly, the company’s forward EV/EBITDA and EV/Sales valuation metrics are also trading below its historical average. The company’s forward EV/EBITDA is 15.71x compared to its 5-year historical average of 22.08x and its forward EV/Sales of 2.58x is also below its historical average of 3.41x.

The company has good growth prospects as the growth of the e-commerce retail business and AWS is expected to re-accelerate moving forward. This coupled with improving margins due to cost-saving initiatives and a favorable cost environment, makes the overall growth prospects even more compelling. I believe the stock’s valuation multiples should re-rate going forward as its growth rates improve. Hence, I believe the stock represents a good buying opportunity due to its favorable valuation and long-term growth prospects.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article is written by Saloni V.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.