Summary:

- Tesla, Inc.’s future financial outlook is uncertain due to macroeconomic conditions, including tightening auto loan standards and rising interest rates.

- The decline in used car prices and the potential for further price cuts suggest that Tesla’s margins will likely continue to deteriorate.

- Tesla stock is overvalued, and the stock price is deviating from weakening fundamentals, making it a risky investment at this time.

sanfel

Investment Thesis

In the second quarter, macroeconomic uncertainties were the highlight for Tesla, Inc. (NASDAQ:TSLA), as executives were not as confident about the future financial outlook as they usually were, as prices were cut and margins narrowed. We think this theme will continue for the rest of the year, and perhaps into 2024. Today, Tesla also announced that it is again lowering prices on certain models in China.

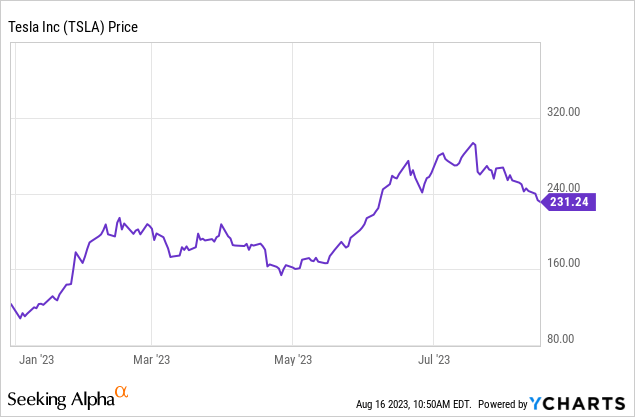

However, based on data on used car prices and other macroeconomic indicators, we believe these latest price cuts may not be the last and margins will continue to deteriorate. But despite the arguably deteriorating fundamentals, the stock still rebounded and is currently still 127.41% off its previous lows from earlier this year. Therefore, we dive into what’s going on, on a macroeconomic basis and gauge where Tesla, along with its margins, is headed in the future.

Economic Malaise

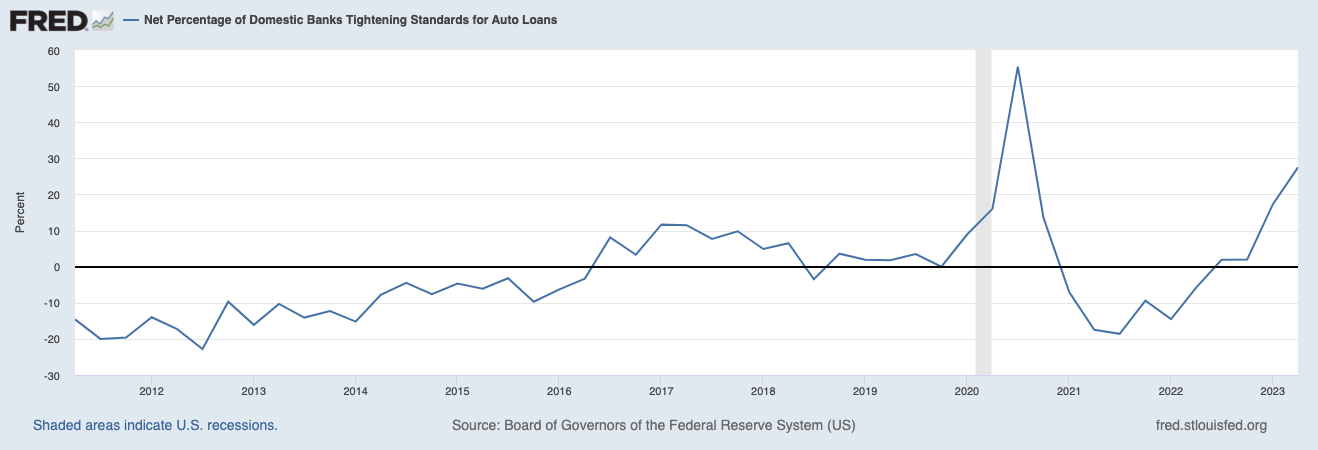

Macroeconomic conditions are not working in Tesla’s favor, to say the least. For example, looking at the Federal Reserve’s Senior Loan Officer Survey, we see that the net percentage of domestic banks that tightened auto loan standards is on the rise. Currently, about 27.5% of domestic banks tightened their auto loan standards in the second quarter.

