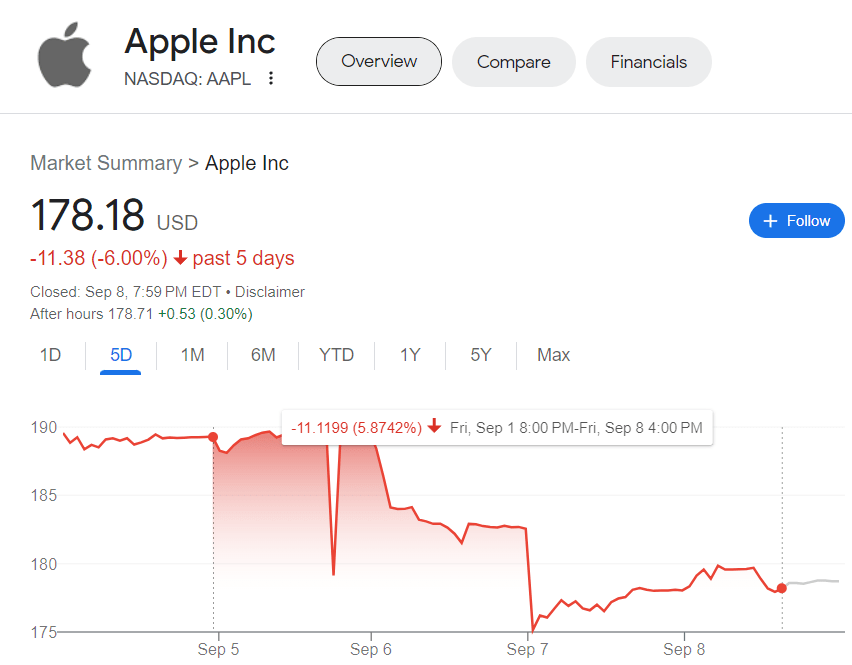

Ahead of its much-awaited iPhone 15 launch event, Apple lost $200 billion in market capitalization last week on news of China banning iPhone use for government and state agency employees.

While financial damage from this move is unlikely to rock Apple’s boat, the Chinese government’s actions open up the possibility of a blanket ban down the road.

In relation to China, Huawei is making a comeback with the Mate 60 series. And Huawei’s re-emergence coupled with government actions look set to hurt the iPhone 15 upgrade cycle.

The China news is a warning shot, and Apple is now firmly caught between the line of fire in the US-China trade war. However, Apple’s China woes maybe just the tip of the iceberg.

Apple is priced for perfection heading into a potential recession (consumer spending slump), and the risk/reward in AAPL stock is skewed to the downside.

Firn

Introduction

Apple (NASDAQ:AAPL) is all set to launch the “iPhone 15” today [12th September 2023], and investors have a lot of expectations from this upcoming upgrade cycle with Apple stock priced at ~30x forward P/E despite showing negative sales growth throughout 2023.

In my previous note – Apple Stock Is Overloved And Overvalued, I reviewed Apple’s latest quarterly earnings report and re-iterated our bearish stance on the tech giant’s stock with the following rationale:

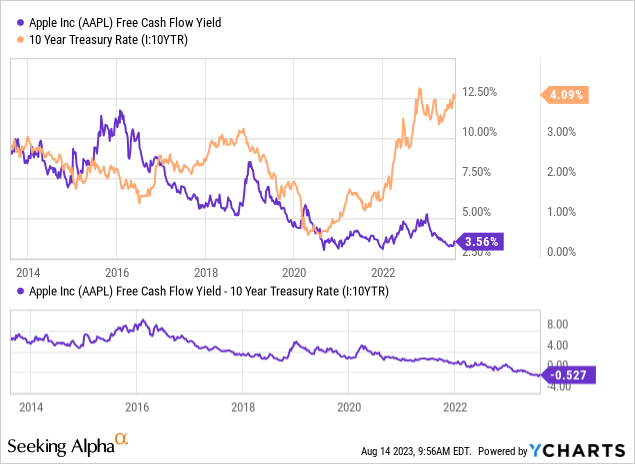

With the recent move in long-duration yields, the 10-yr US treasury yield now sits close to October-2022 highs of ~4.25%. And since my last update on AAPL, Apple’s equity risk premium [the spread between Apple’s free cash flow yield and 10-yr US treasury yield] has gotten even more negative. Under immutable laws of money, equity risk premium must be positive, and this is why, I think Apple’s current valuation is unsustainable

