Summary:

- Apple’s stock slips from the $3 trillion market cap milestone after reporting a third consecutive quarter of sales declines.

- Demand challenges due to macroeconomic uncertainties and FX headwinds continue to be a prominent downside.

- This is likely overshadowing consistent margin expansion buoyed by resilient services sales.

Shahid Jamil

The macroeconomic drag is finally catching up on investors’ sentiment over Apple Inc. (NASDAQ:AAPL), with its stock slipping from the $3 trillion market cap milestone after the company reported its third consecutive quarter of sales declines. The persistently tepid results – a first in two decades – highlight a combination of demand challenges due to macroeconomic uncertainties, as well as FX headwinds as the stronger dollar weighs on the majority of Apple’s sales made overseas.

Despite impressive profit margins, helped primarily by robust acceleration in the services segment during the June quarter, markets are adjusting their appetite to the stock’s high-flying valuation premium as its underlying business’ fundamentals continue to struggle amid a mixed macroeconomic climate. Investors’ focus has largely shifted away from the earlier hype on the Vision Pro’s launch and towards core fundamentals, highlighting market’s demand for tangible themes that would be supportive of the stock’s near-term prospects.

The company reported $81.8 billion in F3Q23 revenue, slightly outperforming consensus estimates. Although a decline, management has reiterated that the quarter’s sales would have been a positive uptick if it were not for FX headwinds. Much of the June quarter’s strength was driven by record-setting services sales, while the demand environment for products stayed tepid. This was largely in line with observations across industry peers, such as Apple’s key supplier QUALCOMM Incorporated, which reported a “steep drop in orders from handset manufacturers, [due to] more inventory than they needed” during the June quarter, suggesting little confidence in recovery hopes through the remainder of calendar 2023.

Despite better than expected results during the June quarter, with modest growth on a constant currency basis and trend-defying expansion in emerging markets – particularly in Greater China – alongside gradual gross profit margin expansion, the stock’s latest post-earnings pullback underscore weakened confidence in the durability of Apple’s valuation premium over the near-term, as little visibility remains on when consumer softness might recover. However, we remain optimistic on resilience observed in services sales, which underscore the competitive advantage of Apple’s massive devices installed base, and effectiveness in optimizing the monetization of which. The higher margin sales are expected to remain a key compensating factor for ongoing macroeconomic headwinds weighing on broader industry consumption trends and, inadvertently, topline expansion.

Looking ahead, growth is likely to stay tepid for the remainder of calendar 2023, as optimism over seasonality demand trends could potentially get offset by a persistently cautious spending environment in the core U.S. market, which management has held a conservative outlook for:

If you look at the U.S., which is in the — obviously in the Americas segment, it is the vast majority of what’s in there, there was also a slight acceleration sequentially, although the Americas is still declining somewhat year-over-year, as you can see on the data sheet. The primary reason for that is that it’s a challenging smartphone market in the U.S. currently.

But durable margin expansion, helped by a favourably mix shift to higher profit services sales alongside broader cost management efforts could continue to bolster the cash-affluent narrative supporting the stock’s prospects. This is likely to address investors’ demand for an all-weather investment pick with a consistent capital return program, especially given the stock’s latest pullback from its historical highs. There is also early optimism that sales have troughed in the first half of calendar 2023, with the latest pullback in the stock potentially benefitting from stronger seasonality sales trends headed into FY 2024, as well as growing risk-on sentiment for big tech ensuing from an aggressive rate hike cycle that is likely nearing an end based on recent improvements observed in economic data.

The Mission-Critical Function of Services

Despite record-setting services sales, and an ensuing positive impact on Apple’s profitability, the post-earnings stock decline highlights an inevitable shift in investors’ focus on a waning demand environment for devices sales.

While iPhone sales in the June quarter have largely defied an extended slump in smartphone shipments worldwide – particularly in Greater China, despite persistent contraction of related product sales in the region – the weak demand environment back home in the U.S. remains an overhang on Apple’s core revenue driver. Specifically, iPhone sales declined by 2% y/y during the June quarter (or up slightly on a constant currency basis), despite robust sales across emerging markets – particularly in China, which recovered from a decline in the March quarter to an increase of 8% in the June quarter – and Europe, highlighting acute headwinds in Apple’s core U.S. smartphone market demand environment. Meanwhile, there is also risks to the durability of improvements in the Chinese market demand environment, given the recent slew of economic data that shows further deterioration in bank loans, exports, and consumer and producer prices last month.

Although Apple has observed a record number of switchers to the iPhone during the June quarter, highlighting resilient demand from more affluent end users even in emerging markets, upgrades from the existing installed base is likely to remain modest due to the uncertain U.S. spending environment, adding to the importance of strong engagement via services sales instead to maintain a higher average selling price in the near-term. While switchers represent a “huge opportunity” for Apple, the average lifetime revenue generated from related sales – whether it is from upgrades or expansion of services subscriptions and engagement – will take longer to ramp up, providing little respite to near-term iPhone sales growth relative to upgrades. This is in line with management’s conservatism for the iPhone segment’s near-term performance – particularly on upgrades – despite guidance for sequential acceleration in the September quarter, potentially driven by an anticipated boost from the upcoming iPhone 15 introduction that is expected to sell at levels consistent with the prior year.

In terms of the upgrade cycle and so forth, it’s very difficult to estimate real time what is going on with the upgrade cycle. I would say, if you think about the iPhone results year-over-year, you have to think about the SE announcement in the year ago quarter, the iPhone SE announcement in the year ago quarter. And so that provides a bit of a headwind on the comp.

Source: Apple F3Q23 Earnings Call Transcript

Meanwhile, the latest earnings results also suggest any potential for a recovery in Mac and iPad sales during the second half of calendar 2023 is becoming further out of reach. Both Mac and iPad sales continue to drop on a sequential and y/y basis, with the latest introduction of the 15″ MacBook Air doing little to arrest a sales slump for Apple silicon fitted PCs. And the near-term outlook on related sales is expected to be further exacerbated by a tough PY comp where F4Q22 had benefitted from pent-up demand due to factory shutdowns in the preceding quarter. Management’s cautious outlook for its PC and tablet segments also corroborates industry expectations that any cyclical recovery tailwinds implied by recently improved data on PC shipments will likely benefit upstream components first across the product supply chain, before meaningfully impacting downstream sell-through rates to end-users.

Taken together, Apple’s latest earnings report continues to highlight the mission critical role of its services segment, as the tech giant looks to better monetize its expansive devices installed base that is now exceeding 2 billion. Services sales has reaccelerated towards the high single-digit range during the June quarter, with management guiding a greater increase exiting fiscal 2023. Although the segment’s pace of growth remains a far cry from the robust double-digits observed prior to the pandemic and recent macroeconomic deterioration, the high-margin revenue stream is complementing the gradual growth in Apple’s active devices installed base, nonetheless. With paid subscriptions now surpassing 1 billion, and Apple’s continued commitment to “improving the breadth and the quality of [its] current services”, the segment’s record-setting quarterly sales underscore robust engagement from customers across the company’s broader ecosystem, which reinforces the durability of high-margin monetization opportunities in ongoing devices sales.

Looking ahead, continued strength in high-margin services sales will be a key compensating factor for both macroeconomic and maturation headwinds on devices sales, which can be corroborated by consistent margin expansion observed in the three quarters through June, despite persistent top-line declines over the same period. Although the stock’s recent pullback potentially implies penalization on Apple’s struggles against a mixed demand environment, we think resilient margin expansion – driven not only by internal cost optimization efforts, but also durability in the growth of recurring, more profitable services revenue- is a plus that is being overlooked. Specifically, continued expansion of higher margin services revenue will be key to bolstering cash generation at Apple – a key consideration to its bullish narrative – and underpin the durability of the stock’s longer-term upside potential by optimizing value realization on the company’s expansive market share in consumer mobile and computing devices.

Fundamental Considerations

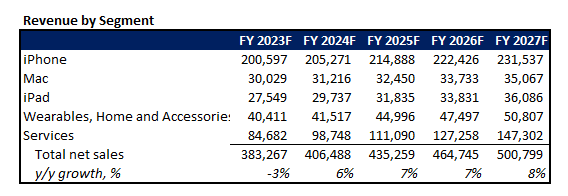

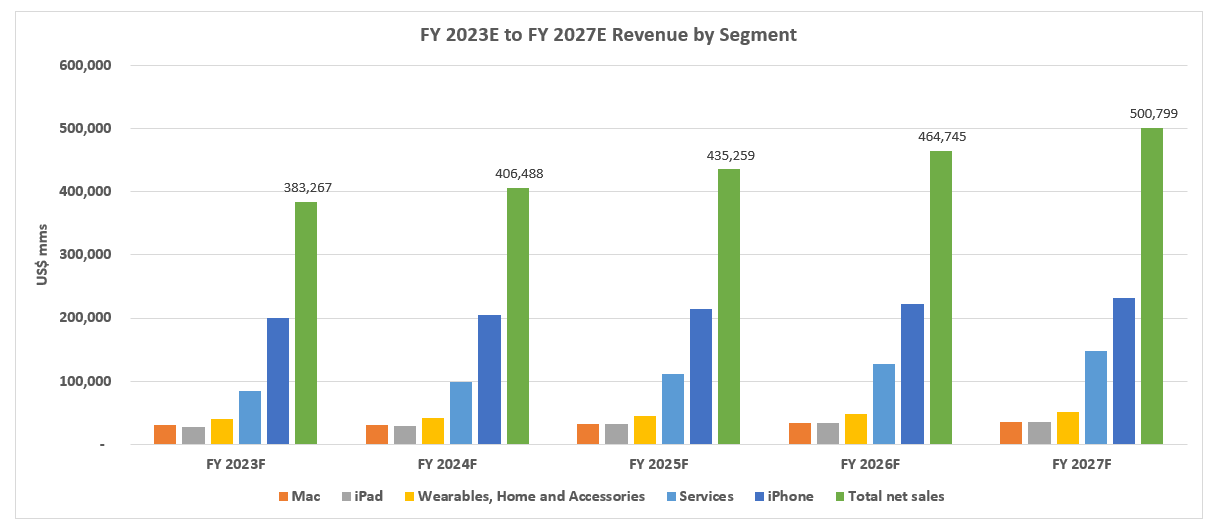

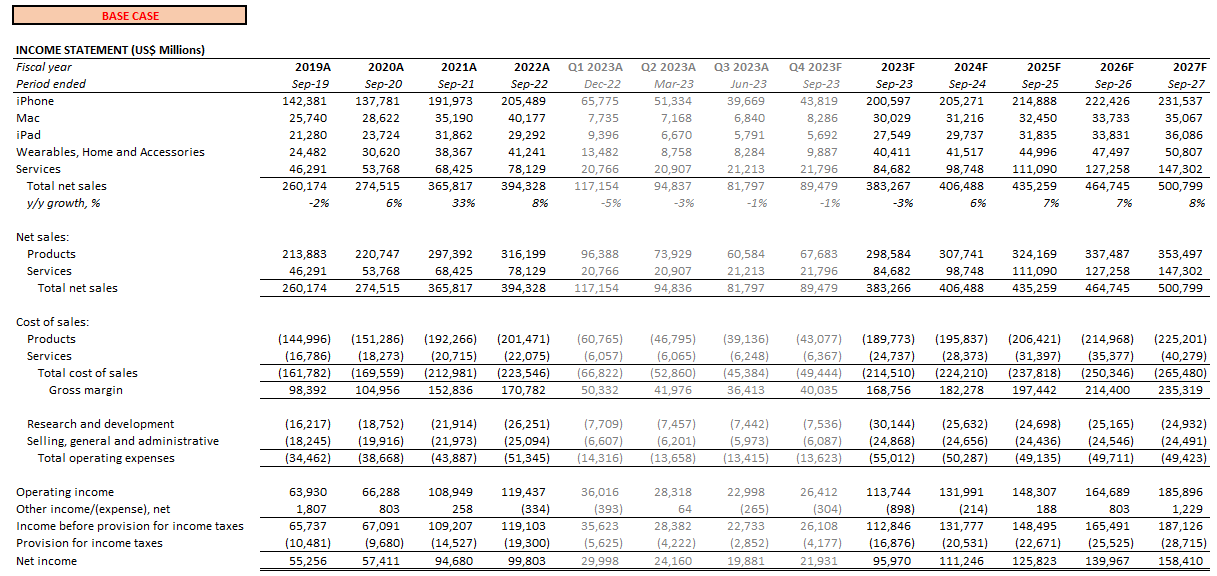

Taking into consideration Apple’s June quarter results, as well as management’s outlook on near-term demand trends for the company’s products and services offered, full fiscal year 2023 revenue is expected to finish at a 3% decline. This should not come as a surprise considering management’s transparent and conservative outlook on its near-term demand environment given the mixed macroeconomic backdrop across its core operating regions. And over the longer-term we expect consolidated sales growth to recover towards the high single-digit percentage range, driven primarily by acceleration in services sales as monetization expands on Apple’s existing – yet still gradually expanding, though at a modest pace – active devices installed base.

Author Author

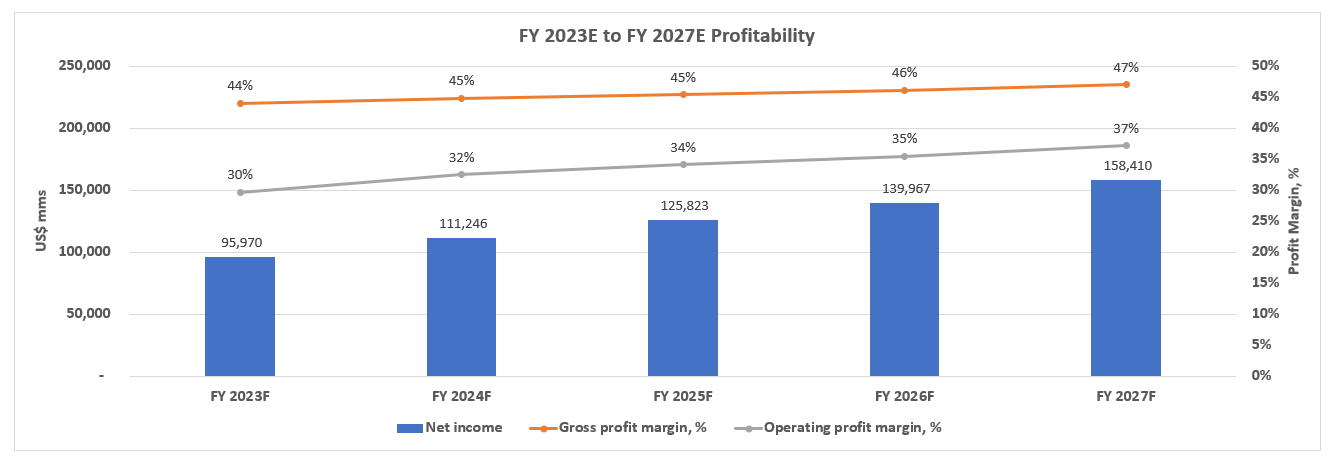

This will inadvertently translate to greater durability in the pace of profit margin expansion observed at Apple in recent quarters, benefiting from a favourable sales mix in addition to cost reduction efforts implemented across every industry over the past year.