Federal Reserve (FRED)

It is also needless to say that the auto industry is relatively dependent on a supply of fresh credit and the fact that most consumers buy vehicles based on the affordability of the monthly payments/ installments. Not only is the auto industry taking a secular hit as people put off major purchases during times of economic uncertainty, but right now, there is also the fact that higher interest rates are making monthly payments harder to overcome for the general consumer.

This makes buying a Tesla more expensive for most, even if Tesla has not raised prices. It may also have been one of the factors that contributed to Tesla’s amazing price cuts across its lineup this year. As Elon Musk mentioned during the earnings call:

Buying a new car is a big decision for the vast majority of people. So, any time there’s economic uncertainty, people generally pause on new car buying at least to see what happens. And then, obviously, another challenge is the interest rate environment. As interest rates rise, the affordability of anything bought with debt decreases, so effectively increasing the price of the car. (Elon Musk, Q2 Earnings Call.)

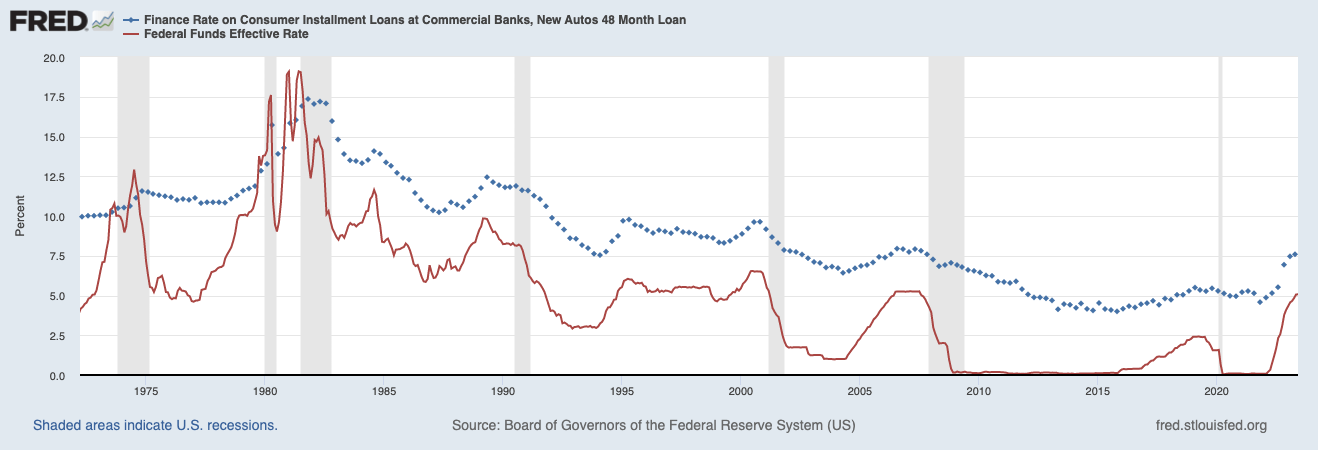

Looking again at the Federal Reserve data, we see that interest rates on 48-month loans have increased from about 4.58% in November 2021 to 7.59% according to the most recent data. However, taking into account recent rate hikes, we think these loan rates are well on their way to 8%, or more or less the same rates as in 2006-2008 when Fed Funds rates were also at 5.50%.

