Summary:

- Amazon’s stock has surged by 83% year-to-date, marking its best performance since 2015.

- Amazon’s Q3 2023 is a testament to its remarkable success across all segments, with significant growth in net sales, operating income, and EPS.

- Analysts anticipate continued growth for Amazon’s AWS business, driven by the integration of AI solutions.

- Amazon’s stock is currently cheap compared to its historical valuation, and I expect with the Fed cutting rates in 2024, its valuation will expand.

- Anticipating an EPS of $3.73 in 2024 and considering a Forward PE of 60x, my projected price target for 2024 lands at $224.

David Ryder

As a dividend growth investor, the common belief is that companies not paying dividends don’t fit into a portfolio centered on dividend growth.

I beg to differ.

Numerous outstanding companies exist that currently don’t pay dividends and may not in the foreseeable future. Despite this, I choose to include the best of them in my portfolio due to their exceptional quality and substantial growth potential.

Ultimately, the dividend yield reflects an average of all holdings in one’s portfolio.

Take Amazon.com Inc. (NASDAQ:AMZN) as a prime example — synonymous with quality and a ‘must-have’ for investors seeking growth.

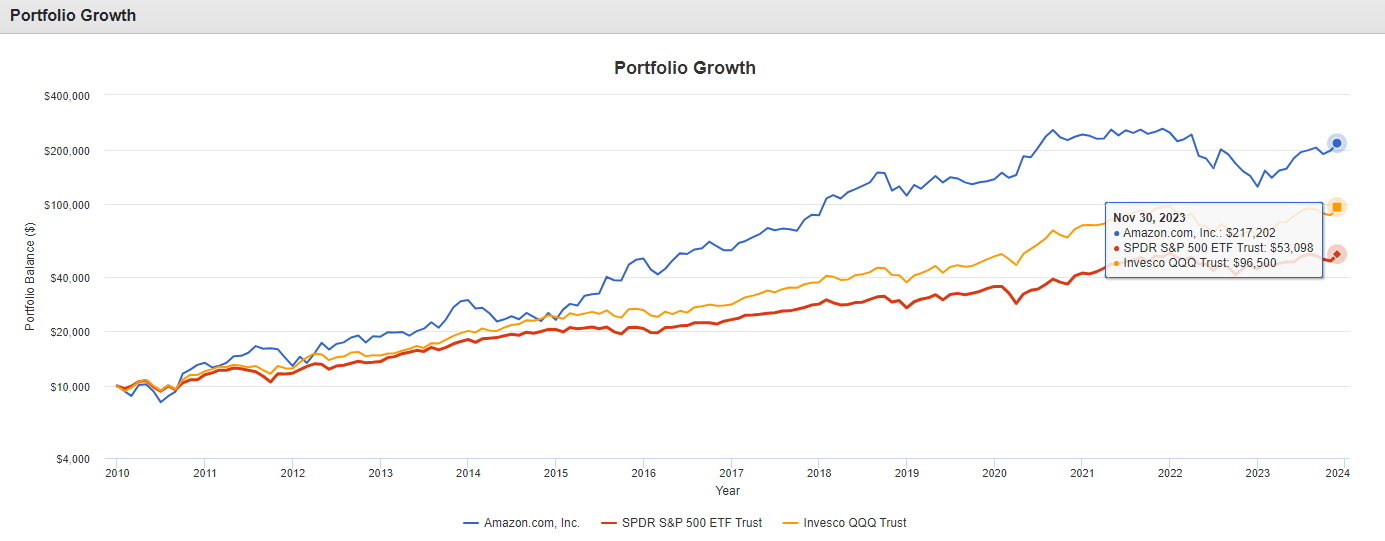

Consider this scenario: if you had invested $10,000 in 2010 and reinvested all the dividends into Amazon, S&P 500 (SPY), and Nasdaq 100 (QQQ), your returns would be as follows:

- AMZN: $217,202, or 24.8% CAGR

- SPY: $53,098, or 12.8% CAGR

- QQQ: $96,500 or 17.7% CAGR

$10,000 Growth Since 2010 (Portfolio Visualizer)

Having followed Amazon for more than a decade and holding it in my portfolio since 2015, I am writing my initial coverage of the company, assigning it an outperform rating heading into 2024.

I view Amazon as being currently undervalued in light of its growth potential, and with the rate cuts coming in 2024, expect valuation expansion and significant growth ahead fueled by demand in its retail business and by AI tailwinds in Amazon Web Services or “AWS”.

83% Gain Year-To-Date Without A Slow-Down In Sight

Amazon’s stock surged during the pandemic as the demand for e-commerce soared. However, as the Fed began raising rates and economic worries surfaced in 2022, the shares plummeted by 49%.

