Summary:

- Advanced Micro Devices, Inc. acquired ZT Systems for $4.9 billion, expanding data center and AI capabilities.

- AMD Q2 2024 earnings beat estimates, with record Data Center revenue and strong guidance for Q3.

- AMD’s recent surge back to mid $150s could lead to a potential breakout to $180 per share, supported by strong market fundamentals.

nmlfd

Last month, Advanced Micro Devices, Inc. (NASDAQ:AMD) was on the verge of breaking out of an extended downtrend. Then, it and the vast majority of semiconductor and AI related equities sustained an extended period of decline that culminated in early August. As it turns out, AMD also touched the bottom of the trading range when the market touched its recent low. Since then, like many other peers, it has substantially appreciated. I believe it is entirely likely that AMD will again test the top of this recent trading range, and potentially break out to the upside this time.

Recent Acquisition

Earlier this week, AMD reported that it will be acquiring ZT Systems, an AI infrastructure provider, in a cash and stock deal worth about $4.9 billion. The transaction also includes a contingent payment that may be worth up to $400 million, based upon reaching certain post-closing milestones.

The acquisition will help AMD expand its data center and AI systems capabilities, and will provide AMD with additional existing AI revenue from its operations. ZT systems also owns a domestic data center infrastructure manufacturing business that AMD intends to divest upon finding a strategic partner. The acquisition is expected to close in the first half of 2025.

AMD CEO Lisa Su noted that

“Combining our high-performance Instinct AI accelerator, EPYC CPU, and networking product portfolios with ZT Systems’ industry-leading data center systems expertise will enable AMD to deliver end-to-end data center AI infrastructure at scale with our ecosystem of OEM and ODM partners.”

Q2 2024 Earnings

At the end of July, AMD reported second quarter 2024 earnings that beat estimates due to multiple factors, including record Data Center segment revenue. AMD’s second quarter revenue came in at $5.84 billion, beating consensus estimates by about $120M, and non-GAAP earnings of $0.69 per share were slightly better than the $0.68 estimate.

As part of its earnings, AMD CEO Lisa Su commented that

“Our AI business continued accelerating, and we are well positioned to deliver strong revenue growth in the second half of the year, led by demand for Instinct, EPYC and Ryzen processors.”

Data Center revenue growth was about 115 percent higher than the same quarter one year ago. Second quarter Data Center revenue was a record $2.8 billion. Moreover, AMD’s Client segment revenue was $1.5 billion, which was a 50 percent year-over-year increase.

Not every segment was as strong. For example, AMD’s Gaming segment was down 59 percent year-over-year to $648 million. This decline was primarily due to a decrease in semi-custom sales. Furthermore, AMD’s Embedded segment realized $861 million in revenue, which was down 41 percent.

AMD provided Q3 2024 guidance expecting total revenue of $6.7 billion, which was a guide higher than consensus analyst estimates of about $6.6 billion.

There are several reasons to expect AMD to remain competitive in coming years, including the company’s history of remaining so with in Intel (INTC) in the market for personal computing chips. It now appears that AMD took a sizable lead in that race since at least mid-2020, when Intel was compelled to announce a delay to its 7nm product due to a defect in the process. At that time, AMD had already brought a 7nm product to market, and has since brought to market a 4nm product.

Despite previously generally lagging Intel in performance, it was able to catch up and eventually surpass that competitor. Now, AMD is likely the second horse in the A.I. chip race, where Nvidia (NVDA) maintains a sizable lead in both technology and market share. It is possible they will one day catch up to NVDA, or at least take a sizable market share by offering reasonably competitive products at a lower price point.

AMD chips are also reasonably competitive for cryptocurrency mining, where its most recent version of the Ryzen 9 is often among the better performing choices at its price point for solving the related algorithms. The competitiveness of AMD’s CPU chips towards such specific tasks is unusual, as it is typically handled by GPUs, such as graphics cards, and application-specific integrated circuits (or ASICs) that are essentially specialists designed to perform only one function.

