Summary:

- The company’s topline growth has been nothing but stellar over the past decade demonstrating a CAGR of about 24%.

- Amazon’s strong balance sheet and cash flow give the company the flexibility to continue to invest in growth initiatives and make strategic acquisitions.

- Amazon’s impressive range of products and services, from online retailing to cloud computing, puts the company in a strong position to continue gaining market share in the years ahead.

- My valuation analysis suggests the stock is almost twice undervalued.

Noah Berger

Investment thesis

In my article I highlight the company’s outstanding financial performance over the past decade as well as its immense growth perspectives, which positions the company for further success in the future. Via strong topline growth and expanding margins, management demonstrated high efficiency of investments in research and development together with strategic acquisitions. The fact that Amazon (NASDAQ:AMZN) represents a compelling investment opportunity is supported by my valuation analysis, which shows that the current market price of Amazon stock does not fully reflect its future growth potential.

Company information

Amazon is one of the world’s largest companies, known for disrupting numerous industries. The company revolutionized the way customers shop online with its marketplace. Amazon serves consumers through its online and physical stores, offering a huge selection of products in dozens of categories, including electronics, apparel and groceries. Amazon’s success is built on its commitment to low prices, fast and free delivery, user-friendly features, and timely customer service.

In addition to serving customers, Amazon also offers services to sellers, developers, businesses, content creators and advertisers. Through its seller programs, Amazon enables businesses of all sizes to grow and sell their products in its stores. Amazon Web Services [AWS] offers developers and businesses a wide range of on-demand technology services, including compute, storage, database, analytics and machine learning services. Amazon also offers programs that enable content creators to publish and sell their work, as well as advertising services that help businesses reach new customers.

With more than 1.5 million employees worldwide, Amazon is a major employer and continues to attract top talent in software development, computer science and other technical fields.

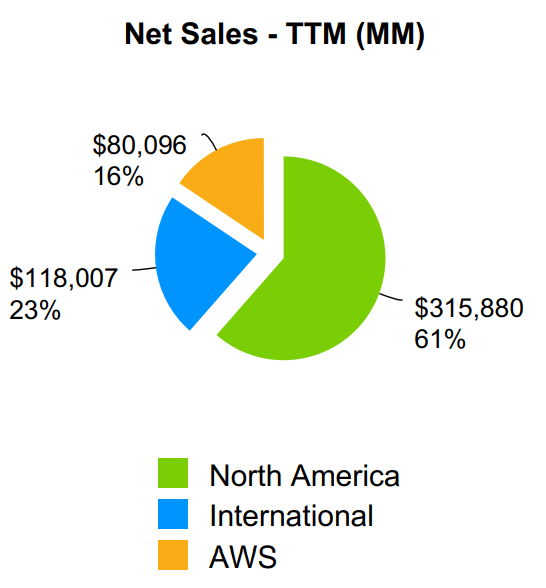

The company organized its business into three segments: North America, International and Amazon Web Services [AWS]. Major part of sales represent North America with 61% out of total revenues.