YCharts

Furthermore, the full effects of the Fed’s aggressive monetary policy tightening haven’t been realized yet (nor are the effects of bank credit tightening being instigated by the regional banking crisis). Hence, the macro environment for Apple remains uncertain, and its financial performance could get even worse in upcoming quarters. Given the sheer lack of an equity risk premium, I think Apple stock is likely to get de-rated at some point. At this moment in time, the market narrative is being dominated by AI talk (and hype to some level); however, financial realities (macro and valuations) still do matter, and a day of reckoning is coming for AAPL stock as it remains overloved and overvalued.

Apple’s China Risk Comes To The Fore Ahead Of iPhone 15 Launch

While the financial impact of this particular iPhone ban is likely to be very limited, it is clearly a warning shot from the Chinese government. The US-China trade war has been going on for quite a while now, but this is the first time that Apple has gotten caught in the line of fire. At this point, a broader blanket ban on Apple in China looks unlikely, but it cannot be ruled out as a potential outcome of the ongoing tit-for-tat bans and curbs between the US and China.

Apple generates ~20% of its total revenue from China, which also happens to be a key growth market for the Cupertino tech giant. Over the last few years, Apple has been winning a ton of market share from Huawei in China after US sanctions on the Chinese telecommunication giant left it uncompetitive. However, Huawei has recently launched a new flagship device – “Mate 60”, and this $900 device seems like a genuine competitor for the iPhone.

Bulls like Wedbush’s Dan Ives have quickly brushed off these potential China headwinds –

We believe China news is way overblown as we estimate ~500k iPhones the max impact we see from govt ban worries. For context we forecast 45 mm iPhones to be sold in China the coming year. Apple a top employer (factoring in Foxconn/supply chain) in China… bark worse than bite

Seen bearishness and Black Swan “this could be the moment” around Apple/China worries for the last decade and this time no different in my view. Not saying it’s roses/champagne backdrop in China BUT Huawei phone will be work phone for some govt workers-iPhone the everyday one

However, other Wall Street analysts have predicted a hit as large as 5-20M iPhone units due to China’s ban and Huawei’s new flagship device. Here’s what Bank of America analysts wrote in a note –

China accounts for roughly 40-50 million iPhone units for Apple. We estimate up to a 5 million to 10 million-unit headwind if such a ban were to go through and subsequently be enforced.

While the Chinese consumer’s love for Apple products is probably as strong as ever, the Chinese government and Huawei could prove to be party poopers this time around in relation to Apple’s iPhone 15 upgrade cycle in China. The full adverse impact of these emerging headwinds will only be clear in due time; however, these developments are clearly an additional negative for Apple.

Apple’s China Woes Are Just The Tip Of The Iceberg, US Consumer Fragility Is An Even Bigger Problem

Apple is a fantastic consumer products and services company, and there’s absolutely no doubt about the moat of its ecosystem. However, despite Apple’s revenue mix shifting towards its higher-margin services segment over the last few years; Apple is still significantly reliant on the success of its hardware devices with ~75% of its revenue still coming from hardware sales (>50% from iPhone alone).

