With Q1 revenues and earnings coming ahead of expectations, Amazon’s stock popped up +12% in yesterday’s after-hours session before surrendering all the gains during the earnings call.

AWS’s revenue growth slowed down to 16% y/y in Q1, with margins getting squeezed. Furthermore, Amazon’s CFO said AWS growth had slowed by another 500 bps in April 2023.

According to Amazon’s management, AWS has a long runway for growth, and this slowdown is temporary. However, Amazon’s competitors – Microsoft and Google – did not dole out such warnings.

As of Q1, Amazon’s business is rebounding nicely after a tough 2022, and the stock remains undervalued. However, the drastic AWS slowdown is troublesome, and I think investors could get better buying opportunities in this stock over the next 6-12 months.

Spoiler Alert: I rate Amazon a “Buy” in the low $100s, with a strong preference for staggered accumulation.

4kodiak

Brief Review Of Amazon’s Q1 2023 Report

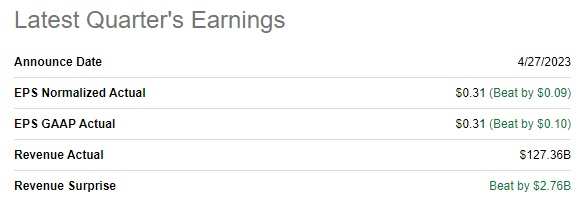

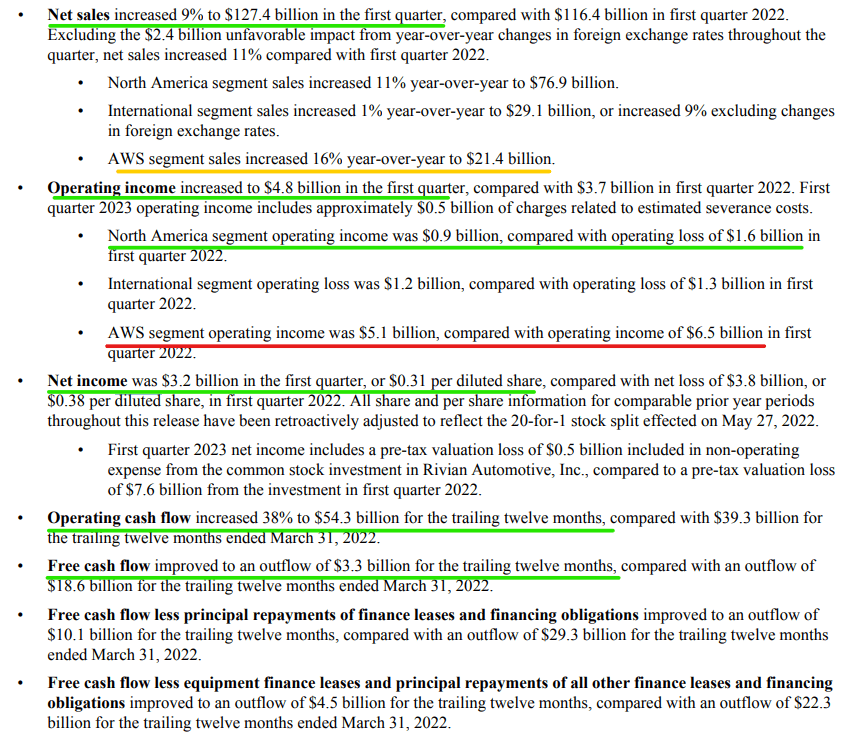

For Q1 2023, Amazon (NASDAQ:AMZN) reported revenues of $127.36B (up +9% y/y), beating street estimates of $124.47B by ~2.3%. While the revenue beat was solid, Amazon’s unexpected earnings beat was more impressive, with the company reporting an EPS of $0.31 (vs. est. $0.21). During Q1, Amazon’s operating income rebounded to +$4.8B, with a sharp rise in TTM operating cash flow to $54.3B.