Amazon

Financials

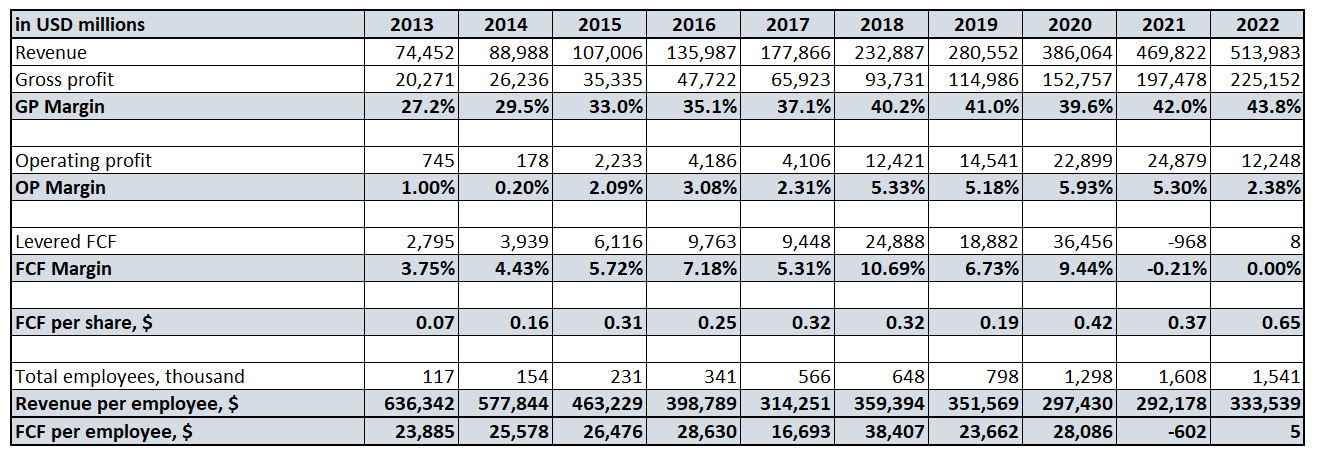

First of all, I would like to zoom out and look at the financials for the last decade. Here I can say that Amazon’s revenue growth has been immense over the last 10 years with gross margin expanding significantly from 27.2% to 43.8%. However, it is important to mention that from one of my favorite efficiency metrics, i.e. revenue per employee, the company did not demonstrate any progress meaning that perhaps they recruited by far more people than they needed to deliver actual revenue growth. This may also indicate that recent and current massive layoffs of AMZN staff was management’s right decision and will not negatively disrupt the company’s operations.

Author’s calculations

The company was able to sustain revenue growth at almost 24% CAGR mainly due to heavy investments in research and development [R&D] and strategic acquisitions. The company’s investments in R&D grew at the faster pace than topline did, starting with a 9% R&D to revenue ratio in 2013 ending up at 14% in the year ended December 31, 2022. From strategic acquisitions point of view, according to Wikipedia, Amazon acquired more than 100 companies across various industries and countries during last 25 years.

