Summary:

- Amazon is set to report earnings on August 1st; and overall, my projections call for $151 billion in revenues at group level, while consensus expects $149 billion.

- Amazon’s retail segment poised for double-digit growth, driven by strong consumer backdrop and Prime membership trends.

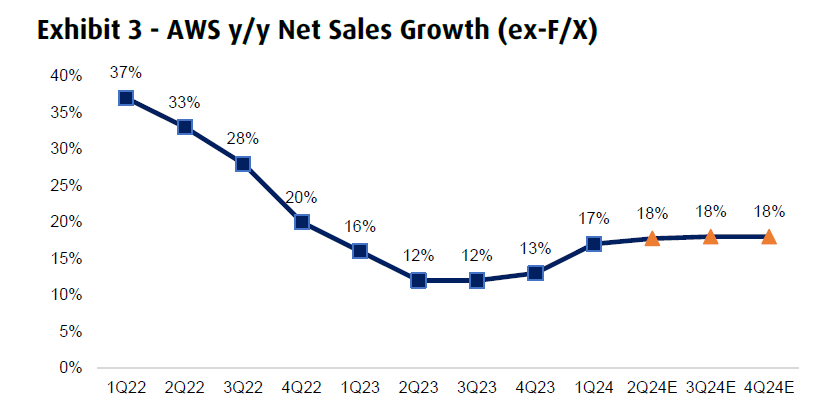

- On cloud, I argue that AWS has continued its strong March-quarter growth trajectory into Q2, driven by product releases and positive market sentiment towards cloud computing.

- AWS business shows strong commercial momentum with multi-billion dollar run-rate in AI/ML.

- I set my target price for Amazon ahead of Q2 reporting, and I see shares as undervalued below $200. “Buy”.

georgeclerk

Amazon is scheduled to report earnings for the June quarter on August 1st, after the market closes. Looking ahead to the upcoming report, I argue that the company’s core retail business is well-positioned for continued growth: The company’s strategic focus on enhancing delivery speeds, expanding Prime membership, and leveraging its advertising platform is driving robust market share gains, while the overall market environment remains healthy, especially in its largest market, the U.S. On that note, I model $91-93 billion in sales for the North America segment and $33-34 billion for the international markets segment. Regarding Amazon’s cloud business, I believe AWS has maintained its strong growth trajectory from the March quarter into Q2, fueled by new product releases and positive market sentiment towards cloud computing. I expect AWS to report $26 billion in Q2 revenue. Consequently, my projections estimate $151 billion in total revenues for the group, compared to the consensus expectation of $149 billion.

