Summary:

- Apple shares have underperformed the large-cap tech space since 2023, and analyst revenue estimates are their lowest in a number of years.

- Shares trade at a more than 10% premium to its big cap tech peers when looking at calendar 2025 street expected earnings per share.

- Apple will need to rely on significant product upgrades to drive decent revenue growth in 2025.

David Paul Morris/Getty Images News

With a little under three weeks to go in 2024, shares of technology giant Apple (NASDAQ:AAPL) are up a little less than 29% on the year. While that certainly is a nice gain, it’s a little more than a percentage point behind the gain we’ve seen in the Invesco QQQ Trust ETF (QQQ). Should Apple end up losing the battle to the QQQ for 2024, it would be the second straight year that the stock underperformed the bellwether large cap tech ETF. While Apple shares might be at an all-time high thanks to a surging market, business expectations are far from it, meaning there’s a lot for the company to prove in 2025.

Previous coverage of the stock:

I last covered Apple shares in early November, a little bit after the company reported its fiscal Q4 results. The September ending period showed top and bottom-line beats, but Services segment revenue and China revenues lagged street estimates. Management issued somewhat weak guidance for the current quarter, fiscal Q1 2025 that ends later this month, which I said would reduce expectations a little moving forward.

Since my previous article, Apple shares have rallied about 12%, which is roughly double the return of the S&P 500. A lot of optimism has come thanks to former President Trump being re-elected, which could result in tax cuts for large corporations and a more pro-business legislature. As the Federal Reserve also looks to be cutting rates again at its upcoming meeting, investors have sent US stocks to new heights in recent weeks.

Analyst estimates have been heading lower:

Going into this year’s iPhone launch, a number of estimates were calling for the iPhone 16 to see a sales super cycle. This was based on the notion that Apple would have numerous Artificial Intelligence (“AI”) features in the latest phone, sparking tremendous interest in upgrades from consumers. However, it turned out that those AI features weren’t going to hit the market around the globe right away, which curtailed super cycle enthusiasm quite a bit.

When management gave that weak guidance for the all important holiday quarter, analysts had no choice but to trim their estimates. As it turns out, AI features have not yet started to drive major consumer demand, with low-end phones reportedly being the ones showing the best growth currently. Since the fiscal Q4 report, the average street revenue estimate for fiscal Q1 has gone from $127.59 billion, or 6.70% year-over-year growth, to $124.34 billion, or just under 4.00% growth. You can check all current estimates right here.

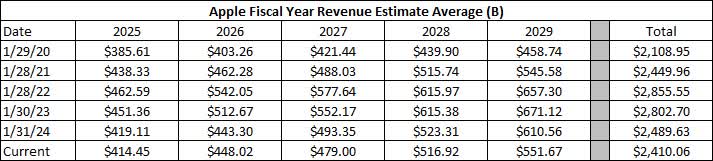

It’s not just short-term estimates that are coming down for Apple, however. As you will see in the table below, the street has been handily reducing its 5-year estimates for the company for a couple of years now. The company has cancelled its plan to launch an electric car, and it was reported last month that lackluster sales of its Vision Pro headset have led to dramatic production cuts. As a reminder, Apple’s fiscal year ends at the end of September.

Apple Revenue Estimates (Seeking Alpha)

Should street estimates for this 5-year period finish next month when they are currently, or even very slightly above, the cumulative total would be at its lowest end of January point since Covid started back in 2020. Like many other companies out there, falling revenue estimates haven’t hurt the stock, however. Even though the above cumulative revenue estimate is down about $40 billion from 1/28/21, the stock’s dividend adjusted close on that day according to Yahoo! Finance was $134.05. Shares now trade for almost $250.

What’s next for Apple:

For 2025, investors will be waiting to see how much Apple Intelligence can actually drive product sales. A big part of this could be in relation to the company’s lowest priced versions of its key products. In the spring, current expectations call for a new iPhone SE to be launched. This has been the most affordable iPhone out there for years, although getting a much larger screen and by going three years between updates, the price point might be a bit higher than its prior generation counterpart.