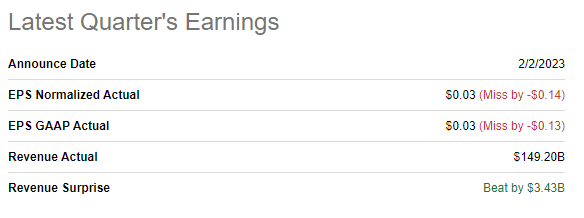

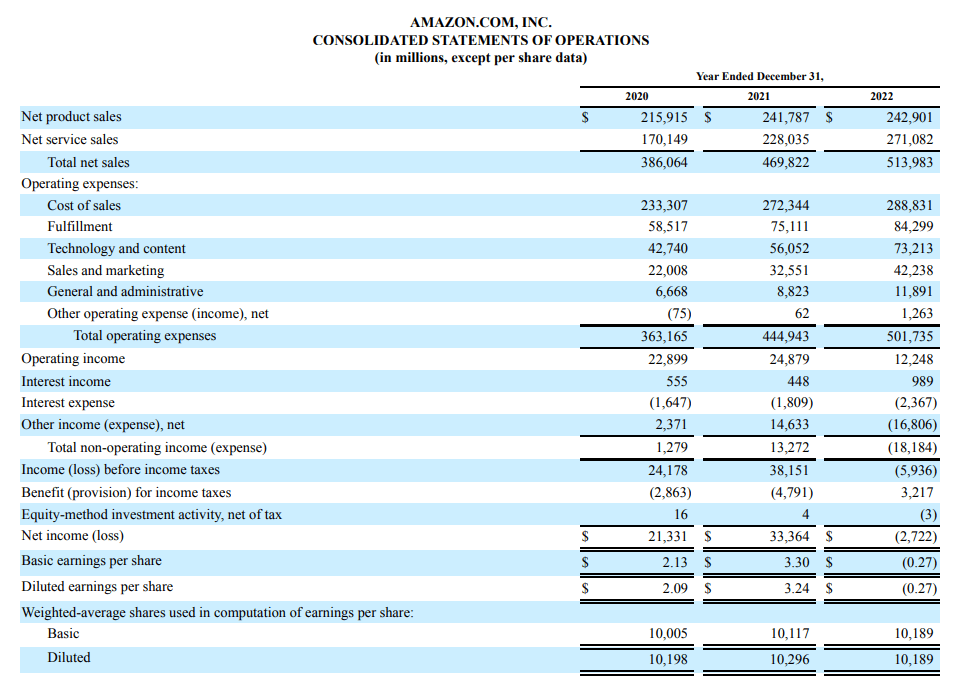

Amazon released its latest quarterly financial results on February 2, 2023. The company demonstrated above-consensus revenue but below-consensus EPS for 4Q2022.

Seeking Alpha

Quarterly results indicate a continued upward topline trajectory for the company. Net sales for the quarter increased 9% and totaled $149.2 billion compared to $137.4 billion in the same period of 2021. Excluding the unfavorable impact of foreign exchange, net sales increased 12% compared to the fourth quarter of last year.

Amazon

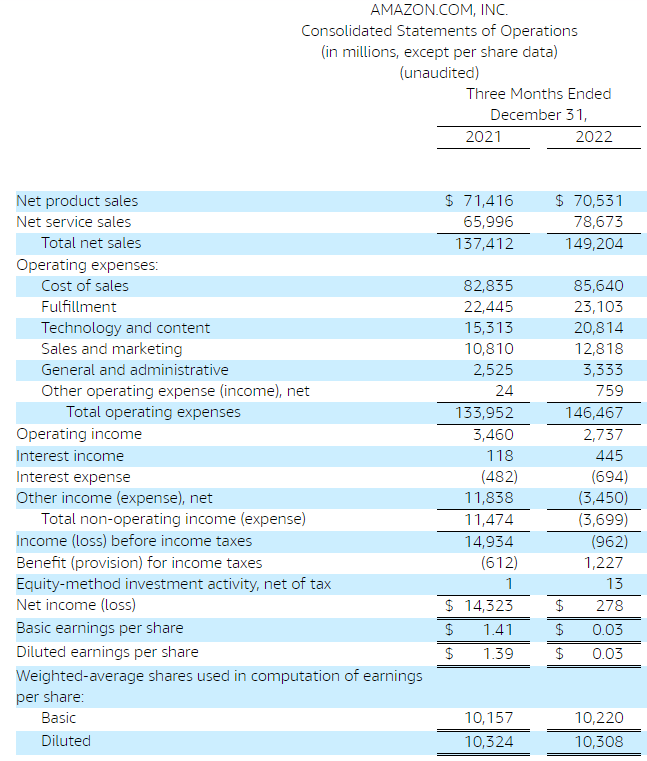

The North America segment was particularly strong, with sales up 13% YoY to $93.4 billion, or 14% when excluding foreign exchange movements. This growth is a testament to Amazon’s strong position in the U.S. market and its ability to capture a greater share of consumer spending. However, the international segment was not as successful, reporting an 8% YoY decline in sales to $34.5 billion. Excluding foreign exchange, the international segment reported a 5% increase in sales. This discrepancy highlights the challenges Amazon faces in expanding its e-commerce platform globally as it navigates through different cultural and economic environments. Amazon’s AWS segment saw a 20% YoY increase in revenue to $21.4 billion. This growth demonstrates the continued demand for cloud computing services and Amazon’s dominance in this market.

Overall, Amazon’s fourth quarter financial results demonstrate the company’s continued strength in e-commerce and cloud computing. While there are challenges in expanding globally and managing currency fluctuations, Amazon’s dominant position in the North American market and success in the AWS segment position the company well for continued growth in the future.