SeekingAlpha

Amazon’s Q1 2023 Earnings Release

As you can see above, Amazon is re-accelerating top-line growth whilst improving profitability. Here’s what Amazon’s CEO, Andy Jassy, had to say about this quarter:

There’s a lot to like about how our teams are delivering for customers, particularly amidst an uncertain economy. Our Stores business is continuing to improve the cost to serve in our fulfillment network while increasing the speed with which we get products into the hands of customers (we expect to have our fastest Prime delivery speeds ever in 2023). Our Advertising business continues to deliver robust growth, largely due to our ongoing machine learning investments that help customers see relevant information when they engage with us, which in turn delivers unusually strong results for brands.

And, while our AWS business navigates companies spending more cautiously in this macro environment, we continue to prioritize building long-term customer relationships both by helping customers save money and enabling them to more easily leverage technologies like Large Language Models and Generative AI with our uniquely cost-effective machine learning chips (“Trainium” and “Inferentia”), managed Large Language Models (“Bedrock”), and AI code companion CodeWhisperer. We like the fundamentals we’re seeing in AWS, and believe there’s much growth ahead.

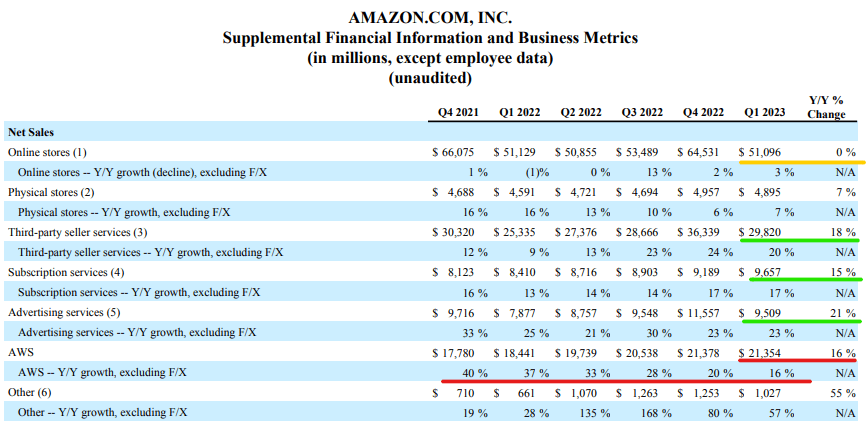

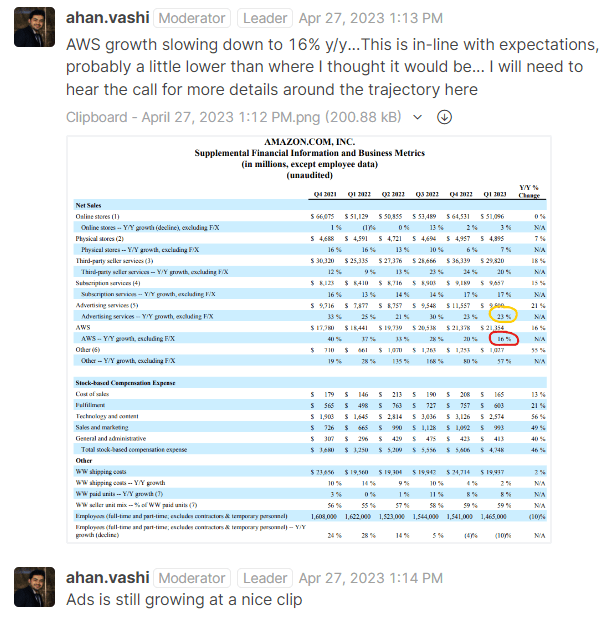

As you can see below, Amazon’s retail business is still digesting pandemic-era growth, and the twin growth engines – AWS and Ads – are slowing down. While Amazon’s Ads revenue is still growing at a healthy clip (~21% y/y), AWS is clearly struggling in this environment. That said, Amazon’s total revenues are seeing a growth re-acceleration as the company laps easier comps after a dreadful 2022, with some macro headwinds like high inflation, rising interest rates, and strengthening US dollar also turning into tailwinds in 2023.

