Summary:

- Apple is a market-leading technology firm with great hardware and software integrations and continued expansion into new services products.

- Despite being a market leader, current valuations ignore weakened profitability and a bearish macroeconomic environment.

- Better opportunities for extracting alpha exist in a largely undervalued market environment.

- Shares potentially trading at a 20% premium relative to intrinsic value.

- Sell rating issued (downgrade).

EKIN KIZILKAYA

Investment Thesis

Apple (NASDAQ:AAPL) is perhaps the most influential technology firm currently in existence. Their devices are market-leading thanks to tight hardware and software integrations with substantial expansion into new services products further driving growth for the firm.

However, even a reasonable Q4 and new releases of iPhones and Macs have not been able to save the firm’s fiscal year 2023 results. Current valuations appear to ignore what is fundamentally a weakened profitability situation at the firm along with a truly bearish macroeconomic environment.

Given that shares may be around 20% overvalued, I have no choice but to downgrade Apple back to a “sell” rating on the basis of their FY23 results and FY24 forecasts.

While I do still like the firm in the long-term, better opportunities exist to extract alpha in a mostly undervalued market environment.

Company Background

Apple FY23 10-K

Apple is an American MNC headquartered in Cupertino, California. The influence Apple holds from both fiscal and societal perspectives is truly unrivalled in the technology industry.

Most of Apple’s revenue arises from their physical technology sales with primary sales coming from their iPhone devices, Mac personal computer range or from the host of other technological accessories such as smartwatches the brand produces.

Apple’s products occupy the luxury end of personal technological devices market with pricing softening being very premium compared to many competitors. Significant diversification into the services industry has positively contributed to the firm’s overall revenue streams and signals a slight pivot in their business strategy.

The firm is trying to shift away from being just a device manufacturer and become a more integrated, unavoidable element of most people’s daily lives through the provision of a wide range of entertainment, financial and health services all accessible solely through their hardware devices.

Apple still has the highest valuation of any company currently being publicly traded with their current market cap of around $2.80T.

For a full in-depth analysis please read my original article written back in February: “Apple: The Right Company At The Wrong Price” and my previous moat-update from Q3: “Apple: The iPhone 15 Changes Things, But Is It Enough?”.

Economic Moat – Full-Year FY23 Update

From an economic moat perspective, little material change has occurred since my last Q3 FY23 update.

Apple’s iPhone 15 sales appear to have been relatively strong despite a softening consumer environment which aligns with my expectations given the introduction of USB-C and the dynamic island features to even the base devices.

Since Q3, Apple has released an updated set of “M” series processors with the Cupertino based tech giant opting to release all three iterations of their M3 chips at once.

Traditionally, Apple has stuck to initially releasing two base model chips with each new iteration of Apple silicon: a binned (de-rated) base chip and a standard performance chip. However, this time Apple introduced a binned M3, standard M3, binned M3 Pro, standard M3 Pro and an M3 Max chip all at once.

The very weak demand for Apple’s M2 chips is largely the reason consumers have been provided with a new set of processors less than a year since the M2 Pro and Max chips were introduced.

Nonetheless, the M3 chips appear to offer customers with around a 20-30% boost in computing performance depending on the type of work done along with a slight improvement in battery life thanks to the new 3nm architecture upon which this chip is built.

While the release of the M3 powered MacBook Pros and iMac is nice to see (especially given the previous iMac still ran a base M1 chip), I am not sure this new iteration of chips expands Apple’s competitive advantage any further in the chip design space.

On the contrary, competing chip designers such as Qualcomm (QCOM) have recently unveiled their newest ARM-based PC chips which appear to best even Apple’s M3 lineup in benchmarking software results.

While these chips will require Microsoft’s (MSFT) Windows on ARM to become more mainstream before their widespread adoption can occur, the head start Apple has got in the ARM-base laptop and computer market appears to slowly be contracting.

While I do still see Apple as having a concrete competitive advantage both from a chip design and overall computer hardware perspective, it is undeniable that the competition is working hard to catch up.