This year tells a very different story. Amazon’s shares have skyrocketed by 83% year-to-date, marking its best performance since 2015, as well as overtaking FedEx (FDX) and UPS (UPS) as the US’s No. 1 delivery business. Its market cap is now nearing $1.6 trillion, making it the fourth-largest stock in the S&P 500, trailing right behind Google’s (GOOGL) A and B shares.

You might be curious about expecting another stellar year for Amazon after its 2023 success. Yet, Amazon plans to leverage this year’s gains by solidifying its leadership position and capitalizing on generative AI. It aims to enhance the profitability of its colossal online retail operations while setting the stage for continued growth.

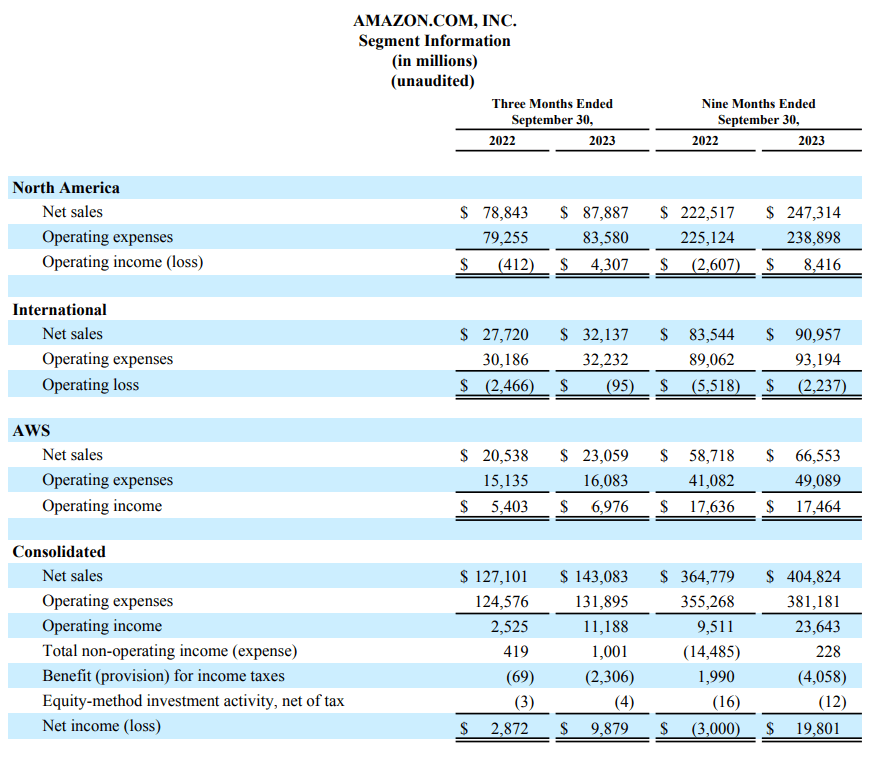

Amazon’s Q3 2023 results showcase their remarkable success across various fronts and confirm the positive momentum.

In the retail sector, the cost-to-serve, and delivery speed took significant strides forward, while AWS saw stabilized growth and advertising revenue experienced robust expansion. Overall, operating income and free cash flow saw notable increases.

The Q3 net sales reached $143.1 billion, marking a 13% increase from Q3 2022’s $127.1 billion. Adjusted for a $1.4 billion favorable impact from changes in foreign exchange rates, net sales grew by 11% compared to the same period last year.

Operating income surged, surpassing fourfold to $11.2 billion in Q3 2023 from $2.5 billion in Q3 2022, driven by strong performances in both the retail and AWS sectors.

This successful quarter translated to an increase in net income, reaching $9.9 billion in Q3 2023, or $0.94 per diluted share, compared to $2.9 billion, or $0.28 per diluted share, in Q3 2022.

Financial Statement (AMZN IR)

Operating cash flow witnessed a staggering 81% increase, totaling $71.7 billion for the trailing twelve months ending September 30, 2023, compared to $39.7 billion for the same period in 2022.

Amazon is firing on all cylinders, witnessing growth and remarkable operational efficiency across all its businesses. Looking ahead, the spotlight for the upcoming year will focus on AI’s integration into AWS.

