Amazon is closing in on $150 per share as investors react positively to reports of strong Black Friday and Cyber Monday online sales.

Despite ongoing macroeconomic uncertainties, Amazon’s business momentum is getting stronger, with stabilization at AWS and robust growth in the Ads business.

According to our valuation model, Amazon’s fair value is around $171 per share and its expected 5-year return is ~18% (far greater than long-term S&P 500 returns of ~8-10%).

While a pullback is certainly a possibility after a +25% jump in AMZN since late October 2023, Amazon’s longer-term technical setup remains bullish, and I can see AMZN making an attempt to test its all-time high ($188.95 per share) within the next 6-12 months.

Henceforth, I continue to rate Amazon a “Buy” at $148 per share, with a preference for staggered buying via DCA.

4kodiak/iStock Unreleased via Getty Images

Introduction

Yesterday, Amazon (NASDAQ:AMZN) stock climbed closer to my year-end price target of $150 per share as investors cheered strong Black Friday and Cyber Monday online sales numbers. According to Adobe Analytics, Black Friday online shopping hit a new record of $9.8B (up 7.5% y/y), with Cyber Monday set to be this year’s biggest online shopping day at $12B (up 6.1% y/y). Given its dominant position in e-commerce, Amazon is an obvious beneficiary of stronger-than-expected online consumer spending.

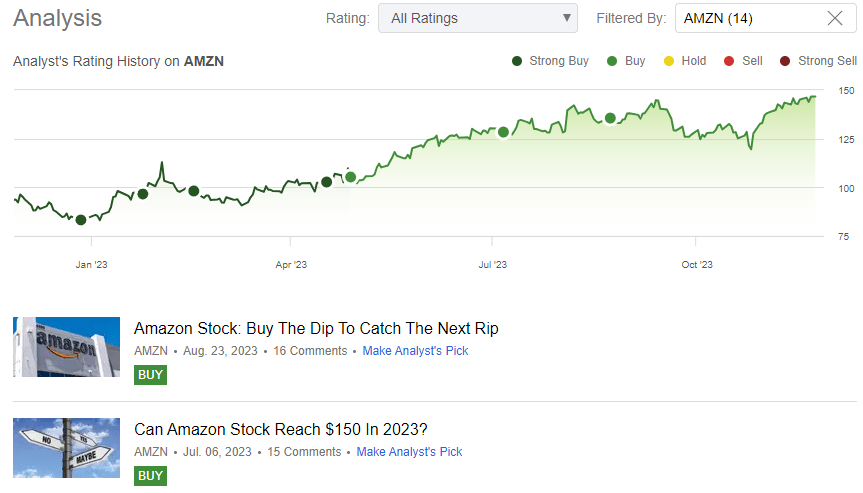

As you can see below, I have published multiple “Strong Buy / Buy” ratings on Amazon over the past year. Back in July, I laid out the path for Amazon stock to hit $150 by year-end in Can Amazon Stock Reach $150 in 2023?:

In an earlier section of this note, we reviewed Amazon’s intrinsic value estimate, which stands at ~$151 per share. Given AMZN’s improving fundamentals, technicals, and quant factor grades, I think there’s a good chance the stock takes a run at its fair value in the near future.

While Amazon’s risk/reward is not as good as it was a couple of months ago, rising investor interest in generative AI and current momentum in AMZN stock (and the tech sector in general) could continue to power it higher in the back half of 2023.

Author’s AMZN Ratings (Seeking Alpha)

Now that we are sitting within touching distance of my year-end price target for 2023, I would like to provide an update on Amazon. In this note, we will review Amazon’s progress through its Q3 2023 earnings report, re-run it through our valuation model, and analyze AMZN’s technical charts & quant factor grades. Without further ado, let’s get started!