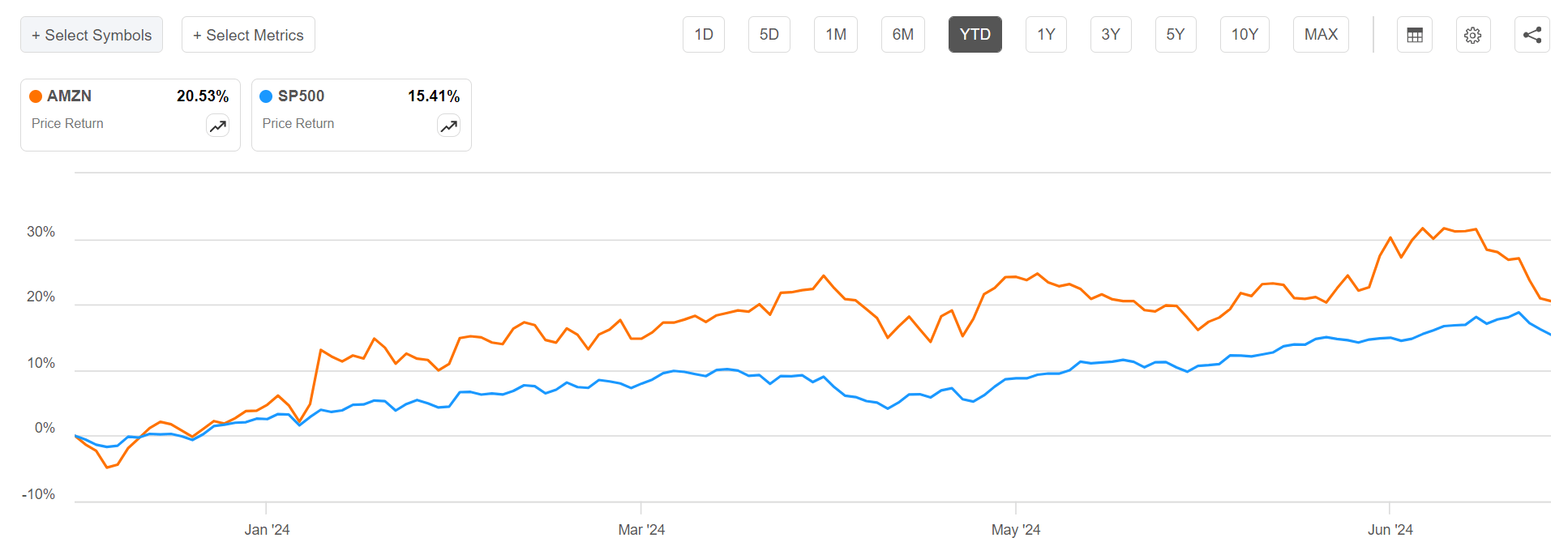

For context, since the start of the year, Amazon shares have notably outperformed the broader market: YTD, AMZN stock is up about 21%, compared to a gain of approximately 15% for the S&P 500.

Seeking Alpha

Since my last coverage, Amazon shares have increased by about 2%, while the S&P 500 has gained approximately 9%. In my latest Amazon article , I discussed the outlook for Amazon’s Q1 performance and concluded with a “Buy” rating. Today, I revisit my thesis for Amazon stock in light of the company’s upcoming earnings report.

The AWS business is firing from all cylinders

Amazon’s Web Services business has likely continued to show strong commercial momentum in Q2, building on trends seen in Q1, with growth trajectory supported by a series of product releases and favorable market sentiment towards cloud. As of the latest reports, AWS has achieved a multi-billion dollar run-rate business in AI/ML, with the AI segment alone projected to drive “tens of billions” in sales in the coming years. Bedrock, AWS’s AI platform, has emerged as one of the fastest-growing services, underscoring the platform’s critical role in the company’s strategy. Additionally, AWS’s market share dominance in cloud computing provides a significant advantage as companies increasingly leverage AI for their data housed within AWS. This has led to material growth in AI/ML workloads, with many AWS customers eager to build on models available through AWS Bedrock for their ease of use, cost efficiency, and security benefits.