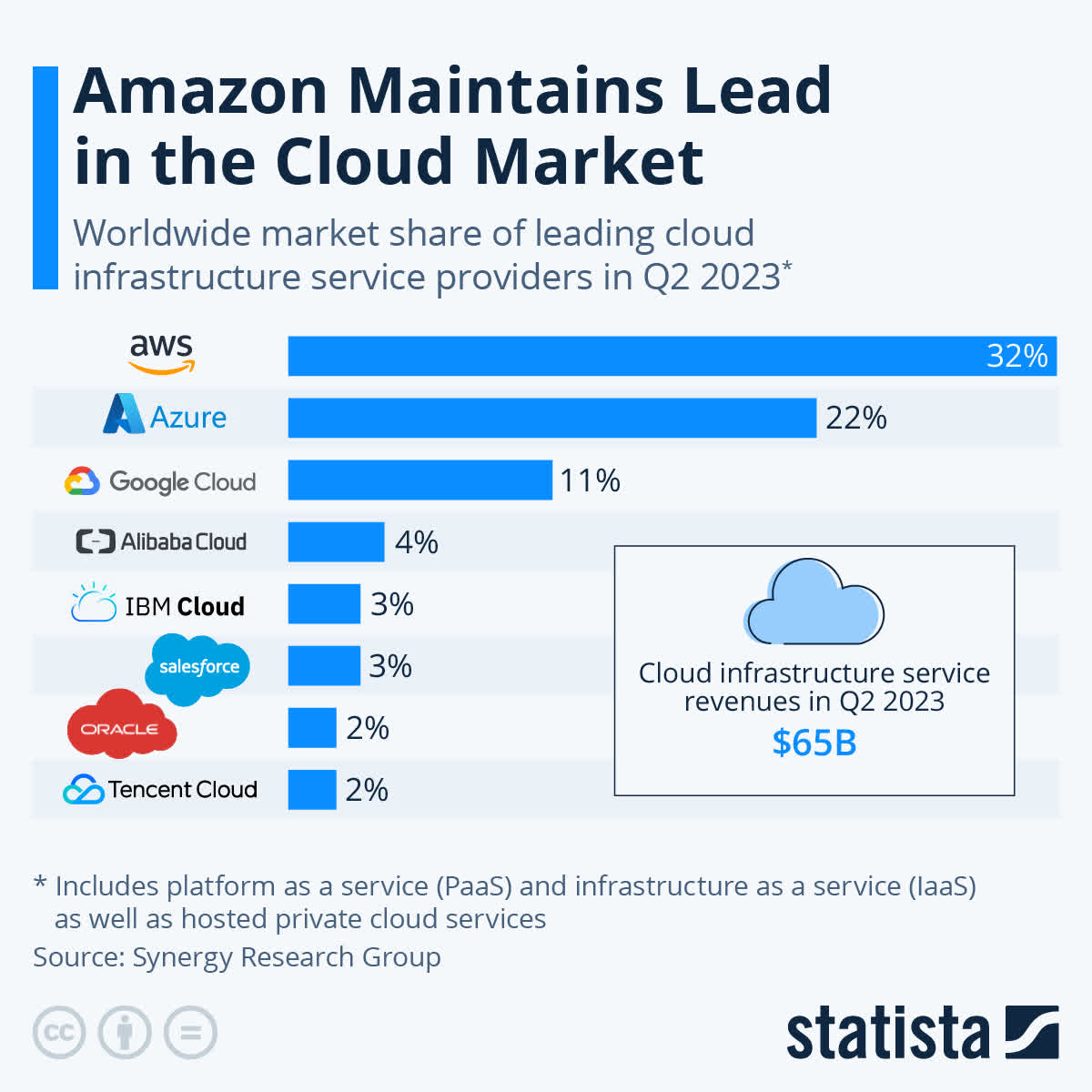

Recently, Amazon revealed a suite of new AI-centric products tailored for its expansive cloud computing division, AWS. During its annual re:Invent conference in late November, AWS leaders introduced a new chatbot for businesses, a deeper collaboration with Nvidia (NVDA), a frontrunner in AI chip technology, and an updated version of its own AI chip.

These product launches underline Amazon’s commitment to maintaining its dominance in the cloud services provider arena. As of Q2 2023, Amazon held a 32% market share, with Microsoft’s Azure (MSFT) following at 22% and Google’s Cloud at 11%.

Analysts expect AWS to continue growing as more companies embrace compute-intensive generative AI products, capitalizing on its already substantial size and market share.

Cloud Market Share (Statista)

The 2024 AI-focused narrative surrounding AWS brings up a recurring point often discussed here on Seeking Alpha: when you invest in Amazon’s stock, you’re essentially investing heavily in the AWS Business, while acquiring the Retail and Advertising Business at a discount.

I agree with this statement to some extent, and here’s why:

During Q3 2023, AWS generated $6.976 billion in Operating Income, standing out as Amazon’s most lucrative business, accounting for over 62% of the total $11.188 billion operating income in the quarter.

While reaching the net income involves further deductions for non-operating income impacts and taxes, a rough estimate suggests that AWS contributed around $0.58 or 62% to the $0.94 diluted EPS for the quarter.