Brief Review of Amazon’s Q3 Earnings Report

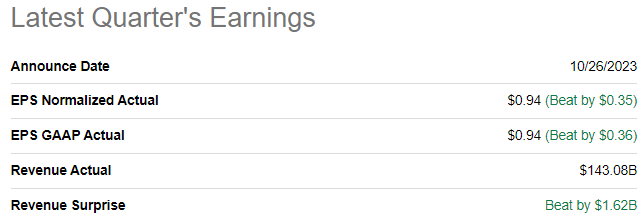

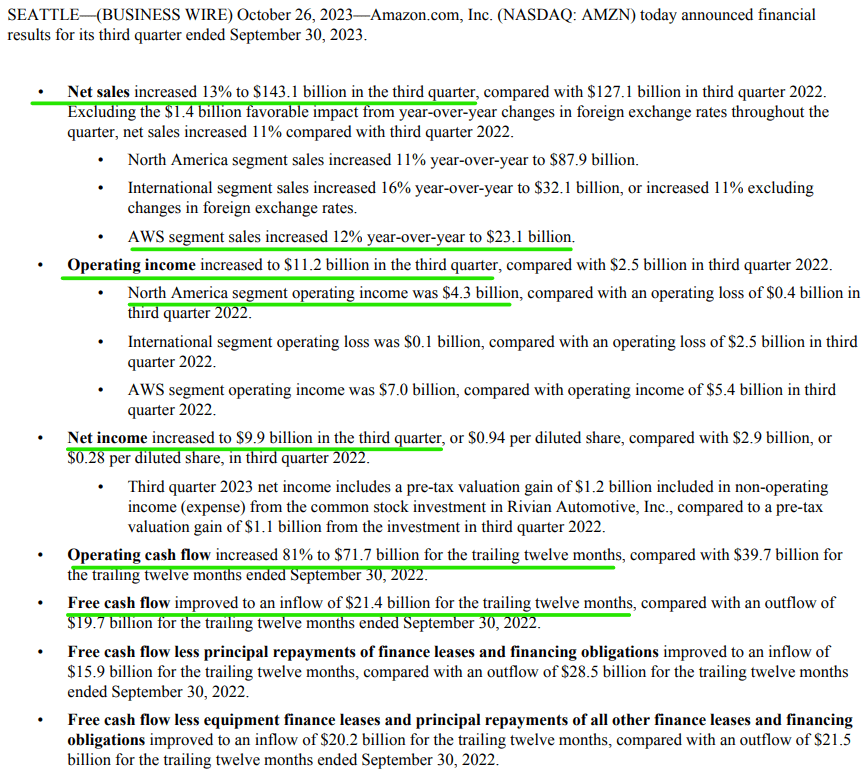

In late October, Amazon reported stronger-than-expected financial results for Q3 2023, with revenues of $143.08B (up +13% y/y) hitting the top end of management’s guidance range and coming in well ahead of consensus street estimates of $141.46B on the back of growth stabilization at AWS, strong performance in digital Ads, and continued momentum within its retail ecosystem. Also, powered by strong top-line performance, the tech conglomerate obliterated consensus expectations on earnings, with normalized EPS for Q3 coming in at $0.94 (vs. Street estimates of $0.59).

Seeking Alpha

Amazon Q3 2023 Earnings Press Release

During Q3 2023, Amazon’s operating income increased to +$11.2B, driving TTM operating cash flow higher to $71.7B (up +81% y/y). Furthermore, Amazon’s TTM free cash flow rose to $21.4B (up from $7.9B in Q2 2023). Clearly, Amazon is proving itself as a massive cash cow!

Here’s what Amazon’s CEO, Andy Jassy, had to say about this quarter:

We had a strong third quarter as our cost to serve and speed of delivery in our Stores business took another step forward, our AWS growth continued to stabilize, our Advertising revenue grew robustly, and overall operating income and free cash flow rose significantly.

The benefits of moving from a single national fulfillment network in the U.S. to eight distinct regions are exceeding our optimistic expectations, and perhaps most importantly, putting us on pace to deliver the fastest delivery speeds for Prime customers in our 29-year history.

The AWS team continues to innovate and deliver at a rapid clip, particularly in generative AI, where the combination of our custom AI chips, Amazon Bedrock being the easiest and most flexible way to build and deploy generative AI applications, and our coding companion (CodeWhisperer) allowing enterprises to have the equivalent of an experienced engineer who understands all of their proprietary code is driving momentum with customers, including adidas, Booking.com, GoDaddy, LexisNexis, Merck, Royal Philips, and United Airlines, all of whom are starting to run generative AI workloads on AWS.

Between AWS re:Invent and our 29th holiday shopping season, this is a particularly action-packed time of year at Amazon and we’re excited for what’s to come