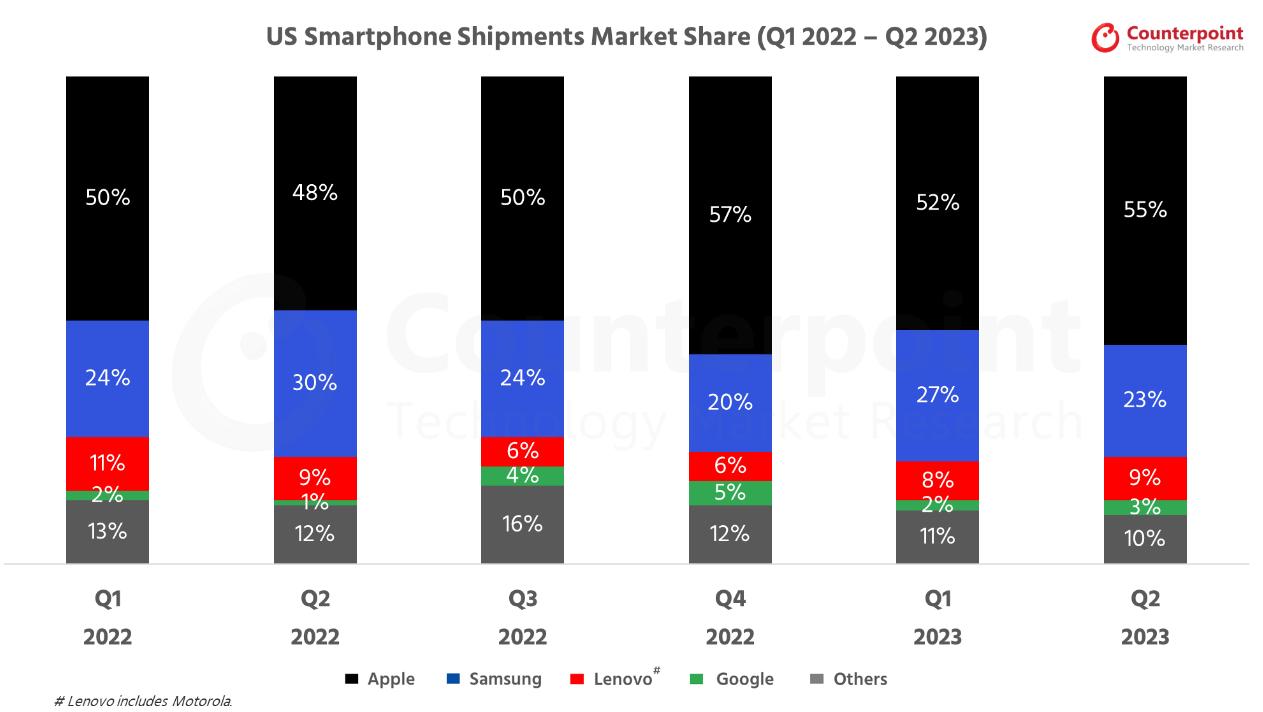

While its China woes are problematic, I see an even bigger issue brewing in Apple’s domestic market. In the US, smartphone shipments declined by -24% y/y in Q2 2023. So far, the bulk of the pain has been limited to the low-end smartphone market, which has propelled the Apple iPhone’s market share in the US to more than 55% in Q2 2023. Now, Apple is winning market share; however, it is doing so with a decline in iPhone shipments (-6% y/y decline in Q2 2023).

Counterpoint Research

In the low-to-zero interest rate environment of the last fifteen years, we have experienced an incredible credit-fueled consumer spending boom, with Apple emerging as a big beneficiary of this free spending. So far in this cycle, the premium smartphone market has remained resilient; however, with higher interest rates and tighter credit conditions, consumer spending on premium smartphones (and other high-end electronic devices) could start to come under pressure in the coming months.

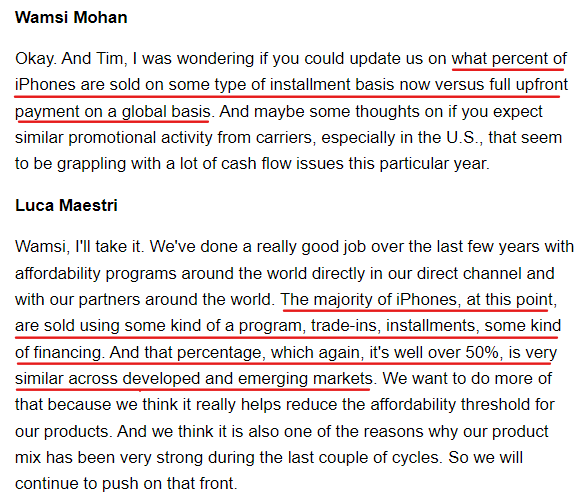

On the back of multiple bank failures in early 2023, a credit crunch is underway, with the FED still raising interest rates and withdrawing billions of dollars from the financial system via QT [quantitative tightening]. According to Apple’s CFO, Luca Maestri, the majority of iPhone sales are sold using some kind of financing:

