Heading into Q1-2023 results, AMZN stock is getting some love from Wall Street after Andy Jassy expressed optimism for Amazon’s future in his second annual shareholder letter.

While AMZN stock jumped up by ~5% last Friday, investors should heed Jassy’s warning on Amazon’s retail, AWS, and Ads businesses.

In this note, we will look at Amazon’s valuation in the context of falling inflation, declining treasury yields, and a weakening US dollar. And then re-evaluate Amazon’s absolute valuation.

Additionally, we will discuss Amazon’s technical setup and quant factor grades going into earnings to see if it’s a buy/sell/hold at current levels.

Thos Robinson/Getty Images Entertainment

Introduction

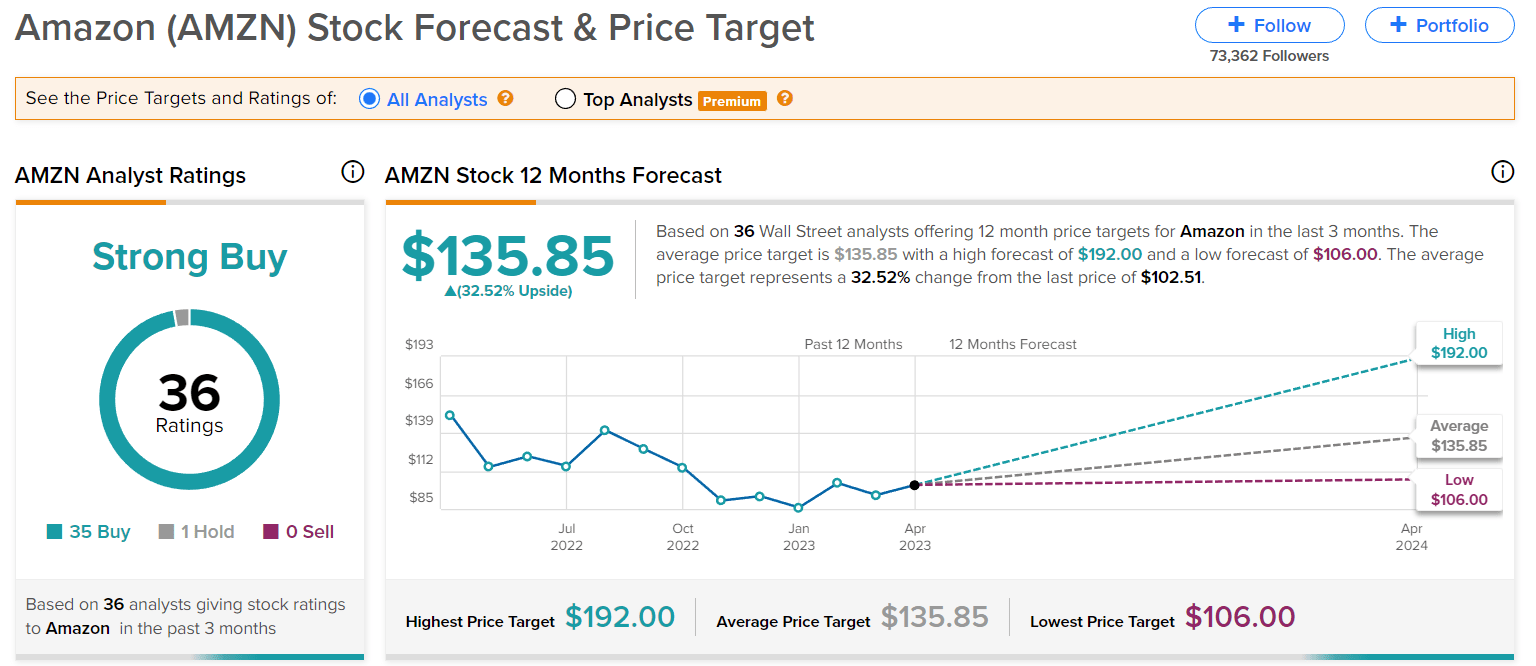

Despite losing ~45% (or $835B) of its market capitalization over the last few years, Amazon (NASDAQ:AMZN) remains a Wall Street darling. As per data from TipRanks, Amazon currently has 35 “Buy” ratings, 1 “Hold” rating, and no “Sell” ratings from Wall Street analysts. From top-tier banks to hedge funds, Amazon is a consensus buy among institutional investors for 2023!