Amazon’s Q1 2023 Earnings Release

Now, as soon as Amazon reported a double beat on revenue and earnings, its stock popped up by ~12% in yesterday’s after-hours session, with Mr. Market seemingly impressed by the Q1 report and forward guidance.

Amazon’s Q1 2023 Earnings Release

However, these gains proved to be short-lived, and Amazon ended the after-hours session in the red. Are you curious to learn what drove the turnaround in Amazon’s stock? Let’s dive into Amazon’s Q1 report to understand what went wrong.

While Amazon easily beat revenue guidance in Q1, AWS seems to be buckling under macro pressures, with growth in Amazon’s cloud business slowing down to 16% y/y. At TQI, our investment thesis for Amazon relies upon AWS and Ads. And so, whilst breaking down the report for our subscribers in TQI’s Earnings Analysis chat channel, I expressed concerns about AWS’s slowdown and margin contraction (at the time, the stock was still trading up ~9% AH):

TQI’s Earnings Analysis Channel

TQI’s Earnings Analysis Channel

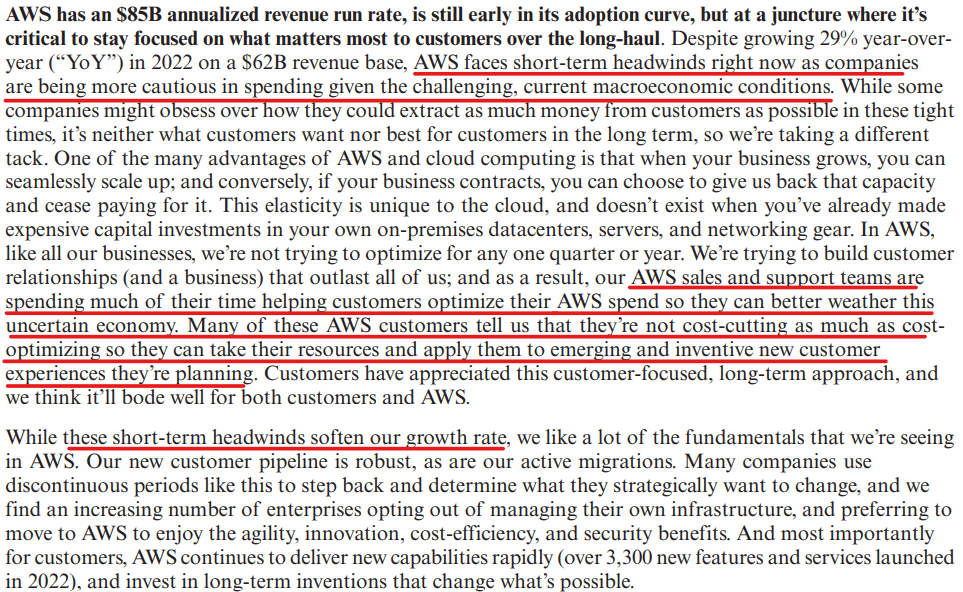

Now, Jassy had already warned us about the slowdown in AWS via his second annual shareholder letter. And despite Amazon’s AWS revenue slowdown and margin contraction looking like a negative surprise to many, we expected this to be the case heading into this quarterly report (and so did the market) –

AWS (cloud): AWS has served as the profit center at Amazon for several years and enabled the spectacular expansion of its retail ecosystem and other business lines. In 2022, AWS achieved record revenues of $80B, and this business is currently running at an ARR of $85B. However, AWS’ growth has been decelerating for multiple quarters now, and this trend is set to continue in 2023, according to Jassy:

Amazon Shareholder Letter 2022

While AWS is still projected to grow at a healthy clip, I think its profit margins are set to come under pressure as customers reduce/optimize spend on the cloud services platform. The slowdown at AWS may only be temporary, given the massive runway ahead (90% of Global IT spend is still on-premise); however, the impact of this slowdown on Amazon’s overall profitability in 2023 is undoubtedly going to be outsized.