Apple Q3 2023 Earnings Call Transcript

In the conversation above, Luca did not address the analyst’s request for comment on the expectation of “promotional activity from carriers this year amid their ongoing cash flow issues”, and in my view, lower promotional activity from carriers could have a big impact on the iPhone 15 upgrade cycle. Here’s why:

Only 24% of the iPhones sold in the United States are directly from Apple. The majority are purchased through wireless carriers (67%), such as AT&T, Verizon, and T-Mobile, which now promote iPhone giveaways each year. Retailers like Best Buy (4%) and others (5%) manage to capture some sales over the official Apple Store.

Now, I would like to believe that Apple and its channel partners can sort out pricing and promotions; however, the consumer appetite to participate in the “iPhone 15 upgrade cycle” is likely to be much weaker than in previous cycles. With sticky services inflation still eating into wage growth, and the labor market showing early signs of loosening, discretionary spending on categories like consumer electronics is likely to remain depressed in coming quarters.

At my investing group, I recently highlighted the fragility of the US consumer:

From a layman’s perspective, the US consumer has run out of excess savings, has borrowed to the hilt, and has started falling behind on debt repayments. A tight labor market is probably the only thing holding up consumer spending right now, and even that is showing some cracks.

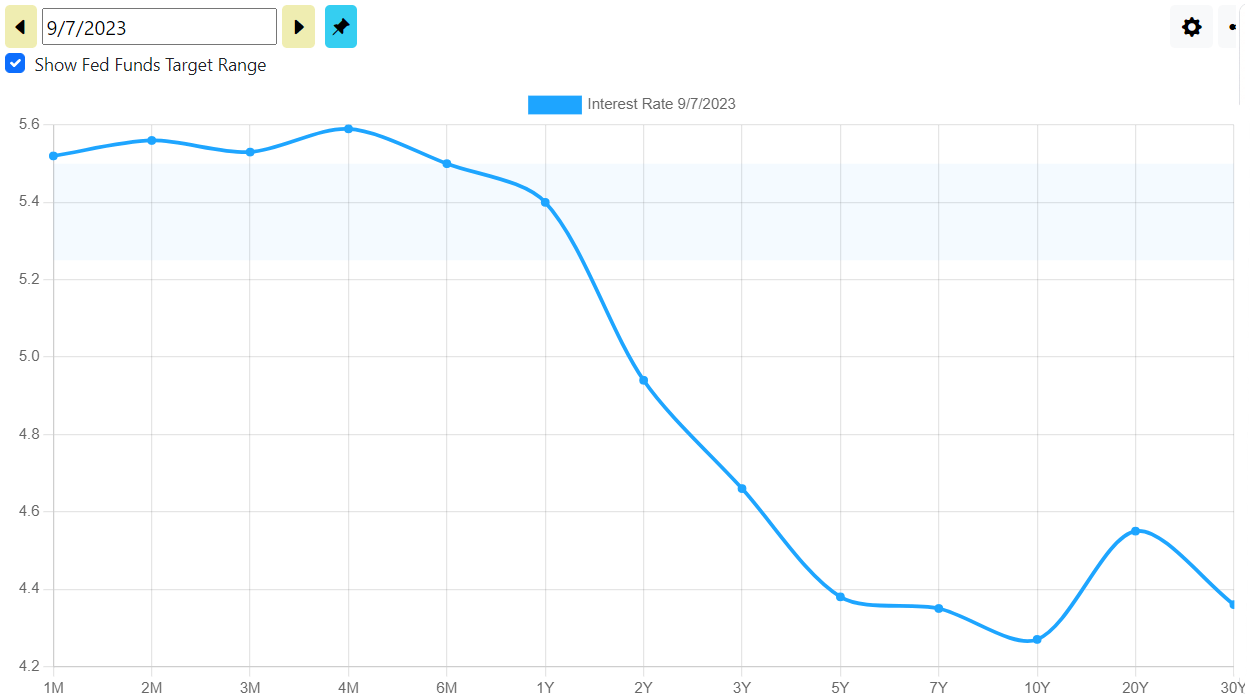

Despite the ongoing bear steepening (long-duration treasury yields moving up faster than short-duration treasury yields to reduce the negative spread), the US treasury yield curve remains inverted, indicating an imminent recession.

ustreasuryyieldcurve