TipRanks

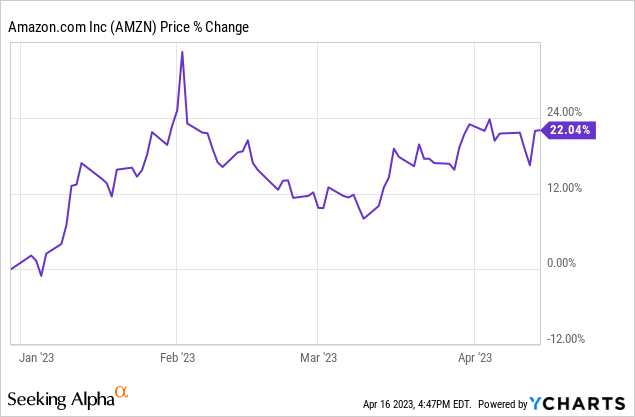

And so far this year, AMZN stock hasn’t disappointed investors – rallying by more than 22% year-to-date:

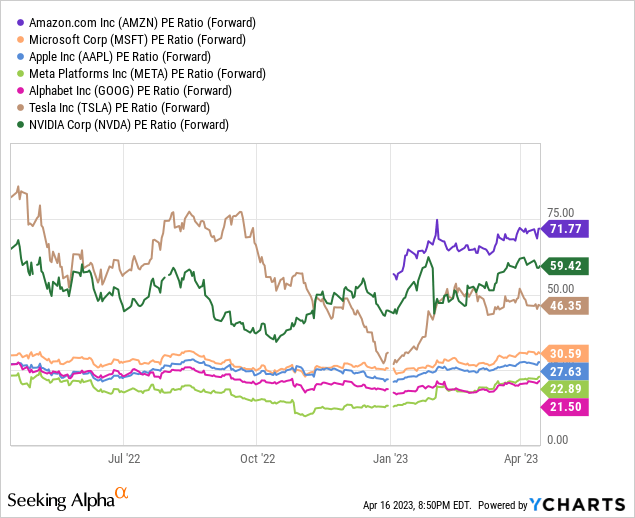

While the macroeconomic environment remains uncertain, three of the biggest headwinds for technology stocks in 2022 – [strong] US dollar, [high] inflation rates, and [rising] treasury yields – have turned into tailwinds this year.

As you may know, inflation, interest rates, and the value of the US dollar all directly impact the value of future cash flows [and, by extension, asset values]. When inflation is high, the value of future cash flows is reduced because the purchasing power of those cash flows will be lower. Similarly, when interest rates are high, the discount rate used to calculate the present value of future cash flows is also higher, which further reduces the value of those cash flows. For multinational companies like Amazon, a strong US dollar has a negative impact on international sales [and profits].

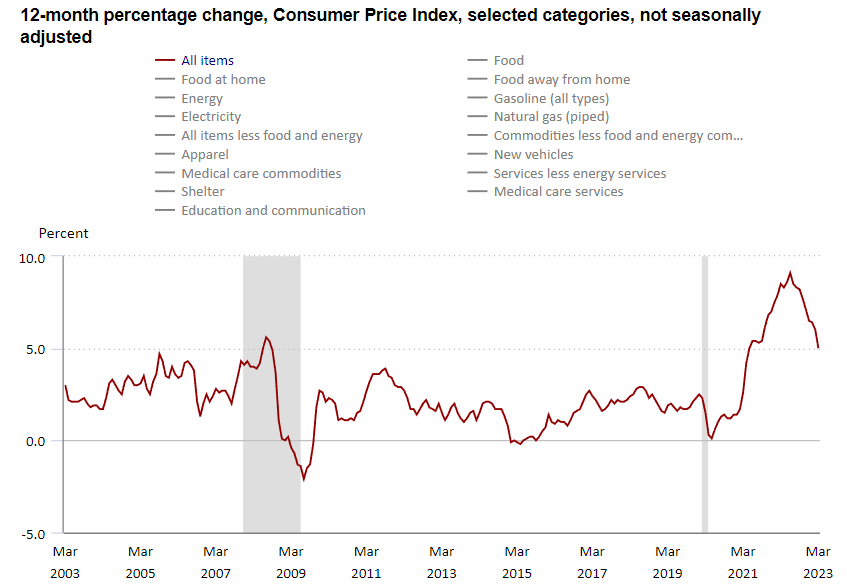

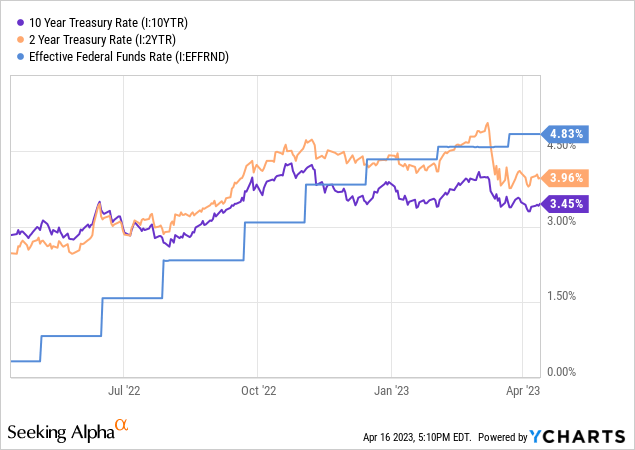

In recent months, inflation has been cooling off, and the latest CPI report showed that inflation rose by just +0.1% m/m in March 2023. Furthermore, interest rates have also moderated significantly in recent weeks, with the 10-year treasury yield down from cycle highs of around 4.3% to around 3.5% as of mid-April 2023. Lastly, the US dollar index (DXY) has declined considerably from its peak, and this should also act as a tailwind for Amazon’s upcoming quarterly results.