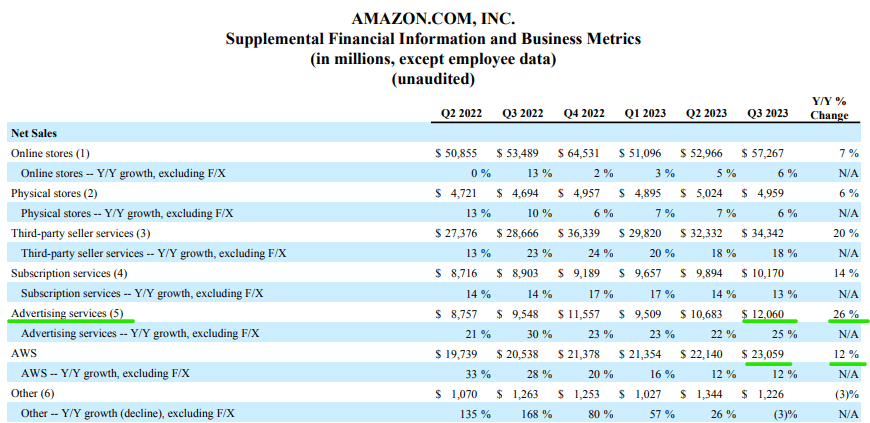

Despite Amazon already re-accelerating top-line growth and improving profitability [margins], I think there’s a lot more to come from this big tech giant as Amazon’s revenue mix shifts toward faster-growing, higher-margin AWS [cloud] and Ads businesses.

Amazon Q3 2023 Earnings Press Release

Amazon’s twin profit-growth engine hit a snag in recent quarters, but both Cloud and Digital Ads businesses are showing green shoots of recovery. Furthermore, Amazon exiting an intense CAPEX-spending cycle (that saw Amazon’s retail business doubling its footprint since the start of the COVID-19 pandemic) is set to boost margins in the retail business as Amazon reaps the benefits of improved capacity utilization and rationalization gets better with a new regional distribution network.

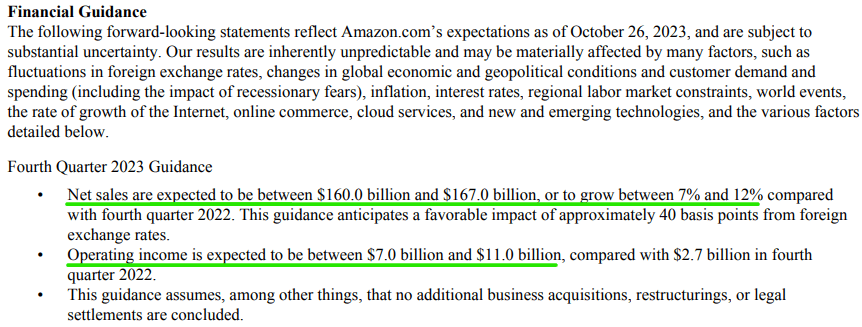

For Q4 2023, Amazon’s management guided for net sales of $160-167B (up 7-12% y/y) [slightly below consensus street estimates going into the Q2 print]; however, given the continued resilience of the US consumer, I believe a quarterly beat for Q4 is a strong possibility.

Amazon Q3 2023 Earnings Press Release

As you may know, my investment thesis for Amazon is centered around its twin profit-growth engine of AWS (cloud) and Ads. In the Q3 2023 report, Amazon showcased further stabilization at AWS (management hinting at a trough in growth rates) and a re-acceleration in the digital Ads business. Furthermore, I continue to view Amazon’s retail business turning profitable at scale like the cherry on top of an already incredible cake.

In a nutshell, I am happy with Amazon’s Q3 results as a long-term investor. Barring a significant deterioration in the macroeconomic environment (consumer spending), Amazon’s financial performance should remain robust over upcoming quarters.

Now, let’s determine Amazon’s intrinsic value and projected returns using our valuation model.