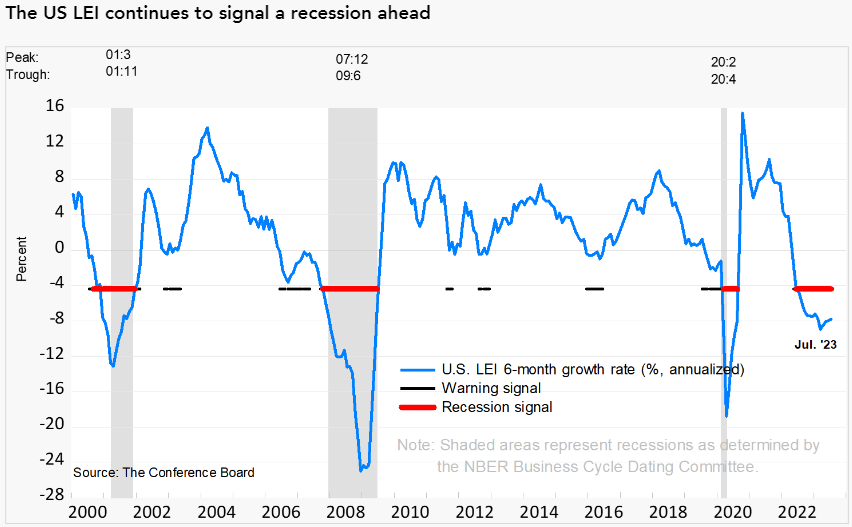

Furthermore, leading economic indicators continue to point toward a recession:

US Leading Economic Indicators (Conference Board)

US Leading Economic Indicators (Conference Board)

While the soft landing narrative has become the consensus in the investing world, every hard landing looked like a soft landing until it didn’t! In my view, the final nail in the coffin for this consumer spending boom could come in the form of a spike in the unemployment rate. We saw a jump in the US Unemployment Rate from 3.5% to 3.8% this month, and while this is just one reading, I think we could be in for a big spike in unemployment over the next 6-12 months. Fifteen years of free money (zero interest rates + QE) has created tons of excesses throughout the economy, and a rapid move in interest rates from 0% to 5%+ is going to break a lot of things in due time. Frankly, another rate hike or two wouldn’t change anything. Given core PCE inflation proving to be sticky at ~4%+, the FED may have to hold rates “higher for longer” (follow through on their indicated policy), hurting consumer demand.

Yes, equity markets can remain detached from economic and financial realities for long periods of time; however, they eventually catch up. Apple’s near-term demand outlook remains uncertain in domestic as well as key foreign markets like China and Europe (the eurozone is struggling with high inflation and low economic growth). As I see it, Apple will continue to struggle for revenue growth in upcoming quarters. At ~30x forward P/E, Apple is priced for perfection, but the business isn’t quite firing on all cylinders in a challenging macro environment. A de-rating of Apple stock is highly likely as a negative risk premium is simply unsustainable.