In the long-run I fully expect the performance divide to fade away but still believe Apple’s more holistically optimized hardware and software ecosystem will provide moatiness to the Mac line of computers in the future.

Apple’s services have continued to grow in revenue with the segment now generating 22% of revenues in FY23 up from around 18% in FY22. I believe the significant expansion of Apple TV’s production capabilities combined with holistic improvements across Apple’s software services ecosystem have contributed to this strong growth in net sales.

The improvements in Apple TV production capabilities combined with the release of initially theater-only movies suggests the firm is serious about becoming a key movie and television show producer in Hollywood.

While some time is required to fully understand how much margin can be extracted from this new business segment, the endeavor certainly has the possibility to further increase the diversity in revenue streams present at Apple and offer a new growth opportunity for the firm.

Overall, the last quarter has seen Apple’s robust and wide economic moat remain largely unchanged. While the new MacBook’s and processors were nice to see, I do not believe any additional moatiness can be applied to these categories.

The advances made in the quality and quantity of services provided to consumers by Apple also suggests the firm is well positioned to continue driving revenues within the segment. While the overall moatiness of new endeavors such as theater-release movies are difficult to estimate at present time, the serious move into Hollywood will be interesting to analyze moving forwards.

Financial Situation – Full-Year FY23 Update

The firm’s full-year results for FY23 are a mixed bag which I believe have been misinterpreted by many institutional and retail investors alike.

AAPL FY23 10K

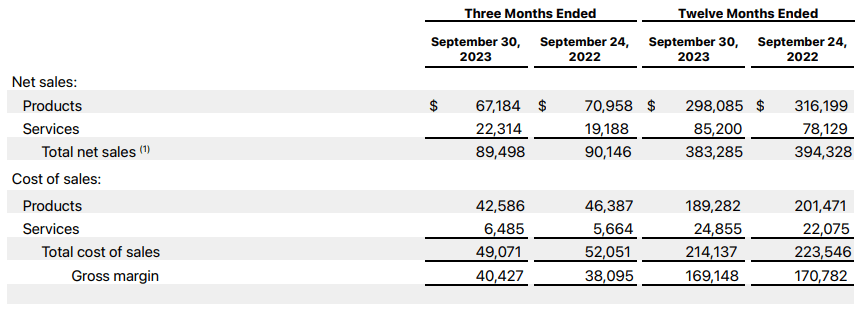

Net sales for FY23 decreased 2.8% YoY due to a significant 5.7% decrease in product (hardware) sales offset slightly by a solid 8.9% increase in services revenues. The soft hardware revenues suggest the increasing fiscal constraint being felt by consumers has taken a real toll on the willingness and ability for consumers to purchase new luxury tech products in 2023.

One must also consider the greater macroeconomic picture which has seen U.S. consumer debt increase massively with current levels now exceeding those witnessed in late 2019. I believe the fundamental effects of tightening monetary policy will only fully be experienced in 2024 and expect Apple’s revenues to continue falling in the new year.

The financing of discretionary consumer spending can only last so long when achieved through lines of credit. The rising rate of credit card delinquencies also suggests real pressure is finally being felt by the bulk of the consumer market. This spells bad news not just for Apple, but for all consumer-oriented businesses alike.

The solid increase in services revenues was in line with previous expectations given the new direction Apple has taken with these software products. The significant focus on providing consumers with an Apple-derived solution to most daily needs and wants appears to be a strategy yielding excellent results for the firm.

While some analysts expect services revenues to plateau in the near future, I do not share this expectation given two key reasons: increased market penetration and the provision of new services.

The market is still rife with competitors to many of Apple’s key services products with the likes of Netflix (NFLX), Disney (DIS), Spotify (SPOT), Nike (NKE), traditional banks and even Hollywood-cinema still rivaling Apple’s own solutions in each respective business environment.

In the long-run, I believe Apple will prevail against competitors in a majority of their business due to the tight integration the firm can achieve with their hardware.