With inflation, treasury yields, and the US dollar cooling down in recent months, Mr. Market has bought up mega-cap tech stocks like Amazon in 2023. And last week, Andy Jassy (Amazon’s CEO) [advertently or inadvertently] fueled another jump in AMZN stock by laying out a compelling investment thesis for Amazon and expressing optimism about Amazon’s business in his second annual shareholder letter. While Mr. Market’s reaction (a ~5% jump in AMZN stock) to this letter was very bullish, I think investors may be wise to read between the lines.

In this note, we will first dissect Amazon’s 2022 shareholder letter. Then, we will preview Amazon’s upcoming quarterly results and review its valuation. Lastly, we will check up on AMZN’s technical chart & quant factor grades to see if it’s a worthwhile buy right now.

Highlights Of Amazon 2022 Shareholder Letter

Over the years, Amazon’s shareholder letters have served as a valuable resource for investors and business leaders, providing insights into Amazon’s business strategy, financial performance, and future plans. The first-ever Amazon shareholder letter was published in 1997, the year the company went public. In the letter, Jeff Bezos outlined his vision for Amazon as “Earth’s most customer-centric company” and discussed the company’s focus on innovation and long-term thinking.

In subsequent letters, Bezos continued to share his insights on Amazon’s business and strategy until last year, when Andy Jassy took over the responsibility of writing this letter as the new CEO of Amazon. If you have read any of these gems, you know that these letters include nuggets about a variety of topics, including customer obsession, innovation, and the importance of long-term thinking.

Last week, Amazon published its 2022 shareholder letter, which received a broadly positive response from investors and analysts alike. In his second shareholder letter, Jassy chose to sugarcoat Amazon’s sobering financial performance and weak near-term outlook by expressing optimism for the company’s long-term future. More importantly, Jassy made a compelling argument to invest in Amazon –

There are two relatively simple statistics that underline our immense future opportunity. While we have a consumer business that’s $434B in 2022, the vast majority of total market segment share in global retail still resides in physical stores (roughly 80%). And, it’s a similar story for Global IT spending, where we have AWS revenue of $80B in 2022, with about 90% of Global IT spending still on-premises and yet to migrate to the cloud. As these equations steadily flip—as we’re already seeing happen—we believe our leading customer experiences, relentless invention, customer focus, and hard work will result in significant growth in the coming years. And, of course, this doesn’t include the other businesses and experiences we’re pursuing at Amazon, all of which are still in their early days.

I strongly believe that our best days are in front of us.

– Andy Jassy, President and CEO of Amazon

While it is hard to believe that a business doing more than $500B in annual revenue has its best days ahead of itself, I think Amazon is well on its way to becoming the first-ever company to reach the $1T annual revenue milestone by the end of this decade. If you have been following my work on AMZN, you know that despite being a big Amazon bull, I am not a fan of Amazon’s retail business and that my entire investment thesis for Amazon is centered on its twin growth engine, i.e., AWS (cloud) and Ads. That said, I have always believed that Amazon’s retail ecosystem is incredibly valuable, and it still has a lot of (slow and steady) growth left in its tank. Now, let’s briefly talk about Jassy’s business-by-business view on Amazon’s future:

Retail/Consumer: In his letter, Jassy focused on the humongous scale of Amazon’s consumer retail business ($434B revenue in 2022) and highlighted multiple avenues for growth, including expansion of Amazon’s grocery business, greater penetration in international markets, and physical retail. Furthermore, Jassy reiterated his confidence in lowering costs, reducing delivery times, and building a more significant retail business with healthy operating margins over the long run. Despite a broadly positive view of Amazon’s retail business, Jassy warned that Amazon is still searching for a mass physical store concept that works!

AWS (cloud): AWS has served as the profit center at Amazon for several years and enabled the spectacular expansion of its retail ecosystem and other business lines. In 2022, AWS achieved record revenues of $80B, and this business is currently running at an ARR of $85B. However, AWS’ growth has been decelerating for multiple quarters now, and this trend is set to continue in 2023, according to Jassy:

Amazon Shareholder Letter 2022

While AWS is still projected to grow at a healthy clip, I think its profit margins are set to come under pressure as customers reduce/optimize spend on the cloud services platform. The slowdown at AWS may only be temporary, given the massive runway ahead (90% of Global IT spend is still on-premise); however, the impact of this slowdown on Amazon’s overall profitability in 2023 is undoubtedly going to be outsized.