Technicals

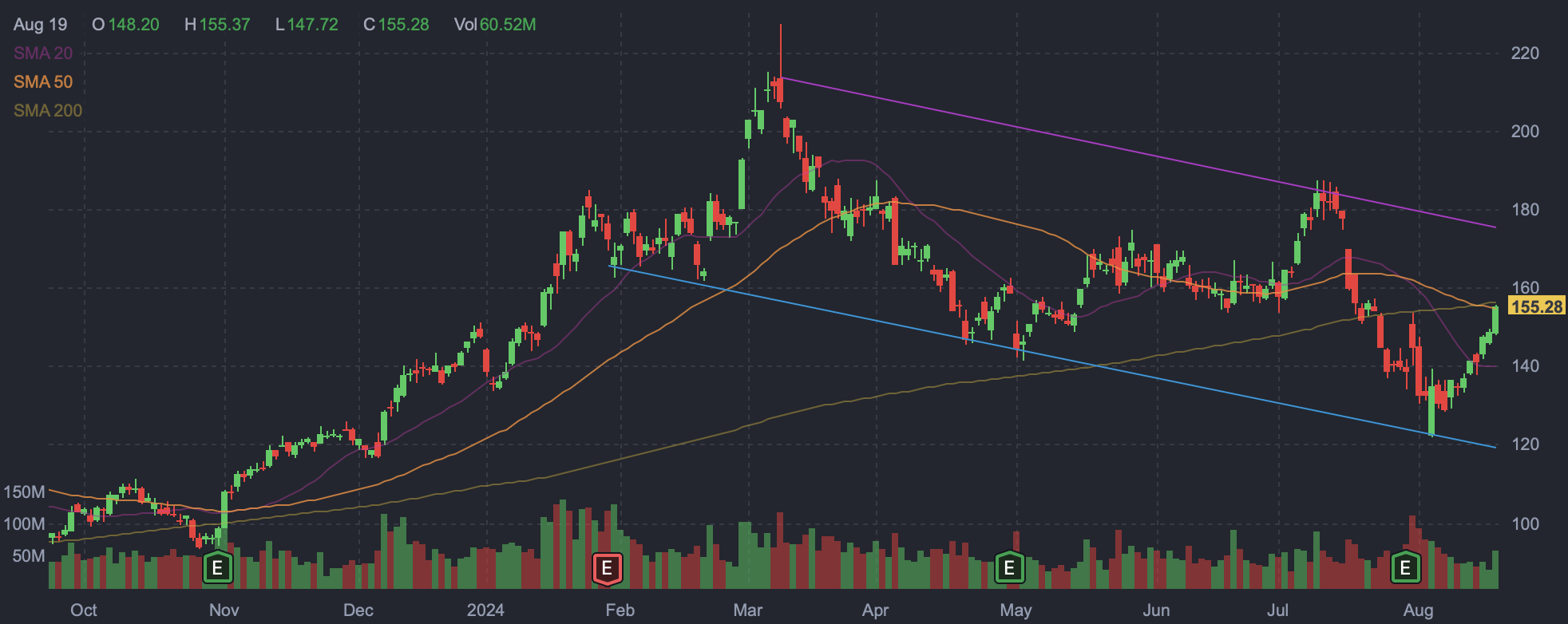

AMD’s recent surge since the market bottomed in early August has taken shares back to the mid-point of the recent trading range, in the $150s. This price point is also roughly coinciding with AMD’s 50 and 200 day moving averages. This pricing is likely to provide some level of resistance, but if AMD can break through here again, it should also act as a level of support.

AMD daily candlestick chart (Finviz.com)

If it can break through the $150s, shares appear likely to again attempt to reach the top of the declining trading range it has been stuck in since around the start of spring of this year. The top of the range is roughly $180 per share, and AMD was there in the first half of July. At that point, it took AMD less than two weeks to make it from the $150s to above $180.

The same could happen in the next two weeks, or at least in the two weeks following AMD’s ability to break above its 50 and 200 day moving averages. Again, shares are basically at those averages, so any continued appreciation could trigger this move higher.

One potential near term catalyst could come in the form of analyst revisions premised upon the acquisition of ZT Systems, as well as AMD’s own recent performance in the second quarter. This acquisition brings with it existing revenue streams, which means AMD should almost certainly realize an increase to its revenue following the combining of ZT’s business into AMD’s. This must result in increases to AMD’s data center and AI revenue after the completion of the acquisition, and this inorganic growth shall eventually be added to estimates for the second half of 2025 and beyond.

Risks

The most apparent risks facing AMD bouncing off this resistance point in the mid $150s and falling back towards the bottom of its trading range, as well as a possible broad market selloff that takes most equities down. If AMD were to fall below the mid $140s, I would lose conviction in AMD making a near term test of the top of its trading range.

Another risk is that analysts react poorly to the ZT Systems acquisition. This appears unlikely, as the market’s immediate response was unquestionably positive. Nonetheless, a change in analyst sentiment would likely act like an anchor to share pricing, and make it more difficult for AMD to move considerably higher in advance of reporting Q3 earnings.

Conclusion

AMD appears to be one of few equities that are likely to be a long-term beneficiary of the current and continuing tailwinds from A.I. and cryptocurrency. Further, AMD is likely to benefit from a potential PC refresh cycle. Despite these probable catalysts, AMD has underperformed since spiking to overbought this spring, where it briefly reached prices above $200 per share.

Last month, AMD almost broke out of its multi-month downtrend, before breaking down and touching the bottom of its trading range when the market bottomed in early August. Since then, AMD has performed exceedingly well and is now back in the middle of its trading rage, at a price point that previously acted as strong support. Any move higher is likely to test the top of this range, at about $180 per share. A potential breakout to higher prices is entirely possible if AMD can report strong earnings and raise guidance when it reports Q3 2024 earnings this autumn.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMDL, AMD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.