Amazon’s Fair Value and Expected Return

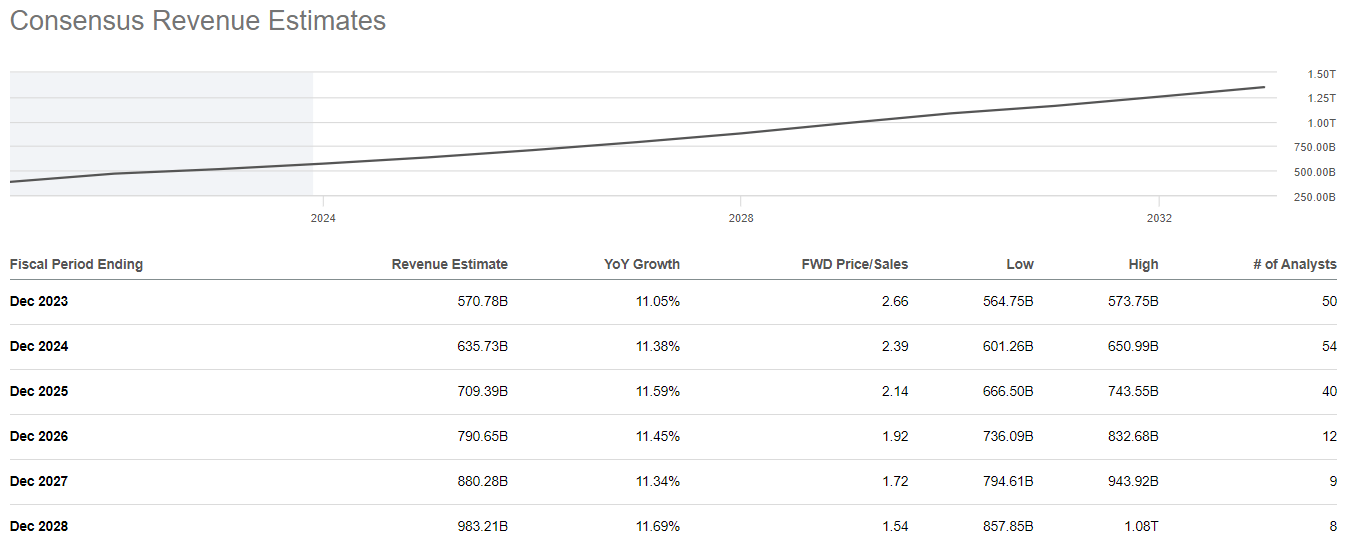

To build a margin of safety into our valuation model for Amazon, I have assumed a 5-year CAGR sales growth rate of 10% (vs. current consensus analyst CAGR estimates of 11.5%).

Amazon’s Revenue Estimates (Seeking Alpha)

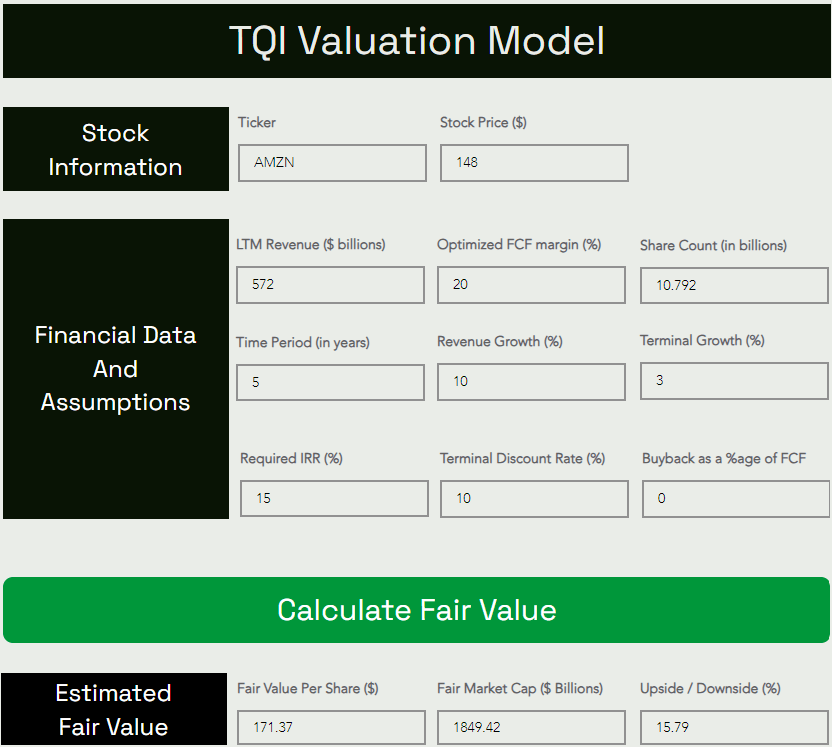

While AMZN bears would disagree with an optimized FCF margin of 20%, I firmly believe that Amazon’s high-margin businesses, i.e., AWS and Ads, can lead FCF margins even higher than 20% over the long run. All other assumptions are relatively straightforward, but if you have any questions, please feel free to share them in the comments section.

Here’s my updated valuation model for Amazon (including 2023E revenue):

TQI Valuation Model (TQIG.org)

According to the valuation model, Amazon’s fair value is ~$171 per share (or $1.85T). With the stock trading at ~$148 per share, AMZN is still trading at a sizeable discount to its intrinsic value, and I couldn’t say the same about any of AMZN’s “Magnificent 7” big tech peers.

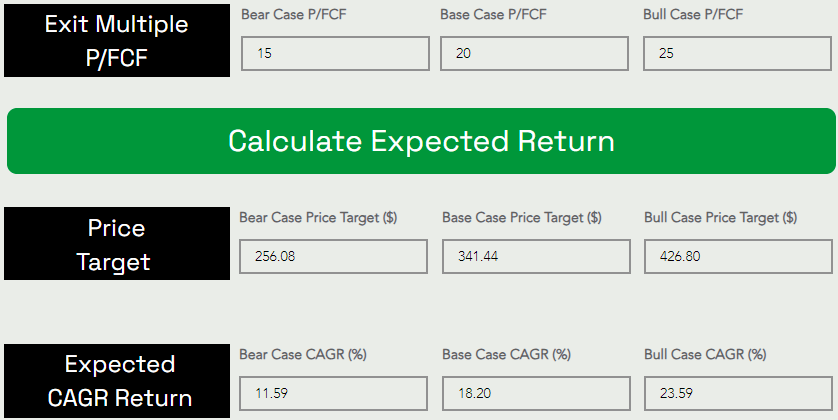

Predicting where a stock would trade in the short term is impossible; however, over the long run, a stock would track its business fundamentals and obey the immutable laws of money. If the interest rates were to stay depressed, higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the historical long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x.