Consolidation within the streaming, fitness, banking and cinema industries is inevitable and to think Apple would be unable to capitalize on such a market environment would be ignoring the firm’s track record of excellent product executions.

AAPL FY23 10K

Another key area misunderstood by the markets arises from Apple’s gross margin. The firm experienced a very slight 1% contraction in their gross margin for the entire FY23 while their Q4 margin expanded YoY by 5.3% despite a drop in revenues.

Fundamentally, I do not believe Apple has managed to increase their gross margin in a tangible manner from a company-wide perspective. The decline in services margins in particular despite an increase in overall revenues suggests the firm has reached at least a temporary plateau in terms of margin expansion from the business segment.

Given the inflationary effects witnessed across global supply chains, it is unrealistic to believe Apple has managed to increase their hardware gross margins substantially. Most likely, a favorable timing of results leading to one-off accounting successes is the culprit for the overall ‘expansion’ in margins witnessed particularly in Q4.

AAPL FY23 10K

This same timing is most likely responsible for the Q4 YoY increase in total operating income and net income. Overall, FY23 was a soft year for Apple with net income falling 2.9% YoY all the while shares have risen in price YTD by more than 46%.

AAPL FY23 10K

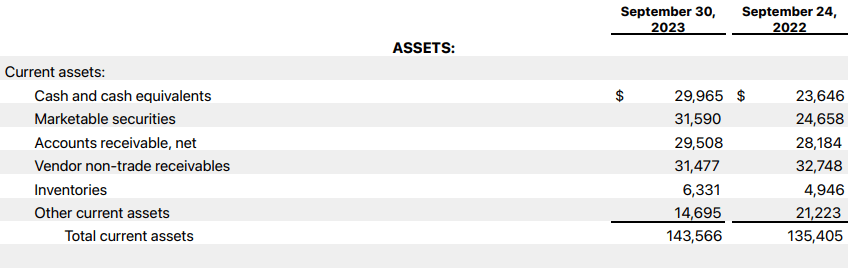

Another key factor present on Apple’s balance sheet continues to raise at the very least a yellow flag indicating faltering consumer demand for the firm’s products. Inventory levels remain 28.6% higher YoY.

While this is down QoQ (which traditionally is the case given the new release of iPhones leading to price cuts on existing models which constitute much of remaining inventory levels), the bearish macroeconomic environment combined with elevated inventories signals a real weakening in consumer demand.

Otherwise, Apple’s balance sheet remains mostly healthy with their current liquidity improving slightly YoY and overall term debt decreasing around 8% YoY. I continue to view Apple’s overall stability from both a short- and long-term perspective as excellent and see no real fiscal liquidity concerns on the horizon for the firm.

Valuation – Full-Year FY 23 Update

Seeking Alpha | AAPL | Valuation

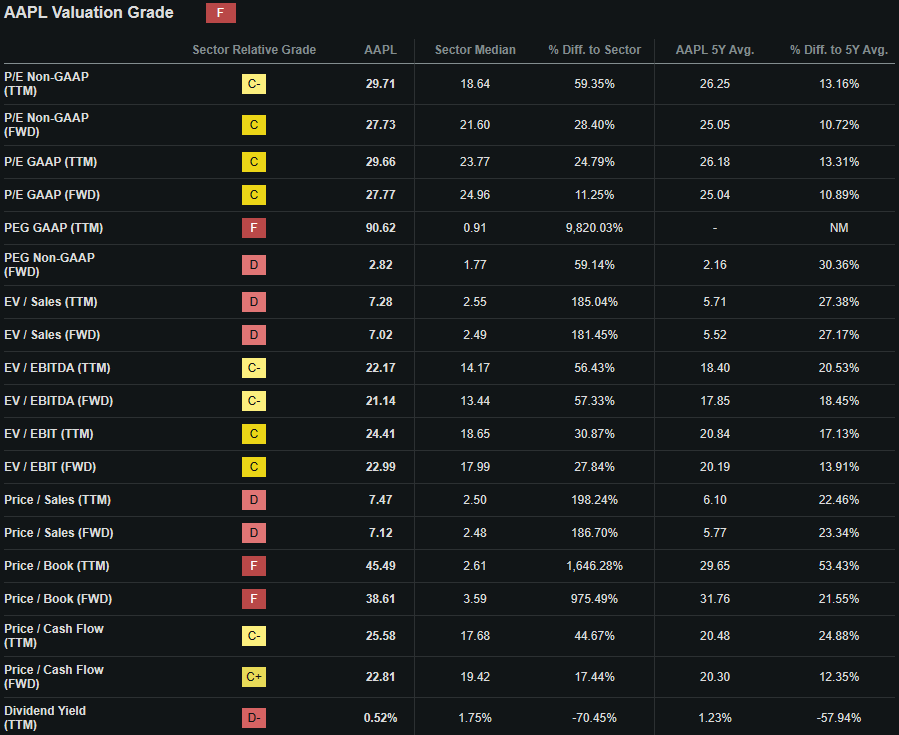

Seeking Alpha’s Quant still assigns Apple with an “F” Valuation rating. I believe this assessment represents a realistic evaluation of Apple’s current market capitalization and earnings potential.

The firm is currently trading at a P/E GAAP FWD ratio of 27.77x and a P/CF TTM ratio of 25.58x. These represent 10.89% and 24.88% increases respectively when compared to their 5Y averages.

When considered against a FWD Price/Book ratio of 38.61x and an EV/Sales FWD of 7.02x (both 21.55% and 27.17% above 5Y averages respectively), it is clear that the from a relative perspective Apple is still severely overvalued in relation to its peers and its own 5Y averages.

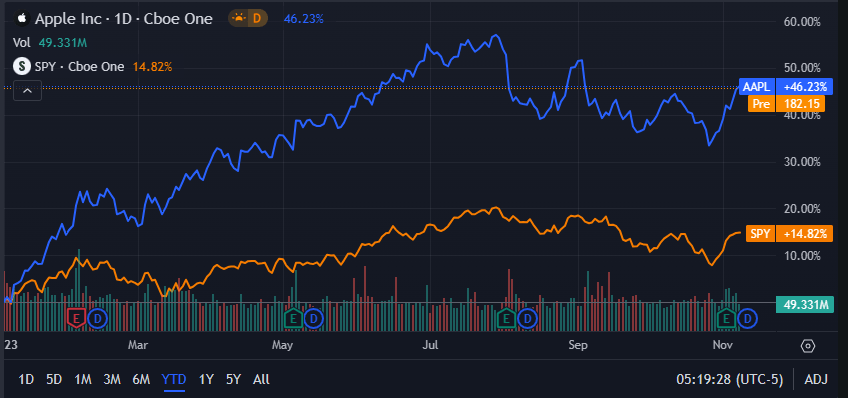

Seeking Alpha | AAPL | Absolute Chart

From an absolute perspective, Apple shares have risen around 46% YTD. This hype-driven bull run has occurred despite the firm’s worst quarterly results in almost 20 years along with a full-year decrease in revenues, margins and profitability.

Despite the firm’s fundamental profitability having decreased, Vision Pro hype, speculation and a “this time it’s different” sentiment has overruled leading to the assigning of new multiples ‘standards’ to the firm.

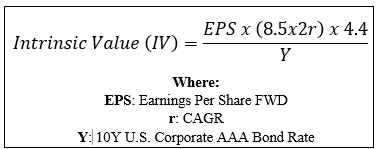

By accomplishing a simple financial valuation based on the calculation below and using Apple’s current share price of $182.89, a revised estimated 2024 EPS of $6.90 a realistic r value of 0.10 (10%) and the current Moody’s Seasoned AAA Corporate Bond Yield of 5.61x, we can derive a base-case IV for Apple of $154.20.

The Value Corner

When using this realistic CAGR value for r, Apple appears to be overvalued by 18.6%. By using a more pessimistic worst-case 2024 growth estimate (which aims to replicate a 2024 recession softening overall hardware sales in particular) CAGR value of 0.08 (8%), shares are valued at around the $133.00-mark, around 35% lower than current prices.

Therefore, I believe Apple is currently trading at a distinct premium relative to both previous valuations and intrinsic value. This represents an downgrade from a previously fairly-valued state according to my calculations.

It must also be considered that Apple has historically been able to command a slight premium for its shares compared to their intrinsic value. Then again, in just December 2022 Apple shares were trading at a 10% discount relative to their fair value.

In the short term (3-10 months) it is difficult to say exactly what the stock will do. While a strong Christmas season could lead to a jump in share prices, I do not believe any fundamental evidence exists to argue an increase in valuations for Apple in the short-term.

Overall, I see significant downward pressure on share in the near-term leading to an overall flatlining in results for the coming year.

In the long term (4-10 years) I fully expect their position as a leader in the industry to become even stronger. Apple does most technology products better than any of their competitors. Their devices are superb to use thanks to a great combination of hardware and software optimization while new services offerings continue to drive Apple’s integration into the daily lives of so many consumers.

While I still believe Apple could be a great long-term investment, the firm currently is overvalued having seen an increase in share prices despite a year characterized by declining revenues, operating margins and profitability.

Risks Facing Apple – Full-Year FY 23 Update

Apple still faces risk from increased competition in the market eroding pricing power along with a few ESG related concerns.

Despite Apple’s massive success with their “M” line of microprocessors, new iPhones and pro-consumer pricing decisions, the firm is not immune to increased competition eroding market share.

In China it has already been witnessed in the smartphone category with recent successes by Huawei and Xiaomi (along with unfavorable foreign relations politics by the state) having eroded some of the popularity of iPhones in the Asian market.

While I still believe Apple has a knack for producing excellent products, it all fundamentally boils down to the people present at the firm. With exits from the silicon department and design department to competing firms in recent years, Apple must ensure their set of engineers, designers and staff remains of the highest quality.

The firm also still faces material ESG risks from all three categories. Environmentally and socially, Apple is still responsible for clear anti-repair tactics that fundamentally undermine the superficial efforts to improve repairability of their devices.

Most of Apple’s improvements in repairability have been driven by changing governance structures which ultimately force the tech giant to comply.

Apple’s reluctance (but ultimate compliance) to transfer to the USB-C standard due to the decrease in proprietary lightning connector royalties and sales illustrates the firm’s continued stubbornness to make meaningful sustainability improvements to their products.

Overall, while I do not see any huge risk arising to Apple from an ESG perspective, some brand damage may occur in the long-term should the firm continue to rebut against sustainability initiatives.

Summary – Full-Year FY 23 Update

Apple continues to be an incredibly profitable, robust and innovative firm. Their market-leading products, excellent services and expansion into new business segments illustrates that the firm is still set on growing substantially moving forwards into the future.

However, FY23 has not been pretty for the firm. While a difficult macroeconomic environment is largely to blame, I believe the real issue arises from the hype-driven increase in valuations witnessed across the fiscal year.

Despite worsening results, investors appear to be incredibly optimistic about Apple’s earnings potential and growth capabilities. While I do believe long-term growth of around 8-10% is achievable, the current headwinds facing the firm are particularly persistent and unlikely to improve in 2024.

While I do believe buying a great company at a good price is better than a good company at a great price, Apple is significantly overvalued probably to the tune of around 20%.

Therefore, I am forced to change my rating to Sell and believe excessive short-term pressure exists over the next year to warrant the huge multiples currently present at Apple.

Given a market with many blue-chip stocks up for grabs at real discounts, I believe better opportunities exist to extract alpha at the present time.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I do not provide or publish investment advice on Seeking Alpha. My articles are opinion pieces only and are not soliciting any content or security. Opinions expressed in my articles are purely my own. Please conduct your own research and analysis before purchasing a security or making investment decisions.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.