Amazon

For the full FY2022, net sales increased by 9% to $514.0 billion, compared to $469.8 billion in the previous year. The North America segment delivered a 13% YoY increase in sales to $315.9 billion, but the International segment sales declined 8% to $118.0 billion. Meanwhile, the AWS segment sales increased by 29% to $80.1 billion.

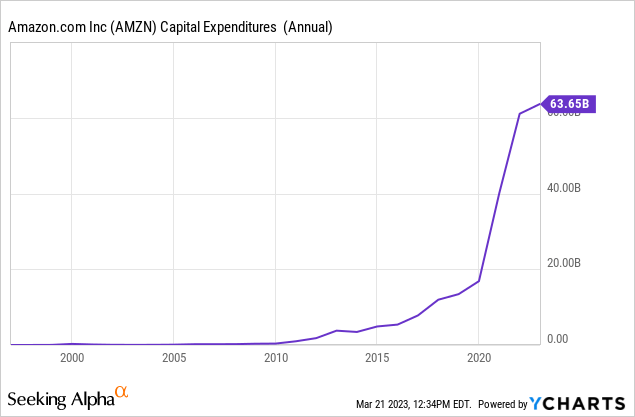

Amazon’s operating cash flow increased slightly by 1% to $46.8 billion over the past twelve months. However, free cash flow decreased to an outflow of $11.6 billion over the past twelve months, compared with an outflow of $9.1 billion a year earlier. Company’s free cash flow deteriorated significantly in last years due to skyrocketing capital expenditures – the company invested about $165 billion during 2020-2022 to fuel future growth. Increased CAPEX primarily reflect investments in technology infrastructure [the majority of which is to support AWS business growth] and in additional capacity to support fulfillment centers network.

In addition, Amazon’s net loss in 2022 was $2.7 billion, in stark contrast to its net income of $33.4 billion in 2021. The loss includes a pre-tax valuation loss of $12.7 billion from the common stock investment in Rivian Automotive, Inc (RIVN). compared to a pre-tax valuation gain of $11.8 billion in 2021. The North America segment also reported an operating loss of $2.8 billion compared to an operating profit of $7.3 billion in 2021, while the International segment reported a loss of $2.8 billion.

Management has provided guidance for the first quarter of 2023, expecting moderate YoY net revenue growth. The company expects net revenue to be between $121.0 billion and $126.0 billion, representing a growth rate of 4% to 8%. However, this forecast is based on the assumption that exchange rates will have an unfavorable impact of approximately 210 basis points. In terms of operating income, Amazon expects to earn between $0 billion and $4.0 billion in the first quarter of 2023 compared to $3.7 billion during the same period last year. It’s important to note that this guidance assumes no further business acquisitions, restructurings or legal settlements are completed this quarter.

From balance sheet perspective I can conclude that the company’s leverage is moderate, which is expected to support CAPEX for future growth. Moreover, the company has large balance of cash of $70 billion as of the 2022 year-end. Furthermore, AMZN’s strong revenue growth trajectory and dominant market position suggest that the company has resilience to generate sufficient cash flows to service its debt obligations.

Valuation

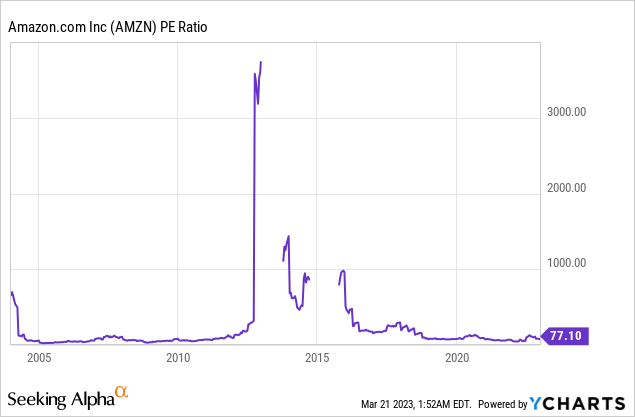

Amazon is a disruptor with outstanding revenue growth and enormous potential for further growth thanks to continuous innovation and the introduction of new business lines with large addressable markets. Therefore, it is not surprising that the company’s valuation metrics have skyrocketed in recent decades.