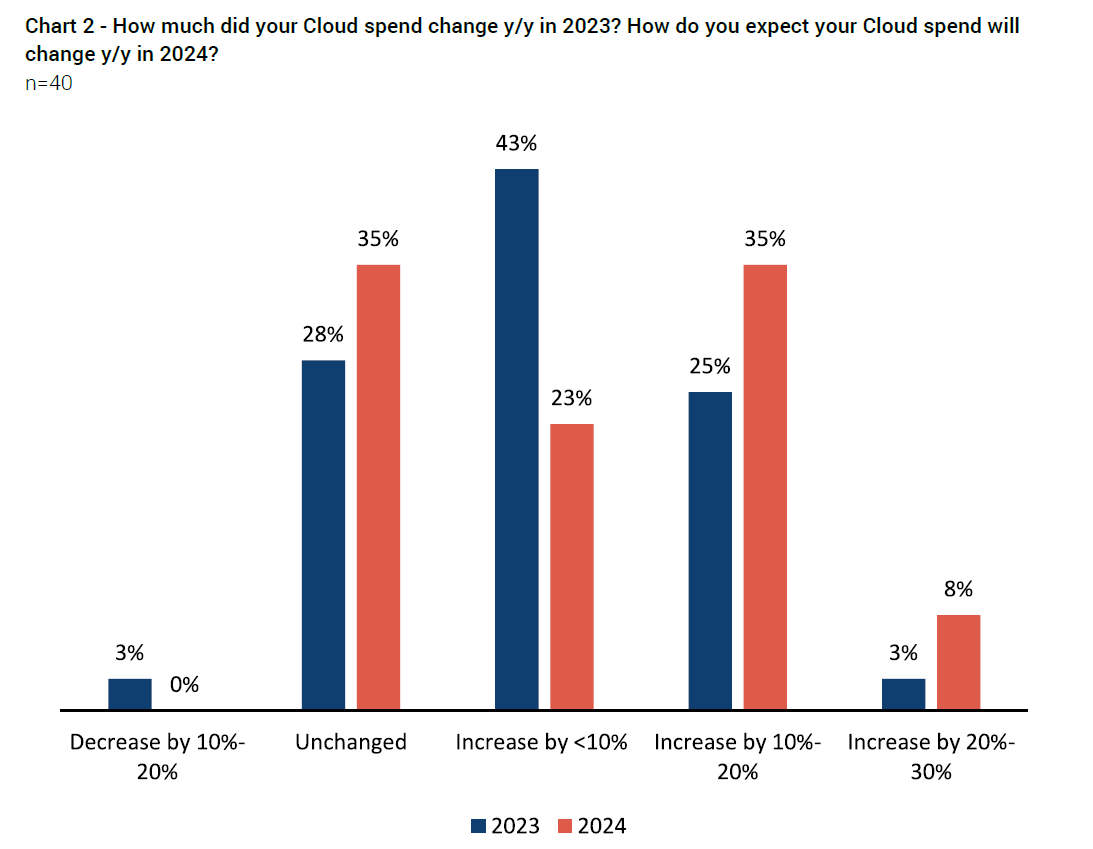

According to a survey conducted by Jefferies, covering 40 CIOs, cloud spending intentions are accelerating. In fact, 43% of respondents highlighted expectations of a more than 10% increase in 2024, compared to 28% who anticipated such an increase in 2023. Moreover, survey feedback suggests a notable, ongoing shift in workloads to the cloud, with 58% of CIOs expecting over 50% of their workloads to be in the cloud by the end of 2025, up from 36% today (Source: Jefferies research note on Cloud survey, dated 8th July). Needless, to say, as the leading cloud company in the world, Amazon should be a prime beneficiary of the favorable cloud spending trends.

Jefferies

Financially, AWS’s importance has grown to be connected to both a growth and value argument: For 2Q24, AWS is expected to report revenue of around $26 billion, with topline expansion accelerating to a 18% YoY (according to BMO estimates; Source BMO, research note on AMZN dated 10th July). With regard to profitability, AWS’s operating income is forecasted to reach $9.5 billion, which implies a breathtaking YoY expansion of around 77%

BMO

Consumer strength supports upside in retail

On the retail front, On a high level, I see Amazon continuing to expand its market share in both B2C and B2B segments, as the company is capitalizing on emerging eCommerce verticals and expanding its presence in international markets, notably emerging markets. For context, in 2023 Amazon delivered about 7 billion Same-Day and One-Day units; which is expected to increase by a double-digit rate to about 8 billion 2024. In my view, this should be a testament to Amazon’s efficiency and retail USP, while delivery speeds is driving increased purchase consideration and frequency among consumers.

Looking at Q2, I project Amazon’s North America segment to generate about $91-93 billion in sales, marking a double digit growth compared to the same period one year earlier. My expectation draws confidence from the strong consumer backdrop in the U.S. and healthy Prime membership trends. According to TD Cowen, in Q2 2024, an estimated 84 million households in the U.S. were Prime members, up from 78 million in the same period the previous year. This increase in Prime membership correlates with strong visiting and purchasing trends, with 94% of Prime subscribers visiting Amazon monthly and 86% making monthly purchases (Source: TD Cowen, research note on Amazon dated July 10th). Moreover, the healthy consumer backdrop is further evidenced by the record-breaking Amazon Prime day in July, with shoppers spending an estimated $14.2 billion during the two-day event, according to Adobe Analytics data. According to my expectation, the company’s international segment will likely report revenues in the range of $33-34 billion.