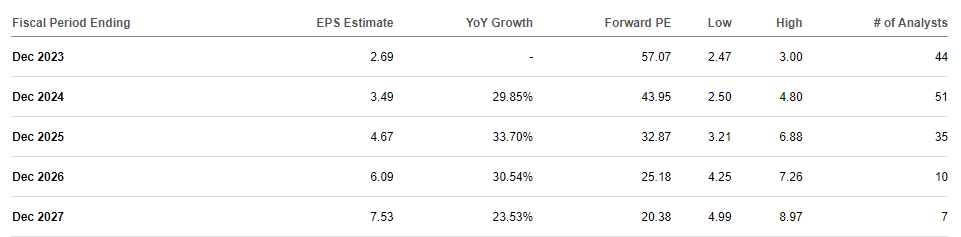

Assuming a similar performance for the next three quarters, we could project an AWS EPS of $2.32 for FY24. For Retail and Advertising businesses, an anticipated EPS of $1.41 over the next four quarters seems reasonable, summing up to a total FY24 EPS of $3.73.

Despite analysts forecasting an EPS of $3.49 in FY24, I hold the view that Amazon might surpass this estimate slightly. This belief rests on the foundation of AI advancements driving growth and a robust growth anticipated in both AWS and retail businesses, bolstered by the Fed’s rate cuts.

EPS Projections (Seeking Alpha)

The current stock price stands at $153, and based on an anticipated FY24 EPS of $3.73, the Forward PE ratio rests at 41x, notably below its historical norms.

With an expected EPS growth of 38.6% from FY23 to FY24 and no indication of growth slowing down due to improved operational efficiency, I propose that the stock should ideally be valued at around 60x its forward earnings.

Should the valuation indeed expand to 60x its FY24 earnings of $3.73, my projected price target would be $224 by the end of 2024. This estimation suggests a potential stock appreciation of 46% from today’s price.

| Fiscal Year | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue (b) | $ 636.3 | $ 710.1 | $ 792.1 | $ 877.6 | $ 976.5 |

| Revenue Growth | 11.5% | 11.6% | 11.5% | 10.8% | 11.3% |

| EPS | $ 3.7 | $ 4.7 | $ 6.1 | $ 7.5 | $ 9.2 |

| EPS Growth | 38.6% | 25.2% | 30.4% | 23.6% | 22.7% |

| Forward PE | 60.0 | 55.0 | 55.0 | 50.0 | 45.0 |

| Stock Price | $ 224 | $ 257 | $ 335 | $ 377 | $ 416 |

As anticipated, the EPS growth is projected to persist in the coming years. Analyst estimates spanning from 2025 to 2028 suggest an average EPS growth of approximately 25.5%.

However, considering a slight decline in this growth trajectory, I foresee a contraction in valuation towards 45x its forward earnings by 2028. This adjustment would potentially lead to a stock price of $416.

While my scenario leans toward heavy bullishness, it’s important to acknowledge the various risks that could potentially impede valuation expansion.

Nevertheless, I firmly believe Amazon is presently trading at a discounted rate compared to its historical valuation. This assumption hinges on the expectation of robust EPS growth and the company’s transition into a new phase of its life cycle characterized by significant improvements in operational efficiency, driving the bottom line of the business.

To put it into perspective, Amazon has earned a place on multiple lucrative top-pick lists for 2024 curated by Wall Street:

- TD Cowen has designated Amazon as its top large-cap pick.

- Bernstein recognizes Amazon as its “Best Idea” among internet stocks.

- Since August, Wedbush has consistently named Amazon as its “Best Idea.”

- Needham includes Amazon among its selection of top big tech companies, alongside Google.

Risks To My Bullish Thesis

At the moment, Amazon is gearing up for what could potentially be the most significant legal battle in its three-decade history. Regulators are questioning the company’s market dominance, signaling that Amazon might face substantial scrutiny in the years ahead.

The FTC alleges that the company has leveraged its market authority to inflate prices and overcharge merchants.

In an October 3 client note, JPMorgan expressed that the lawsuit “was largely anticipated, and anticipates difficulties in proving that AMZN unlawfully sustains monopoly power.”

Simultaneously, the risk of an economic slowdown could act as a brake on Amazon’s growth, impacting both its retail and AWS businesses. This risk remains, even if the Fed successfully engineers a soft landing in 2024, yet the GDP contracts more than expected.

Takeaway

After a challenging 2022, Amazon has bounced back, surging by 83% year-to-date.

This upswing isn’t driven by FOMO or market hysteria. Instead, the business is firing on all cylinders, witnessing recovery and growth across AWS, Retail, and Advertising sectors.

I anticipate Amazon will capitalize on this momentum, marking 2024 as the onset of a new era focused on operational efficiency, paving the way for significant profitability.

Presently, the valuation falls below historical averages. With expected rate cuts in 2024, I foresee valuation expansion, leading me to a bullish price target of $220 by the end of 2024, with further growth potential ahead.

While I find the valuation of many businesses appealing, Amazon holds a spot among my top 5 picks for 2024. I anticipate a substantial rally and significant stock appreciation for the company.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN, GOOG, MSFT, NVDA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.