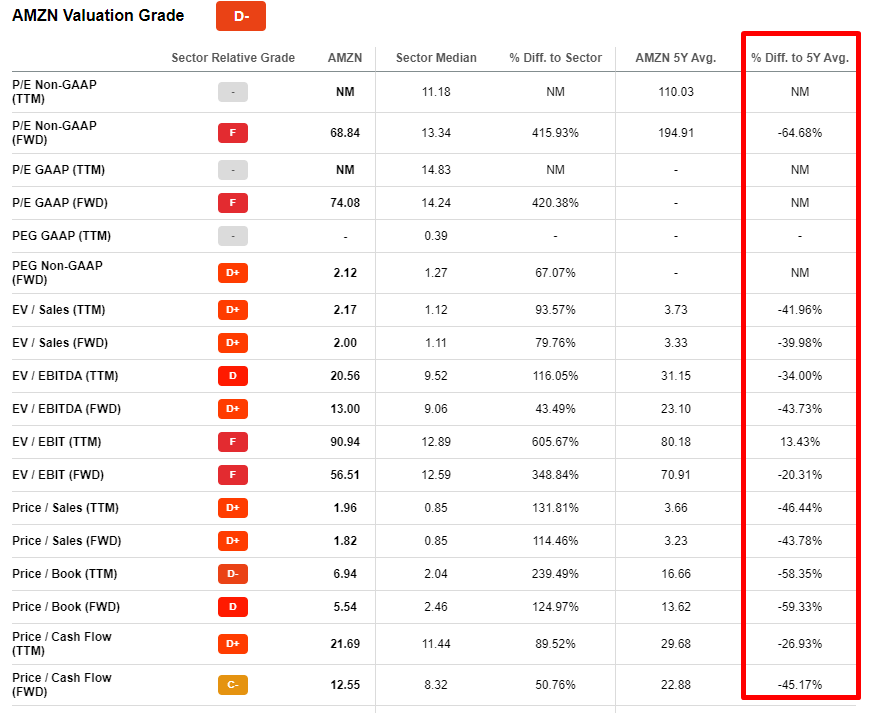

Before we would go in more details in valuation I would like to pay readers attention on the fact that current multiples are currently much lower than the company’s 5-year averages, according to Seeking Alpha Quant. This could indicate undervaluation, so we need to take a closer look at this issue.