TQI Valuation Model (TQIG.org)

Assuming an exit multiple of 20x P/FCF, I see Amazon’s stock price rising from $148 to $341 at a CAGR rate of ~18.2% over the next five years. With Amazon’s 5-year expected CAGR return still exceeding our investment hurdle of 15%, AMZN stock remains a long-term “Buy” under our valuation process.

Amazon’s Technical Chart and Quant Factor Grades

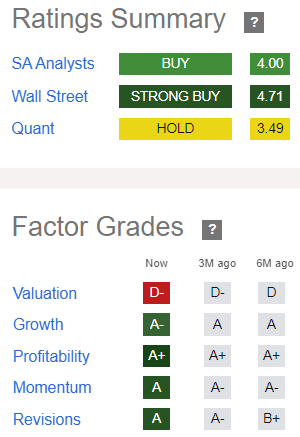

According to Seeking Alpha’s Quant Rating system, Amazon is rated a “Hold” with a score of 3.49/5, primarily due to its “Valuation” factor grade of “D-“.

Seeking Alpha

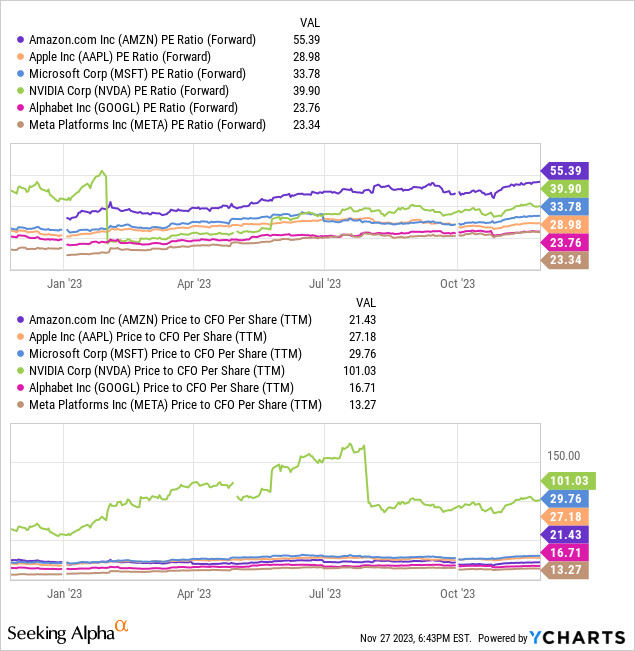

On a relative earnings basis, Amazon looks expensive compared to its industry peers, and that’s reflected in AMZN’s valuation factor grade. However, as we know, Amazon’s earnings are masked by its intense CAPEX-spending cycle, which the company is slowly exiting. In my view, investors should look at operational cash flows to evaluate Amazon. As you can see below, on a price-to-CFO basis, Amazon is one of the cheaper big tech names, along with Alphabet (GOOGL) (GOOG) and Meta (META).

Furthermore, we have already seen that Amazon is undervalued on an absolute basis. Hence, investors should look beyond AMZN’s current earnings multiple. With Amazon back to reporting strong operational cash flow generation (and positive net income) in 2023, AMZN’s “Profitability” grade of “A+” is now beyond the scope of any doubts. As Amazon re-accelerates growth and improves its margin profile, “Growth” and “Revisions” quant factor grades of “A-” and “A” appear to be a fair reflection of strong ongoing business momentum and near-term expectations.