Amazon Ads: Despite showing signs of deceleration in 2022, Amazon’s digital Ads business managed to grow at a brisk clip last year at a time when rivals like Meta (META) and Alphabet (GOOGL) experienced a massive revenue growth slowdown. Jassy highlighted the unique strength of Amazon’s Ad business and talked about future integration opportunities in video, live sports, audio, and grocery products. While Jassy did not explicitly write anything negative about the Ads business, the numbers clearly reflect a slowdown due to the macroeconomic environment, which looks set to worsen over the coming months.

Additionally, Jassy mentioned that Amazon is currently working on finding its fourth pillar of growth by investing in three significant long-term opportunities: Amazon Healthcare, Kuiper, and Generative AI. While this may seem like a desperate attempt to boost investor sentiment, Jassy compared Amazon Healthcare and Kuiper to a 2003 AWS. And despite Amazon announcing Bedrock a few days back, the inclusion of generative AI in the letter almost felt a little forced. For more details on these opportunities, refer to this letter.

In a nutshell, Amazon’s 2022 shareholder letter is filled with long-term optimism and near-term pessimism. With Jassy explicitly warning that the current macroeconomic environment is negatively impacting AWS (Amazon’s profit center), I can’t see Amazon outperforming bottom-line expectations in the near term. Furthermore, I think it will be hard for Amazon to meet the consensus FCF estimates of +$28B for 2023.

That said, I continue to believe in Amazon’s long-term free cash flow generation potential, and hence, I retain a bullish stance on the business. Back in February, we discussed Amazon’s Q4 2022 results and TQI’s investment thesis for AMZN in the following report:

While the collapse in inflation and the moderation in interest rates are tailwinds for Amazon’s stock, the latest US Retail Sales (down ~1% m/m) report showed that consumer demand is deteriorating rapidly. As the economy potentially steers toward a hard landing [economic recession], Amazon’s financial performance is likely to remain under pressure despite the company facing easier comps this year.

What To Expect From Amazon’s Upcoming Quarterly Results?

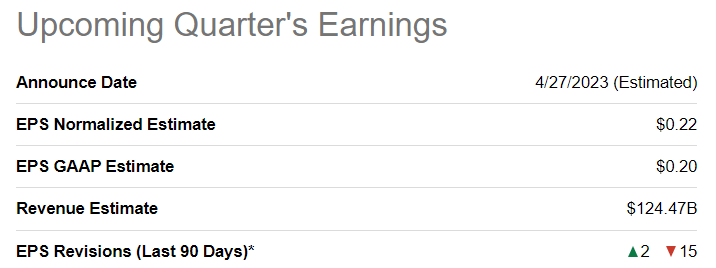

Going into the Q1 2023 report, consensus analyst estimates for Amazon’s upcoming quarterly report now stand at –

Revenue: $124.47B (vs. management’s guidance of $121-$126B)

Normalized EPS: $0.22

SeekingAlpha

Now, Amazon is an incredible company; however, it is not immune from the macroeconomic environment. The tech giant is set to release its Q1 2023 quarterly report on 27th April 2023. Based on Jassy’s subtle warnings on Amazon’s retail, AWS, and Ads businesses in the shareholder letter, I think AMZN’s Q1 report could be a rude awakening for investors [especially on the profitability front].