Federal Reserve (FRED)

Putting these rates in context, the difference in interest rates on perhaps Tesla’s most popular car, a base Model Y, is certainly noticeable. A base model costing $52,130 carries $7,451 in interest costs on a 72-month loan at 4.5%, while this now rises to $13,679 on financing at 8%. In other words, a base Model Y has become $6,228 more expensive, or a 10.45% price increase just because of interest rates. Elon Musk also commented on this fact during the latest earnings call by saying:

So when interest rates rise dramatically, we actually have to reduce the price of the car because the interest payments increase the price of the car. And this is — at least up until recently, it was, I believe, the sharpest interest rate rise in history. So, we had to do something about that. If somebody’s got a crystal ball for the global economy, I really appreciate it, if I could borrow that crystal ball. (Elon Musk, Q2 Earnings Call.)

Something not often discussed, for example, is the fact that Tesla recently introduced even 84-month car loans, allowing users to extend the term of their car loan, whereas the longest term was previously 72 months. While this could essentially increase affordability, customers will end up paying more interest. On the other hand, customers can still take advantage of a federal tax credit of up to $7,500 on certain models thanks to the Inflation Reduction Act.

They have also recently launched a number of other incentives, such as offering 3 months of free Full Self-Driving (FSD) and are reportedly offering some hefty discounts on stock models. In the earnings call, Elon also unveiled an incentive to get users to switch FSD in Q3, which may also cause people to upgrade their cars. In terms of Elon Musk’s other key economic comments, he also seemed rather pessimistic, pointing out a number of other factors, such as the surge in credit card debt and the interest payments associated with it, that are eating up people’s monthly budgets.

So, if interest rates continue to rise, that reduces the affordability of cars. And for a lot of people, they’re really — they’re just really breaking even every month. In fact, if you look at the rise in credit card debt, they are, in fact, not breaking even every month. Credit card debt is looking scary. So, we just don’t control the market conditions. If market condition is stable, I think prices will be stable. If they’re not stable, then we would have lower prices. Yes. (Elon Musk, Q2 Earnings Call.)

Federal Reserve (FRED)