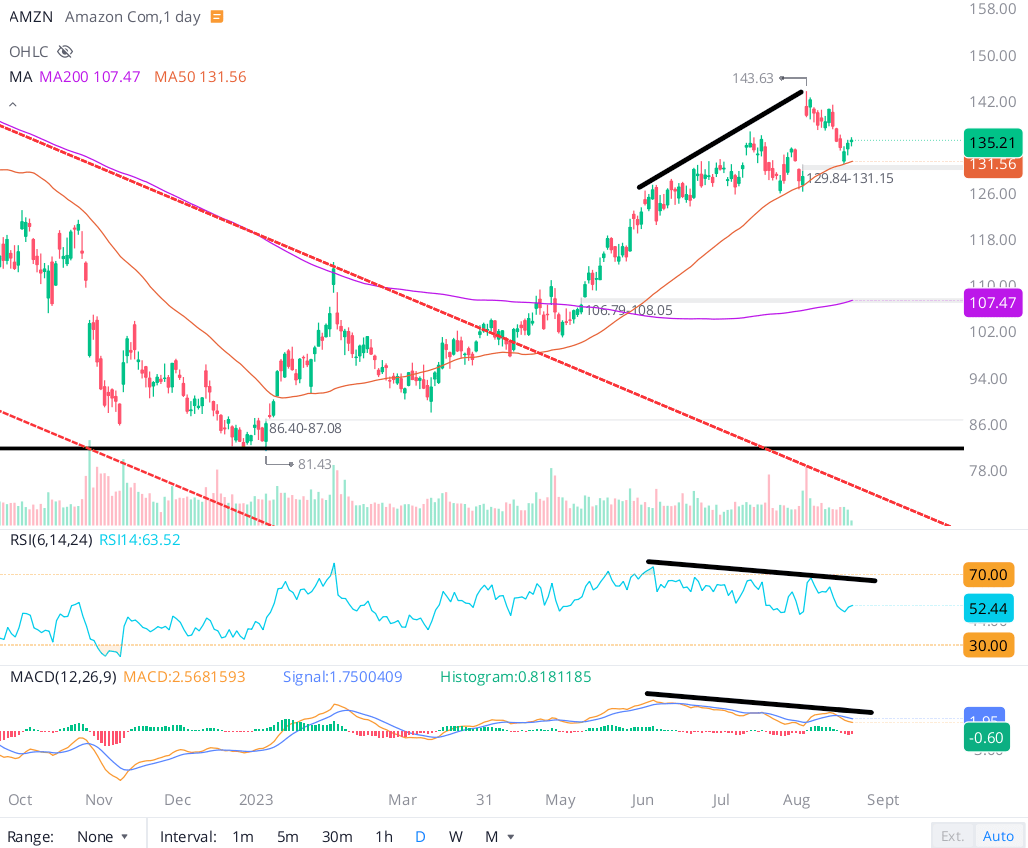

Lastly, a “Momentum” grade of “A” indicates that Amazon’s technical momentum remains bullish. In my previous note on AMZN (published in August), I wrote the following –

In 2023, Amazon’s stock has had an incredible run, and this strength is visible in its “Momentum” grade, which has improved from “D+” to “A-” over the last six months. While mega-cap tech names like Apple (AAPL) and Microsoft (MSFT) have lost a good bit of momentum in recent trading sessions, Amazon’s bullish momentum is still intact with AMZN stock trading above both 50-DMA and 200-DMA levels.

Amazon stock chart (August-2023) (WeBull Desktop)