Author Author Author

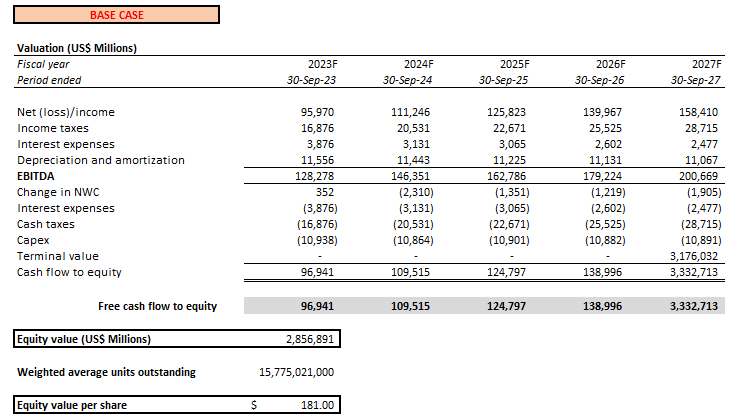

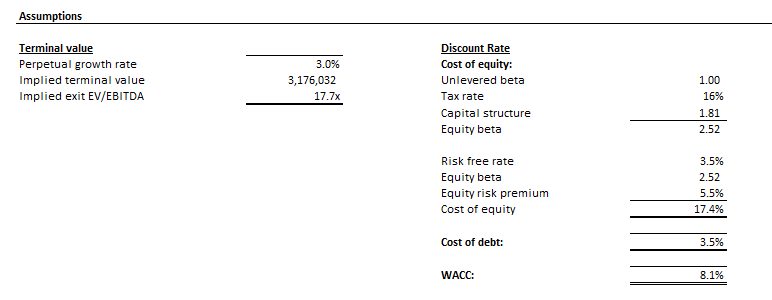

Apple Forecasted Financial Information

Valuation Analysis

Author

And from a valuation perspective, we expect consistent margin expansion, paired with a potential return to growth across all segments headed into fiscal 2024 will be value accretive for the stock. But near-term expectations for a mixed demand environment – especially with lingering weakness in Mac and iPad sales – could continue to overshadow the durability of Apple’s profit prospects, representing an overhanging multiple compression risk for the stock. This could lead to range-bound trading in the stock through calendar 2023, as investors balance between aversion to the low level of visibility into Apple’s near-term growth outlook given the uncertain macroeconomic backdrop, and liking for its growing cash pile that will continue to sustain a stable capital return program and future growth investments.