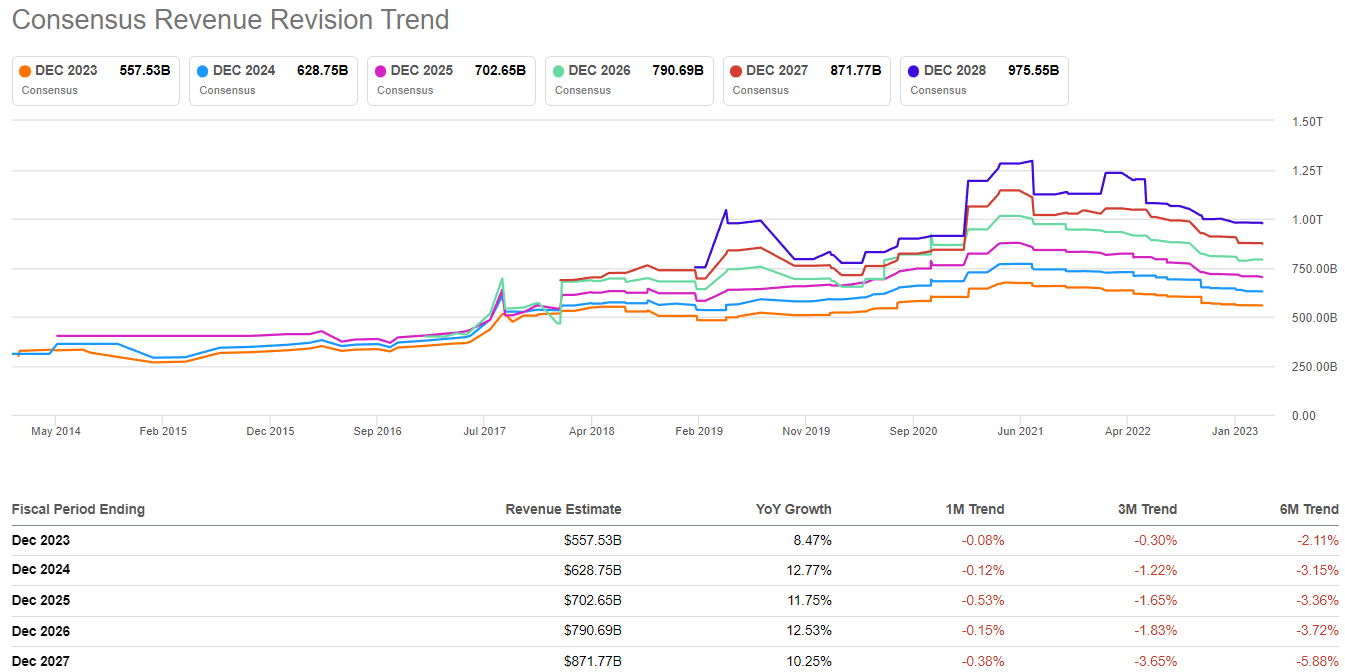

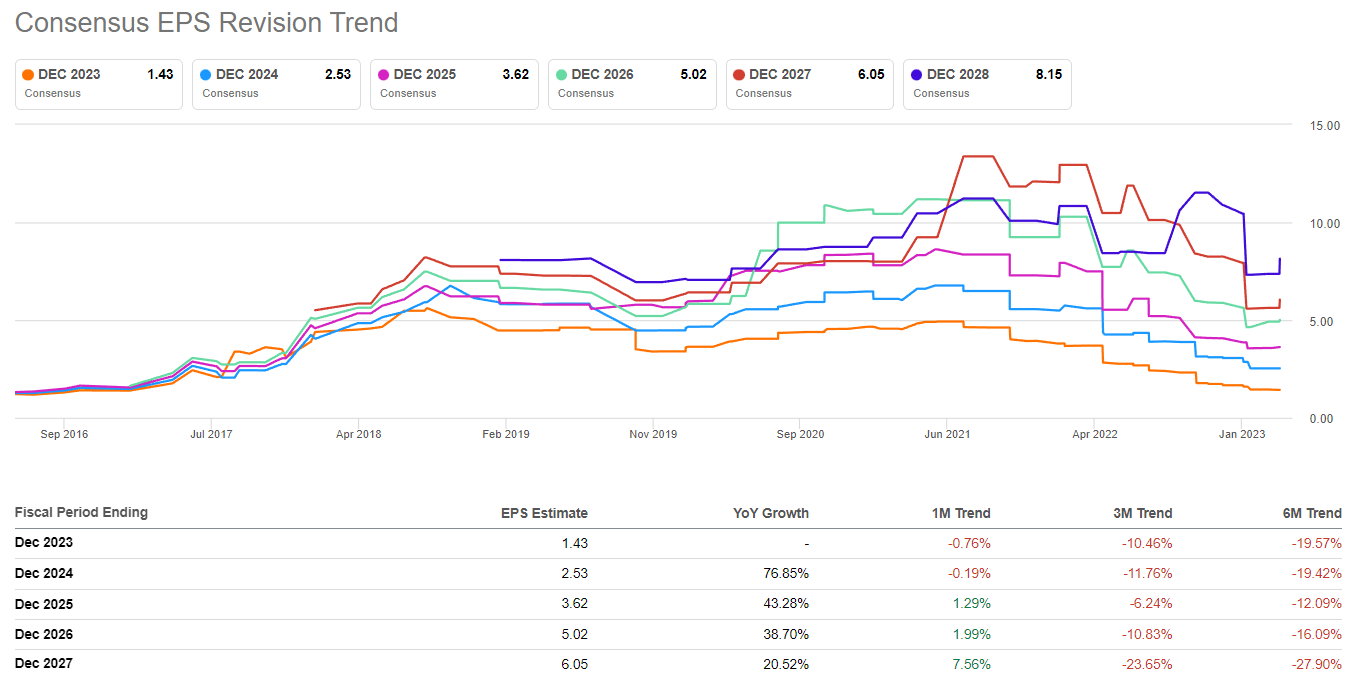

Over the last six months, Amazon’s consensus revenue and earnings estimates for 2023 have been lowered by ~2% and ~20%, respectively. And the upcoming quarterly report could lead to further cuts from analysts depending on financial performance in Q1 2023, management’s guidance for Q2, and commentary about the rest of this year.

SeekingAlpha

SeekingAlpha

In 2022, Amazon’s revenue grew by ~9.4%, and for 2023, Amazon is currently projected to grow revenue by ~8.5%. Hence, Amazon’s growth rate is still expected to decelerate in 2023. With Amazon still in the early stages of exiting a multi-year heavy CAPEX spending cycle, Amazon’s free cash flows and profits are likely to remain compressed in the near term. Due to its revenue growth deceleration and compressed earnings, Amazon appears to be very expensive on a Forward Price-to-Earnings basis relative to its mega-cap tech peers.

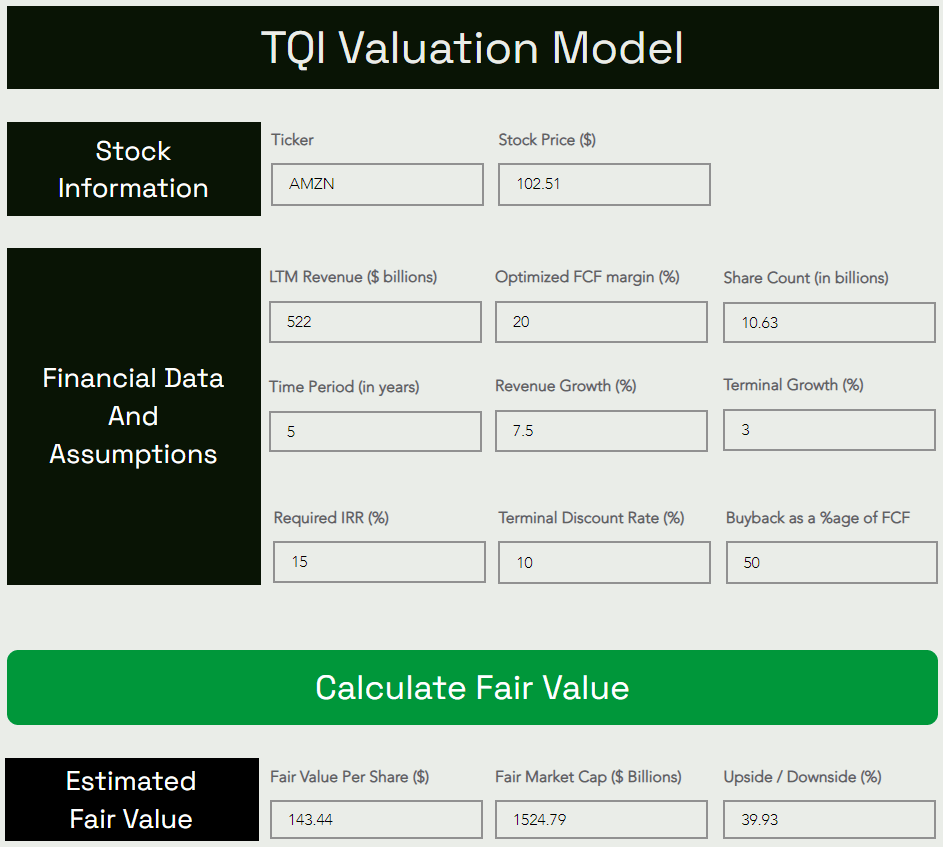

However, as we have discussed in the past, Amazon’s true earnings and cash flows are currently being masked due to a heavy CAPEX spending cycle. Hence, we must evaluate Amazon’s intrinsic value using conservative steady-state assumptions. Let’s do so through TQI’s Valuation Model.

Amazon’s Fair Value And Expected Returns

To build a margin of safety into our valuation model for Amazon, I have assumed a CAGR growth rate of just 7.5% (vs. current consensus analyst estimates of 11.15%). While AMZN bears may disagree with a steady-state free cash flow margin of 20%, I think Amazon’s high-margin businesses, i.e., AWS and Ads, can lead FCF margins even higher than 20% over the long run. All other assumptions are relatively straightforward, but if you have any questions, please feel free to share them in the comments section.

Here’s my updated valuation model for Amazon (including Q1 expectations):

TQI Valuation Model (TQIG.org)

According to TQI’s Valuation Model, Microsoft’s fair value is ~$161.26 per share (or $1.2T). With the stock trading at ~$239 per share, I think it is still trading at a hefty premium to its intrinsic value.

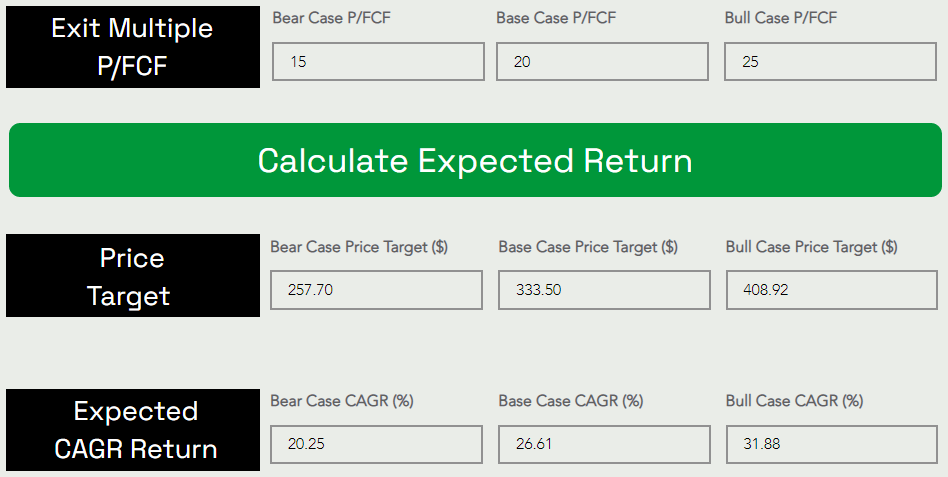

Predicting where a stock would trade in the short term is impossible; however, over the long run, a stock would track its business fundamentals and obey the immutable laws of money. If the interest rates were to stay depressed, higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x.

TQI Valuation Model (TQIG.org)

By 2027, Amazon’s stock price could grow from ~$102.5 to ~$333.5 at a CAGR of 26.61%. With these expected returns far exceeding my investment hurdle rate of 15%, I consider Amazon a truly asymmetric risk/reward bet for long-term investors.

AMZN’s Technical Chart & Quant Factor Grades

Amazon’s stock has been undergoing a complex correction for nearly two years now, with its trading multiples normalizing in a higher interest rate environment. In my last update on Amazon, I wrote the following:

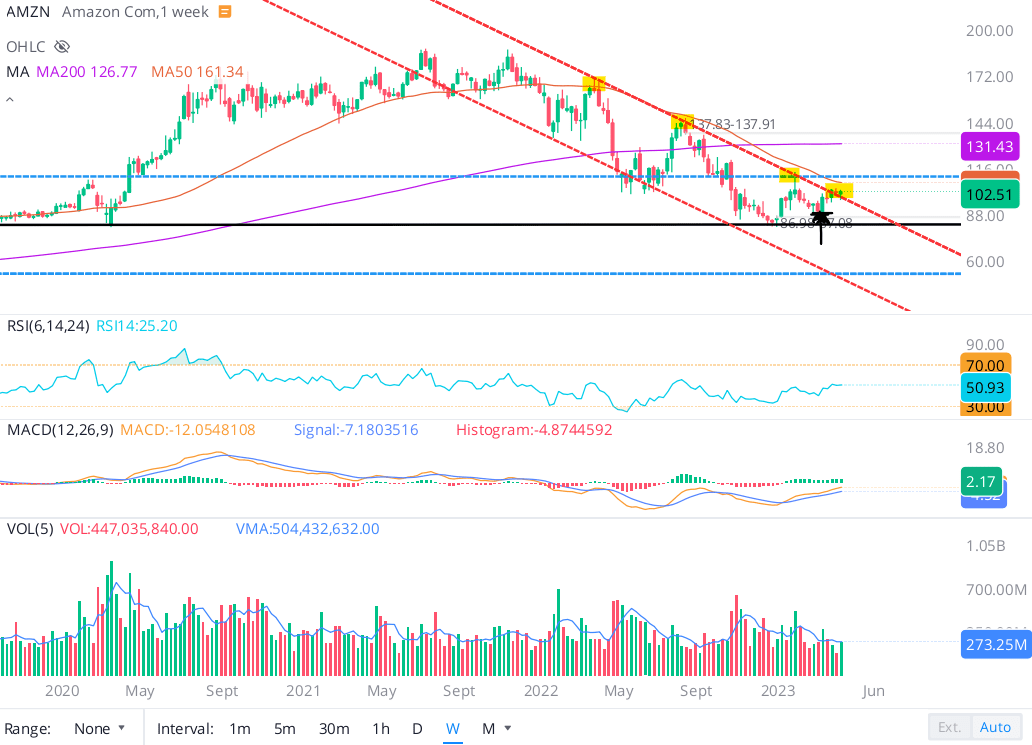

After getting rejected from the upper trendline of the falling downward channel (marked in dotted red), AMZN looks nailed on to re-test its recent lows in the low to mid $80s.

WeBull Desktop

Here’s what I said about Amazon in one of my recent notes –

As pointed out in my previous note, Amazon’s stock held multi-year support at $80 and bounced off this level. After a sharp 16%+ YTD bounce, Amazon looks primed to re-test the $100-$105 range in the coming weeks. If the stock fails to break this level, I would expect it to remain rangebound in the $80-$100 range.