With the slowdown in AWS being well-telegraphed by Amazon’s management, why did AMZN stock lose all of its post-ER gains during the earnings conference call yesterday?

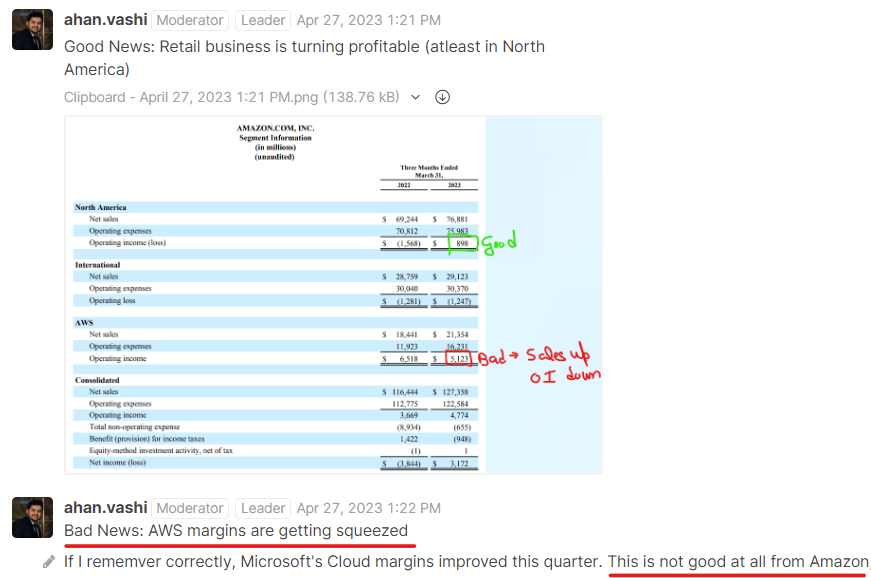

Well, after delivering some good (retail business profitability) and bad news (AWS slowdown and margin contraction) about their business, Amazon’s CFO, Brian Olavsky, dished out a new warning during the earnings call –

Customers continue to evaluate ways to optimize their cloud spending in response to these tough economic conditions in Q1 and we are seeing these optimizations continue into Q2 with April revenue growth rates about 500bps lower than what we saw in Q1

Considering AWS’s Q1 revenue growth rate of 16% y/y, a further 500 bps decline in growth rates would peg AWS’s revenue growth rate at ~11% y/y in Q2, which is barely in the double digits. That’s a drastic slowdown for AWS, and while it may be temporary, this is undoubtedly a dent in our investment thesis.

A usage-based model allows customers to scale up and scale down as required, and this dynamic could inflict a lot of pain on AWS (and other cloud infrastructure services providers like Azure and GCP) in the event of an economic contraction. While we saw a deceleration in growth rates at Alphabet’s and Microsoft’s respective cloud businesses during Q1, the guidance for these companies’ cloud revenues and margins is nothing like Amazon’s poor guidance. And I think this is the ugly part of Amazon’s Q1 report!

Now, despite AWS suffering growth slowdown and margin compression, Amazon’s stock remains undervalued and offers robust long-term returns.

Amazon’s Stock Remains Attractive

Before we look at Amazon’s technical charts and quant factors grades to understand the near-term outlook for the stock, let’s evaluate Amazon’s fair value using a long-term perspective.