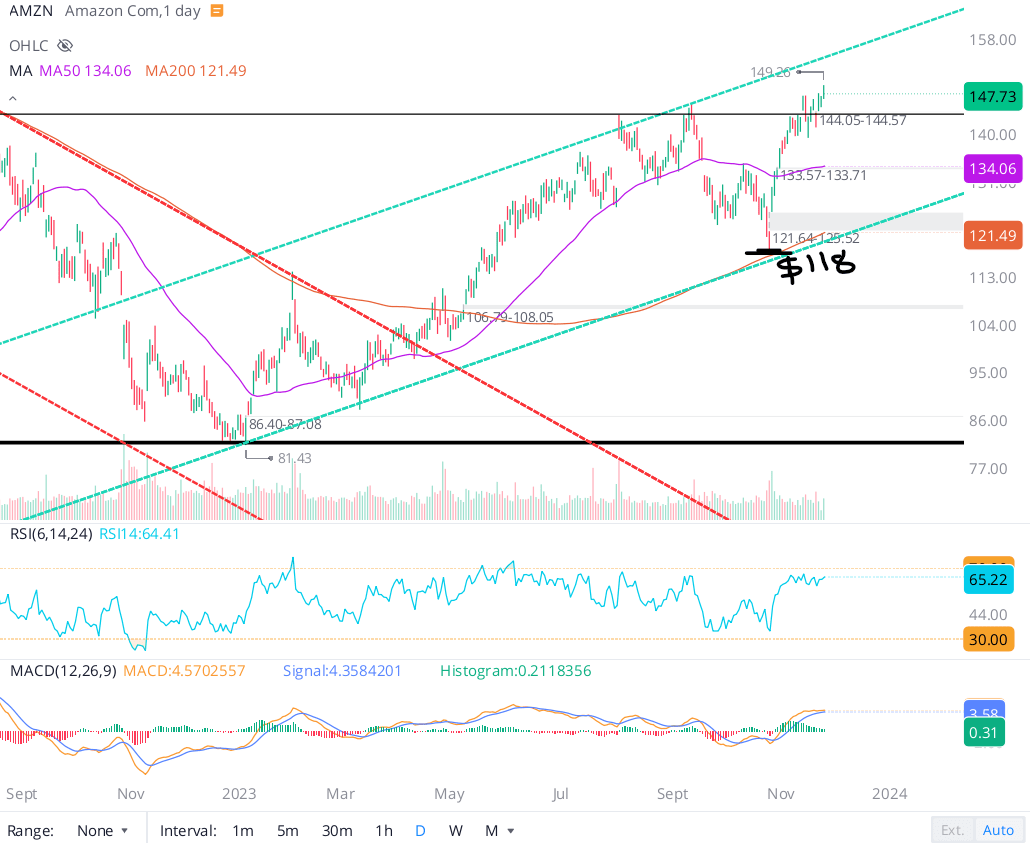

That said, I see a negative divergence between AMZN’s stock and key indicators such as RSI and MACD. Given this setup, Amazon may also join its peers in breaking below the 50-DMA level in the near future. And if AMZN breaks below the ~$130 (50-DMA) level, I can see the stock re-testing the $110-120 range.

Amazon stock chart (August-2023) (WeBull Desktop)

