Summary:

- Apple Inc. is a high-quality company capable of huge profitability and sustained growth.

- A poor start to 2023 seems to have gone ignored by investors, with dropping net incomes and margins being drowned out by hype and momentum.

- Current valuations leave little to be desired for value-oriented investors. I believe the 20% premium currently present in share prices combined with a recessionary environment spells danger.

- I cannot see any real returns for investors over the next 6-12 months, thus I assign Apple stock a Sell rating.

- At a better price point, Apple is a fantastic investment. At current prices, though, I’d take my winnings and watch the correction from afar.

EKIN KIZILKAYA

Investment Thesis

Apple Inc. (NASDAQ:AAPL) has provided investors with significant returns for a good part of the last decade.

Their ability to maintain a strong operating and net margin even in the most difficult of economic environments highlights just how powerful the company has become in the tech industry.

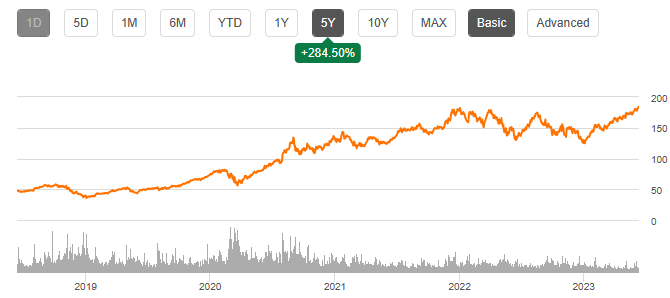

The recent YTD rally of 47% has left Apple’s shares trading at record high valuations of around $183.

While the launch of many new products and services at WWDC (including the company’s Vision Pro AR headset) spurred share prices even higher, the fundamental profitability metrics, revenue growth and macroeconomic conditions fail to support these newfound highs.

I, therefore, rate Apple a Sell due to the more than likely market correction that is about to take place.

Company Background

Apple.com | Homepage

Apple is an American MNC headquartered in Cupertino, California, currently the largest technology company in the world (by revenue). The economic and social influence their brand has generated over the past two decades has resulted in an incredibly loyal consumer base and desirable corporate image.

Most of Apple’s revenue arises from their physical technology sales with primary sales coming from their iPhone lineup, Mac personal computer range or from the host of other technological accessories such as smartwatches the brand pursues. All of Apple’s products occupy the luxury end of personal technological devices.

The company has the highest valuation of any company currently being publicly traded. Their current market cap of around $2.89T is truly incomprehensible and most definitely not supported by intrinsic value calculations.

Economic Moat – Mid Q2 FY23 Update

I conducted a full in-depth analysis of Apple’s economic moat back in February 2023 which I still believe holds validity in today’s market environment, despite some small changes.

For the full in-depth analysis check-out my original article: “Apple: The Right Company At The Wrong Price.”

Nonetheless, I will conduct another quick update here to sum up the company’s core business model along with the changes that have affected Apple’s key moatiness drivers.

Apple hosts an incredibly broad moat when compared to most other personal electronic device manufacturers. The primary drivers for their moat are their incredibly valuable brand image, extensive proprietary product ecosystem and the innovative nature of their products.

The company is the market leader when it comes to luxury personal technology devices. Their ability to combine high-quality physical devices with an outstandingly intuitive user interface has allowed the company to create products which customers aspire to own.

Apple complements these products with a large portfolio of Apple-specific auxiliary services such as Apple Music, Apple TV, Apple Card and now, their ultimate collection package named Apple One. The features these services provide help Apple enhance the eco-system effect of their brand which makes it significantly more difficult (both physically and psychologically) for consumers to switch to competing products.

Apple’s continued focus on increasing switching costs for consumers by providing more Apple exclusive services seems to be working.

Some weakness seems to be brewing in Apple’s hardware sales with reported sales of their core revenue drivers slowing. Both iPhone, iPad and Mac sales have taken a hit in 2023 with these slowing sales figures expected to negatively impact Apple’s overall 2023 results.

Mac sales have been particularly hard hit, with shipments having fallen over 40.5% in Q1 of 2023.

Apple.com | Vision Pro

WWDC 2023 may have been one of the most influential Apple events we have seen in a long time, as the presentation included the launch of an entirely new computing solution: the Apple Vision Pro.

Vision Pro is an augmented reality computing headset designed to replace a user’s computer, monitor, TV, cinema setup and more. The concept of “spatial computing” and using one’s eyes, hands and voice to control a computer is a truly unique and while not new idea, Apple seems to be nailing the execution of it.

Apple.com | Vision Pro

While this device is no-doubt revolutionary and has the potential to completely change the way in which we interact with computational technology, defining what degree of moatiness this brings the company is difficult.

On the one-hand, Vision Pro could be viewed as a hugely influential device which will ultimately shape the way in which we use computers. While I believe Vision Pro is undoubtedly going to spur a multitude of competitors to enter the space, from an investor perspective it is most important to try and understand what value this generates for the company.

For the first 3-4 years of Vision Pro, I fully expect demand to significantly outstrip Apple’s proposed supply levels, even at the hefty $3,499 price tag. This means Apple should quite certainly be able to create some tangible returns on the headset in the short term.

Thereafter, it is difficult to forecast what impact the headset will have on Apple’s profitability and economic moat.

I consider Vision Pro to be a hype-generating asset which in and of itself could help spur short-term sales of other Apple products. Vision Pro could also entice many new customers into the Apple Ecosystem which also could yield and increase in sales.

Therefore, I assign the Vision Pro a medium economic moatiness level thanks to the high price-tag Apple will be able to command for the product and the revolutionary nature of the product.

When considering the company as a whole, it is clear Apple still possesses an unrivalled brand image which permits the firm to charge consumers significant premiums for their products. The company is also laser-focused on creating high-quality products which provide consumers with superior user-experience both through ecosystem benefits and through excellent hardware.

However, while their software solutions continue to drive an increased economic moat for the firm, the weaker than expected hardware sales results suggest the company is not as immune to global economic trends as many investors expected.

I still rate Apple as having a very wide economic moat which provides the company a tangible competitive advantage for at least the next 10 years.

Financial Situation – Q2 FY23 Update

Apple has been a hugely profitable firm for the greater part of the last two decades. Their consistent EBITDA margins of 33% combined with a 5Y average ROIC of 34% is incredibly impressive.

Their strong pricing power has allowed the company to generate 10Y average gross margins of almost 40% with an average net margin for the same time period of 20%.

Apple FY23 Q2 Press Release

FY23 Q2 results were a little less impressive than Apple’s press release might suggest. They illustrate an undercurrent of lack lustered performance brewing at the company.

Total net sales for Q2 were down 3% YoY with quarterly revenue also falling 3% compared to FY22. This relatively poor performance is most likely due to inflation finally beginning to place a pinch on consumers’ pockets.

The luxury nature of Apple’s products means that consumer spending on these goods during a recession or highly inflationary period will drop first due to the non-essential quality of their devices.

Gross margins contracted 1.7% YoY primarily as a result of the decrease in product sales. COGS as a % of total revenue remained the same for Apple’s hardware products segment.

Apple FY23 Q2 Press Release

While iPhone sales saw a new revenue record in the March quarter, the strength in their mobile phone division was unable to support the overall poor sales of other devices.

Mac sales fell 31% YoY with iPad and wearables, Home and Accessories segments also seeing single digit drops. Even net iPhone sales for H1 FY23 were down 4%.

Interestingly, Apple’s services segment saw healthy growth in Q2 with net sales increasing 5.6% YoY. COGS for the segment as a % of revenue increased 2% totaling 29% compared to FY22 Q2’s COGS/Services Sales ratio of 27%.

I believe this continued growth in services revenues and profits illustrates the more sticky nature of these goods. Given the high switching costs and potential for FOMO compared to their peers, consumers are less willing to sacrifice cancelling a service when compared to not purchasing a new iPhone or Mac.

Total operating expenses increased 8.7% YoY in Q2 due to a significant increase in research and development costs. This was most likely due to the significant investment required to make the Vision Pro demo units for certain influential individuals to test as rumors suggested the devices were in a rough state leading up to WWDC.

R&D into the new A17 bionic and M3 chips is also undoubtedly responsible for increasing these figures as Apple prepares to launch their new range of 3nm chips.

Overall, net income for Q2 dropped 3.6% YoY which while not surprising, suggests even Apple is not immune to the difficult and persisting inflationary environment currently impacting economies across the globe.

Seeking Alpha | AAPL | Earnings

While Apple’s EPS of $1.52 in Q2 FY23 beat expectations by $0.09, with revenue surprise generating a $2.0B beat, the overall tone of Q2 FY23 was one of weaker than desired performance.

While Apple remains an incredibly cash-rich and stable company from a balance sheet perspective, (with cash and cash equivalents increasing by $1B YoY), it is worth noting that their accounts receivables have dropped by a whopping $11B.

This suggests Apple’s future revenues may be set to drop even further with weaker demand resulting in further decreased net sales.

I believe Apple’s managements authorization of $90 billion worth of share repurchases illustrates an over-optimistic attitude which is aimed at soothing any souring sentiment among investors. While in the long-term this will have little consequence for the company, this act could illustrate a slightly bombastic attitude at a financial management level.

I have conducted a more detailed financial analysis in my original article. Nonetheless, the truth remains that Apple continues to be a highly profitable company. Their profit generating abilities in the long-term still seem solid, although FY23 may prove difficult due to the significant macroeconomic headwinds in the form of an expected recession on the horizon.

Such an economic slowdown will undoubtedly hurt Apple’s margins and sales figures as consumers have less to spend on luxury goods. Therefore, I take a more bearish view of the short-term future for Apple from an earnings perspective.

I expected H2 results to be weaker than anticipated.

Still, I don’t believe investors are going to be hurt much by Apple’s profitability in the future thanks to their robust economic moat and strong business model. The key issue currently facing shareholders is their excessive valuation.