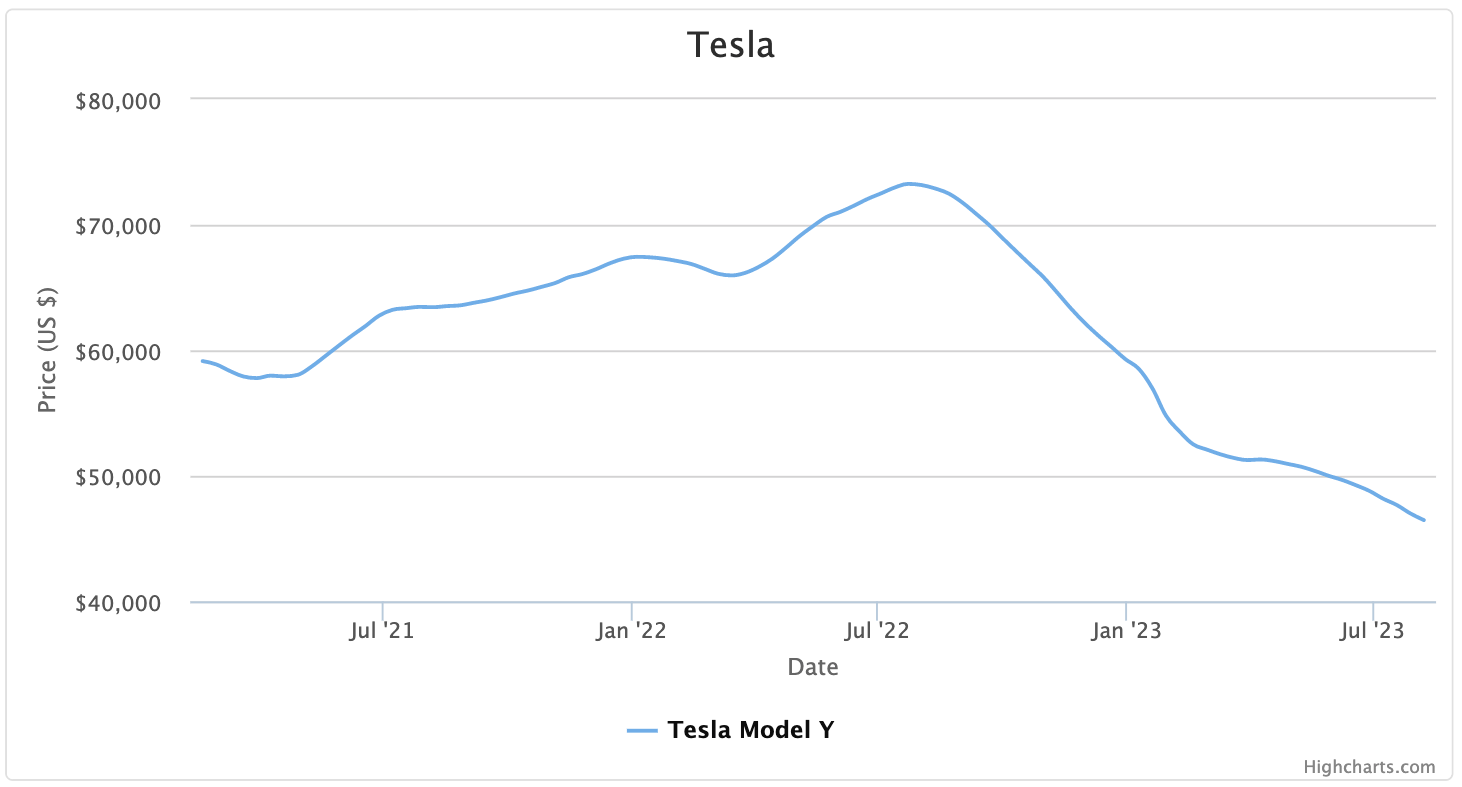

Speaking of price cuts, we think the latest Model 3 and Model Y price cuts may not be the last for this year, looking at data on used car sales prices. According to data collected by Cargurus, the list price for a Tesla Model Y fell from $73,228 at its peak in 2022, to the end of the second quarter with an average list price of $50,166. Since then, however, the average list price has continued to decline and currently stands at $46,472.

CarGurus

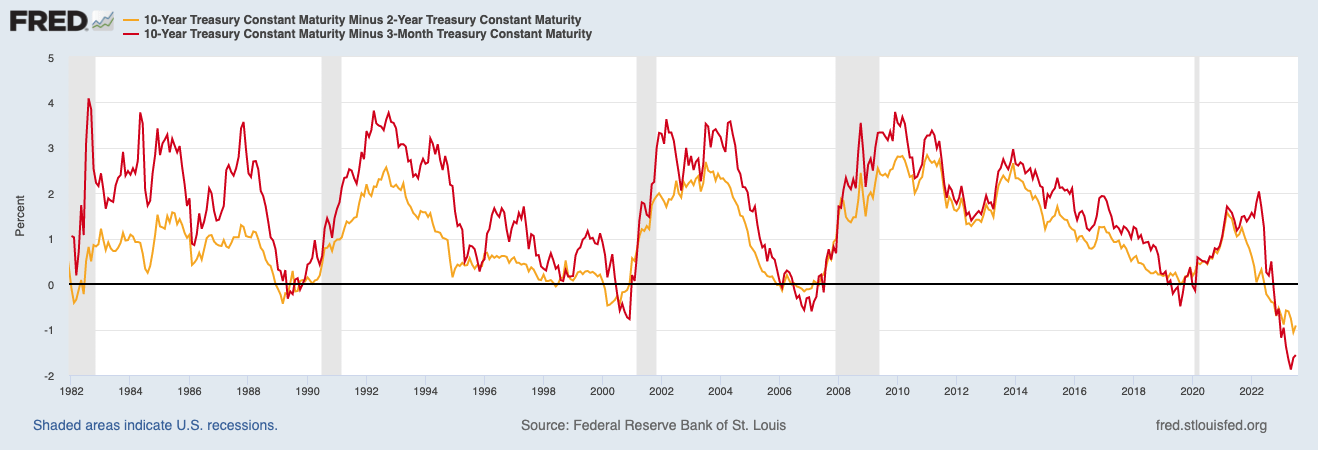

And if we look at some of the most reliable economic indicators, the yield curve, we see that the spread between both the 2-year and 10-year treasuries, and the 3-month to 10-year treasuries is as inverted as ever before. In recent history, an inversion of this magnitude has always signaled a recession, and we think this time is no different and that a recession is still in progress for 2H 2023.