Seeking Alpha

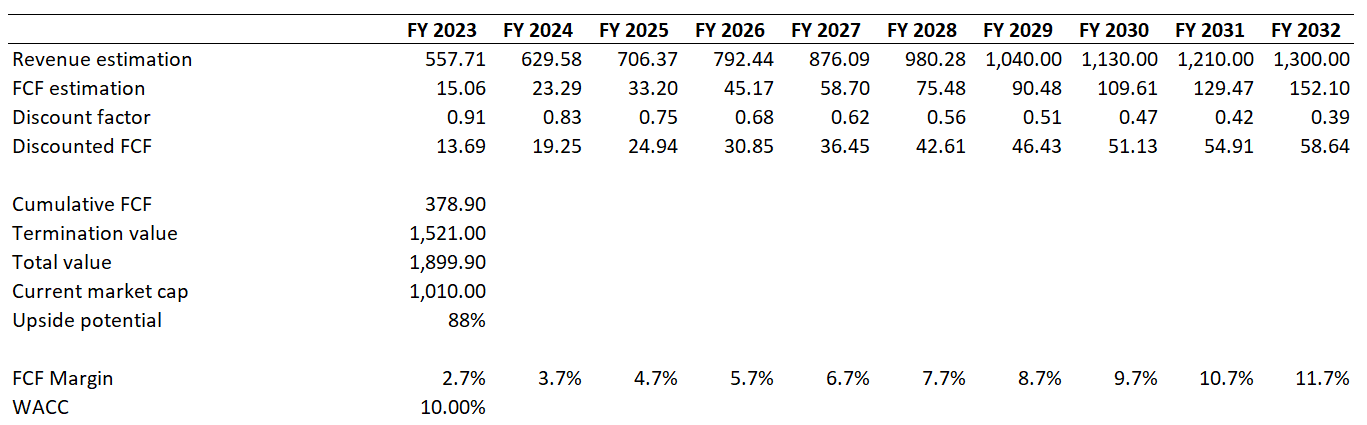

To calculate AMZN stock fair value I implemented discounted cash flow [DCF] approach using WACC of 10% which was provided by Gurufocus. Revenue estimates for the next decade were based on consensus estimates, and a very conservative assumption was made for free cash flow levered margin, which was assumed to be twice lower than 5-year average of 5.4%. To account for potential growth in free cash flow margin, an annual expansion of 100 basis points was factored into the analysis.

Author’s calculations

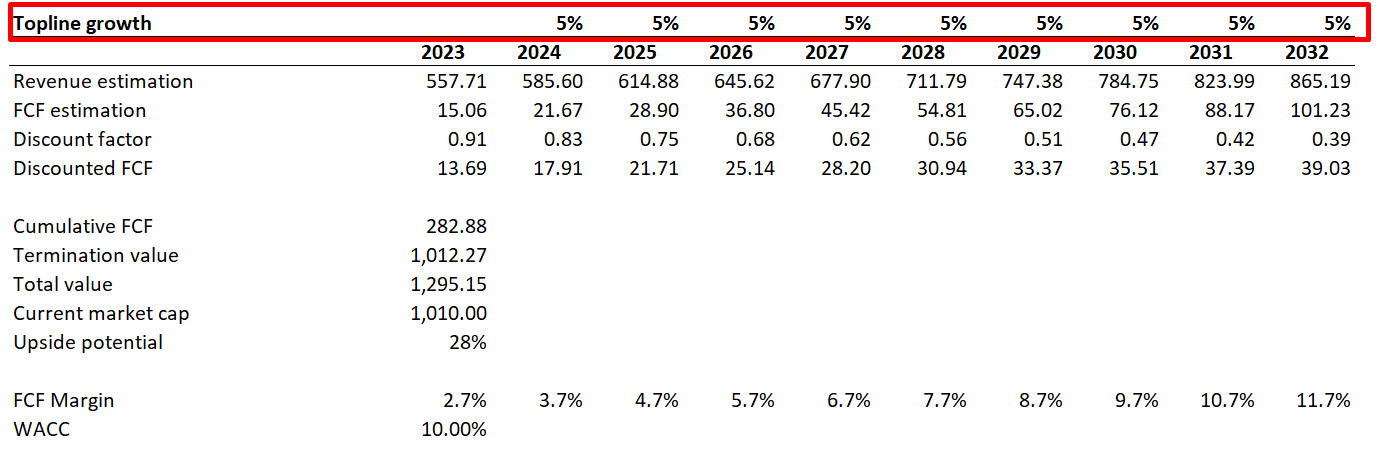

After including all the assumptions described above, the fair value of Amazon’s business was calculated to be 88% higher than its current market capitalization, indicating that the stock is massively undervalued. However, it is very important to remember that DCF analysis relies heavily on assumptions. Therefore, I decided to use more pessimistic revenue growth assumptions to understand the undervaluation of the stock in a much worse case scenario. Consensus estimates forecast a CAGR for revenue of about 10%, so I lowered that value by twice for my pessimistic scenario.