Valuation

Seeking Alpha | AAPL | Valuation

Seeking Alpha’s Quant has assigned Apple with an F Valuation rating. Unfortunately, I believe this assessment represents a fair evaluation of Apple’s current share price when considered against traditional valuation metrics.

Apple’s valuation stinks.

The firm is currently trading at a P/E GAAP FWD ratio of 30.69x and a P/CF TTM ratio of 26.38x. When considered against a FWD Price/Book ratio of 48.37x and an EV/Sales FWD of 7.36x, it is clear that the current share price represents a significant intrinsic overvaluation of the firm.

Seeking Alpha | AAPL | Summary Chart

From an absolute perspective, Apple shares have risen 47% since January 2023. This has occurred on the heels of Apple’s worst Q1 quarterly fiscal report since 2020 along with a relatively weak Q2 report too.

When considering that these valuations have been reached following poor economic performance, it is difficult to attribute this huge rally to anything but hype and momentum.

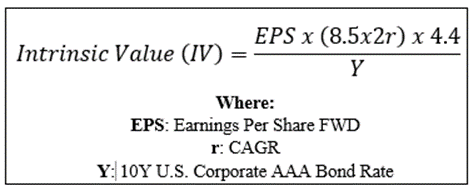

By accomplishing a simple financial valuation based on the calculation below and using the estimated 2023 EPS of $5.97 a realistic r value of 0.09 (9%) and the current Moody’s Seasoned AAA Corporate Bond Yield, we can derive a base-case IV for Apple of $155.00.

The Value Corner

When using this realistic CAGR value for r, Apple appears to be overvalued by around 18%. By using a more pessimistic worst-case 2023 growth estimate CAGR value of 0.07 (7%), share are valued at around the $132.00 mark, 38% lower than currently.

Therefore, I believe Apple is currently moderately overvalued. Both its absolute comparison to historic share prices combined with an intrinsic value calculation suggest the company’s shares are trading at a tangible premium to their real value.

In the short term (3-10 months) it is difficult to say exactly what the stock will do. I believe share prices will fall significantly as the market corrects for the huge overvaluation currently present.

Thereafter, much depends on the prevailing macroeconomic conditions and the severity of the recession now forecast for H2 2023. Given the over 80% chance for a recession to occur combined with the increasing realization that fed rate-hikes will most likely continue, the short-term looks bleak for Apple.

In the long term (2-4 years) I fully expect their position as a leader in the industry to become even stronger. Their unique product offerings combined with the undoubtable branding power places little doubt in my mind over the almost undoubtable returns the company should be able to provide to shareholders.

Therefore, it is almost impossible to argue that the current share price would leave any tangible room for value investors to become involved with the stock. While the firm has supported a historic overvaluation, the risk associated with investing in a company which fails to exhibit any real undervaluation is significant.

Risks Facing Apple – Q2 FY23 Update

Apple still faces the same risks of increased competition within the market, failed execution of products along with the negative social sentiment arising from anti-repair tactics. However, the company also faces the very real short-term risk of falling consumer discretionary income.

If consumers have less to spend on luxury goods, Apple’s core revenue driving product categories such as the iPhone, iPad and Mac lineups will see declining sales and popularity. This could definitely hurt FY23 results thus potentially leading to a pronounced market correction in the firm’s share prices.

This very real threat should not be underestimated given how hard it is to predict how markets will react to certain events. While the impacts of the U.S. banking crisis seem to have been relatively mute in wider equities markets, the underlying market fundamentals suggest a recession is very likely in 2023.

Summary

Apple Inc. has had an incredibly impressive history from an investor standpoint. Their robust, premium business model, excellent operational efficiency and iconic brand reputation have allowed the company to become a true profit generation powerhouse. There really is a reason the firm boasts the highest valuation of any company in the world.

Unfortunately, the huge YTD rally has left shares trading at a fundamentally irrational price point with little room for further growth. Both absolute and intrinsic valuation methods suggest shares are materially overvalued thus making building a position from any form of value perspective impossible.

Even from a growth point of view, little room and probability exists for Apple to achieve any tangible success in 2023 due to the significantly unfavorable macroeconomic conditions.

While Apple has had a history of trading a relative premium to its intrinsic value, current prices are truly exaggerated and remain unsupported by any fundamentals at the firm.

As a short-term investment, I believe there is too much volatility particularly exposing investors to downside potential. This has been amplified by the hype surrounding the Vision Pro headset.

However, in the long-term, I still fully believe their undeniable position as a market leader places Apple firmly in position to generate great shareholder value. At a better price, or even fair valuation, one could undoubtedly argue building a position in the tech giant.

The huge overvaluation combined with lack lustered 2023 performance warrants a downgrade of my rating to Sell.

While long-term value generation has not been compromised, short-term headwinds are too great to justify building a position in Apple Inc. stock.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I do not provide or publish investment advice on Seeking Alpha. My articles are opinion pieces only and are not soliciting any content or security. Opinions expressed in my articles are purely my own. Please conduct your own research and analysis before purchasing a security or making investment decisions.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.