Valuation update: target price at $201

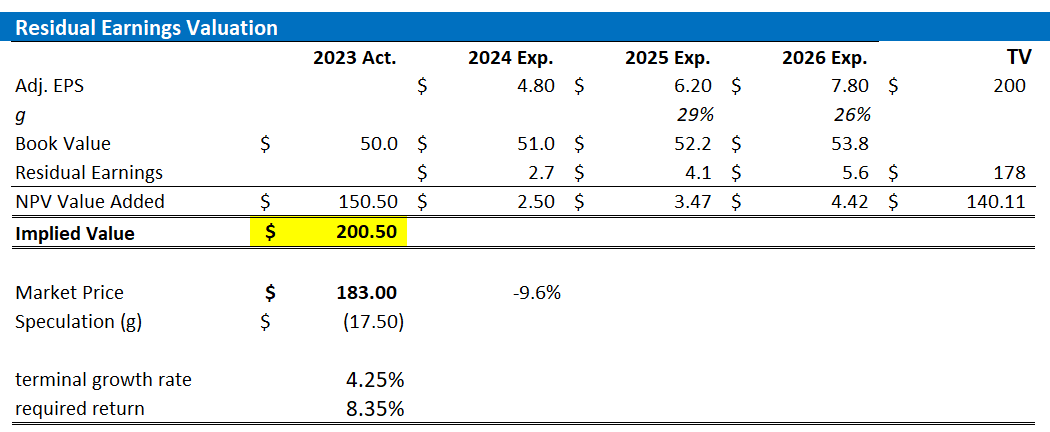

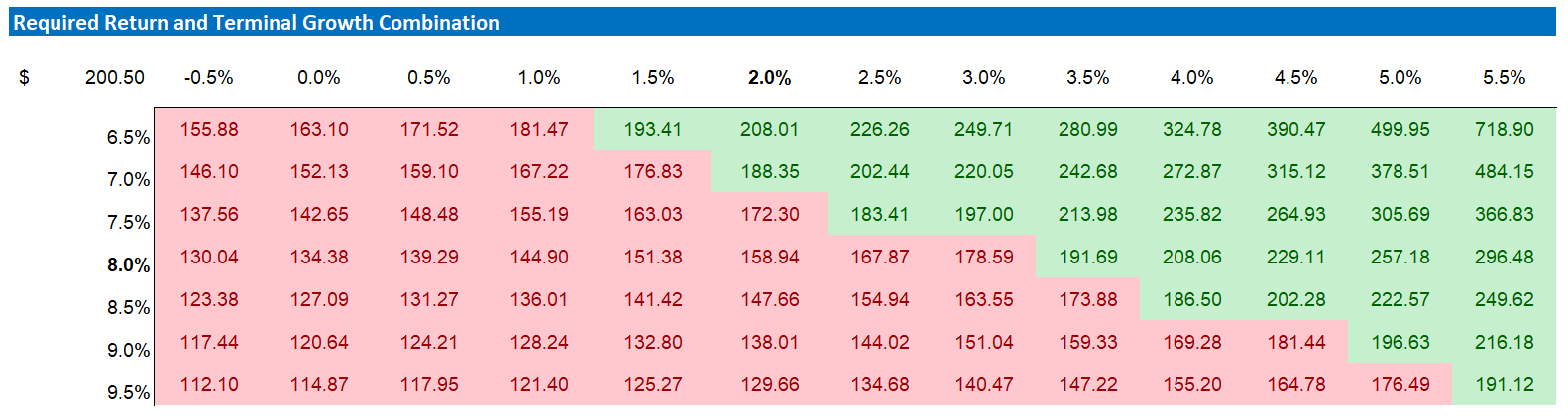

In line with my projections for strong revenue and earnings momentum for Amazon, I have updated my residual earnings model for the e-commerce and cloud giant’s stock. For FY 2024, 2025, and 2026, I now anticipate EPS to be approximately $4.8, $6.2, and $7.8, respectively. These EPS estimates are about 10%-15% higher than consensus, primarily due to underestimations of Amazon’s advertising and cloud momentum. Additionally, I maintain a 3.5% terminal growth rate post-2026 and have adjusted my cost of equity assumption down by 50 basis points to 8.5%, aligning it with the broader Magnificent Seven group. With these updated EPS projections, I calculate a fair implied share price for Amazon at $201.

For context, the value “Speculation” is just the difference to fair implied value. A positive value implies a premium; or in other words, markets are speculating to price a more fundamental upside compared to my estimates. In addition, I highlight that my new valuation model projects EPS for Amazon only through 2026, compared to a long-dated projection until 2028 previously. I view the new calculation methodology as less risky, because the projection horizon has been decreased by 2 years. At the same time, however, this adjustment caused my target price to fall by about $4.

Refinitiv; Company Financials; Cavenagh Research’s EPS Estimates and Calculation

Below you can also find the updated sensitivity table.

Refinitiv; Company Financials; Cavenagh Research’s EPS Estimates and Calculation

Risks to my thesis

In my view, a key risk to this thesis is the potential for increased competition in the e-commerce and cloud markets, which could pressure Amazon’s market share and profitability, especially if competitors enhance their delivery capabilities and cloud offerings. Another risk is the possibility of macroeconomic downturns or shifts in consumer behavior, which could negatively impact Amazon’s sales projections, particularly in the North American and international markets, leading to revenue shortfalls compared to the projected $151 billion.

Investor takeaway

Overall, Amazon’s core retail business is well-positioned for continued growth: The company’s strategic focus on enhancing delivery speeds, expanding Prime membership, and leveraging its advertising platform is driving robust market share gains, while the general market backdrop is healthy (especially in the company’s biggest market, the U.S.). Personally, I model $91-93 billion in sales for the North America segment and $33-34 billion for the international markets segment. Relating to Amazon’s cloud business, I argue that AWS has continued its strong March-quarter growth trajectory into Q2, driven by product releases and positive market sentiment towards cloud computing. In my view, AWS is expected to report $26 billion in Q2 revenue. Accordingly, my projections call for $151 billion in revenues at group level, while consensus expects $149 billion. Concluding, I set my target price for Amazon ahead of Q2 reporting, and I see shares as undervalued below $200. “Buy”.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Not financial advice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.