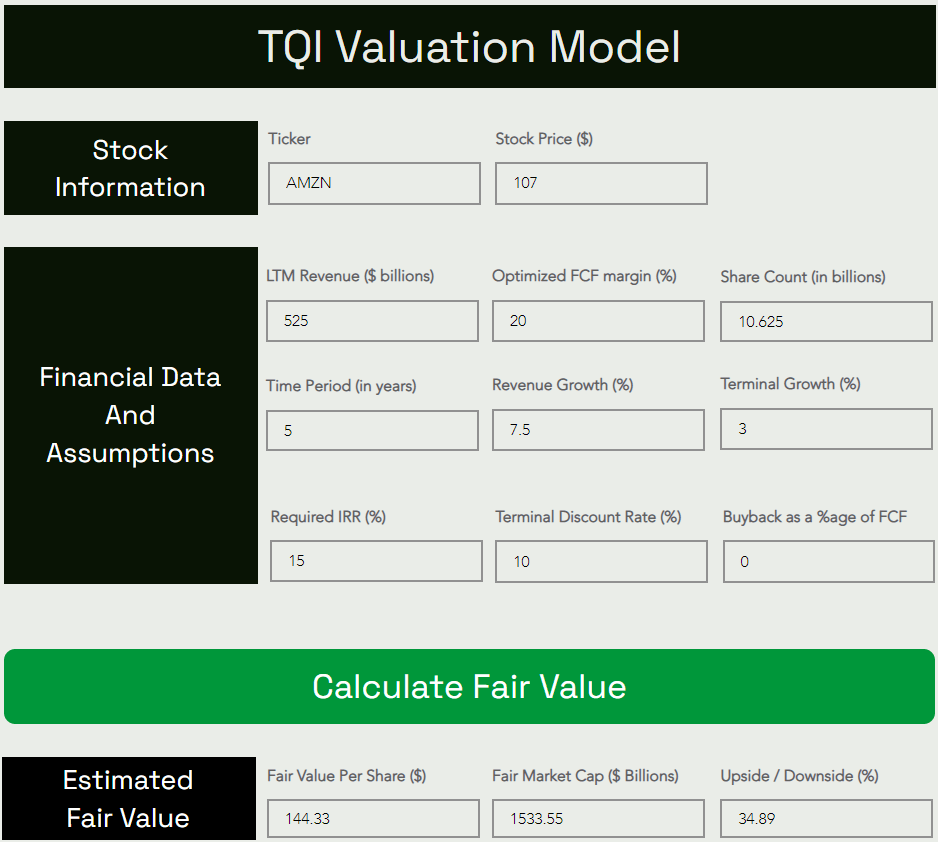

Here’s my updated valuation model for Amazon in light of Q1 earnings:

TQI Valuation Model (TQIG.org)

According to TQI’s Valuation Model, Amazon’s fair value is ~$144 per share (or $1.53T). With the stock trading at ~$107 per share, AMZN is trading at a hefty (35%) discount to its intrinsic value.

To build a margin of safety into our valuation model for Amazon, I have assumed a 5-yr CAGR growth rate of just 7.5% (vs. current consensus analyst estimates of ~11%). While AMZN bears may disagree with a steady-state free cash flow margin of 20%, I think Amazon’s high-margin segments, i.e., AWS and Ads, can lead FCF margins even higher than 20% over the long run. All other assumptions are relatively straightforward, but if you have any questions, please feel free to share them in the comments section.

Predicting where a stock would trade in the short term is impossible; however, over the long run, a stock would track its business fundamentals and obey the immutable laws of money. If the interest rates were to stay depressed, higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the long-term average of ~5%. By inverting this figure, we get a trading multiple of ~20x.

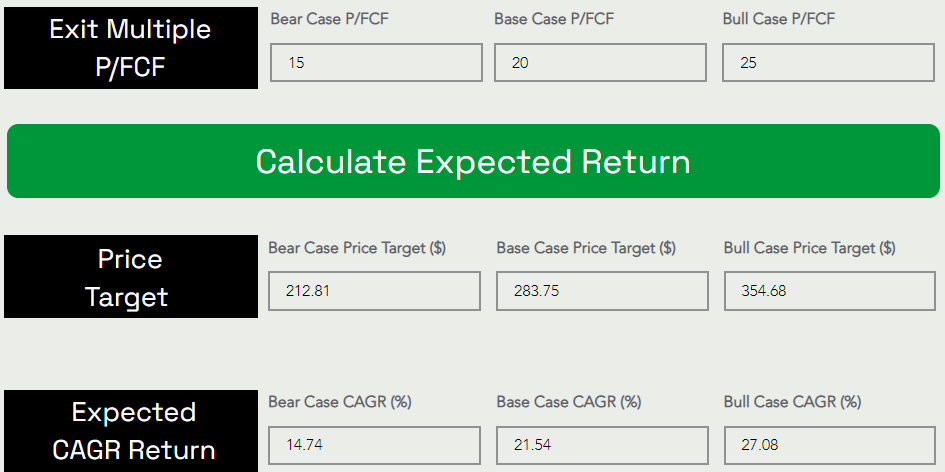

Assuming an exit multiple of 20x P/FCF, I can see Amazon’s stock price rising from $107 to $284 by the end of 2027-28.

TQI Valuation Model (TQIG.org)

As shown above, Amazon’s stock offers a 5-yr CAGR return of 21.54%, which far exceeds my investment hurdle rate of 15%. And this is why I continue to believe that Amazon is a solid buy at current levels.

With today’s update, our base case 5-yr price target for Amazon has shifted from $333 to $284. This downshift is a result of reducing our “Buyback as a % of FCF” from 50% to 0%. While I continue to believe that Amazon will turn into a free cash flow machine over the next few years, AWS’ drastic slowdown and unexpected margin compression warrant this additional caution.

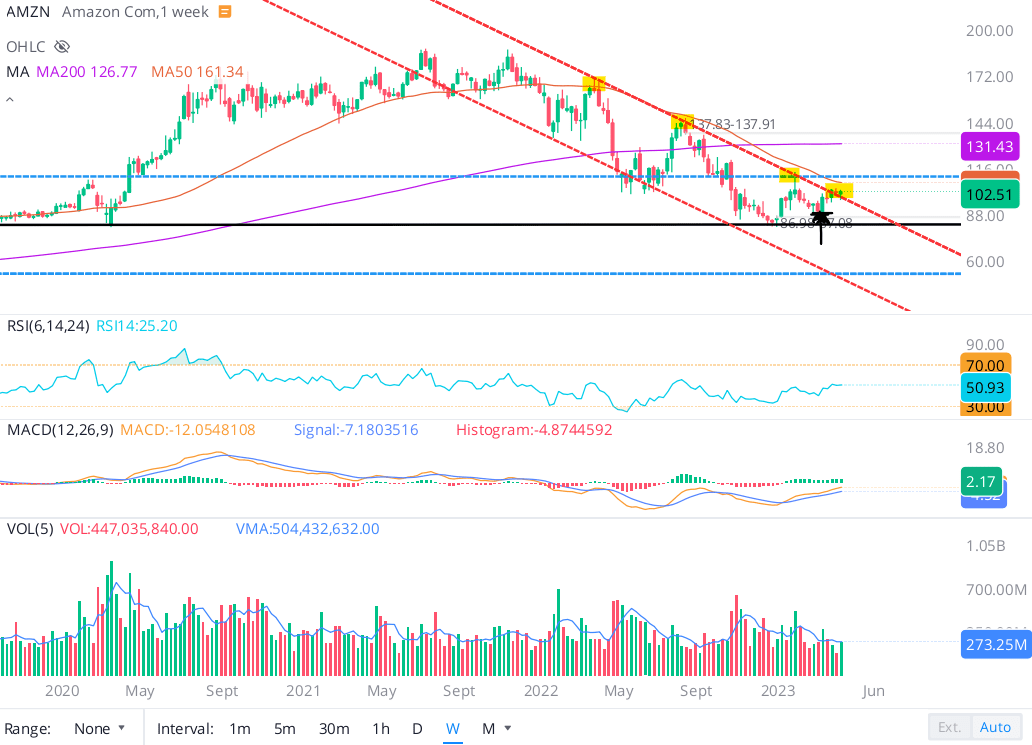

Amazon’s stock has been undergoing a complex correction for nearly two years now, with its trading multiples normalizing in a higher interest rate environment. In my last update on Amazon, I wrote the following:

After getting rejected from the upper trendline of the falling downward channel (marked in dotted red), AMZN looks nailed on to re-test its recent lows in the low to mid $80s.

WeBull Desktop

As pointed out in my previous note, Amazon’s stock held multi-year support at $80 and bounced off this level. After a sharp 16%+ YTD bounce, Amazon looks primed to re-test the $100-$105 range in the coming weeks. If the stock fails to break this level, I would expect it to remain rangebound in the $80-$100 range.

And for now, I stick to this call for Amazon to remain rangebound in the $80-$100 range. If Amazon were to break down the multi-year support in the low $80s, then we could see the stock slide down to the next big support zone on the chart, which is in the $50s. Now, I do not expect Amazon to go this low until and unless we have a deep, deep recession!

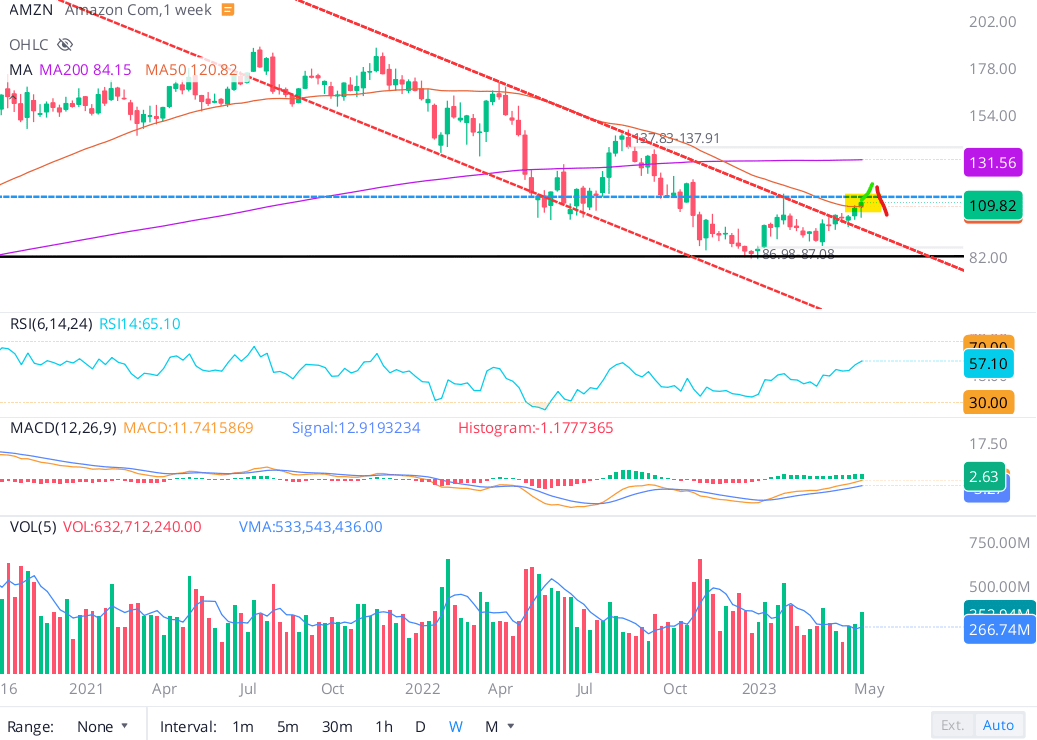

Since that call in mid-February, Amazon’s stock went down to ~$87-88 level before rebounding back to ~$100. And then last Friday, Amazon’s stock bounced up above the $100 level in what appears to be a potential breakout.