Federal Reserve (FRED)

Elon Musk also addressed the fact that even they themselves can’t seem to figure out where the economy is headed in the future, where sometimes demand looks good, while sometimes it looks like the economy is falling apart on a global scale:

So, I mean, one day, it seems like the world economy is falling apart and the next day, everything is fine. I don’t know what’s going on. It’d be totally fine. I wish I did. (Elon Musk, Q2 Earnings Call.)

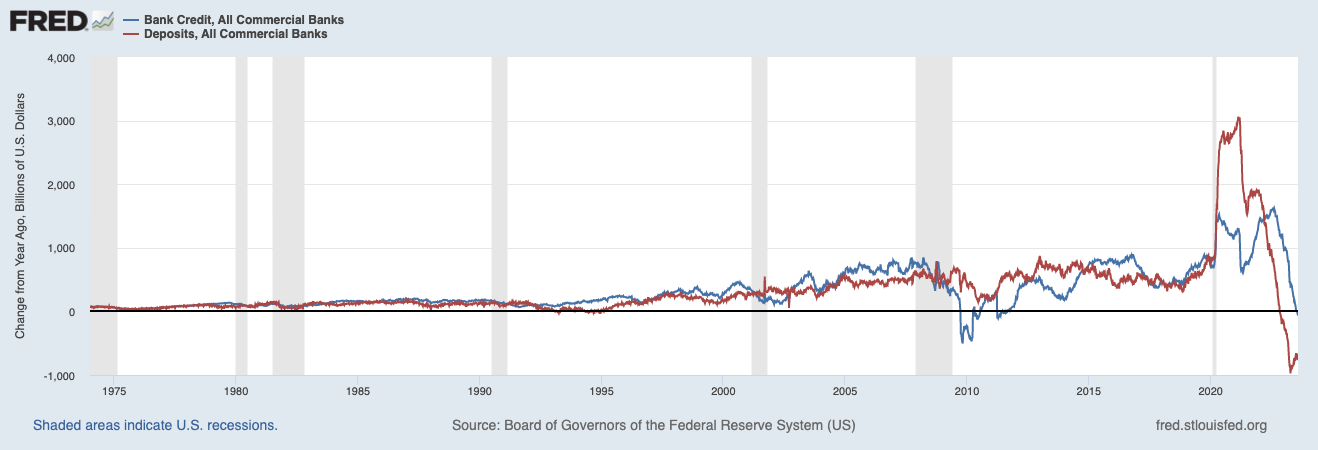

The credit market per se, looking more specifically at lending and leasing volume, also seems to be experiencing some hiccups lately, with monetary policy at its tightest in decades. When you combine this with the fact that there is apparently still deposit flight, with money flowing into money market funds at staggering rates, banks are, to say the least, not eager to make more auto loans or expand their loan portfolios. For now, it appears that a combination of credit scarcity and deflationary forces will plunge the U.S. into recession, with more hard times ahead for Tesla.

Federal Reserve (FRED)

The Trillion-Dollar Question

As for the trillion-dollar question, when it comes to valuation, we think Tesla’s future depends mostly on a mix of automotive margins, fully self-driving and other innovative projects in robotics, energy and compute, for example.

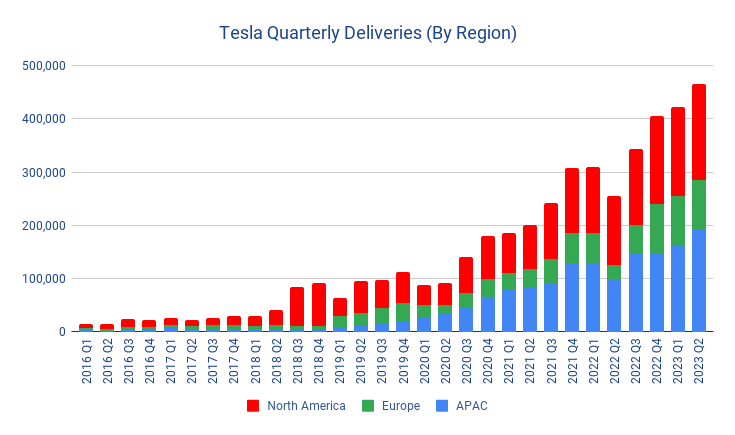

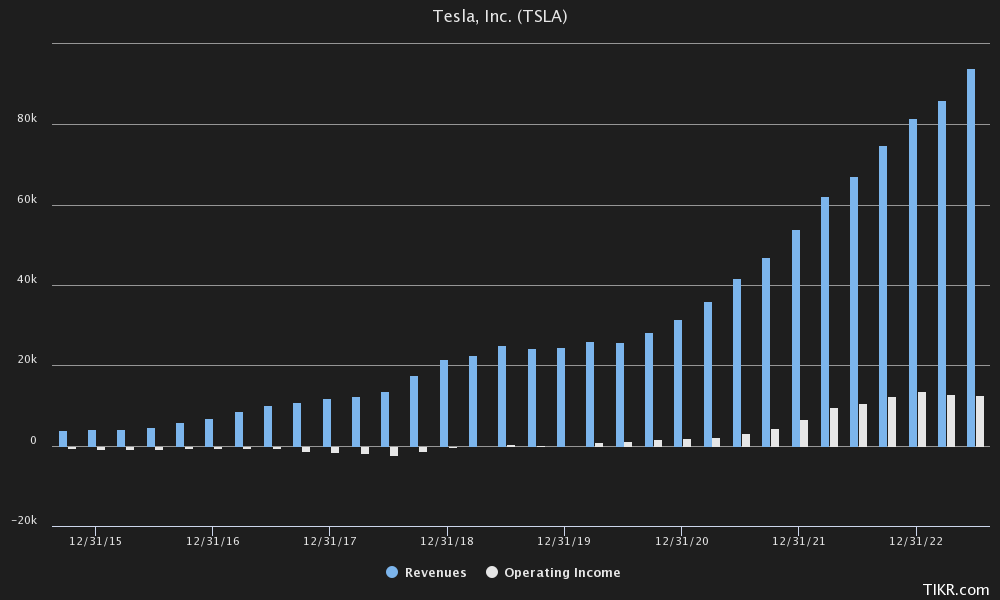

To start with automotive margins, we are not overly optimistic at this time about Tesla’s ability to grow volume, or at least not at the expense of automotive margins. While Tesla can be lauded for its volume growth, which will reach 466,140 deliveries per quarter as of the second quarter of 2023, we think it will come at a heavy cost to its automotive gross margins.

Author’s Data & Tesla IR Data

We have previously noted the decline in the resale value of both Model 3s and Model Ys, which make up the bulk of Tesla’s volume, and we can imagine these going hand-in-hand with their gross margins for cars. While we saw the resale value of both models plummet, so did Tesla’s car margins. In other words, we think that while Tesla is growing volume, it is not growing at a rate that is favorable to their net profits. In the chart below, you can also see that each quarter on a Trailing 12 months (TTM) basis, revenue is still growing, while operating income has remained essentially flat.

TIKR

So we think the “trillion-dollar question” has mostly to do with autonomy and Tesla’s ability to monetize their existing fleet in the future. During the last earnings call, Elon Musk even boldly emphasized that they believe it makes sense to sacrifice margins, because they believe they can unlock much more value with FSD:

So, I think it’s sort of, it would be — I think it — it does make sense to sacrifice margins in favor of making more vehicles because we think in the not too distant future, they will have a dramatic valuation increase. I think the Tesla fleet value increase at the point which we can upload full self-driving and is approved by regulators will be the single biggest step change in asset value maybe in history. (Elon Musk, Q2 Earnings Call.)

And although there are already other players that are almost fully operational, such as Waymo & Cruise, we are not entirely sure that Tesla can be released to the general public anytime soon, because their technology depends on vision and still needs to be refined. Even Waymo & Cruise, who use more sensors and Lidars, still have problems from time to time. So we wouldn’t count on receiving any meaningful net income from that side of the business any time soon.

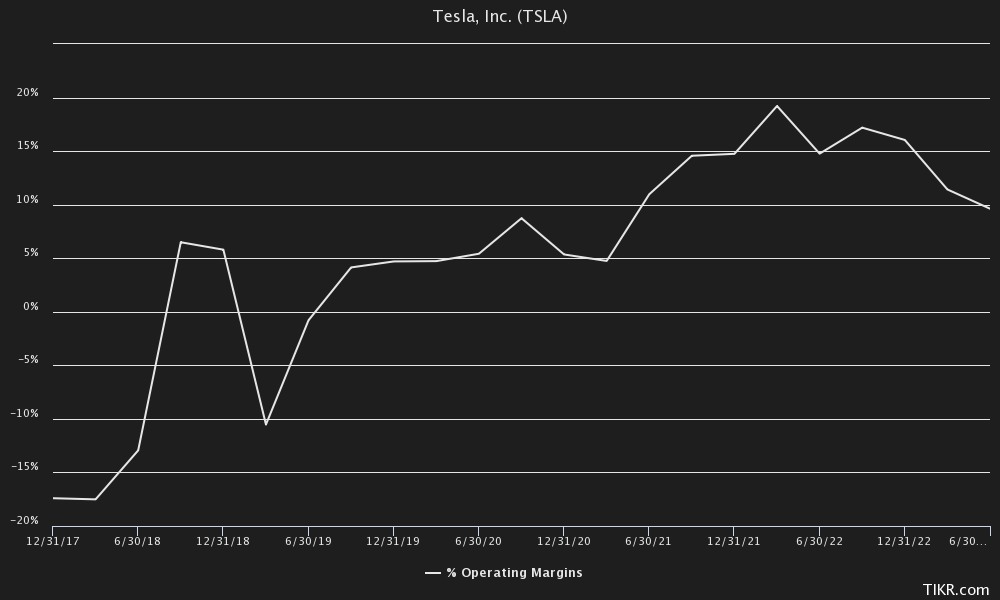

In terms of margins on operating income in general, as mentioned earlier, we think there is more room for downward adjustment as the resale value of used models still seems to be declining and as Tesla continues to grow volume by nearly 40%. If margins were to stabilize around 10%, as we saw in the second quarter, that would also be closer to BYD’s (OTCPK:BYDDF) (OTCPK:BYDDY) operating margins, which have historically averaged around 6-7%.

TIKR

If we take Tesla’s revenue of $24.93 billion as of the second quarter on an annualized basis and apply a 10% operating margin, we are left with $9.97 billion in operating income. If Tesla were able to maintain these margins while growing volume at a 40% CAGR, we believe it would be trading at fair value with a PEG ratio of 1x. In other words, we think that in an optimistic scenario Tesla should be worth buying at about $398.88BN, or $125.67 per share.

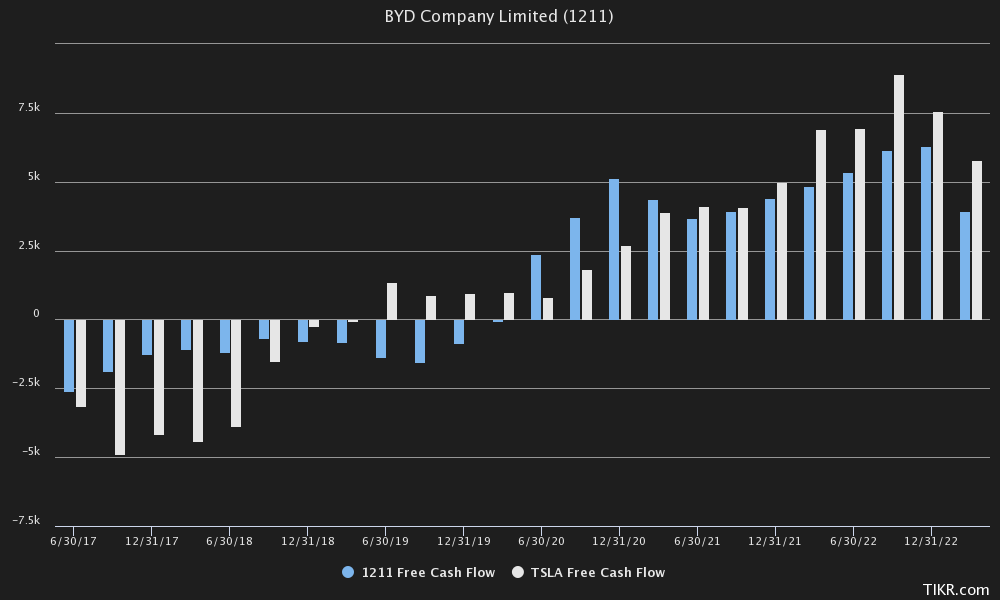

However, if we look at it from a relative valuation perspective and value it based on Free Cash Flow, we believe Tesla is also quite overvalued. Tesla’s Chinese competitor, BYD, for example, has a very similar Free Cash Flow profile to Tesla, while only trading with a market cap of $94.46 billion. While we believe that China is also currently going through some tough macroeconomic times, we find it hard to believe that Tesla should be worth more than 5x as much as BYD from a free cash flow (“FCF”) perspective as it is now.

TIKR

Even if we took Tesla’s FCF from the past 12 months, which totaled $6.16BN, and applied a multiple of 40x, Tesla would only be trading around $246.48BN, or just $77.66 per share.

And speaking of China, Tesla even announced today that it is lowering Model S and Model X prices by another 6%, which did not surprise us since they are still facing stiff competition from BYD. A few days ago, they also lowered the prices of some Model Y stock models in China.

The Bottom Line

We believe Tesla, Inc. stock is currently both overvalued on a relative and absolute basis. With the current growth outlook, pressure on margins and increasing competition, we believe Tesla’s fair value is below its current price of $233 unless Tesla’s ability to deploy an autonomous fleet quickly becomes a viable proposition. While we generally do not go short equities, we believe it may be best for investors to either currently hold the stock or to reduce their exposure, looking objectively at the available data.

Rather, we would take a cue from Elon’s book and follow the advice he gave to smaller/private shareholders about buying/holding or selling the stock. As it stands, we think the stock price is deviating in the wrong direction from fundamentals, which are weakening. Unless we believe in a huge unlocking of the value of an autonomous vehicle fleet, we believe Tesla does not present a buying opportunity at this time.

I love you, guys. And so, we can’t control these macro shocks or the thematic depressive nature of the stock market. So, that’s why I recommend against margin loans in times that are turbulent. If times are not that turbulent, actually margin loan can be a smart move within reason. But we’re in, I would call it, turbulent times. (Elon Musk, Q2 Earnings Call.)

We think it is likely that Tesla, Inc. stock is heading for its previous lows, after which we believe it could become a buying opportunity again.

And then generally, if you see — if you provide your confidence about what that company’s products or services are, when the market panics, buy; and when the market is overly exuberant, you can sell. I’m not recommending you sell Tesla, but yes, buy low, sell high. (Elon Musk, Q2 Earnings Call.)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.