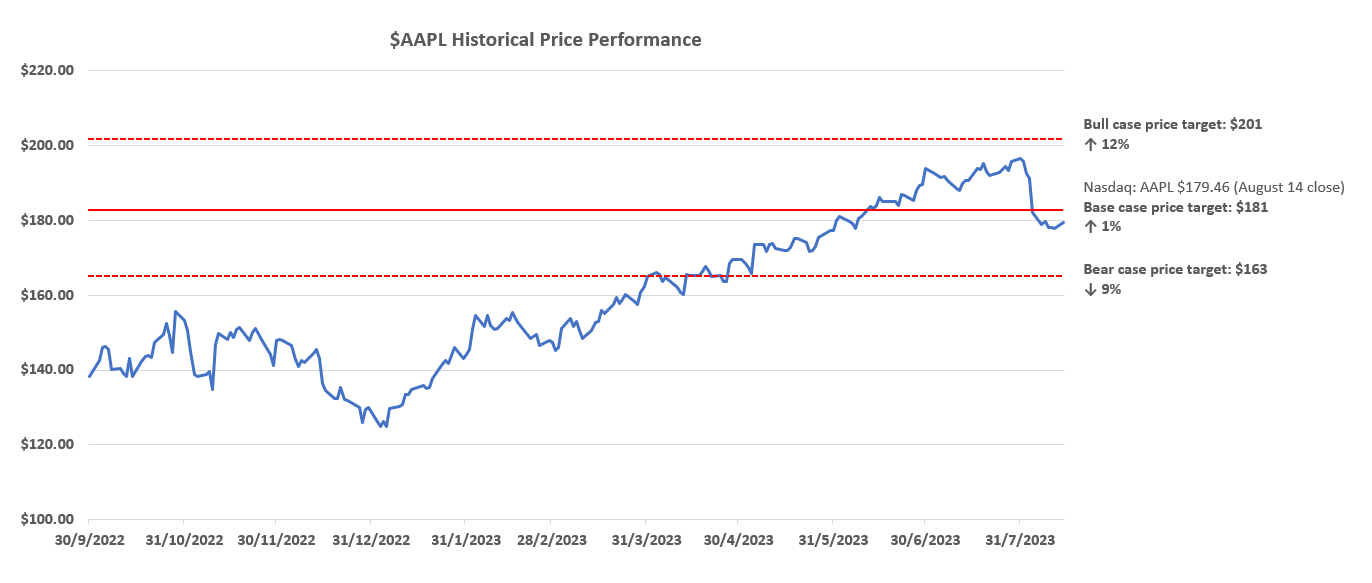

Drawing on projected cash flows in conjunction with our updated base case fundamental forecast for Apple, the stock’s current price at $179 apiece represents an estimated terminal value multiple of about 17.5x, in line with observations across its megacap tech peers and our base case PT of $181.

Author Author

But the upside case is not completely out of reach for Apple. In addition to its annual introduction of the new iPhone in September, which has typically been a boon for the stock and quarterly sales, Apple’s valuation could also benefit from a shift in investors’ preference for durable profitability over growth amid the volatile market climate, blighted by lingering macroeconomic uncertainties. Increasing market optimism that inflation might finally be trending towards the Fed’s target range without having to tighten the economy into recession based on recent economic data is also driving up hopes that the most aggressive pace of rate hikes in four decades might finally be coming to an end. Although it is still too early to anticipate for rate cuts in the near-term, a declared end to the latest round of monetary policy tightening expected for calendar 2024 could improve visibility on the broader macroeconomic outlook, potentially lifting a significant multiple compression risk that has been most penalizing on tech stocks whose valuations are underpinned by future cash flows.

Likewise, worse than expected performance in Mac and iPad sales could drive a downside scenario where consolidated revenue falls into a steeper decline. Despite historical seasonality on sequential Mac and iPad sales growth during the fiscal fourth quarter, driven primarily by back-to-school demand, recently observed declines which have been persistent even with the introduction of new products to the line-up underscore risks of a steeper than expected macroeconomic drag on the consumer. The restart of student loan repayments coming October is expected to further exacerbate the lack of visibility on American consumer strength headed into the second half of calendar 2023, potentially weighing further on Apple’s struggles in restoring demand for its products in its core operating region. Recent research shows that the resumption of student loan repayments could potentially diminish monthly disposable income by as much as $9 billion on a monthly basis, or $100 billion on an annualized basis. Meanwhile, more than half of student loan borrowers have expressed a need to “choose between making their loan payment or covering necessities, like rent and groceries” when the pandemic-era moratorium ends, highlighting incremental risks to back-to-school demand this time around.

The Bottom Line

Despite expectations for near-term volatility in the stock, driven primarily by a mixed demand environment ahead of persistent macroeconomic headwinds, Apple’s robust check-book for facilitating innovative growth investments, fuelled by consideration of even just monetization opportunities on its sizable devices installed base, remains a tangible cornerstone to longer-term upside potential. We expect investors’ focus to remain on the durability of Apple’s margin expansion efforts, as well as resilience in iPhone and services sales critical to the company’s bottom line. This is expected to create pent up value in the stock that will likely become realizable when broader cyclical tailwinds are restored and all core operating segments – including Mac and iPad – return to growth.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Thank you for reading my analysis. If you are interested in interacting with me directly in chat, more research content and tools designed for growth investing, and joining a community of like-minded investors, please take a moment to review my Marketplace service Livy Investment Research. Our service’s key offerings include:

- A subscription to our weekly tech and market news recap

- Full access to our portfolio of research coverage and complementary editing-enabled financial models

- A compilation of growth-focused industry primers and peer comps

Feel free to check it out risk-free through the two-week free trial. I hope to see you there!