WeBull Desktop

With mega-cap tech names enjoying a wild run so far in 2023, Amazon bulls are yearning for an upside breakout from the $80-100 range, and I am certainly a part of this hopeful camp. If we do break out to the upside, the first target would be the ~$120-140 range. On the flip side, a breakdown back below $100 could see Amazon resume its rangebound action, and we could very well get that re-test of recent lows in the low-to-mid $80s. In my opinion, Amazon’s upcoming quarterly report could prove to be decisive in determining the future path of its stock.

After the release of its quarterly report, Amazon’s stock jumped +12% to hit the $120 level; however, the stock reversed during the earnings call and ended the after-hours session in the red. We already know that the sharp reversal was driven by management’s commentary on a further slowdown in AWS; however, technically, this leaves Amazon’s stock at a key pivot level at ~$110. If AMZN manages to break above this level, we could be headed to the $120-140 target range.

WeBull Desktop

However, a breakdown below $100 could ensure more rangebound action in the $80-100 consolidation range AMZN has traded in over the last several months. With Amazon’s profit center [AWS] showing a slowdown and margin contraction, I think the risk here is tilted to the downside. That said, Amazon’s technical chart is finely poised for now, and we will be watching the stock closely to see which way this one breaks.

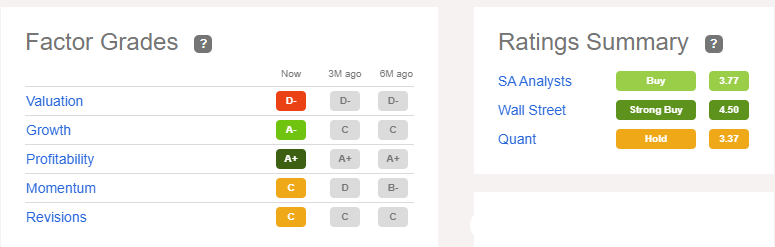

According to Seeking Alpha’s Quant Rating system, Amazon is rated a “Hold” with a score of 3.37/5. As we have remarked in the past, Amazon’s quant factor grades have been trending in the right direction in recent months.

SeekingAlpha

Until recently, Amazon’s “Profitability” grade of “A+” was looking iffy; however, Amazon’s return to positive net income (and strong operating cash flow generation) in Q1 is justifying the profitability grade. With the stock doing well since the turn of the year, Amazon’s “Momentum” grade has improved from “D” to “C”. Lastly, AMZN’s “Valuation” and “Revisions” grades have held up firmly. Despite Amazon’s quant factor grades heading in the right direction, they still do not support a fresh long position at current levels.

Concluding Thoughts

Based on a mix of fundamental, quantitative, and technical data analysis, Amazon’s stock remains a solid long-term buy at current levels. Yesterday’s Q1 report showcased a continued rebound in Amazon’s business after a disastrous 2022, with revenues and EPS coming in ahead of expectations. However, AWS’s drastic growth slowdown and margin contraction are alarming, and it should be enough to test the resolve of Amazon’s shareholder base.

As we noted in this article, Amazon’s stock remains undervalued, and the long-term risk/reward looks attractive. That said, given the heightened business uncertainty, AMZN could provide better buying opportunities (entry points) over the coming months. Hence I strongly prefer a staggered accumulation of AMZN shares over 6-12 months over a lump sum investment into the stock.

Key Takeaway: I rate Amazon a “Buy” in the low $100s, with a strong preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking to upgrade your investing operations?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

We have recently reduced our subscription prices to make our community more accessible. TQI’s annual membership now costs only $480 (or $50 per month) for a limited period only.