And for now, I stick to this call for Amazon to remain rangebound in the $80-$100 range. If Amazon were to break down the multi-year support in the low $80s, then we could see the stock slide down to the next big support zone on the chart, which is in the $50s. Now, I do not expect Amazon to go this low until and unless we have a deep, deep recession!

Since that call in mid-February, Amazon’s stock went down to ~$87-88 level before rebounding back to ~$100. And then last Friday, Amazon’s stock bounced up above the $100 level in what appears to be a potential breakout.

WeBull Desktop

With mega-cap tech names enjoying a wild run so far in 2023, Amazon bulls are yearning for an upside breakout from the $80-100 range, and I am certainly a part of this hopeful camp. If we do break out to the upside, the first target would be the ~$120-140 range. On the flip side, a breakdown back below $100 could see Amazon resume its rangebound action, and we could very well get that re-test of recent lows in the low-to-mid $80s. In my opinion, Amazon’s upcoming quarterly report could prove to be decisive in determining the future path of its stock.

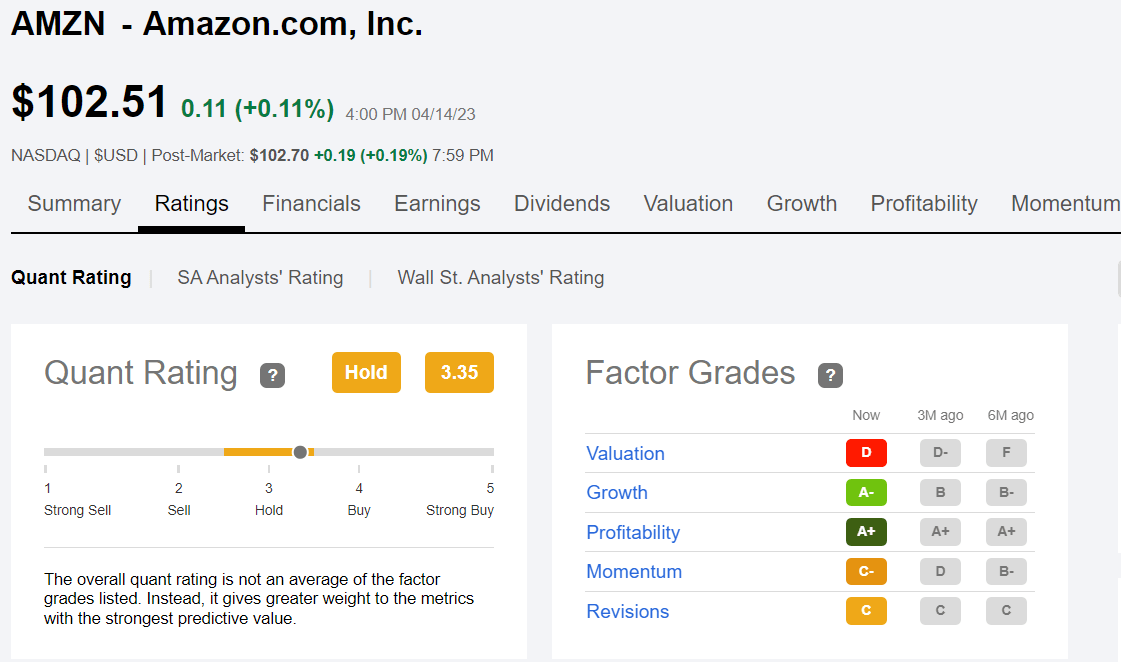

According to Seeking Alpha’s Quant Rating system, Amazon is rated a “Hold” with a score of 3.35/5.

SeekingAlpha

While Amazon’s “Profitability” grade of “A+” is befuddling, given the company has been free cash flow negative in recent quarters, I think Amazon’s operating cash flows are extremely healthy and do warrant a robust profitability rating for AMZN. With “Valuation”, “Growth”, and “Momentum” improving over the last six months, Amazon’s quant factors grades are headed in the right direction.

Final Thoughts

Based on a mix of fundamental, quantitative, and technical data analysis, Amazon’s stock is a solid buy right now; however, given Andy Jassy’s subtle warnings on the near-term performance of Amazon’s retail, AWS, and Ads businesses amid heightened macroeconomic uncertainty, I strongly prefer a staggered accumulation of AMZN shares over 6-12 months over a lump sum investment into the stock.

Key Takeaway: I continue to rate Amazon a “Strong Buy” at ~$100, with a strong preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN, META, GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking to upgrade your investing operations?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

We have recently reduced our subscription prices to make our community more accessible. TQI’s annual membership now costs only $480 (or $50 per month) for a limited period only.