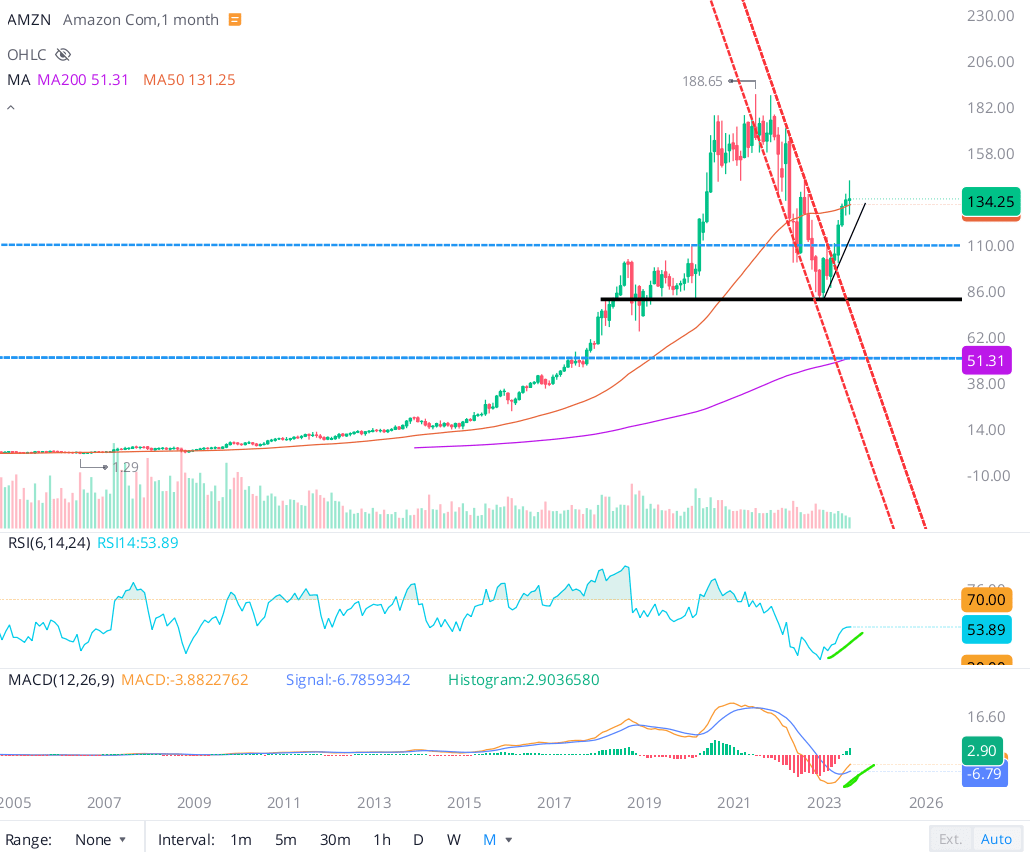

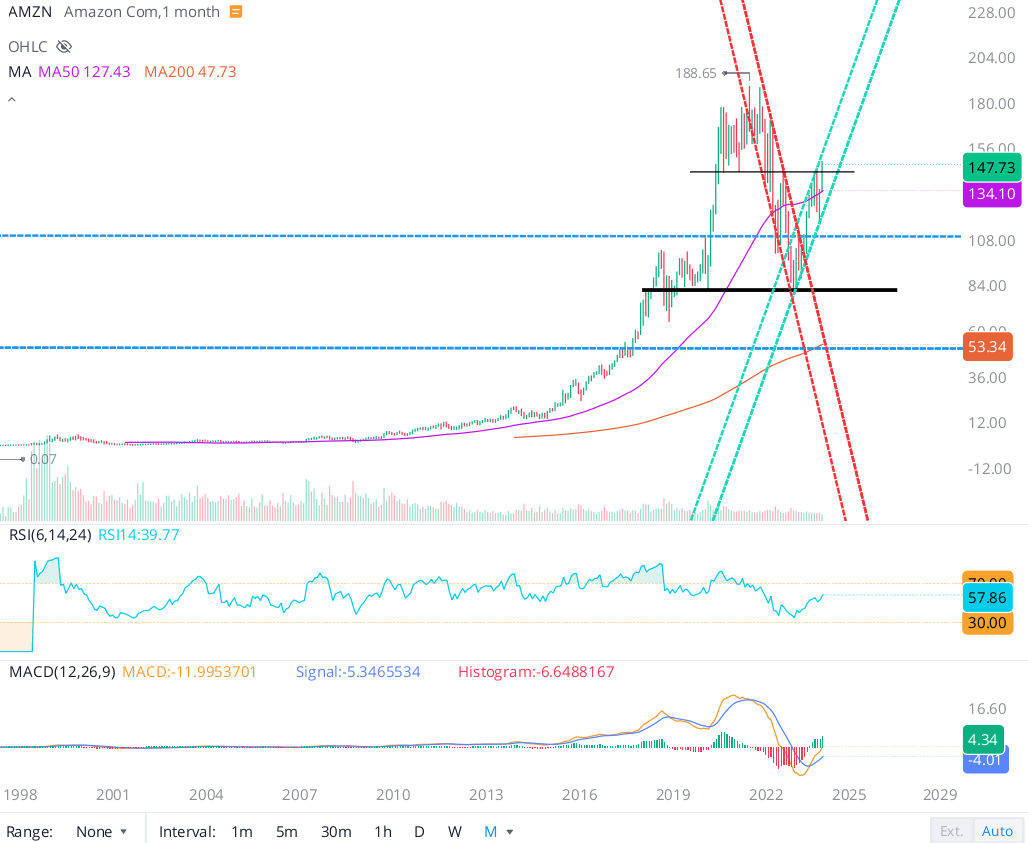

Now, a near-term correction in AMZN is possible (in fact it is quite likely); however, the longer-term setup for Amazon is looking bullish, with MACD on the monthly chart curling up and RSI (54) still far off overbought territory.

After the publication of this report, Amazon pulled back down to ~$118 by late October (within my suggested target range of $110-120 for a correction) amid a sharp rise in long-duration treasury yields. However, as you may know, long-duration treasury yields have subsided drastically in November, with 10-year treasury yield falling by 60 bps from nearly 5% to 4.4%. And this move in yields has bolstered Amazon’s stock, the tech sector, and the broader equity market in general.

WeBull Desktop

Since reporting its Q3 results on 26th October, Amazon’s stock is up 25%, and yet, AMZN isn’t overbought (daily RSI < 70). While a near-term pullback cannot be ruled out, Amazon’s longer-term monthly chart is still bullish:

WeBull Desktop

Amazon’s all-time high is at $188.65 per share, which is +27% from current levels. While such an upside move is difficult to foresee, a Santa Rally could see AMZN take a run at these levels in what’s left of 2023. If not this year, I can certainly see Amazon testing its all-time highs sometime in 2024 [barring a macroeconomic shocker].

Concluding Thoughts

Despite continued macroeconomic uncertainty, Amazon remains a fundamentally sound business, with market-leading positions in humongous markets: e-commerce, digital advertising, and cloud. As per our analysis, improving business fundamentals, solid technicals, and long-term risk/reward [based on absolute valuation] continue to render Amazon stock a buy.

Key Takeaway: I rate AMZN a “Buy” at $148 per share, with a strong preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

How To Invest In This Environment?

In order to navigate this tricky economic period, we are pursuing “Bold, Active Investing with Proactive Risk Management” at our investing group – “The Quantamental Investor“. With a laser focus on valuations, profitability, and balance sheet strength, we are buying the winners of tomorrow! Furthermore, we are utilizing index-based options to guard against significant broad-market declines. Join us today to prepare for whatever the market may throw at you in 2024, now at a deeply discounted price this holiday season: