Summary:

- I think A. O. Smith is a wonderful business. I think this is very much a growth business, as evidenced by the uptick in revenue and net income over the years.

- The issue I have is that the shares are no longer objectively cheap. In this game, a 10% difference in valuation matters, so I don’t want to add it here.

- I would normally sell put options, but the premia on offer for decent strikes is too thin in my estimation. That said, short puts have done well over time for me.

cemagraphics

It’s been just shy of six months since I wrote my bullish piece on A. O. Smith Corporation (NYSE:AOS), and in that time, the shares have returned about 5% against a loss of 1% for the S&P 500. I absolutely hate to brag, so I’m just going to let that relative performance sink in for a moment. Anyway, in this article I want to decide whether or not it makes sense to add to the position, hold it, or take profits. I’ll make that determination by looking at the most recent financial results, and by looking at the stock as a thing distinct from the underlying business. Additionally, I want to write about how my options trades have worked out, because I think these offer interesting lessons in risk adjusted returns for all investors.

As the new year dawns, and dim memories of holidays mercifully fade, we all become a bit more busy. I imagine my readers are busy planning exotic vacations, doing groundbreaking research in some new field of science. For my part, the holidays caused me to miss dozens of hours of my favorite soap operas, so I’ve got lots of watching to do. Because you’re busy, you may not have time to read an entire article, especially one as riddled with tedious self-congratulation as mine tend to be. For that reason, I present to you a “thesis statement” paragraph. This gives you the gist of my thinking, so you won’t have to wade through the full 1,600 of my words. You’re very welcome. Anyway, I really like A. O. Smith, and I anticipate the dividend growing from current levels. My problem is that the shares are no longer objectively cheap. So I’ll be holding, but not buying more. I’ll buy aggressively on any pullback, though. Additionally, while I’ve earned a great risk adjusted return of about $8.55 on short puts here, and I love to repeat success when I can, I won’t sell puts at the moment. This is because the premia on offer is too thin in my view. Thus, I can do nothing but sit, wait, and hope for a significant drop in price. I may miss further upside, but I’m of the view that capital preservation is more important at the moment. There you have it. That was my “thesis statement.” If you read on from here, that’s on you.

Financial Snapshot

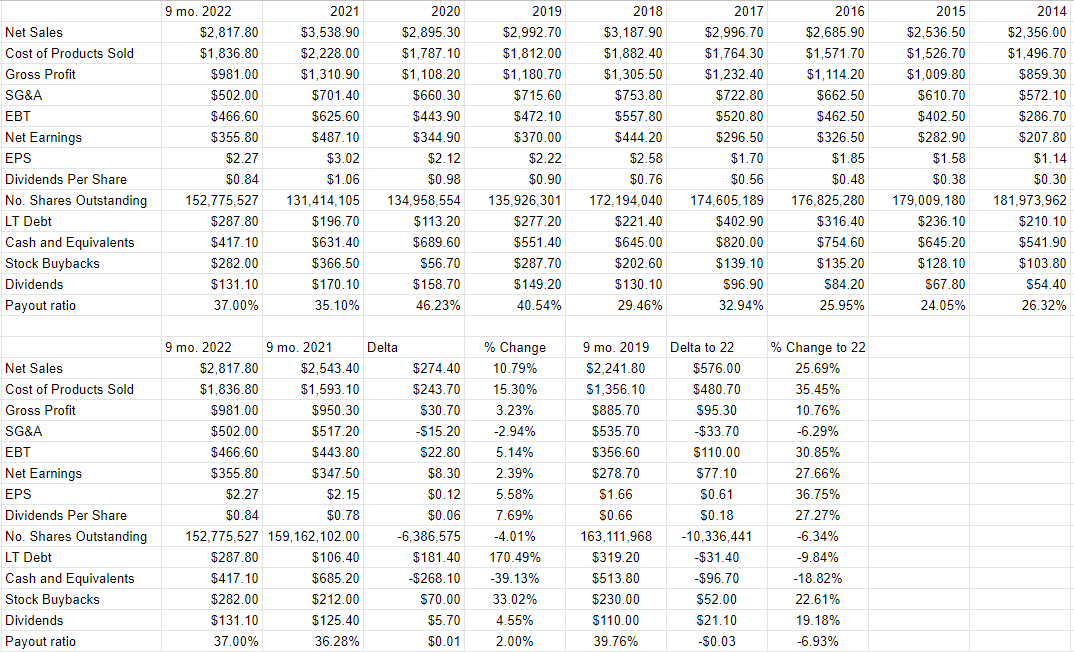

The financial performance over the first nine months of 2022 was quite good in my estimation. Revenue and net income climbed by 10.8% and 2.4% respectively. That net income figure may not seem like much, but let’s not forget that 2021 was a banner year for the firm. Relative to the pre-pandemic era in 2019, for instance, revenue and net income in 2022 were higher by 25.7% and 27.7% respectively. Growth has been robust. Another way to frame this is by saying that earnings per share during the first nine months of 2022 was about 2.25% higher than it was during the whole of 2019.

It’s not all sunshine and lollipops over at A. O. Smith, though. The capital structure has worsened considerably compared to 2021. Long term debt is up about $181 million, or 170% compared to the same time last year, while cash is lower by about $268 million, or 39%. Before I try to make my fainting couch, though, I should also recognize the fact that long term debt is $31.4 million lower today than it was in 2019. So, 2022 is not anomalous, 2021 was.

I’m of the view that the financials here are quite strong. I’d be very happy to add to this position at the right price.

A. O. Smith Financials (A. O. Smith investor relations)

The Stock

My regulars know that I’ve talked myself out of some profitable trades with the words “at the right price.” So, if you’re heading to the comments section to write about how my fastidiousness in this regard is self-harming, save yourself the effort because I’m way ahead of you. In response to this criticism, I’d point out that I’m of the view that it’s better to miss out on some gains than lose capital. My regulars also know that I consider the “business” and the “stock” to be quite different things. Every business buys a number of inputs and turns them into a final product, like water heaters, and boilers for instance. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd’s rapidly changing views about the future health of the business, future demand for products, future margins, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about “the market” in general. A reasonable sounding, if counterfactual, argument can be made to suggest that shares of A. O. Smith would have done even better if the S&P 500 itself hadn’t dropped since I bought. It’s impossible to prove this point definitively, but it’s worth considering. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it’s a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. In my experience, this is the only way to generate profits trading stocks: by determining the crowd’s expectations about a given company’s performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I’ve also found it’s the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

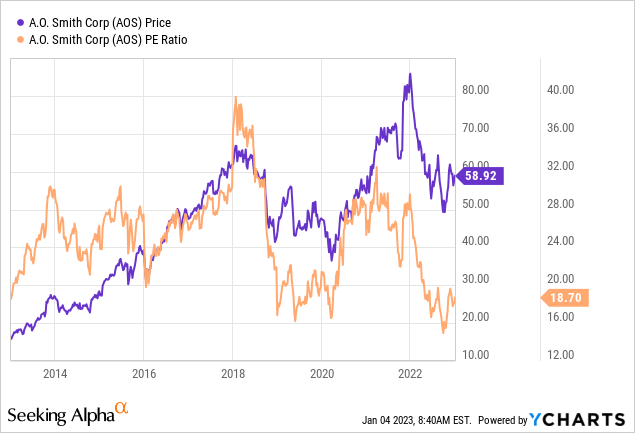

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. In case you don’t have your copy of “Doyle’s Almanac of 2022 Trades” in front of you, I turned very bullish on this stock when it hit a PE of 17, and sported a dividend yield just over 2%. Fast forward to the present and the shares are about 10% more expensive, and the dividend yield is about 5% lower for people just coming to this party, per the following:

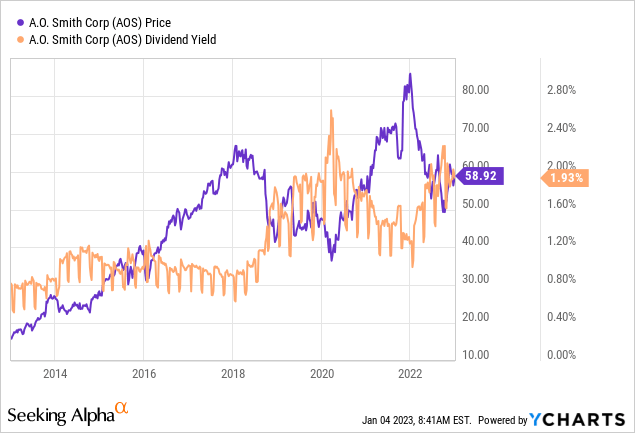

Although the yield is about 5% lower than it was when I last reviewed the name, per the following, it’s still rather high by historical standards. This is obviously a function of the growth in dividends per share, and the fact that the stock has dropped about 29% over the past twelve months. Given the currently low payout ratio of about 37%, I think it reasonable to suppose that the yield will rise even further from current levels.

As my regulars know, I also want to try to understand what the crowd is currently “assuming” about the future of a given company. If the crowd is assuming great things from the company, that’s a sign that the shares are generally expensive. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Anyway, applying this approach to A. O. Smith at the moment suggests the market is assuming that this company will now grow profits at a rate of about 6% from here. That is a pretty optimistic forecast in my view, which doesn’t fill me with a strong urge to buy more shares. Given that I’m in the mood to preserve capital, I’ll not add to my position here.

Puts As Alternative?

In my previous missive, I pointed out that I have earned about $8.55 in put premia on A. O. Smith over the years. I also pointed out that my short puts had done very well relative to shares when the stock cratered earlier. Specifically, my puts had lost about $.60 as the bid price jumped higher, while the stock had lost about $15. In my view, my experience here demonstrated yet again that my short puts often offer a superior risk adjusted return when compared to stocks.

While I love to try to repeat success, I can’t in this case, because the premia on offer for acceptable strike prices is way too thin in my estimation. For instance, the July puts with a strike of $45 are bid at $.50, which represents an annualized yield of about 2.2%. Thus, selling puts isn’t worth it at the moment, though I’ll continue watching, and hoping for weakness in the stock.

Disclosure: I/we have a beneficial long position in the shares of AOS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.