In a similar respect, Apple did not launch a new version of its entry-level iPad in 2024, so expectations are for a spring 2025 update for the tablet. We could also see a new iPad Air at that time, although it is unclear if one or both of these new tablet models would get Apple Intelligence features right away or later in the year. New iPad Pro models are not expected until the second half of calendar 2025.

Since we are still about nine months away from the projected annual Apple iPhone event in September 2025, the rumors right now are all over the place. It does appear that the iPhone Plus will be axed in favor of a new thinner model, which could get the name iPhone Air. That device could have a smaller screen size than the Plus, but still larger than the base iPhone, that is expected to get a display size increase. It appears that we may see more phone hardware updates than a normal year, with the main attraction being some big upgrades coming to the camera setups.

Given the expected launch of the iPhone SE next year, it wouldn’t surprise me if the main iPhone lineup sees somewhat of a pricing increase. The main and Plus versions have started at the same price three years in a row in the US. A boost in storage to 256 GB for the base versions along with some decent hardware upgrades could push prices up $50 to $100, with perhaps a 1 TB version being offered as well. This would provide more separation between the iPhone SE and the main versions, while Apple could also boost Pro model pricing given the extra features that those models usually get.

Valuation remains a bit stretched:

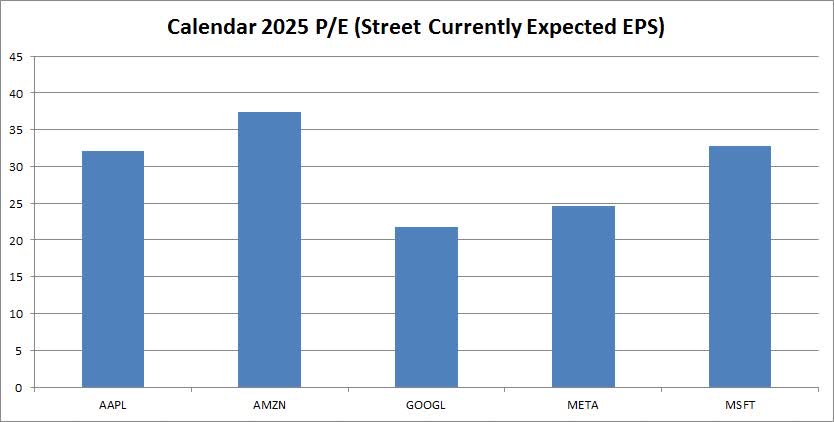

When looking at price to earnings, Apple shares are a bit more expensive than some of its large cap technology counterparts, as the chart below shows. As of Wednesday’s close, Apple traded at a little more than 32.1 times its calendar 2025 street expected earnings. That’s a 10% plus premium to the average of Amazon (AMZN), Alphabet (GOOG) (GOOGL), Microsoft (MSFT), and Meta Platforms (META). But while you are paying a premium to the average here, don’t forget that Apple is projected for the least amount of revenue and earnings growth among these names in 2025.

Big Tech Valuations (Seeking Alpha)

On the flip side, things have changed quite a bit when it comes to the analyst community. At my last article, Apple shares were trading about $20 below the average street price target. However, the recent rally in shares combined with limited valuation hikes now has the stock a couple of dollars above the average target for the first time in about five months. With Apple shares having spent most of the past three years trading below their average target, that history suggests that now is not the best time to be buying the stock.

Final thoughts and recommendation:

With Apple shares having underperformed the large cap tech sector since the start of 2023, the company has a bit to prove next year. It appears that the iPhone super cycle driven by AI demand isn’t quite yet happening, resulting in analyst revenue estimates dropping to their lowest point since a little after the pandemic started. With the electric car plan shelved and Vision Pro headset sales reportedly floundering, the company will need to rely on meaningful upgrades of its current products to really move the revenue needle.

I still like the long-term story here, with some growth and a huge capital return plan, but the valuation is a bit high for my liking at the moment. Expectations coming down certainly helps if you want to see future revenue and earnings beats, but it also means that things aren’t going as well as previously hoped. I’m going to maintain my hold rating on the stock until we get some more data points to see whether Apple AI is really starting to drive sales or not. For now, it just seems like the stock will trend with the overall market, meaning if you are looking for significant outperformance, you probably want to be elsewhere.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.