Author’s calculations

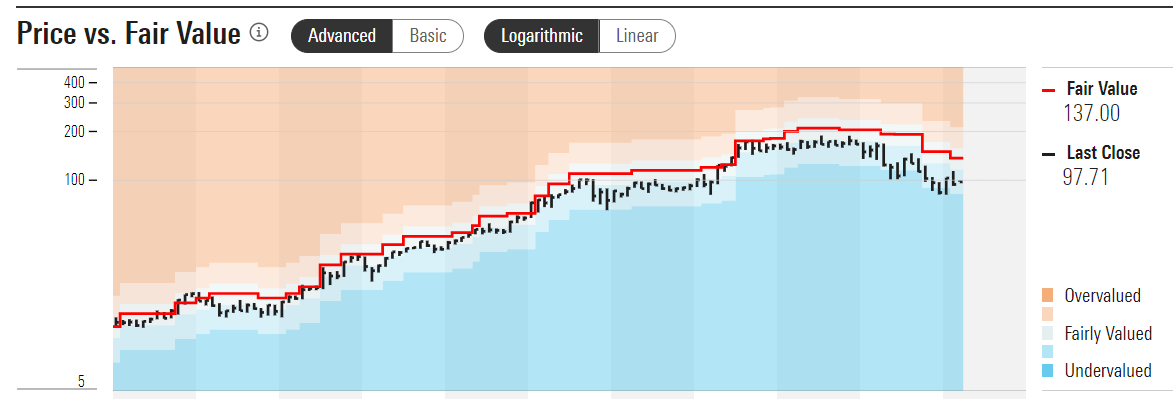

As you can see from the above screenshot, even under very pessimistic topline growth assumptions, DCF indicates the stock is about 28% undervalued. Additionally, Morningstar suggests that Amazon stock is currently traded with 29% discount, while Argus Research gives target price of $165 per share indicating about 65% upside potential from current levels. On the chart below you can see how actual stock price followed Morningstar’s fair value estimations over long-term horizon.

Morningstar

Risks to consider

Since Amazon is a large company with various business lines, investors of AMZN bear numerous risks.

First of all, Amazon’s core e-commerce business faces fierce competition both from traditional retailers like Walmart (WMT) and Target (TGT) and from other online retailers like Shopify (SHOP) or Alibaba (BABA). Competitors possess vast resources and also invest heavily in innovation to increase reach for their online offerings, so it becomes more difficult for Amazon to maintain market share. Amazon’s current main star, AWS, also operates in highly competitive environment where rivals include giants like Microsoft (MSFT) and Alphabet (GOOGL). So Amazon has to continue investing in innovation heavily to be able to adapt in highly competitive environment.

Second significant risk to me is cybersecurity risk, which the company is vulnerable to. As a large technology company Amazon handles vast amounts of sensitive consumer data. Therefore there are risks of cybersecurity threats like hacking, phishing, malware or data breaches. Theft of consumer information with loss of sensitive business data will severely undermine Amazon’s reputation. The company mitigates this risk by investing heavily in cybersecurity solutions, but I believe that the risk is significant for a company like Amazon.

Third, regulatory risks should also be a key consideration for potential Amazon investors. The company’s ability to navigate regulatory risks is crucial because it operates in highly regulated industry including mainly antitrust and data privacy. Being one of the world’s largest e-commerce companies, Amazon faces criticism for the dominance on the market and its impact on competition. The company is frequently under antitrust challenges and reviews both in the U.S. and in Europe.

Last but not least, the general and currently biggest risk is a global economic downturn. Amazon is heavily dependent on consumer spending, and a good economy drives up revenues. In times of economic turmoil, consumers are more hesitant to make discretionary purchases, which will limit sales of non-essential goods such as electronics, clothing and household goods. The economic downturn will also impact the businesses of third-party sellers who rely on the Amazon marketplace to sell their products. This will negatively impact AMZN’s revenue from commissions earned with third-party sellers. To conclude this part: Amazon is not without risks for investors. As discussed above, there are several potential risks associated with investing in AMZN stock. Therefore, investors should carefully consider these risks to understand whether they meet their risk tolerance before making an investment decision.

Bottom line

In summary, despite potential risks associated with investing in AMZN, upside potential by far outweighs these risks. Amazon’s ability to innovate and dominate across multiple business lines, as well as strong brand recognition and customer loyalty, position the company for long-term success. Therefore, I have high conviction that the stock is a strong buy for long-term investors as part of well-diversified investment portfolios.

Disclosure: I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.