AAPL Stock: Tryst With Troublesome Technicals

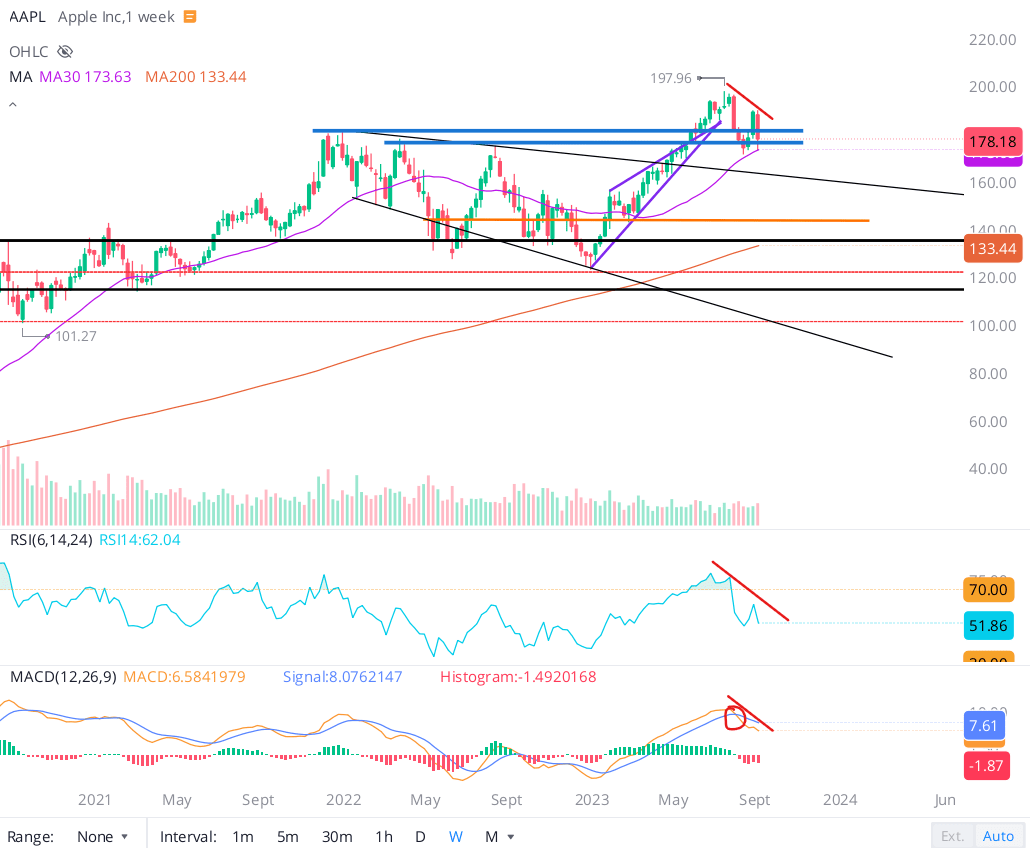

The China headwinds may have triggered last week’s sell-off, but a much deeper pullback is overdue in AAPL stock. From a technical perspective, Apple stock seeing such a sharp rejection from the “golden retracement zone” [61.8% to 78.6% Fibonacci levels] of its recent decline from ~$198 to ~$171 is extremely bearish.

Apple stock chart (WeBull Desktop)

With RSI and MACD indicators on the weekly chart rolling over, Apple stock is losing technical momentum, and I think a much deeper pullback is underway here. The “iPhone 15” event could breathe some life into AAPL stock early next week (delaying the inevitable); however, if Apple suffers a breakdown of the ~$171 level, you should expect to see a further -15-20% near-term move in the stock.

Bottom Line

Ahead of Apple’s big yearly “iPhone” launch event, the risk/reward setup for investors continues to be skewed to the downside. While Apple’s China woes are concerning, this may just be the tip of the iceberg for the Cupertino giant with the US consumer looking fragile heading into a potential recession.

Key Takeaway: I continue to rate Apple’s stock as a tactical “Sell” in the $175-180 range.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are You Prepared For Whatever The Market Throws At Us Next?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

To navigate this highly uncertain macroeconomic environment, we Qvestors [TQI community members] are pursuing bold, active investing with proactive risk management. Join our investing community and take control of your financial future today.